Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

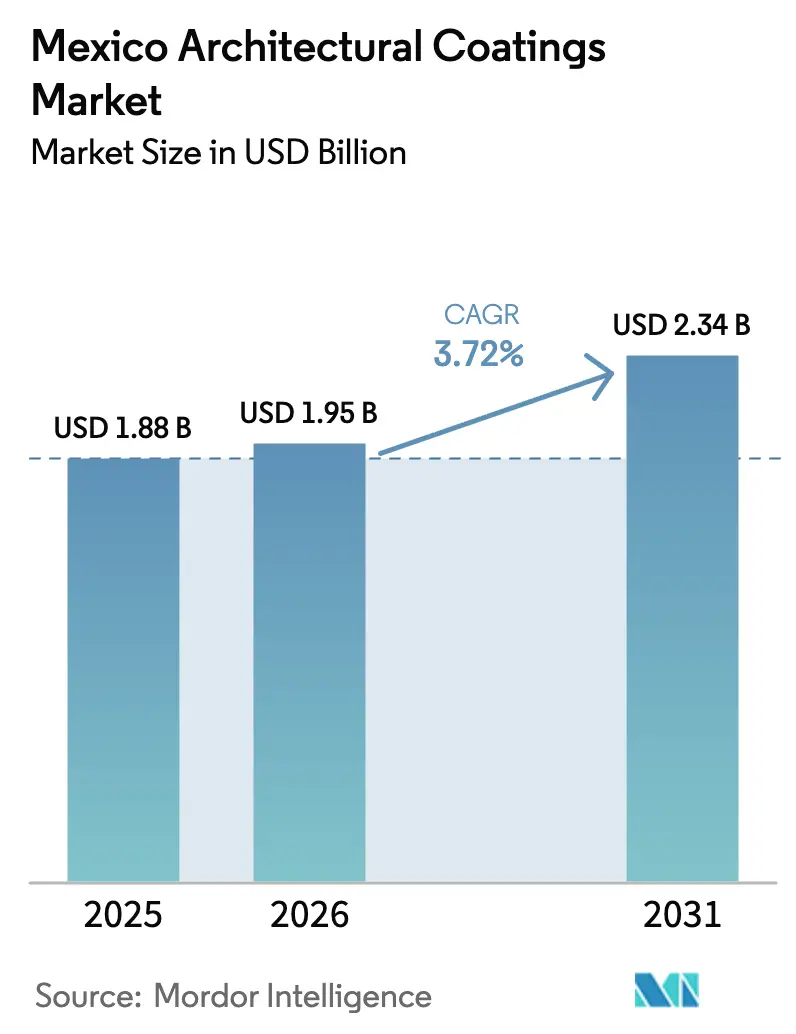

| Base Year Market Size (2025) | USD 1.88 Billion |

| Market Size (2026) | USD 1.95 Billion |

| Market Size (2031) | USD 2.34 Billion |

| Growth Rate (2026 - 2031) | 3.72% CAGR |

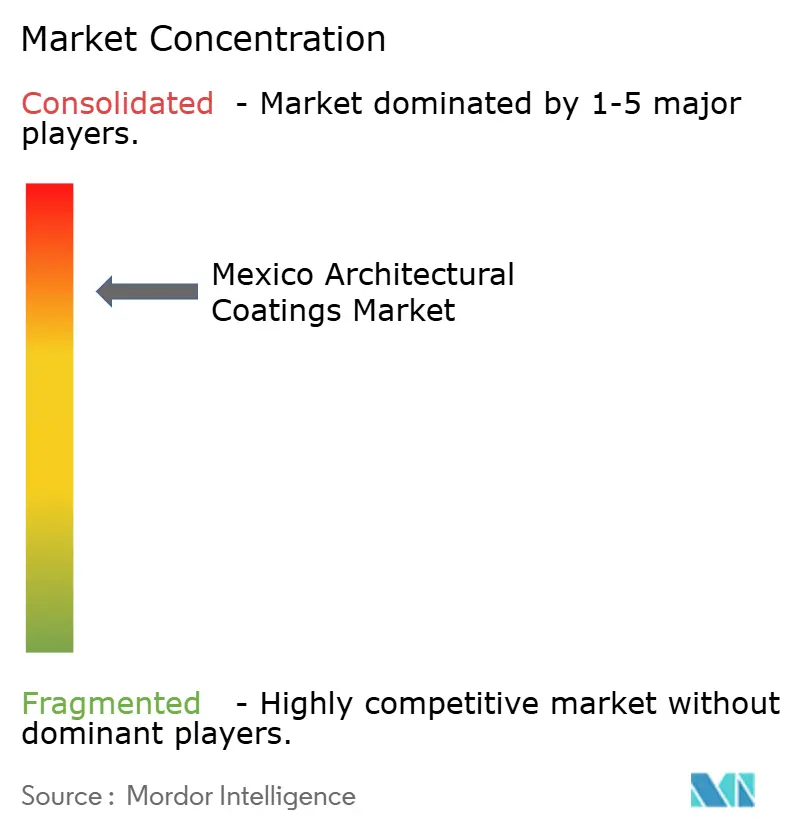

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Architectural Coatings Market Analysis by Mordor Intelligence

The Mexico Architectural Coatings Market size is projected to be USD 1.88 billion in 2025, USD 1.95 billion in 2026, and reach USD 2.34 billion by 2031, growing at a CAGR of 3.72% from 2026 to 2031. The measured growth in the market is driven by a shift toward low-VOC acrylic systems, increased residential demand fueled by near-shoring, and growing competition in online retail. Approximately 400,000 new housing units are planned for 2026, alongside stricter regulations on solvent-borne finishes and rising DIY renovation spending in cities such as Mexico City, Guadalajara, and Monterrey, which continue to boost paint consumption. However, water scarcity in northern states poses challenges for transitioning to water-borne production. In response, manufacturers are expanding capacity in central Mexico, where water supply is more stable. The market also faces pricing pressures from counterfeit imports, which undercut legitimate brands by up to 30% and often exceed the proposed 90 ppm lead limit.

Key Report Takeaways

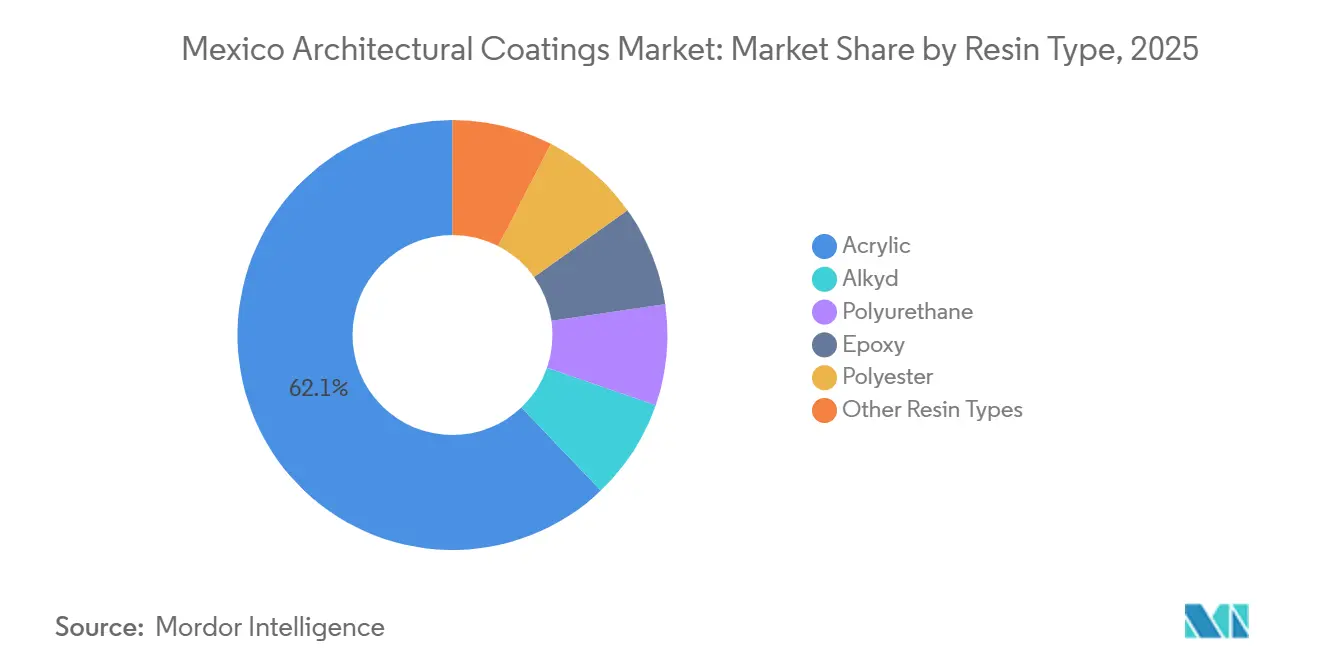

- By resin type, acrylic led with 62.12% of the Mexico architectural coatings market share in 2025 and is projected to grow at a 4.12% CAGR through 2031.

- By technology, water-borne captured 66.13% of the Mexico architectural coatings market share in 2025 and is forecast to register a 4.29% CAGR through 2031.

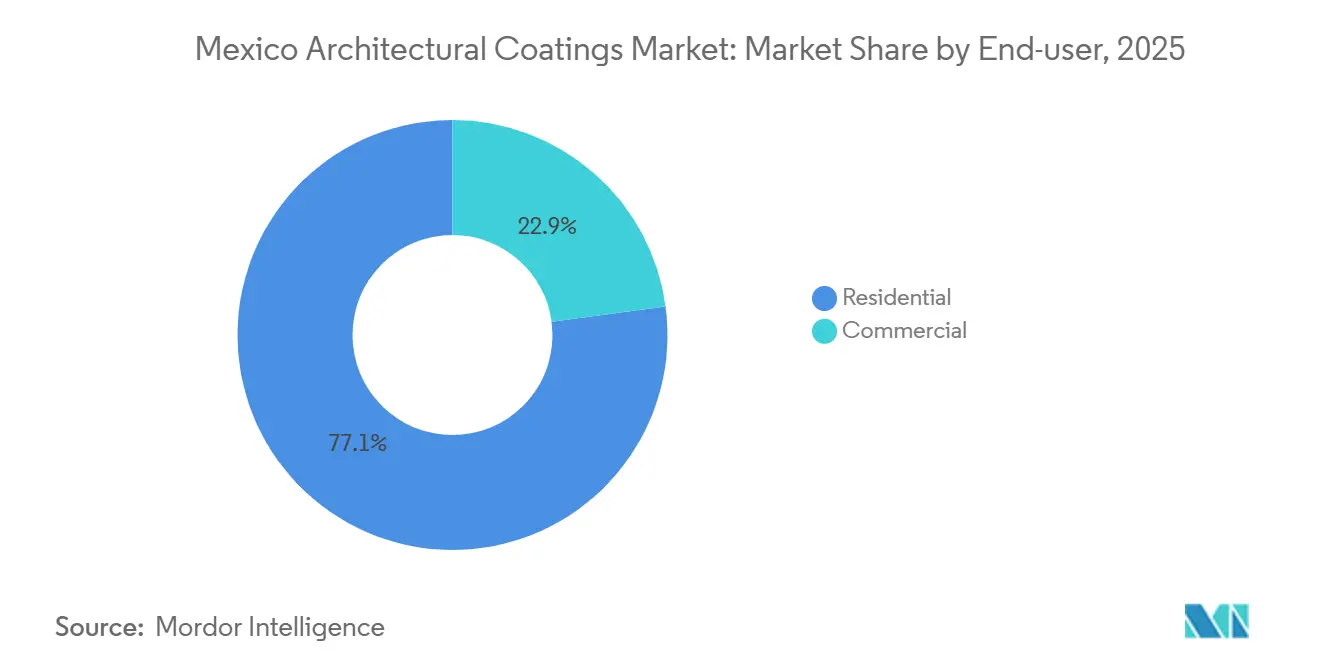

- By end-user, the residential segment commanded 77.12% of the Mexico architectural coatings market share in 2025 and is advancing at a 3.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Architectural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization-led DIY interior renovation surge | +1.2% | National, concentrated in CDMX, Guadalajara, Monterrey metro areas | Medium term (2-4 years) |

| Regulatory pivot toward low-VOC/water-borne systems | +0.9% | National, with enforcement focus in Mexico City (NADF-011-AMBT-2013) | Long term (≥ 4 years) |

| Premiumization via AR color-visualization and e-commerce | +0.6% | National, early adoption in urban centers with high smartphone penetration | Short term (≤ 2 years) |

| Near-shoring-fueled worker-housing demand corridors | +1.4% | Northern states (Nuevo León, Coahuila, Chihuahua), Bajío (Guanajuato, Querétaro) | Medium term (2-4 years) |

| Airbnb-driven micro-renovation cycle in tourist hubs | +0.4% | Quintana Roo (Cancún, Playa del Carmen, Tulum), Jalisco (Puerto Vallarta), CDMX | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urbanization-Led DIY Interior Renovation Surge

By 2025, Mexico's urbanization rate exceeded 81%, concentrating purchasing power in major metropolitan areas. In these regions, households increasingly opt to repaint existing dwellings rather than relocate. Mortgage funding from INFONAVIT and CONAVI, amounting to approximately MXN 70 billion (USD 3.5 billion) annually, supports kitchen, bathroom, and façade renovations, driving demand for quick-drying, low-odor acrylic paints. Home Depot Mexico's augmented-reality mobile app, launched in 2024, enables users to preview 3,500 colors on their smartphones, significantly reducing decision-making time from weeks to hours and boosting sales of higher-margin products. In cities like Mexico City (CDMX), Guadalajara, and Monterrey, where over 75% of adults own smartphones, online paint sales are growing at double-digit rates. Branded players leverage design visualization tools and low-VOC claims to command 40-50% price premiums, even as demand for commodity white paints remains stagnant.

Regulatory Pivot Toward Low-VOC/Water-Borne Systems

Mexico enforces VOC limits through regulations such as NOM-123-SEMARNAT-1998 and NOM-121-SEMARNAT-1997, with Mexico City’s NADF-011-AMBT-2013 imposing stricter caps. Although two federal draft rules on labeling and VOC ceilings were withdrawn in 2024, multinational manufacturers voluntarily adhere to North American standards. For instance, Sherwin-Williams’ Super Kem Tone line features VOC levels below 50 g/L and holds GREENGUARD certification[1]The Sherwin-Williams Company, “Super Kem Tone EPD,” sherwin-williams.com . Similarly, Henkel introduced Fester Acriton Green-Shield Fachadas in 2025, offering a VOC level of 7.5 g/L and a Solar Reflectance Index (SRI) of 110[2]Henkel, “Fester Acriton Green-Shield Fachadas Launch,” henkel.com . The growing preference for sub-50 g/L coatings is driving increased demand for acrylic paints while phasing out high-VOC alkyds, even as regulatory bodies continue to deliberate on new VOC ceiling timelines.

Premiumization via AR Color-Visualization and E-Commerce

Augmented-reality (AR) color visualization tools address the challenge of visualizing room-size finishes from small swatches. Home Depot’s AI-powered app integrates color selection, purchasing, and delivery, empowering consumers and encouraging them to choose premium interior paint lines with features like stain resistance and antimicrobial additives. PPG’s Comex stores have adopted a similar approach, offering custom-tint reservations across their 4,000-store network. Digital retail channels reduce intermediary costs, as seen in Grupo Coppel’s 2024 omnichannel expansion, which links online browsing with in-store pickup at 100 new locations, posing a challenge to smaller distributors. Homeowners are increasingly willing to pay a premium for perfect color matches and low-odor paints that allow same-day occupancy.

Near-Shoring-Fueled Worker-Housing Demand Corridors

USMCA tariff benefits are attracting electronics and automotive manufacturers to regions like Nuevo León, Coahuila, and Chihuahua, leading to large-scale worker-housing developments. Monterrey alone requires 500,000 new housing units, significantly increasing paint demand. However, water scarcity in northern Mexico limits the adoption of water-borne coatings in these areas. To address this, manufacturers are expanding resin production in central Mexico, where water supply is more reliable. For example, PPG invested USD 100 million in 2026 to expand its Tepexpan plant, achieving local resin production autonomy and reducing logistics costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening VOC/PFAS and lead-content compliance costs | -0.7% | National, with stricter enforcement in CDMX and Estado de México | Long term (≥ 4 years) |

| Water-scarcity capex for water-borne lines in arid North | -0.5% | Northern states (Nuevo León, Chihuahua, Coahuila, Sonora) | Medium term (2-4 years) |

| Counterfeit and grey-market paints undercutting premiums | -0.9% | National, concentrated in informal retail channels and border states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening VOC/PFAS and Lead-Content Compliance Costs

Proposals to reduce the lead content ceiling from 600 ppm to 90 ppm are pressuring smaller Mexican brands to replace low-cost leaded pigments with more expensive titanium dioxide, reducing profit margins by up to 12%. Similarly, European Union restrictions on PFAS are prompting global suppliers to phase out fluorinated wetting agents, leading to higher reformulation costs. While multinational companies can distribute research and development expenses across extensive North American portfolios, regional firms face significant costs for testing and recertification, compounded by regulatory uncertainties.

Water-Scarcity Capex for Water-Borne Lines in Arid North

Water-borne technologies require a consistent water supply, but regions like Monterrey, which are key near-shoring hubs, face persistent water scarcity. Investments in closed-loop recycling, wastewater treatment, and humidity control increase capital expenditures by 20-30% compared to solvent-borne production lines, delaying investment decisions. Although state-supported desalination projects are in development, they remain years from completion. As a result, the supply chain is divided: water-borne production is concentrated in regions such as Estado de México, Jalisco, and Querétaro, while solvent-borne production continues in the North despite stricter VOC regulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Dominance Anchored in VOC Compliance

Acrylic resins accounted for 62.12% of the Mexico architectural coatings market in 2025 and are projected to grow at a 4.12% CAGR through 2031. Their superior adhesion to concrete, masonry, and stucco, combined with low-VOC properties, aligns with increasingly stringent regulations. Examples include Sherwin-Williams’ Super Kem Tone line with VOC levels below 50 g/L and Henkel’s SRI-110 Green-Shield at 7.5 g/L, showcasing acrylic's versatility. In contrast, alkyd resins, once favored for their gloss and cost-effectiveness, face challenges due to VOC limits under NOM-123-SEMARNAT-1998, which caps VOC levels at 250 g/L for flat finishes and 380 g/L for gloss finishes, necessitating expensive reformulations. Polyurethanes maintain a niche in hospitality and retail flooring applications, where their abrasion resistance justifies their 50-70% higher costs. Epoxies remain primarily used on industrial substrates due to their brittleness under UV exposure. Arkema’s upcoming 2024 water-borne facility in Queretaro will focus on PVDF-acrylic hybrids, offering 15-20 years of coastal durability and targeting corrosion-prone resort areas.

By Technology: Water-Borne Ascendancy Constrained by Northern Water Scarcity

Water-borne coatings represented 66.13% of the market in 2025 and are expected to grow at a 4.29% CAGR through 2031, driven by green-building standards like LEED, which mandate VOC levels below 50 g/L. PPG’s Tepexpan expansion aims to increase internal water-borne resin production, with the company projecting its share to exceed 75% by 2030. However, adoption is slower in regions like Nuevo León, where water scarcity has led to chemical plant closures, forcing manufacturers to maintain solvent-borne production capacity. Behr’s GREENGUARD-Gold Premium Exterior range, with VOC levels between 17-47 g/L, demonstrates that water-borne coatings can achieve comparable 10-year durability, addressing performance gaps traditionally favoring solvent-based alternatives.

By End-user: Residential Segment Buoyed by Federal Housing Push

The residential segment accounted for 77.12% of the Mexico architectural coatings market in 2025 and is projected to grow at a 3.54% CAGR through 2031. Federal housing initiatives aim to deliver 400,000 homes in 2026, up from 138,645 in 2025, significantly expanding the demand base. Additionally, housing for workers involved in shoring projects further contributes to revenue growth. Monterrey’s requirement for 500,000 housing units amplifies the need for coatings while increasing demand for durable products to reduce repainting cycles. In the commercial segment, demand is driven by big-box retail expansions, including Home Depot’s 12 new outlets and Grupo Coppel’s rollout of 100 omnichannel stores, which emphasize high-washability and low-odor specialty paints.

Geography Analysis

Mexico's coatings production capacity is concentrated in Estado de México and Nuevo León. Estado de México is home to PPG's Tepexpan facility and several small-to-medium-sized plants, benefiting from central logistics and more reliable water access. Nuevo León capitalizes on near-shoring trends but faces challenges from drought conditions, which limit the use of fresh water-borne coatings and extend reliance on solvent-borne alternatives. The Bajío region, including Guanajuato, Querétaro, and San Luis Potosí, benefits from the establishment of new OEM plants and Arkema's investment in solvent-free resin production. In Quintana Roo, the tourism-driven economy supports frequent repainting cycles, favoring high-SRI acrylic coatings that withstand salty and humid conditions. Border states experience higher counterfeit product penetration due to porous trade routes and informal retail channels.

Competitive Landscape

The market demonstrates moderate consolidation, with the top five suppliers, including PPG Industries, Inc., Sherwin-Williams, Pinturas Berel, S.A. de C.V., Pinturas Osel, and Pinturas Acuario, collectively accounting for 80% of the market share. PPG leverages its network of 4,000 branded stores and a newly established USD 100 million resin production line to enhance vertical integration. Sherwin-Williams, after its unsuccessful 2013 bid to acquire Comex, focuses on organic retail expansion and GREENGUARD-certified product lines. Pinturas Berel, with an estimated revenue of approximately MXN 4.5 billion (USD 225 million), faces pressure from the transition to lead-free products. Digital innovations are reshaping market dynamics, with Home Depot's augmented reality (AR) app streamlining consumer decision-making and Grupo Coppel's hybrid model combining online selection with next-day in-store pickup. Counterfeiting continues to undermine brand pricing power, prompting established players to advocate for stricter customs regulations and mandatory product registration.

Mexico Architectural Coatings Industry Leaders

PPG Industries, Inc.

The Sherwin-Williams Company

Pinturas Berel, S.A. de C.V.

Pinturas Osel

Pinturas Acuario

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: PPG Industries, Inc. enhanced its manufacturing capabilities in Mexico by upgrading its Tepexpan facility to produce low-emission, water-borne, and solvent-borne resins. This development supported the architectural coatings market by enabling the production of resins used in these coatings.

- March 2024: WEG announced an investment of BRL 100 million (USD 18.63 million) to establish a new industrial liquid paints factory in Mexico. The facility was designed to enhance WEG Coatings' production capacity, focusing on the North and Central American markets.

Mexico Architectural Coatings Market Report Scope

Architectural coatings are protective and decorative finishes used in residential and commercial buildings to protect surfaces from weathering, UV radiation, and wear. These coatings include paints, primers, sealers, stains, and varnishes applied to walls, roofs, and floors.

The Mexico Architectural Coatings Market is segmented by resin type, technology, and end-user. By resin type, the market is segmented into acrylic, alkyd, polyurethane, epoxy, polyester, and other resin types. By technology, the market is segmented into water-borne and solvent-borne. By end-user, the market is segmented into residential and commercial. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Resin Type

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Other Resin Types |

By Technology

| Water-borne |

| Solvent-borne |

By End-user

| Residential |

| Commercial |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Other Resin Types | |

| By Technology | Water-borne |

| Solvent-borne | |

| By End-user | Residential |

| Commercial |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms