Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

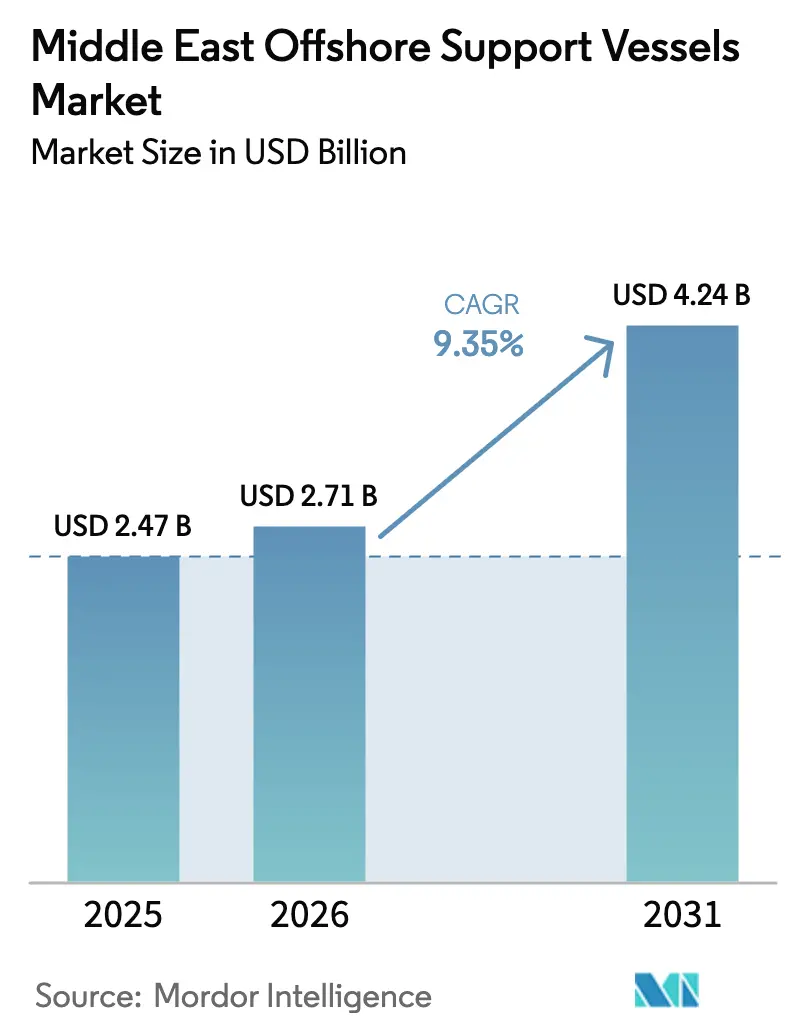

| Base Year Market Size (2025) | USD 2.47 Billion |

| Market Size (2026) | USD 2.71 Billion |

| Market Size (2031) | USD 4.24 Billion |

| Growth Rate (2026 - 2031) | 9.35% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Offshore Support Vessels Market Analysis by Mordor Intelligence

The Middle East Offshore Support Vessels Market size is projected to be USD 2.47 billion in 2025, USD 2.71 billion in 2026, and reach USD 4.24 billion by 2031, growing at a CAGR of 9.35% from 2026 to 2031.

Growth is underpinned by accelerated upstream investment from national oil companies, long-term LNG expansion programs in Qatar and Saudi Arabia, and mandatory fleet renewal to comply with International Maritime Organization Carbon Intensity Indicator rules. Rising gas monetization to meet Asia-Pacific demand is lifting multi-year charter commitments, while localization mandates in Saudi Arabia and the United Arab Emirates are funneling spend toward Gulf-built or Gulf-retrofitted tonnage. Day-rate momentum is evident: Tidewater’s average regional rate rose to USD 20,900 in Q3 2024, up 13% year over year, indicating that tightening supply is translating into pricing power. Counterbalancing forces include Brent volatility and the growing use of dynamically positioned drillships with integrated supply systems, but the net effect remains a positive utilization trajectory for modern, IMO-compliant vessels.

Key Report Takeaways

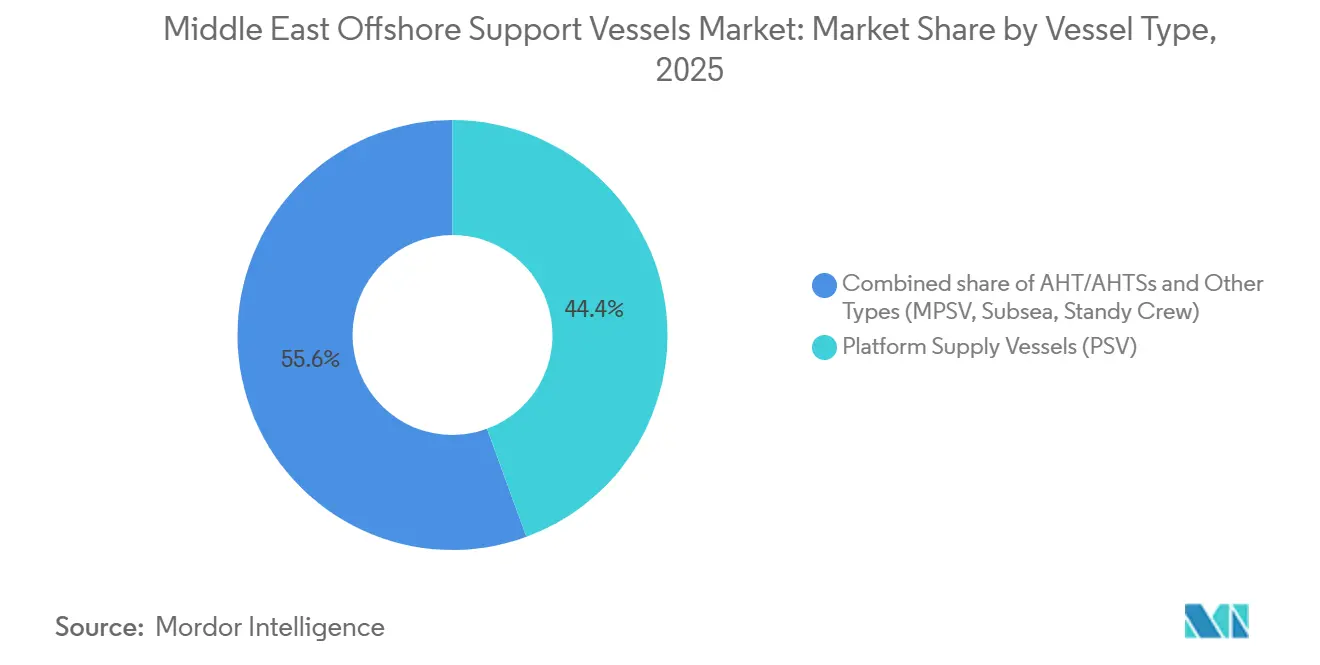

- By vessel type, platform supply vessels led with 44.4% of the Middle East offshore support vessels market share in 2025, while the Other Types category is forecast to expand at an 11.8% CAGR through 2031.

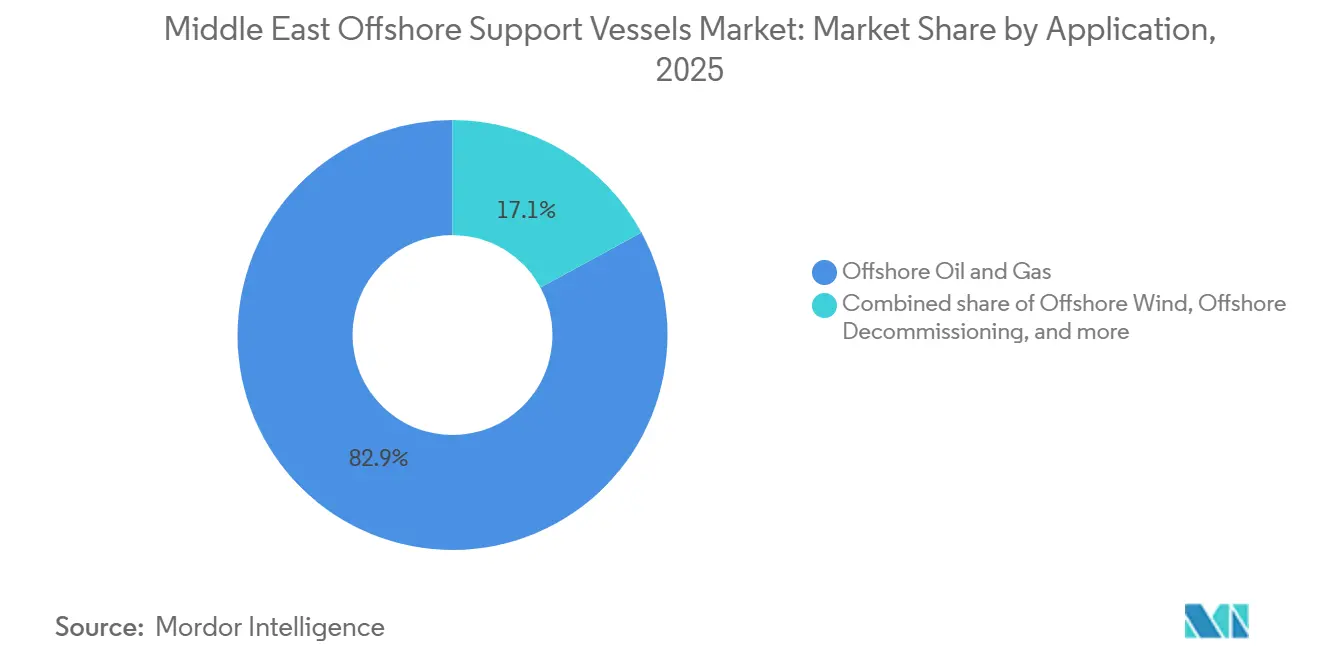

- By application, offshore oil and gas accounted for 82.9% of demand in 2025; offshore wind is projected to advance at a 12.5% CAGR over 2026-2031.

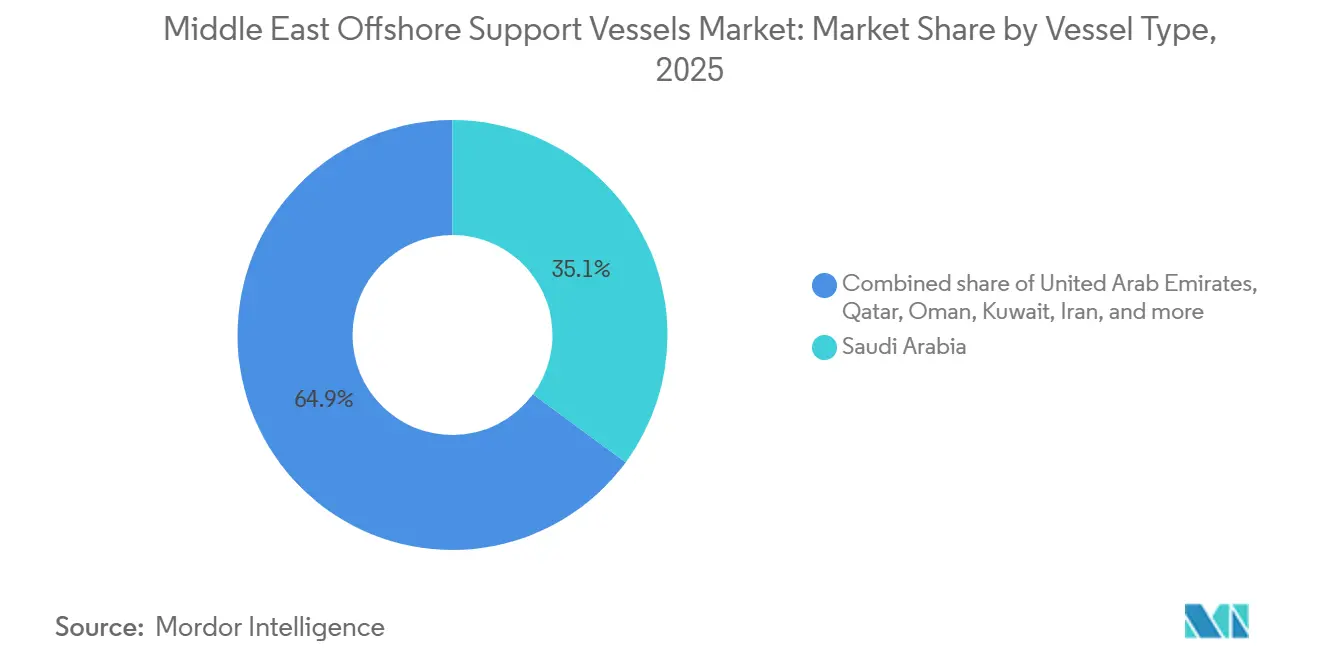

- By geography, Saudi Arabia captured 35.1% of revenue in 2025 and is expected to grow at a 10.2% CAGR, the fastest in the region.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East Offshore Support Vessels Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing offshore E&P spending rebound | +2.8% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Offshore wind farm build-out in Red Sea & Gulf | +1.9% | Saudi Arabia, Egypt (Red Sea corridor) | Long term (≥ 4 years) |

| Fleet renewal to meet IMO CII/EEXI rules | +2.1% | Global, with early adoption in UAE, Saudi Arabia | Short term (≤ 2 years) |

| Localization & in-country-value mandates | +1.6% | Saudi Arabia (IKTVA), UAE (ICV), Qatar, Oman | Medium term (2-4 years) |

| Port & yard capacity upgrades in KSA & UAE | +0.9% | Saudi Arabia (Ras Al Khair), UAE (Jebel Ali) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Offshore E&P Spending Rebound

Saudi Aramco finalized USD 12.4 billion in funding for the Marjan increment, targeting 300,000 bpd by late 2025 and requiring more than 18 PSVs and six anchor-handling tugs across the construction window.[1]Khalid Al-Falih, “Marjan Field Expansion,” aramco.com ADNOC sanctioned the Hail & Ghasha sour-gas project, which needs high-specification subsea construction units for 180 km of pipeline lay.[2]ADNOC Logistics & Services, “ICV Certified Fleet,” adnoc.ae QatarEnergy’s North Field expansion schedules 80-100 dedicated vessels to support drilling and subsea tie-ins through 2027.[3]Saad al-Kaabi, “North Field Expansion,” qatarenergy.qa These commitments reduce spot availability and keep utilization elevated across platform supply and anchor-handling segments. Rising gas demand from Asia strengthens long-term charter tenors, allowing owners to justify hybrid-propulsion retrofits that improve carbon intensity scores. The spending cycle is therefore both a revenue catalyst and a technology-upgrade trigger.

Offshore Wind Farm Build-Out in Red Sea & Gulf

The NEOM Green Hydrogen Company is progressing a 4 GW wind-and-solar complex in the Gulf of Aqaba, with turbine installation slated for 2027.[4]NEOM Company, “Green Hydrogen Project,” neom.com Egypt’s 500 MW Red Sea wind farm follows on a 2028 timeline. Each gigawatt of offshore wind construction typically mobilizes 15-20 specialized support vessels, translating to 60-80 units for NEOM alone. Current regional supply of wind-certified tonnage is under 20 units, prompting PSV retrofits with A-frames and motion-compensated gangways. Certification under DNV or Bureau Veritas standards can take up to 18 months, creating a near-term equipment gap that favors operators able to fast-track modifications in Gulf yards. Long term, wind projects diversify revenue streams and lessen dependence on oil-price cycles.

Fleet Renewal to Meet IMO CII/EEXI Rules

IMO’s Carbon Intensity Indicator grading system became enforceable in 2023 and now obliges corrective action after three consecutive D grades or a single E grade. Energy Efficiency Existing Ship Index limits further tighten installed-power-to-deadweight ratios through 2026. Tidewater disclosed that 18 regional vessels required USD 2.5 million hybrid-propulsion upgrades each to retain CII-B ratings. The retrofit wave is accelerating the scrapping of pre-2010 hulls and driving 30-month new-build lead times at Asian yards. Near-term vessel supply is therefore constrained, supporting day-rate appreciation, while smaller operators lacking capital face exit pressure. Cutting emissions also satisfies procurement rules from national oil companies that increasingly demand Scope 1 reductions.

Localization & In-Country-Value Mandates

Saudi Arabia’s IKTVA program requires 50% local content in energy contracts, compelling foreign owners to partner with domestic entities or establish in-kingdom subsidiaries. ADNOC’s In-Country Value framework imposes similar conditions around Emirati ownership and technology transfer. P&O Maritime Logistics secured UAE certification in 2024 by partnering with Al Seer Marine on 12 vessel retrofits. Zamil Offshore expanded its Dammam yard to capture retrofit demand that counts toward IKTVA scoring. These policies tilt contract awards toward Gulf-flagged or Gulf-refitted fleets, altering ownership patterns and strengthening the local supply chain for equipment and skilled labor.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile oil price outlook | -1.4% | Global, acute in Saudi Arabia, UAE | Short term (≤ 2 years) |

| Surge in DP-rig spot chartering crowds out OSVs | -0.8% | UAE, Qatar, Saudi Arabia | Medium term (2-4 years) |

| Tightening regional carbon-intensity limits | -0.6% | Saudi Arabia, UAE (IMO CII enforcement) | Medium term (2-4 years) |

| Geopolitical choke-point disruptions | -1.1% | Red Sea (Bab al-Mandeb), Strait of Hormuz | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Oil Price Outlook

Brent futures ranged between USD 70-90 per barrel through 2025, hampering budget visibility for exploration programs. Saudi Aramco postponed final investment decisions on three offshore blocks in Q2 2025 amid price swings, directly trimming PSV utilization. Tidewater reports that every USD 10 decline in Brent contracts average charter rates by 6-8% within a quarter. Operators hedge by prioritizing multi-year fixtures with national oil companies, yet spot exposure remains high for smaller fleets. If prices fall below USD 65, cold-stacking and lay-ups could reverse utilization gains achieved since 2023. Conversely, sustained prices above USD 95 would unlock deferred projects, underlining the double-edged nature of volatility.

Surge in DP-Rig Spot Chartering Crowds Out OSVs

Dynamically positioned drillships like Transocean’s Deepwater Asgard can store 3,000 tonnes of mud and cement and receive cargo by helicopter, reducing reliance on PSVs for short-distance resupply. ADNOC awarded four such rig contracts in 2024 with optional helicopter cargo clauses, eliminating an estimated 12-15 PSV voyages per rig per year. The economics are most favorable in shallow-water fields within 50 nautical miles of shore. PSV owners respond by bundling just-in-time delivery software and cargo-tracking to retain value, but margins tighten as the service proposition shifts from tonnage to logistics data. Over the medium term, the rig-integration trend caps PSV demand growth, especially for lower-spec vessels unsuitable for retrofit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vessel Type: PSVs Anchor Market, Specialty Units Gain Share

Platform supply vessels controlled 44.4% of the Middle East offshore support vessels market in 2025, reflecting their versatility in transporting drilling fluids, cement, and tubulars to rigs from Safaniya to Zakum. Hybrid-propulsion upgrades allowed Maersk Supply Service to introduce four DP2-class PSVs that cut fuel use by 20% and meet CII-A targets now required on multi-year Saudi Aramco charters. Anchor-handling tug supply vessels serve deep-water block positioning beyond 1,500 m, but demand is episodic. The Other Types segment, including subsea construction units and crew-transfer boats, will grow fastest at an 11.8% CAGR, propelled by NEOM’s wind timetable and Qatar’s subsea tie-backs. Subsea vessels equipped with remotely operated vehicles are increasingly chartered for pipeline inspection on the Hail & Ghasha project, underscoring specialization as a competitive moat.

Fleet operators are re-evaluating capital allocation as the Middle East offshore support vessels market size for Other Types rises quickly. Bourbon plans USD 3-4 million A-frame retrofits on six PSVs to gain wind-project eligibility. Standby crew boats, though small in revenue terms, enjoy peaks during turbine-installation seasons that require 24-hour personnel shuttle capability. Growth in these specialty categories tilts yard demand toward cranes, gangways, and battery systems rather than pure bollard-pull metrics, signaling a structural shift in specification priorities.

By Application: Oil & Gas Dominates, Wind Segment Emerges

Offshore oil and gas applications generated 82.9% of 2025 revenue, underwritten by Saudi Aramco’s drive to 13 million bpd and QatarEnergy’s LNG output expansion to 126 million t per year by 2027. Vessel-day commitments for drilling, pipelay, and subsea installation keep PSVs and anchor-handlers near full utilization. Yet offshore wind will post the fastest growth at a 12.5% CAGR, catalyzed by NEOM’s 4 GW complex that mandates wind-certified vessels meeting DNV standards. This divergence forces owners to choose between oil-centric charters with steady volumes and wind contracts with higher environmental requirements but longer lead times.

The Middle East offshore support vessels market size for wind support remains small today, but offers margin-accretive pricing due to limited certified supply. Bourbon’s retrofits target this niche, while Zamil Offshore’s Dammam yard now advertises turnkey gangway installations to expedite certification. Offshore decommissioning activity is muted, with fewer than 10 Gulf platforms scheduled for removal through 2031, yet regulators signal stricter end-of-life rules post-2030, hinting at a future uptick in heavy-lift and well-plugging demand.

Geography Analysis

Saudi Arabia captured 35.1% of the Middle East offshore support vessels market in 2025 and is projected to grow at a 10.2% CAGR through 2031. The Marjan and Berri increments combined with NEOM’s offshore wind package sustain long-cycle vessel demand, while IKTVA’s 50% local-content rule channels spend to in-kingdom yards and joint ventures. Ras Al Khair’s USD 1.2 billion port expansion adds four deep-water berths and a 300-tonne mobile crane, reducing repositioning costs by up to 20%

The United Arab Emirates ranks second, anchored by ADNOC’s Hail & Ghasha project that contracts DP2 PSVs and subsea units through 2029. ADNOC Logistics & Services operates 47 vessels and gained In-Country Value certification in 2024 after partnering with Al Seer Marine on hybrid upgrades. Qatar follows, with North Field charters spanning 80-100 vessels, many on five-year terms. Oman is positioning Duqm as a subsea hub, while Kuwait’s Al-Zour refinery spurs localized supply base activity. Bahrain remains niche with under 15 vessels serving the Awali field.

Iran’s fleet modernity lags due to sanctions that limit access to DP systems; twelve new PSVs were built domestically in 2024, but lack CII-compliant engines. The rest of the Middle East contributes less than 8% of regional demand, constrained by geopolitical instability in Iraq and Yemen. Overall, the geographic dispersion underscores that securing local certification is as important as vessel specification for contract success.

Regulatory Landscape

The Middle East OSV operating environment blends global maritime decarbonization requirements with country-specific licensing and energy-operator vetting. IMO Carbon Intensity Indicator (CII) enforcement, effective since 2023, and tightening EEXI-related constraints through 2026 are pushing retrofit and replacement decisions for older PSVs and AHTSs. On the operator side, Saudi Aramco updated its Marine Ports and Terminals rules and regulations in July 2025, while ADNOC Petroleum Ports Authority maintains standards for harbor, wharf, and pier management, adding a further compliance layer alongside flag-state and port-state requirements.

National regulators are also modernizing and tightening enforcement. In Ras Al Khaimah, the Transport Authority issued executive regulations in May 2026 for Law No. 13 of 2023, formalizing licensing, operating requirements, and safety and environmental compliance for marine vessels. Kuwait enacted Decree Law No. 61/2026 in June 2026 to regulate maritime establishments and floating units, introducing requirements such as AIS and providing a stated grace period for compliance. In Saudi Arabia, the Transport General Authority issued a time-bound, 30-day exemption in March 2026 tied to navigation-license document validity for vessels in Arabian Gulf waters, highlighting how short-notice administrative measures can affect mobilization planning and documentation controls for OSV operators.

Competitive Landscape

The market exhibits moderate concentration: the top five operators, Tidewater, ADNOC Logistics & Services, Maersk Supply Service, P&O Maritime Logistics, and Bourbon, control roughly 50% of regional capacity. Tidewater achieved 88% utilization and USD 20,900 average day rates in Q3 2024, illustrating pricing leverage for modern fleets. Localization rules redistribute power toward regional players; Zamil Offshore and Zakher Marine win tenders by offering IKTVA or ICV-ready vessels. Technical differentiation now centers on hybrid-propulsion retrofits, real-time cargo-tracking software, and verified CII-A ratings.

White-space opportunities remain in wind support, where fewer than 20 vessels hold DNV/BV wind certification. Maersk’s DP2 hybrids set a new efficiency benchmark and spur retrofit programs among rivals. Smaller entrants like Al Seer Marine bundle engineering services with equity participation to satisfy local-content scoring, lowering entry barriers for international owners. The competitive narrative is therefore shifting from capacity counts to compliance agility and digital service layers.

Middle East Offshore Support Vessels Industry Leaders

ADNOC Logistics & Services

Tidewater Inc.

Zamil Offshore Services

Maersk Supply Service

Bourbon Corporation SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term opportunity centers on securing multi-year vessel demand linked to large, sanctioned offshore developments and building the contractor ecosystem around them. In the UAE, ADNOC announced a final investment decision for the SARB Deep Gas Development in January 2026, and EPCI activity is visible in awards such as McDermott securing a USD 750 million to USD 1 billion contract for the Nasr-115 expansion, along with contractor selections in June 2026 for packages connected to ADNOC's Upper Zakum expansion program. These programs broaden requirements beyond conventional PSVs and AHTSs into higher-spec subsea support, construction support, and dive support tonnage, creating openings for owners that can deliver DP capability, verified CII performance, and NOC-accepted safety systems.

A second opportunity track comes from localization and compliance-driven fleet renewal, which shifts spending toward Gulf-refitted tonnage and locally certified operations rather than pure spot-market availability. Saudi IKTVA (50% local content) and UAE ICV frameworks, combined with NOC-specific vetting such as ADNOC's Acceptance Standards for Marine Vessels, raise the value of in-country partnerships, regional maintenance capacity, and tighter documentation discipline. Operators with access to retrofit yards and classification pathways, for example Tasneef rules for offshore units effective from April 2025 and updated offshore-unit class rules from bodies such as ABS in 2026, can monetize conversion packages, including hybrid upgrades and mission-equipment additions (A-frames, gangways, ROV systems). This can expand charter eligibility into segments such as offshore wind support and specialized construction support.

Recent Industry Developments

- March 2026: Tidewater reported Q1 2026 results highlighting higher Middle East operating costs tied to elevated insurance and crew-related expenses, while utilization in the region held up better than anticipated. The disclosure underscores how geopolitical and security-linked cost inflation is becoming a central variable in charter pricing and contract terms for OSV owners operating in the Gulf.

- November 2025: Zamil Offshore Services launched the final fast crewboat in a three-vessel aluminium monohull series built by Lita Ocean for operations supporting Saudi Aramco. The delivery adds modern crew-transfer capability and reflects ongoing fleet refresh activity aligned with Saudi Aramco demand and local operating requirements.

- December 2024: ADNOC Logistics and Services expanded its Integrated Logistics business by acquiring 20 offshore assets, including nine offshore support vessels, and secured hire contracts linked to 19 jack-up barge deployments. The acquisition increased controlled capacity and strengthened ADNOC L&S's ability to bundle marine logistics with offshore campaign needs, influencing competitive intensity for regional spot and term charters.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue earned from offshore support vessels operating across Middle East offshore activity, where vessels are chartered to move supplies, support offshore jobs, and keep offshore assets running safely.

Scope exclusions: Onshore marine logistics, inland waterway vessels, and port-only harbor tug services are excluded when they are not tied to offshore field support work.

Segmentation Overview

- By Vessel Type

- Anchor Handling Tug/Anchor Handling Towing Supply Vessels (AHT/AHTSs)

- Platform Supply Vessels (PSV)

- Other Types (MPSV, Subsea, Standy Crew)

- By Application

- Offshore Oil and Gas

- Offshore Wind

- Offshore Decommissioning

- Other Applications

- By Geography

- Saudi Arabia

- United Arab Emirates

- Qatar

- Oman

- Kuwait

- Bahrain

- Iran

- Rest of Middle East

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping the offshore activity base and the vessel supply picture in the Middle East so the model has a real anchor. We used public sources such as OPEC publications, IEA energy outlooks, national statistics portals, and maritime administration releases to understand offshore project momentum, policy signals, and operating constraints.

To convert activity into demand signals, we also reviewed sources such as UN Comtrade trade statistics, port authority updates, safety and marine notices, and peer-reviewed marine engineering papers that discuss OSV utilization patterns and operating costs. Company filings, investor presentations, and reputable press were used to track fleet moves, contract announcements, and day rate direction. In a few places, paid subscriptions that compile company financials, tender activity, and shipment-level trade records were referenced to cross-check timelines and normalize assumptions. The sources listed here are illustrative and not exhaustive, and several other references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions, especially around day rates, vessel utilization, contract length, and the speed of pricing resets after changes in offshore work scopes. We spoke with a mix of vessel owners, chartering and operations teams, offshore project stakeholders, and service coordinators across key Middle East offshore hubs to confirm the practical demand pool and to close data gaps.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | |

| Mid tier: 57% | Functional/Unit leaders: 27% | |

| Smaller Players: 15% | Managers: 59% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach where offshore oil and gas activity, offshore wind work scopes, and decommissioning workloads are translated into an implied vessel demand pool for the region. That demand pool is then expressed in revenue terms using realistic operating days and pricing, and it is corroborated with selective bottom-up checks such as sampled day rate by vessel class, a utilization cross-check, and a limited roll-up of known fleet capacity in active waters.

Key inputs used in the model include the count and intensity of offshore projects, drilling and maintenance cadence, vessel availability by major OSV classes (AHT/AHTS, PSVs, and other support types), day rate progression by contract type, and utilization levels by season and work program timing. We also track cost inflation signals that influence pricing resets, along with country-level offshore spending direction where that link is visible in public plans. Where data is thin for a smaller geography or a niche vessel role, assumptions are filled using the closest comparable offshore hub, then corrected through interview feedback and observed contract patterns.

For forecasting, scenario analysis is used because offshore activity and vessel pricing can shift quickly when project schedules move or when rates are renegotiated. Growth paths are built from expected offshore workload changes, then adjusted based on expert views on how utilization and day rates are likely to respond over the forecast window.

Data Validation & Update Cycle

Outputs are checked against independent signals like fleet availability direction, visible tender flow, and whether implied utilization and day rates look reasonable for each vessel class. If a country-level number looks out of line, the assumptions are revisited, and follow-up calls are triggered to confirm whether the variance is real or a modeling artifact.

Before sign-off, the model goes through multi-step analyst review where inputs, conversions, and currency handling are rechecked, followed by a final sanity pass on growth steps year by year. Reports are refreshed annually, and interim updates are made when material events occur, such as sudden rate changes, major contract awards, or shifts in offshore project timelines. Right before delivery, an analyst performs a fresh review so clients receive the latest updated view.

Mordor Intelligence's Middle East Offshore Support Vessels Market Market Estimate Compared With Other Published Estimates

It is normal to see different market sizes published for offshore support vessels because the scope can shift in small ways, and those small shifts add up fast. The biggest differences usually come from what is counted as OSV revenue, which years are treated as the base, and how day rates and utilization are carried forward.

A refresh-led gap often shows up when one study updates day rates and exchange-rate timing closer to the current contracting cycle, while another keeps older pricing or uses a blended currency assumption that smooths real moves. Charter checks and year-matched currency conversion are the controls used to keep the 2025 number aligned to the current rate environment in the Middle East OSV market, which is why Mordor Intelligence lands at a different level than some other published figures.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.47 B (2025) | |

| Regional Consultancy A | USD 2.85 B (2026) | Uses a later year and a wider OSV boundary that reads closer to offshore vessel services supporting energy installations, and the revenue build can be lifted if higher day rates are applied early without matching utilization realism by vessel class. |

| Industry Publisher B | USD 0.30 B (2024) | Uses a different geography (Middle East and Africa combined) and a much smaller stated value, which suggests the scope may be closer to a narrower sub-segment or a constrained revenue definition rather than the full OSV revenue pool tied to Middle East offshore activity. |

The spread across published numbers is mainly explained by timing and scope choices, followed by how pricing is stepped through the forecast years. By keeping the revenue build tied to observable offshore workload signals and by rechecking day rates and utilization through field feedback, the final estimate stays traceable to clear drivers and repeatable steps.

Key Questions Answered in the Report

How large is the Middle East offshore support vessels market in 2026?

The market is estimated at about USD 2.71 billion in 2026, on a growth path toward USD 4.24 billion by 2031.

Which vessel type holds the largest share?

Platform supply vessels led with 44.4% share in 2025, reflecting their versatility across drilling logistics.

What drives future demand beyond oil and gas?

Offshore wind projects, notably the 4 GW NEOM complex, are accelerating demand for cable-lay and crew-transfer units.

How do localization mandates affect foreign owners?

Saudi IKTVA and UAE ICV rules require joint ventures or local subsidiaries, influencing ownership structures and retrofit decisions.

Are hybrid-propulsion retrofits economically justified?

Yes, because CII compliance avoids charter penalties and supports day-rate premiums that offset retrofit capital within three-five years.

Which country is the fastest-growing regional market?

Saudi Arabia is projected to expand at a 10.2% CAGR through 2031, buoyed by upstream increments and wind investments.

Page last updated on: