South America Data Center Power Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

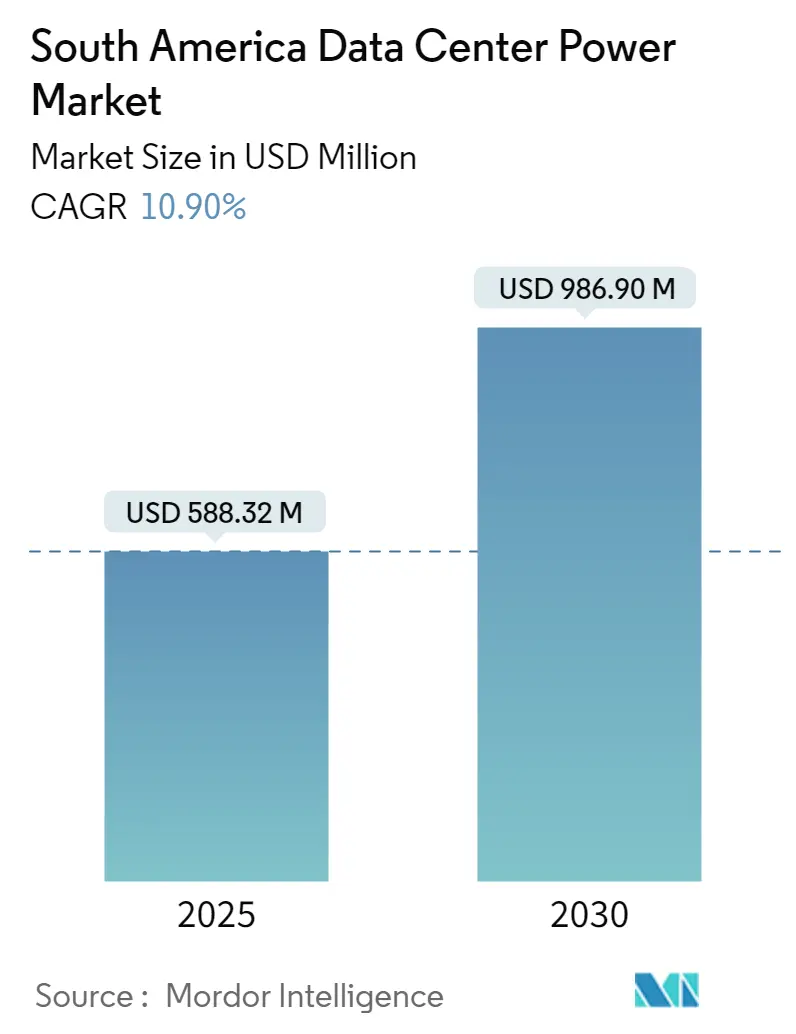

| Market Size (2025) | USD 588.32 Million |

| Market Size (2030) | USD 986.90 Million |

| Growth Rate (2025 - 2030) | 10.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Data Center Power Market Analysis by Mordor Intelligence

The South America data center power market stood at USD 588.32 million in 2025 and is forecast to reach USD 986.90 million by 2030, advancing at a 10.9% CAGR. Hyperscale investment momentum, aggressive renewable-energy procurement, and policy-driven digitalization across Brazil, Chile, Colombia, and Argentina keep demand for resilient power architectures high. AI training clusters and latency-sensitive cloud workloads are lifting average rack densities, accelerating the shift toward liquid cooling, medium-voltage switchgear, and battery energy storage. Renewable power purchase agreements are trimming operating costs, while local data-sovereignty mandates are pushing global providers to build in-region capacity. However, chronic grid instability outside tier-1 metros and rising capex for transformers and switchgear continue to influence site selection and capital budgeting.

Key Report Takeaways

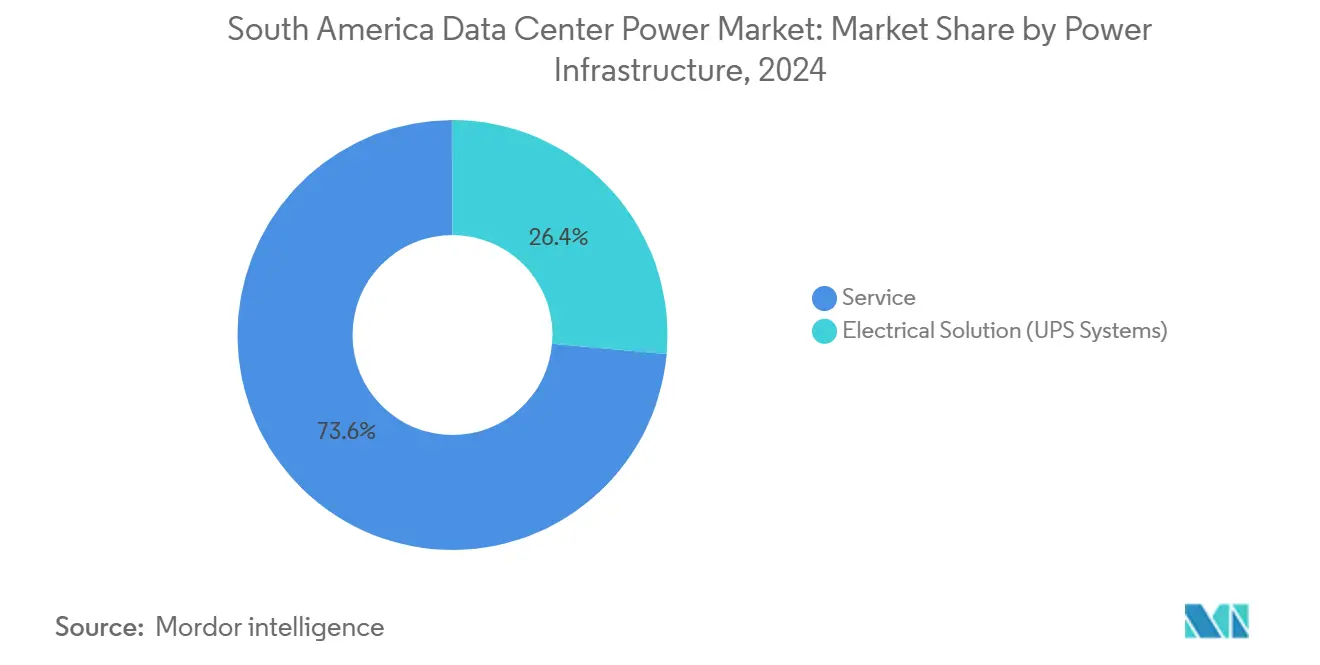

- By component, UPS systems led with 26.4% revenue share in 2024, while power distribution units registered the fastest 13.2% CAGR through 2030.

- By data-center type, colocation providers held 62.3% of the South America data center power market share in 2024; hyperscale/cloud service providers are expanding at a 14.5% CAGR to 2030.

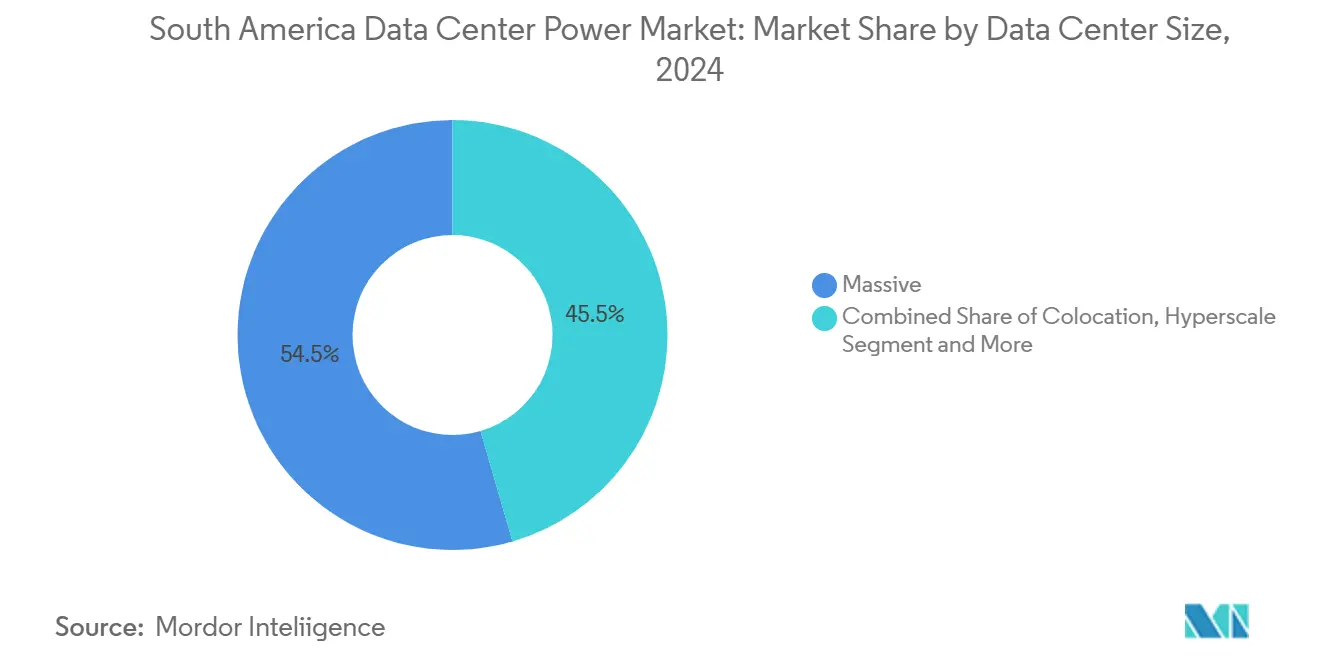

- By power-capacity range, massive facilities (>15 MW) accounted for 54.5% of the South America data center power market size in 2024 and mega facilities (5–15 MW) are projected to advance at 12.5% CAGR through 2030.

- By tier, Tier 3 deployments represented 51.2% of 2024 revenue, whereas Tier 4 configurations are growing at a 14.2% CAGR.

- ABB, Schneider Electric, Vertiv, Eaton, Scala Data Centers, and Ascenty together supplied slightly more than half of total installed UPS and switchgear capacity in 2024.

South America Data Center Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of mega data centers and cloud computing | +2.8% | Brazil, Chile, Colombia core markets | Medium term (2-4 years) |

| Surging AI/ML workloads driving high-density power demand | +3.2% | Brazil dominance, Chile secondary | Long term (≥ 4 years) |

| Accelerated renewable-energy PPAs to cut OPEX and carbon taxes | +1.9% | Chile, Brazil renewable corridors | Medium term (2-4 years) |

| Grid modernisation programmes (Brazil Proinfra, Chile PMGD) | +1.4% | Brazil national, Chile regional focus | Long term (≥ 4 years) |

| Hyperscaler localisation mandates (LGPD, Chile Ley de Datos) | +1.1% | Brazil LGPD compliance, Chile data sovereignty | Short term (≤ 2 years) |

| Battery-energy-storage integration improves uptime economics | +0.8% | Brazil grid-tied, Argentina backup focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Mega Data Centers and Cloud Computing

Mega data centers exceeding 50 MW have become the preferred format for hyperscale operators. Scala Data Centers broke ground on a 54 MW campus in Eldorado do Sul that is anchored on a 100% renewable supply contract and a dedicated 560 MW substation Scala Data Centers. Patria’s USD 1 billion platform and Microsoft’s USD 2.4 billion expansion signal institutional confidence in scale economics, pushing developers toward medium-voltage switchgear, redundant UPS blocks, and on-site substations that can be replicated across the region. Higher density and consolidated loads are improving power-usage effectiveness and trimming land and staffing costs, but they are raising the bar on utility interconnection, fault tolerance, and sustainability reporting.

Surging AI/ML Workloads Driving High-Density Power Demand

AI training clusters consume up to six times the power of legacy racks, pushing densities toward 70 kW and obliging operators to overhaul electrical paths from transformer to server node.[1]Vertiv, “Investor Presentation Q1 2024,” vertiv.com Liquid cooling and direct-to-chip technologies cut thermal loads by as much as 40%, but they necessitate redundant pumps, higher-capacity branch circuits, and low-impedance busbars. Argentina is marketing Patagonia’s nuclear generation to anchor GPU campuses whose continuous power draw can exceed 500 MW per site.[2] Rest of World, “Argentina’s Nuclear-Powered AI Data Center Pitch,” restofworld.org Immediate design revisions across Brazil and Chile are therefore centered on medium-voltage gear that can support dense, low-latency AI zones, underscoring the fastest-growing equipment budgets in the South America data center power market.

Accelerated Renewable-Energy PPAs to Cut OPEX and Carbon Taxes

Operators shift from spot electricity to captive wind and solar contracts that hedge price volatility and satisfy carbon rules. In 2025, Scala Data Centers signed a 900 MW wind PPA ensuring fixed tariffs for 20 years, insulating OPEX and exporting excess power to the grid during non-critical loads. Chile’s portfolio of distributed solar projects above 3 GW lets colocation providers lock in sub-USD 40/MWh pricing, while battery energy storage systems assure dispatchable power for up to four hours.[3] Rest of World, “Argentina’s Nuclear-Powered AI Data Center Pitch,” restofworld.org This PPA momentum guides site selection: proximity to renewable corridors now ranks alongside fiber access when allocating capital inside the South America data center power market.

Grid Modernisation Programmes (Brazil Proinfra, Chile PMGD)

Brazil’s Proinfra roadmap mandates optical ground wire on new transmission lines, enabling integrated telecoms and quicker outage detection. Chile’s PMGD scheme offers incentives for distributed generation up to 9 MW, creating pockets of embedded solar that reduce feeder congestion near Santiago. While both programmes strengthen long-term reliability, they highlight short-term weaknesses. Brazil’s 2024 blackouts affected 3.1 million properties, forcing colocation operators to run diesel generators for extended periods. As a response, data-center owners are installing dual feeds from separate substations, synchronised transfer switches, and island-mode battery systems that can sustain the full IT load for several minutes until backup engines stabilise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex for switchgear and medium-voltage interconnects | -1.8% | Brazil, Argentina cost-sensitive markets | Short term (≤ 2 years) |

| Chronic grid instability outside tier-1 metros | -2.1% | Colombia, Argentina secondary cities | Medium term (2-4 years) |

| Slow permitting for on-site renewables and gas gensets | -1.2% | Brazil regulatory bottlenecks, Chile environmental approvals | Long term (≥ 4 years) |

| Rising social push-back on energy-water footprint | -0.7% | Brazil water-stressed regions, Chile environmental concerns | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex for Switchgear and Medium-Voltage Interconnects

Eaton’s USD 340 million transformer plant underscores supply shortages and steep pricing for core electrical components. Project timelines now factor in 12-month lead times for medium-voltage switchgear, with spot prices inflating by double digits since 2023. Smaller operators in Argentina and secondary Brazilian cities face stretched payback periods because redundant switchgear and automatic transfer systems can equal one-third of total capex. Some developers split projects into phased 5 MW blocks to ease cash flow, but this approach introduces complexity in future upgrades and raises total lifecycle cost.

Chronic Grid Instability Outside Tier-1 Metros

Brazil’s national grid operator forecasts a 50% rise in distributed generation by 2029, risking local overloading and voltage deviations. Severe storms in 2024 damaged transmission lines in Rio Grande do Sul and São Paulo, leading to rolling outages that lasted several hours. Operators responded by oversizing diesel reserves, installing battery energy storage for ride-through, and exploring microgrid designs that combine solar PV with lithium-ion packs. These measures improve resilience but add upfront cost and complicate compliance with environmental licensing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Infrastructure: UPS Systems Hold the Revenue Lead

UPS platforms captured 26.4% of the South America data center power market in 2024, underscoring their status as the core safeguard against grid disruptions. Power distribution units, however, register the fastest 13.2% CAGR as AI clusters necessitate branch-circuit monitoring and load balancing at scale. Switchgear demand also rises but faces procurement delays, prompting operators to pre-order two years ahead of commissioning schedules. Liquid-cooled busways and high-capacity lithium-ion battery strings reconfigure traditional topologies, ensuring that integrated solutions eclipse standalone component sales through 2030.

Service revenues amplify because operators need advisory and maintenance expertise to mesh UPS, battery storage, and renewable interfaces. As a result, vendors offering end-to-end power chains command higher wallet share than point-product suppliers. The South America data center power market size attributable to services is projected to accelerate faster than equipment as regulatory regimes impose stringent uptime and efficiency metrics.

By End User: IT and Telecom Set the Pace

IT and telecom operators anchor more than half of current megawatt off-take, reflecting accelerated cloud adoption by enterprises pursuing cost agility and data-sovereignty compliance. Financial-services firms are on an aggressive migration path, typified by Banco Itaú’s complete cloud transition roadmap for 2028. Healthcare and life-sciences projects are rising, driven by imaging workloads that require low-latency compute zones within national borders.

Telecommunication carriers expand edge nodes to backhaul 5G traffic locally, yet still colocate core workloads in hyperscale hubs. Their hybrid approach triggers demand for mid-tier power blocks between 3 MW and 10 MW. Collectively, these verticals ensure a resilient revenue pipeline across the South America data center power industry while diversifying risk from any one sector.

By Power Capacity Range: ≥15 MW Builds Surge

Projects exceeding 15 MW register the steepest expansion curve because hyperscalers bundle AI training clusters, storage, and content-delivery caches under the same roof. Facilities within the 5-15 MW band remain attractive to colocation incumbents who value modular up-scaling while controlling capex. Sub-5 MW builds focus on edge proximity and disaster-recovery nodes, and they often rely on prefabricated power pods for speed.

Liquid-cooling adoption tightly correlates with capacity size. Operators above 15 MW are mandating coolant distribution units embedded in the switchgear lineup, while smaller builds retain air cooling until workloads justify retrofits. This divergence shapes purchasing patterns within the South America data center power market size hierarchy.

By Data Center Size: Hyperscale Growth Outpaces Others

Massive data centers held 54.5% share in 2024, but the hyperscale subset posts a 14.5% CAGR, reflecting accelerated regional entry by global cloud firms triggered by Brazil’s LGPD and Chile’s forthcoming data protection statute. Enterprise facilities grow modestly, maintaining on-premises control for latency-sensitive and regulated workloads. Wholesale colocation is positioned between these extremes, luring mid-sized cloud-native businesses seeking flexible expansion paths.

Mega sites blur traditional boundaries by combining wholesale suites with dedicated hyperscale halls. Operators in this bracket often negotiate direct transmission lines to renewable parks, embedding power reliability as a differentiator. Consequently, integrated renewable-plus-storage designs become standard across new blueprints in the South America data center power market.

Geography Analysis

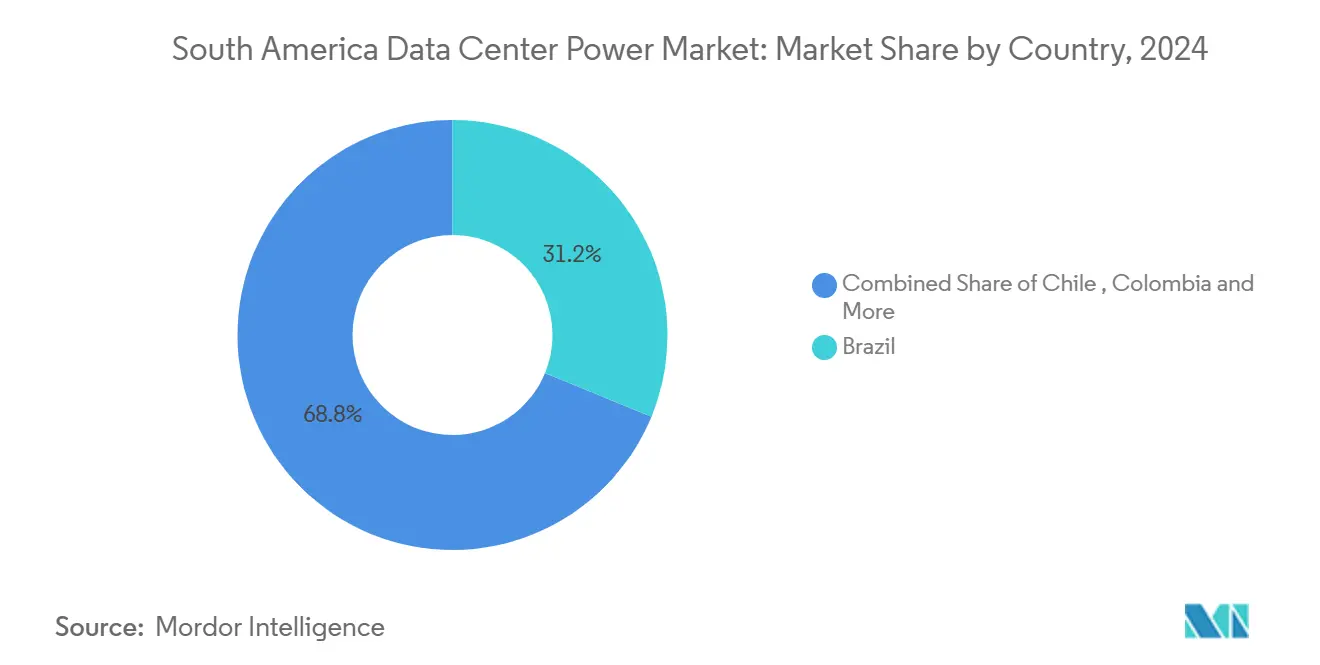

Brazil remains the heavyweight, housing more than 80% of installed IT load and benefitting from an 85% renewable energy mix that delivers competitive electricity tariffs mme.gov.br. The federal government lists 22 new data-center projects that could require up to 9 GW of incremental capacity, spurring utilities to fast-track substation builds around Campinas and Rio Grande do Sul. Microsoft and AWS together committed over USD 4.5 billion to deepen regional footprints, creating a pull-through effect on switchgear, UPS, and battery suppliers. Despite strong fundamentals, transmission congestion around São Paulo prompts developers to scout secondary corridors such as Minas Gerais for grid headroom.

Chile emerges as the fastest-growing node, facilitated by more than 3 GW of distributed solar and a national BESS pipeline above 6 GW energystoragenews.com. Amazon’s USD 4 billion stake underlines confidence in Chile’s data sovereignty law and its streamlined permitting pathway that cuts average build-time by six months. The PMGD framework further enables behind-the-meter solar pairing, reducing exposure to spot-price volatility. Chile’s combination of renewables, regulatory clarity, and submarine-cable proximity positions it as a Pacific gateway for the South America data center power market.

Colombia and Argentina are emerging challengers. Bogotá benefits from a government plan to derive 25% of the power mix from alternatives by 2050, attracting expansion from KIO Data Centers. Argentina courts AI-focused data centers through nuclear baseload offers and investment incentives enshrined in the 2024 RIGI reform, despite currency volatility that elevates import costs for electrical gear. Elsewhere, Peru and Uruguay host smaller builds aimed at serving domestic enterprise demand, but grid inertia and modest market size keep expansion cautious.

Competitive Landscape

Competition in the South America data center power market revolves around technology integration, regional partnership networks, and sustainability credentials. ABB, Schneider Electric, Vertiv, and Eaton collectively supplied more than 50% of UPS kVA added in 2024, leveraging broad portfolios and factory-trained service engineers. Scala Data Centers, Ascenty, V.tal, and Tecto differentiate through campus footprints, renewable-energy sourcing, and locally engineered substation expertise. Equipment makers are deepening alliances with hyperscale operators; Vertiv co-designed a liquid-cooling manifold for Intel’s Gaudi3 accelerator that ships pre-fabricated with matched power shelves, reducing site commissioning time.

Battery-energy-storage vendors such as WEG and Fluence see rising opportunity as Brazilian auctions carve revenue streams for reserve capacity. WEG is investing R$ 100 million in a lithium-pack factory set to open in 2026. In switchgear, Siemens and Mitsubishi Electric are pushing greener SF6-free alternatives, banking on forthcoming environmental regulations. Service portfolios are also expanding; ABB’s purchase of SEAM Group added thermal imaging, arc-flash risk assessments, and digital twinning, elevating its predictive-maintenance proposition for data-center operators supervising mixed fleets of legacy and next-gen equipment.

Regional system integrators compete on fast-track construction and bilingual project teams. Constructora Sudamericana installed a 40 MVA dual-feed substation for a hyperscale client in Santiago within 14 months, demonstrating advantages in navigating local permitting. Meanwhile, global consultancy-engineers remain active in conceptual design but increasingly partner with local EPC firms for execution. Market participants recognise liquid cooling and renewable microgrid integration as the next battlegrounds, with pilot installations already showing 5–10% total energy savings compared with traditional air-cooled, grid-only designs.

South America Data Center Power Industry Leaders

Schneider Electric SE

Vertiv Holdings Co

ABB Ltd

Eaton Corporation plc

Cummins Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Patria launched a data-center platform with an initial USD 1 billion investment, aiming to build multiple Brazilian facilities

- February 2025: Eaton announced USD 340 million for a transformer plant in South Carolina to ease component shortages affecting Latin American builds

- January 2025: V.tal broke ground on a Fortaleza data center as part of a USD 1 billion capex plan

- January 2025: Tecto declared a new 200 MW campus, one of the largest single-facility projects in Brazil

- December 2025: Chile introduced the National Data Centers Plan targeting USD 2.5 billion in new investment.

- September 2025: Scala Data Centers unveiled a USD 50 billion, 4.7 GW campus blueprint in Eldorado do Sul

South America Data Center Power Market Report Scope

Data center power refers to the power infrastructure, including electrical components and electrical distribution systems, which provide the power necessary to operate and support the devices and servers within the data center. It includes various components and technologies designed to ensure a reliable, uninterruptible power supply for data center IT equipment, including uninterruptible power supplies (UPS), power distribution units (PDU), backup generators, and other power management solutions tailored to the specific needs of data centers. Data center operators achieve redundancy through duplicated components to maintain uninterrupted operations in the event of failure of some components and to maintain uptime during maintenance.

The South American data center power market is segmented by power infrastructure (electrical solution (UPS systems, generators, power distribution solutions (PDU, switchgear, critical power distribution, transfer switches, remote power panels, and other solutions)), and service), end user (IT & telecommunication, BFSI, government, media & entertainment, and other end users), and country. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Electrical Solution | UPS Systems | |

| Generators | ||

| Power Distribution Solutions | PDU | |

| Switchgear | ||

| Critical Power Distribution | ||

| Transfer Switches | ||

| Remote Power Panels | ||

| Other Solutions | ||

| Service | ||

| IT and Telecommunication |

| BFSI |

| Government |

| Media and Entertainment |

| Healthcare and Life Sciences |

| Other End Users |

| Less than 1 MW |

| 1–5 MW |

| 5–15 MW |

| Greater than 15 MW |

| Enterprise |

| Colocation / Wholesale |

| Hyperscale |

| Brazil |

| Chile |

| Colombia |

| Argentina |

| Rest of South America |

| By Power Infrastructure | Electrical Solution | UPS Systems | |

| Generators | |||

| Power Distribution Solutions | PDU | ||

| Switchgear | |||

| Critical Power Distribution | |||

| Transfer Switches | |||

| Remote Power Panels | |||

| Other Solutions | |||

| Service | |||

| By End User | IT and Telecommunication | ||

| BFSI | |||

| Government | |||

| Media and Entertainment | |||

| Healthcare and Life Sciences | |||

| Other End Users | |||

| By Power Capacity Range | Less than 1 MW | ||

| 1–5 MW | |||

| 5–15 MW | |||

| Greater than 15 MW | |||

| By Data Center Size | Enterprise | ||

| Colocation / Wholesale | |||

| Hyperscale | |||

| By Country | Brazil | ||

| Chile | |||

| Colombia | |||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the South America data center power market?

The market reached USD 588.32 million in 2025 and is projected to approach USD 986.90 million by 2030.

Which component generates the most revenue?

UPS systems lead with 26.4% revenue share because uninterrupted power remains the primary uptime safeguard.

How fast are hyperscale data centers growing in the region?

Facilities owned by hyperscale and cloud providers are advancing at a 14.5% CAGR, supported by AI workloads and data-sovereignty requirements.

Why are renewable-energy PPAs important for data-center operators?

Long-term PPAs lower electricity cost volatility and help companies meet carbon-reduction targets that are increasingly imposed by regulators and enterprise clients.

What limits expansion outside tier-1 metros?

Chronic grid instability and lengthy lead times for switchgear and transformers make secondary cities riskier, pushing operators to invest in additional backup systems.

Page last updated on: