ASEAN Switchgear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

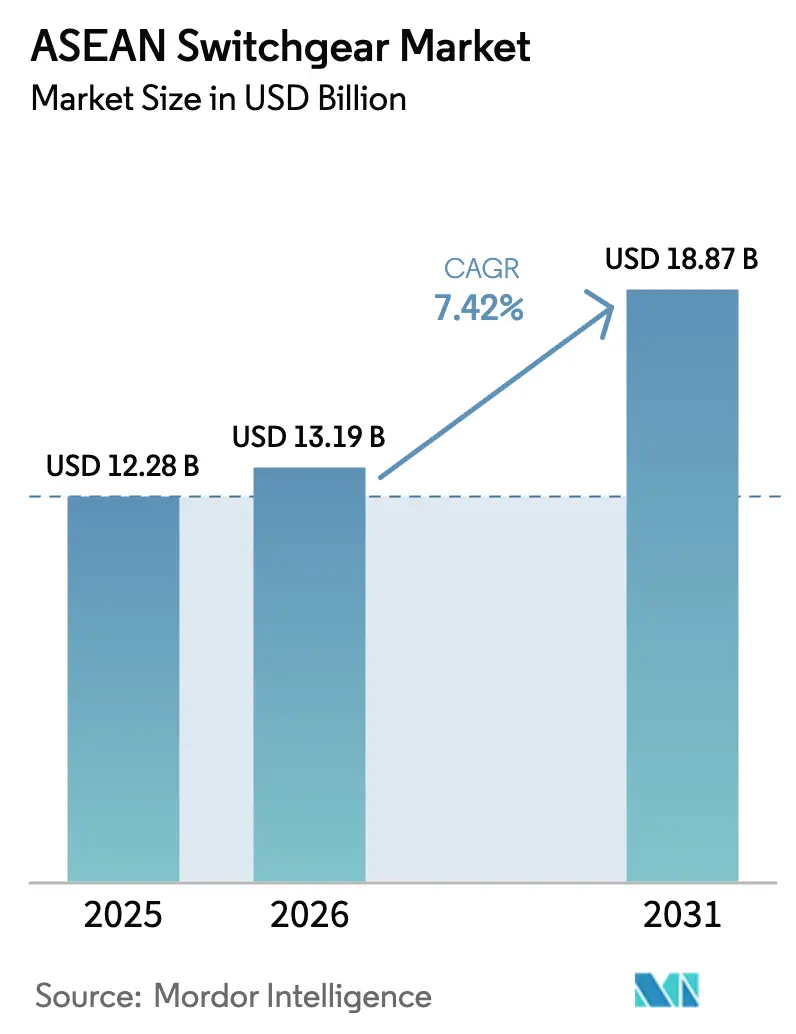

| Base Year Market Size (2025) | USD 12.28 Billion |

| Market Size (2026) | USD 13.19 Billion |

| Market Size (2031) | USD 18.87 Billion |

| Growth Rate (2026 - 2031) | 7.42% CAGR |

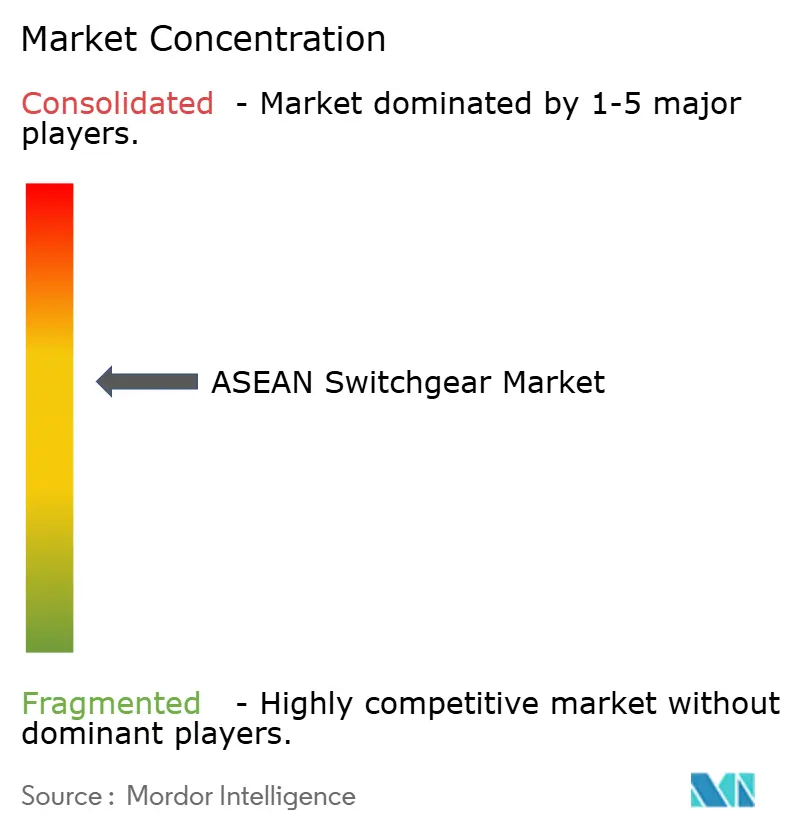

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Switchgear Market Analysis by Mordor Intelligence

The ASEAN Switchgear Market size was valued at USD 12.28 billion in 2025 and estimated to grow from USD 13.19 billion in 2026 to reach USD 18.87 billion by 2031, at a CAGR of 7.42% during the forecast period (2026-2031).

Rising grid modernization budgets, hyperscale data center construction, and industrial electrification programs anchor demand, while commodity price swings and policy uncertainty temper near-term spending cycles. Utilities continue to procure intelligent medium- and high-voltage gear to upgrade substations, whereas commercial builders specify low-voltage solutions that integrate with smart-building platforms. Manufacturers compete on digital functionality, SF₆-free insulation, and local manufacturing footprints that satisfy domestic value-add rules. Cross-border HVDC interconnectors and rail electrification projects amplify the need for specialized outdoor and DC-rated assemblies, positioning the ASEAN switchgear market as a focal point for next-generation power infrastructure.

Key Report Takeaways

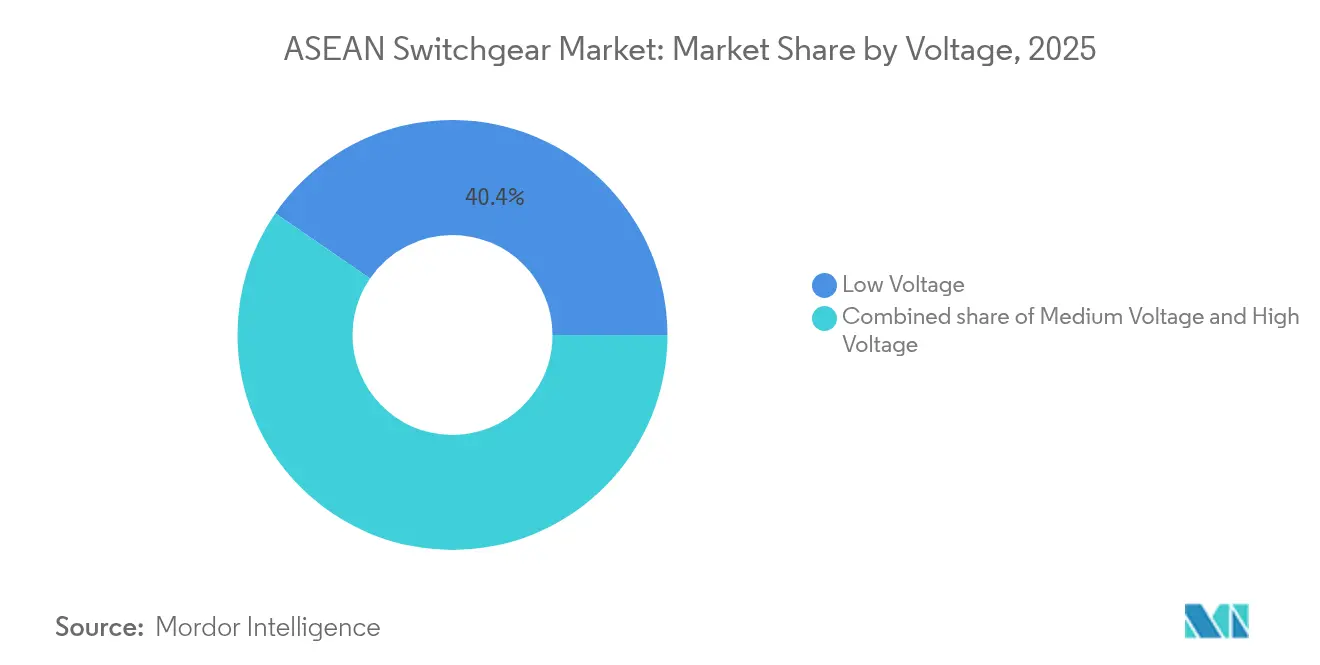

- By voltage class, low-voltage products led with 40.42% revenue share in 2025, while high-voltage products recorded the fastest expansion at a 9.35% CAGR through 2031.

- By insulation type, air-insulated units held 70.95% of the ASEAN switchgear market share in 2025; SF₆-free and hybrid alternatives are projected to grow at a 15.48% CAGR to 2031.

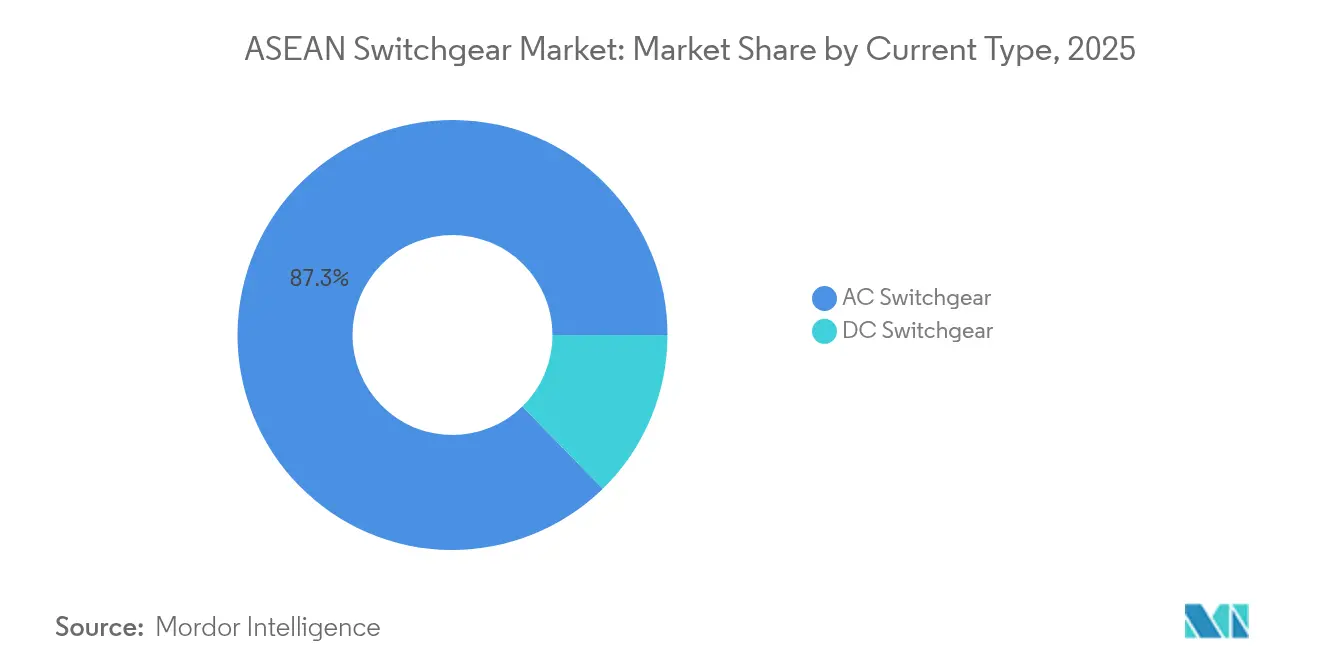

- By current type, AC equipment accounted for 87.32% of the ASEAN switchgear market size in 2025; DC variants are poised to climb at an 8.42% CAGR during 2026-2031.

- By 2025, indoor configurations commanded 80.74% of sales, whereas outdoor systems are expected to expand at a 10.21% CAGR through 2031.

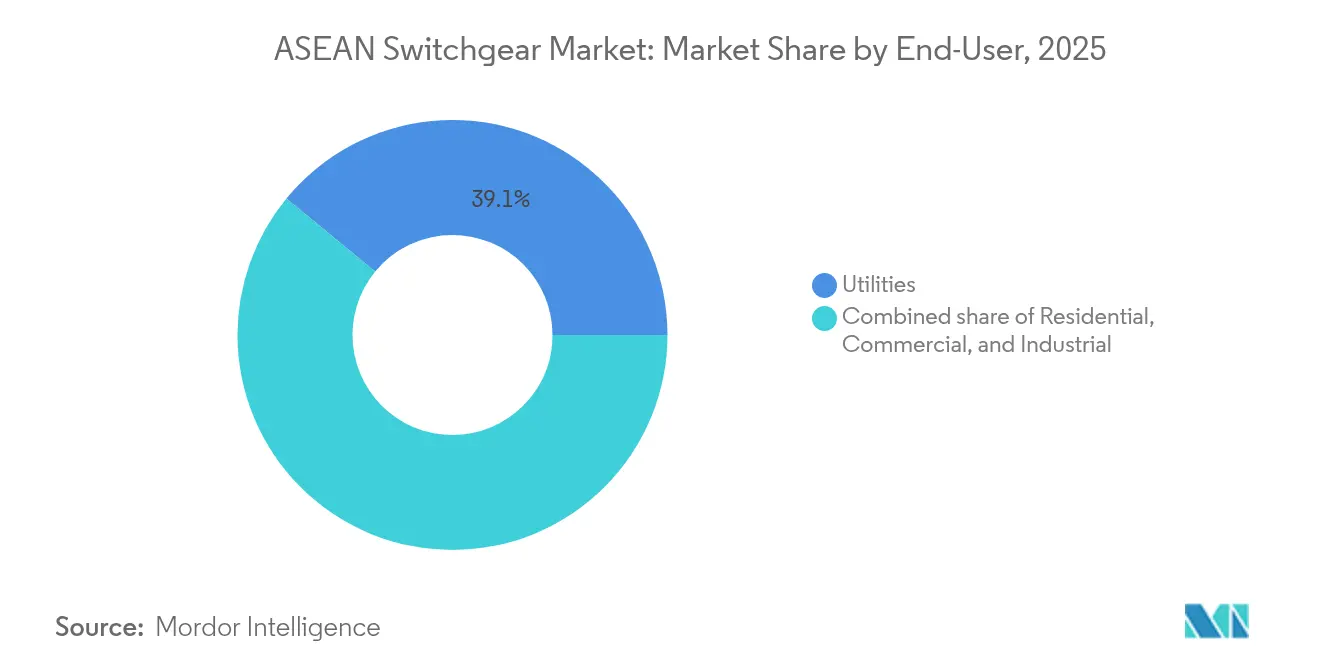

- By end-user, utilities captured 39.05% of 2025 revenues and are projected to grow at an 8.16% CAGR to 2031, driven by USD 764 billion in regional grid investments.

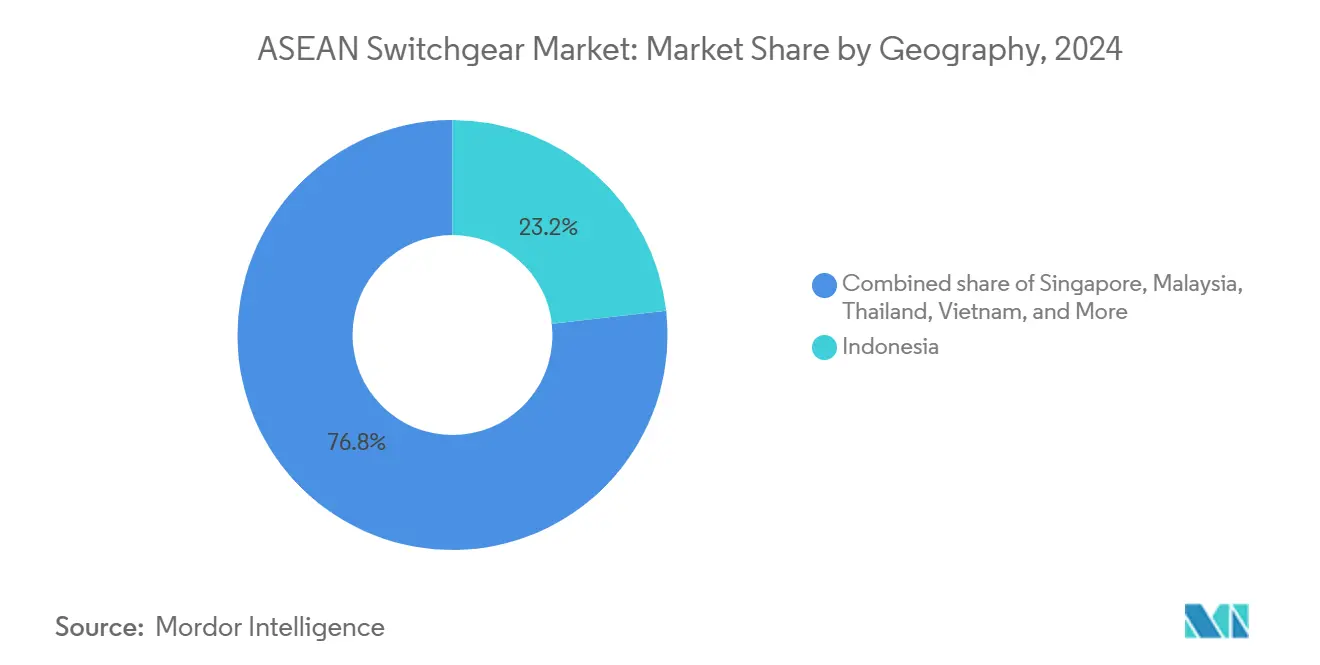

- By geography, Indonesia commanded a 22.85% revenue share in 2025, while Malaysia is forecasted to register the fastest CAGR of 8.12% from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Switchgear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid grid-modernisation & ASEAN Power Grid projects | 2.10% | Indonesia, Malaysia, Thailand core with spillover to Vietnam, Philippines | Medium term (2-4 years) |

| Surging data-centre & AI load densification | 1.80% | Singapore, Malaysia, Indonesia primary with expansion to Thailand | Short term (≤ 2 years) |

| Industrial electrification & urban rail expansion | 1.20% | Indonesia, Vietnam, Thailand manufacturing hubs with urban centers | Medium term (2-4 years) |

| Localised manufacturing of MV/HV switchgear in Indonesia & Vietnam | 0.90% | Indonesia, Vietnam with supply chain effects across ASEAN | Long term (≥ 4 years) |

| Singapore-led SF₆-free procurement mandates | 0.80% | Singapore leading, Malaysia and Thailand following | Medium term (2-4 years) |

| Sub-sea HVDC interconnectors driving extra-high-voltage demand | 0.60% | Singapore-Malaysia-Vietnam corridor with regional grid integration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Grid-Modernization & ASEAN Power Grid Projects

More than USD 764 billion is earmarked for cross-border transmission upgrades, with USD 50 billion already funded for near-term builds that specify 132-500 kV switchgear platforms. Governments are favoring digital control, IEC 61850 compliance, and remote diagnostics to enhance resilience following recent climate-related blackouts. National programs, such as Malaysia’s RM 43 billion (USD 9.7 billion) grid overhaul, embed cybersecurity and condition-monitoring clauses in tenders. Standardization across member states simplifies spares management and enables competitive bidding at scale. Manufacturers offering modular GIS and hybrid switchgear with built-in automation are positioned to capture multi-country frame contracts. Local utilities couple these rollouts with workforce-training grants that accelerate knowledge transfer and shorten commissioning cycles.

Surging Data-Center & AI Load Densification

Data-center capacity exceeding 1,000 MW in Singapore, Malaysia, and Indonesia drives demand for dual-feed, 99.99% availability switchgear designed for 30-50 kW rack densities.[1]Bloomberg News, “Southeast Asia Data-Center Expansion Tops 1 GW,” bloomberg.com AI training clusters impose higher harmonic distortion, compelling buyers to specify low-impedance busbars and active filtering. Hyperscalers favor modular, plug-and-play line-ups that can be installed during live operations, cutting outage windows to less than four milliseconds. Edge-computing nodes expanding across urban cores create incremental orders for compact 4-15 kV units with integrated metering. Suppliers differentiate through digital twins that model load scenarios and predict remaining useful life, helping operators meet stringent service-level agreements.

Industrial Electrification & Urban Rail Expansion

The electrification of automotive, electronics, and food-processing plants in Indonesia, Vietnam, and Thailand is increasing medium-voltage demand, as factories replace fossil-fuel boilers with electric alternatives at an annual adoption rate of over 25%.[2]Schneider Electric, “Industrial Electrification Trends in ASEAN,” se.com Bangkok’s and Jakarta’s rail extensions require 25 kV traction power systems with regenerative-braking-optimized switchgear capable of managing rapid load reversals. Manufacturers integrate SCADA gateways, enabling transit agencies to overlay predictive maintenance across rolling stock and substations. ISO 50001 energy-efficiency mandates encourage factories to deploy switchgear with embedded power-quality meters that feed energy-management dashboards. Combined, these trends prompt OEMs to bundle software analytics with hardware, thereby monetizing their after-sales digital services.

Localised Manufacturing of MV/HV Switchgear in Indonesia & Vietnam

Indonesia’s 40% local-content rule encourages global players, such as ABB and Siemens, to add assembly lines that reduce import duties by up to 15%.[3]Indonesia Ministry of Industry, “Local-Content Regulations for Power Equipment,” kemenperin.go.id Vietnam’s tax holidays and industrial-park incentives reduce lead times from 20 to 12 weeks for standard product sets. Domestic production reduces freight costs, creates seismic-resistant designs tailored to the region, and enhances the availability of spare parts. Technology-transfer partnerships enhance indigenous engineering skills, while cost savings of 15-20% compared to imports enable competitive bids on budget-constrained projects. Localization also supports faster customization for tropical climates, including anti-corrosion coatings and high-humidity insulation clearances.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Up-front capex & long OEM lead-times | -1.50% | Global ASEAN impact with acute effects in Philippines, Myanmar | Short term (≤ 2 years) |

| Copper & aluminium price volatility | -1.10% | Indonesia, Vietnam manufacturing centers with cost pass-through effects | Short term (≤ 2 years) |

| FIT-policy reversals delaying utility budgets | -0.70% | Vietnam primary impact with spillover concerns in Thailand, Philippines | Medium term (2-4 years) |

| Indonesia local-content rules complicating foreign supply | -0.40% | Indonesia focused with supply chain effects across ASEAN | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Up-Front Capex & Long OEM Lead-Times

Specialized 245-500 kV switchgear now ships in 16-24 months, stretching project schedules and inflating interest during construction. Hardware can account for 25% of substation budgets, forcing smaller utilities to stagger installations and accept sub-optimal load flows. Semiconductor shortages limit the availability of digital relays and sensors, further extending delivery windows. Developers increasingly break projects into phases to spread payments, yet this fragmentation of commissioning raises lifecycle costs. Concentrated manufacturing capacity among a few global vendors magnifies the impact of any factory disruption on regional rollout plans.

Copper & Aluminium Price Volatility

Aluminium moved from USD 2,419 per tonne in 2024 to USD 2,635 in 2025, lifting conductor costs that represent up to 35% of a medium-voltage switchgear bill of materials.[4]Economist Intelligence Unit, “Base-Metal Price Forecast 2025,” eiu.com Spot copper trades near USD 9,560 per tonne and exhibits high daily volatility, prompting OEMs to revise their quotes quarterly and pass the risk to buyers. Regional makers lack hedging scale, leading to frequent repricing that challenges project feasibility for public-sector owners with fixed budgets. End-users delay awards when prices spike, resulting in lumpy demand and underutilized factory capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Voltage: High-Voltage Momentum Within Low-Voltage Leadership

Low-voltage assemblies accounted for 40.42% of 2025 revenue, underscoring their widespread use in buildings, factories, and residential complexes that operate at voltages below 1 kV. High-voltage solutions, however, are growing at a 9.35% CAGR as utilities build 275-500 kV corridors for renewable integration. The ASEAN switchgear market size for high-voltage units is expected to exceed USD 6.33 billion by 2031, driven by the expansion of cross-border grid links and offshore wind tie-ins. Medium-voltage gear remains essential for data-center campuses and industrial parks, balancing power from primary feeders down to facility loads. Suppliers position compact GIS options for urban substations where land is scarce, while air-insulated configurations dominate rural transmission yards owing to cost advantages. In Singapore, hyperscale operators opt for redundant 480V lineups with smart metering to comply with stringent uptime requirements. Conversely, Indonesia’s Super Grid program specifies 500 kV dead-tank breakers for long-haul transmission, elevating demand for extra-high-voltage switchgear. Regional planners increasingly bundle low-voltage feeders with battery-storage interfaces, creating hybrid procurement packages that favor vendors offering broad portfolios.

Manufacturers deploy digital twins to predict insulation aging under tropical humidity, enhancing reliability at both extremes of the voltage spectrum. The ASEAN switchgear market share for low-voltage products will compress marginally as high-voltage investments increase, yet absolute low-voltage volumes will continue to rise alongside construction activity. Suppliers that can tier pricing across voltage classes while maintaining firmware compatibility are likely to gain from enterprise-wide rollouts by multinational customers.

By Insulation: Sustainability Shifts Design Preferences

Air-insulated technology held a 70.95% revenue share in 2025 due to its low acquisition cost and maintenance familiarity. Yet regulations targeting SF₆ emissions elevate demand for gas- and vacuum-based hybrids, driving a 15.48% CAGR for alternative systems through 2031. Singapore’s public-sector procurement now mandates SF₆-free mediums for new substation builds, encouraging regional utilities to pilot similar standards. Compact GIS addresses land-scarcity issues in urban nodes, reducing footprint by up to 90% compared to AIS. Manufacturers tout a vacuum-interrupter lifetime of 30,000 operations, which lowers the total cost of ownership despite higher upfront pricing. Hybrid solutions enable phased conversions: existing AIS bays receive vacuum interrupters while retaining primary busbars, easing capital budgeting. The ASEAN switchgear market size related to SF₆-free technology could reach USD 3.18 billion by 2031 if current policies extend to all member states.

Equipment specifiers weigh thermal performance under ambient temperatures exceeding 35°C, compelling OEMs to upgrade their heat-dissipation designs. Corrosion-resistant housings, silicone rubber bushings, and anti-condensation heaters become standard options. Vendors that provide environmental declarations and recycling programs earn points in tender evaluations. Over time, life-cycle assessment metrics may become as influential as acquisition costs when utilities compare bids for projects.

By Current Type: DC Uptick Signals Grid Evolution

AC architectures dominate, accounting for 87.32% of 2025 deployments, underscoring the entrenched legacy infrastructure. Direct-current equipment nonetheless grows at an 8.42% CAGR, driven by HVDC submarine cables, such as the 1 GW Singapore–Malaysia link, and the rising adoption of 380 V DC buses in data centers. The ASEAN switchgear market size for DC solutions is forecast to surpass USD 1.49 billion by 2031 as more offshore policy-driven efforts for renewable penetration and microgrid resilience indicate a gradual yet persistent shift, and projects prefer HVDC export lines to slash reactive-power losses. In colocation campuses, operators adopt DC distribution at the rack level to eliminate conversion stages, trimming energy loss by 5-8%. Manufacturers respond with solid-state DC breakers that feature sub-millisecond interruption and arc-free operation, thereby enhancing safety in confined spaces.

Hybrid nodes emerge where AC grid interfaces hand off to DC microgrids, which power servers and battery storage. Standards bodies accelerate work on interoperability guidelines, driving vendor certification programs. AC incumbency still anchors bulk-power transfer within mainland networks, but policy-driven efforts for renewable penetration and microgrid resilience indicate a gradual yet persistent shift toward DC platforms across select applications.

By Installation: Outdoor Builds Surge on Utility Spending

Indoor installations retained an 80.74% share in 2025, reflecting legacy placement inside plant rooms and commercial switchboards. Outdoor variants, however, are climbing at a 10.21% CAGR as utilities expand transmission corridors through difficult terrain. GIS housed in prefabricated e-houses offers plug-and-play yard installs, reducing civil works schedules by 25%. Solar farms and onshore wind arrays adopt weather-sealed cubicles with IP55 ratings and UV-resistant coatings. Seismic-grade anchoring gains attention in the Philippines and parts of Indonesia, prompting OEMs to test cabinets to IEEE 693 high-performance levels. Extended warranty packages and remote condition monitoring help offset the harsher duty cycle of outdoor gear. By 2031, the ASEAN switchgear market share for outdoor systems is expected to reach 24.6% as renewable energy penetration deepens.

Urban utilities still favor indoor AIS or GIS due to aesthetic and noise constraints; however, modular skid solutions enable faster replacements in aging substations. Designers integrate fire-suppression and arc-flash-detection cameras to meet city safety ordinances. Building owners appreciate that indoor switchboards with withdrawable drawers cut mean-time-to-repair to less than 30 minutes, preserving facility uptime.

By End-User: Utilities Drive Scale and Innovation

Utilities captured 39.05% of 2025 turnover and are projected to grow at 8.16% CAGR, reflecting USD 764 billion in announced grid spending across the bloc. They specify digital relays, SF₆-free interruptors, and cyber-secure communication links as default tender requirements. Industrial buyers come second, driven by automation and electrification, which increase demand for medium-voltage panels. Automotive manufacturers in Thailand and Vietnam retrofit their factories with energy-management-ready switchgear to meet corporate carbon reduction targets. Commercial buildings pioneer low-voltage switchboards linked to building-management systems, while residential developers deploy arc-fault detection to enhance safety in high-rise apartments.

Utilities also influence technology roadmaps by hosting pilot projects for solid-state breakers and peer-to-peer energy-trading nodes. Their buying power shapes standardization, pushing vendors to maintain multi-country certification lists. Conversely, fragmented industrial demand provides local fabricators with room to compete on price, especially when projects prioritize cost over advanced analytics.

Geography Analysis

Indonesia led with 22.85% revenue in 2025, driven by its 47,758-circuit-km Super Grid plan and buoyant manufacturing output. Local-content mandates of 40% drive joint ventures that shorten lead times and cut import tariffs. The government’s electrification targets for outer islands necessitate modular outdoor switchgear that can withstand salt-spray resistance and be remotely monitored over VSAT links. Malaysia exhibits the highest growth trajectory at 8.12% CAGR, driven by Tenaga Nasional Berhad’s RM 43 billion modernization program and a flourishing data center predictive analytics pipeline valued at USD 5 billion. Projects often pair 132 kV GIS bays with 22 kV ring-main units to accommodate mixed-use urban developments.

Singapore commands a premium niche focused on high-reliability applications, with utilities and colocation providers adopting SF₆-free equipment and predictive analytics service contracts. Thailand’s rail and industrial policies elevate medium-voltage uptake, while Vietnam’s renewable push drives both low- and high-voltage requisitions, albeit tempered by FIT revisions that introduce procurement delays. The Philippines pursues rural electrification, though fiscal constraints slow bulk orders, and Myanmar faces sanction-related supply hurdles that channel purchases toward Chinese vendors.

Regional integration through the ASEAN Power Grid increases demand for standardized 275-500 kV interconnection equipment across member states. Currency fluctuations influence tender timing, with buyers advancing purchases when local units strengthen against the USD. Localized production in Indonesia and Vietnam provides hedges against exchange-rate risk, thereby improving the competitiveness of domestically assembled switchgear across neighboring markets.

Competitive Landscape

Competition is moderately fragmented, with the top five international companies, Schneider Electric, ABB, Siemens, Hitachi Energy, and Eaton, collectively controlling roughly 45% of the 2024 ASEAN revenues. They leverage global R&D and digital-service stacks to defend premium segments. Regional players, such as Pekat Group, EPE Power, and Lucy Electric, gain market share by targeting price-sensitive projects with shorter delivery promises. Pekat’s USD 15.2 million acquisition of EPE Power’s Malaysian switchgear business exemplifies a regional consolidation trend that enhances localized engineering and post-sales support. Joint ventures, such as Siemens-Lilama in Vietnam, facilitate technology transfer and sidestep import duties, thereby eroding the multinationals’ cost advantage.

Product differentiation pivots on environmental credentials and embedded analytics. Schneider’s SF₆-free line, ABB’s eco-GIS, and Siemens’ Sensformer-ready modules address sustainability clauses in tenders. Meanwhile, Indonesian assemblers offer tailor-made AIS solutions optimized for tropical humidity at 10-15% lower prices. Service capabilities become a battleground; Lucy Electric’s Jakarta hub cuts spare-part lead time to 48 hours, enhancing its bids for utility O&M contracts. Vendors increasingly bundle multi-year condition-based maintenance as a subscription, improving revenue predictability and deepening customer lock-in.

Digital ecosystems widen competitive moats. Hitachi Energy’s Lumada Asset Performance combines IoT sensors and AI analytics, enabling predictive failure alerts that can reduce unplanned outages by 20%. Smaller firms partner with cloud platforms to offer lite versions of similar dashboards. Procurement committees now score bids based on software openness and cybersecurity audits, rewarding suppliers who are prepared for IEC 62443 compliance.

ASEAN Switchgear Industry Leaders

ABB Ltd

Siemens AG

Mitsubishi Electric Corporation

Schneider Electric SE

Hitachi Energy Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: ABB has launched its next-generation MNS low-voltage switchgear, featuring the SACE Emax 3 circuit breaker, designed for AI-driven data centers.

- August 2025: Schneider Electric has signed a long-term framework agreement with E.ON to deploy SF₆-free medium-voltage switchgear across its network, covering GM-AirSeT primary and RM-AirSeT secondary panels.

- June 2025: ACIT, led by Pham Dinh Thang, won the 2025 Tran Dai Nghia Award for developing 24kV and 40.5kV medium-voltage switchgear certified to IEC 62271-200 standards, reducing Vietnam’s reliance on imports.

- November 2024: Croatian company Koncar Elektroindustrija’s unit Koncar Switchgear delivered a 22 kV substation with 19 medium-voltage panels to Thailand’s Provincial Electricity Authority.

ASEAN Switchgear Market Report Scope

Switchgears are electrical equipment that controls, protects, and isolates electrical circuits and equipment. They are commonly used in power systems, industrial and commercial facilities, and other applications that require reliable and safe electrical power distribution. Switchgear typically consists of circuit breakers, disconnect switches, fuses, relays, and transformers. These components work together to ensure the safe and efficient operation of the electrical system.

The ASEAN switchgear market is segmented by application, installation, insulation, voltage, and geography. The market is segmented by application into residential, industrial, commercial, and utility. By installation, the market is segmented into indoor and outdoor. By insulation, the market is segmented into air, gas, and others. The market is segmented by voltage into low, medium, and high. The report also covers the market size and forecasts across major regional countries. The market sizing and forecasts for each segment are based on a revenue capacity (USD billion).

| Low Voltage |

| Medium Voltage |

| High Voltage |

| Gas Insulated Switchgear (GIS) |

| Air Insulated Switchgear (AIS) |

| Others |

| AC Switchgear |

| DC Switchgear |

| Indoor |

| Outdoor |

| Utilities |

| Residential |

| Commercial |

| Industrial |

| Singapore |

| Malaysia |

| Indonesia |

| Thailand |

| Vietnam |

| Philippines |

| Myanmar |

| Rest of ASEAN Countries |

| By Voltage | Low Voltage |

| Medium Voltage | |

| High Voltage | |

| By Insulation | Gas Insulated Switchgear (GIS) |

| Air Insulated Switchgear (AIS) | |

| Others | |

| By Current Type | AC Switchgear |

| DC Switchgear | |

| By Installation | Indoor |

| Outdoor | |

| By End-User | Utilities |

| Residential | |

| Commercial | |

| Industrial | |

| By Geography | Singapore |

| Malaysia | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Philippines | |

| Myanmar | |

| Rest of ASEAN Countries |

Key Questions Answered in the Report

What is the 2026 value of the ASEAN switchgear market?

It stands at USD 13.19 billion, up from USD 12.28 billion in 2025 due to ongoing grid-upgrade programs.

Which voltage class is growing fastest?

High-voltage equipment is expanding at a 9.35% CAGR on the back of cross-border transmission projects.

Why are SF?-free switchgear solutions gaining traction?

National mandates, led by Singapore, aim to curtail greenhouse-gas emissions, pushing utilities toward vacuum and gas-mixture insulation.

How do local-content rules influence purchasing decisions in Indonesia?

A 40% domestic value-add requirement encourages OEMs to assemble locally, lowering import tariffs and shortening lead times.

What is driving DC switchgear demand?

HVDC interconnectors and data-center adoption of 380 V DC buses are propelling an 8.42% CAGR for DC-rated equipment.

Which end-user segment leads spending?

Utilities remain the largest and fastest-growing buyers, fueled by USD 764 billion in planned network investments.

Page last updated on: