Medical Tourism Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 110.97 Billion |

| Market Size (2031) | USD 258.32 Billion |

| Growth Rate (2026 - 2031) | 18.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Tourism Market Analysis by Mordor Intelligence

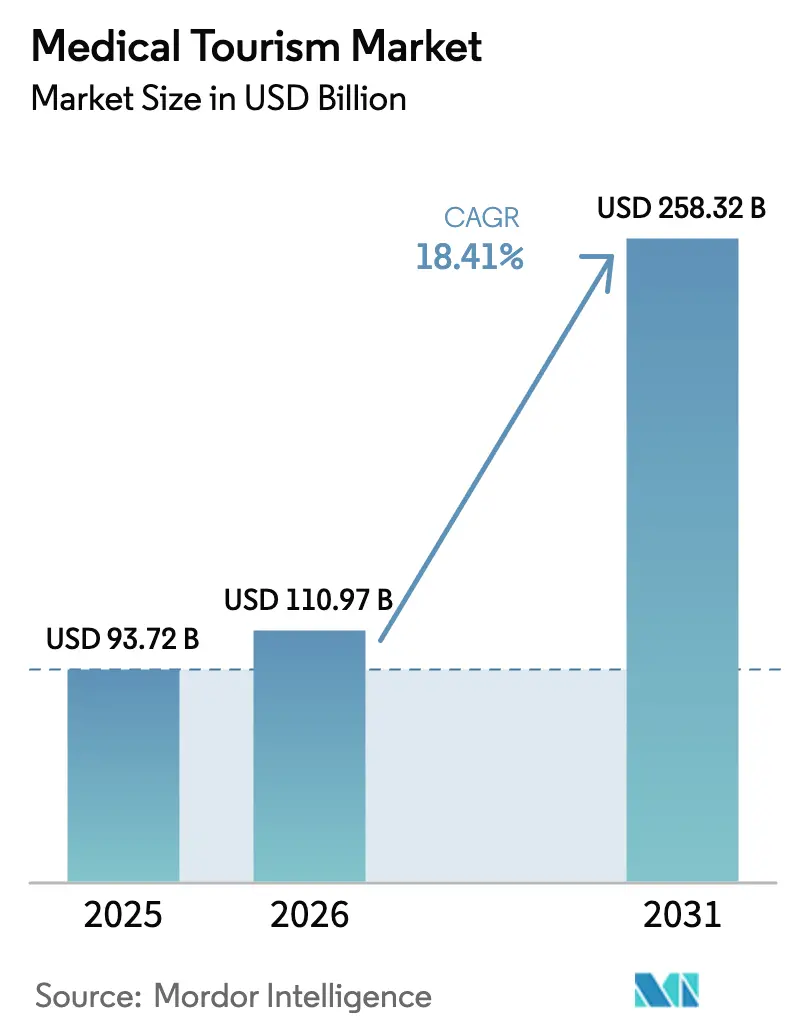

The Medical Tourism Market size was valued at USD 93.72 billion in 2025 and is estimated to grow from USD 110.97 billion in 2026 to reach USD 258.32 billion by 2031, at a CAGR of 18.41% during the forecast period (2026-2031).

Persistent cost arbitrage means patients continue to save 40-70% on complex procedures, even after factoring in airfare, which anchors the structural momentum behind cross-border care. In the Asia-Pacific, the Middle East, and select Latin American destinations, this gap has widened by streamlining visas, subsidizing technology adoption, and positioning tertiary hospitals as export generators rather than domestic cost centers. Supply-side investments in proton therapy, robotic surgery, and AI-enabled diagnostics are compressing the traditional quality delta between destination and source countries, shifting competition from price alone to a blend of clinical parity and patient-experience differentiation. Simultaneously, high-income nations face rising deductibles and lengthening waitlists for elective surgery, which prompt self-pay patients to seek treatment abroad despite tighter travel budgets. Governments that treat inbound clinical travel as an economic priority, such as Thailand, Singapore, the UAE, and Malaysia, now operate national portals and bundled insurance products that reduce friction and amplify the appeal of the medical tourism market.

Key Report Takeaways

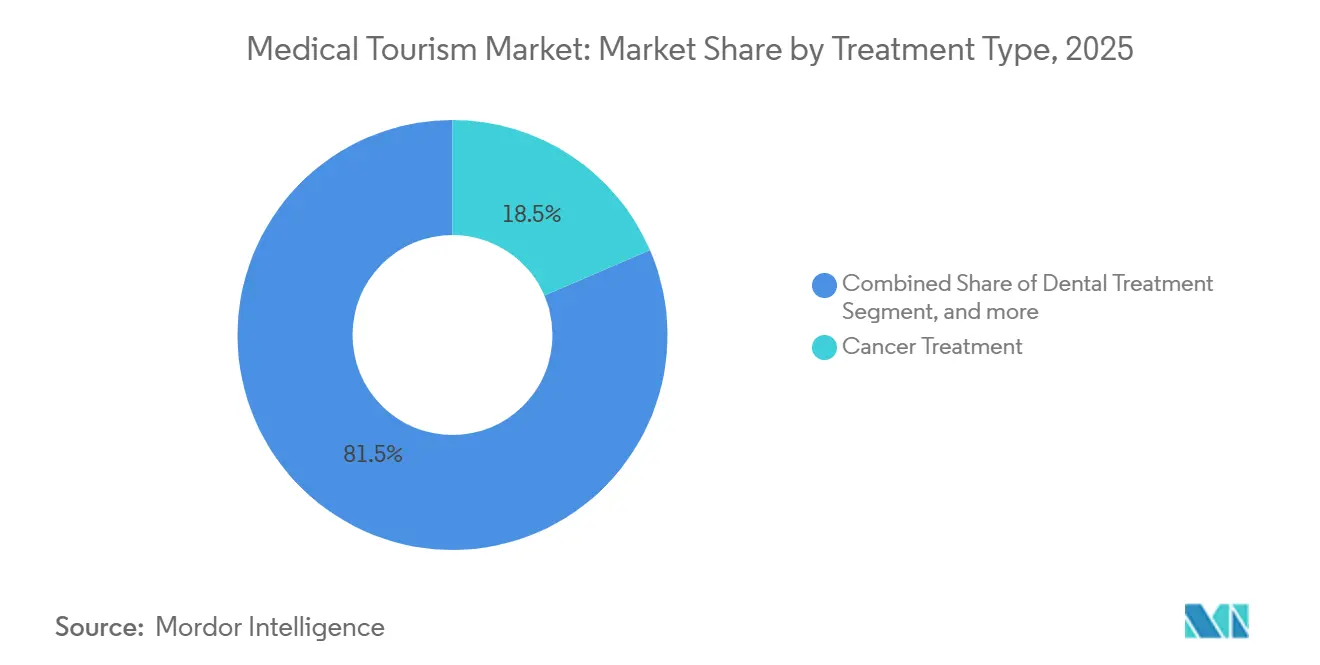

- By treatment type, cancer treatment held 18.54% of the medical tourism market share in 2025, while orthopedic treatment is forecast to expand at a 20.45% CAGR through 2031.

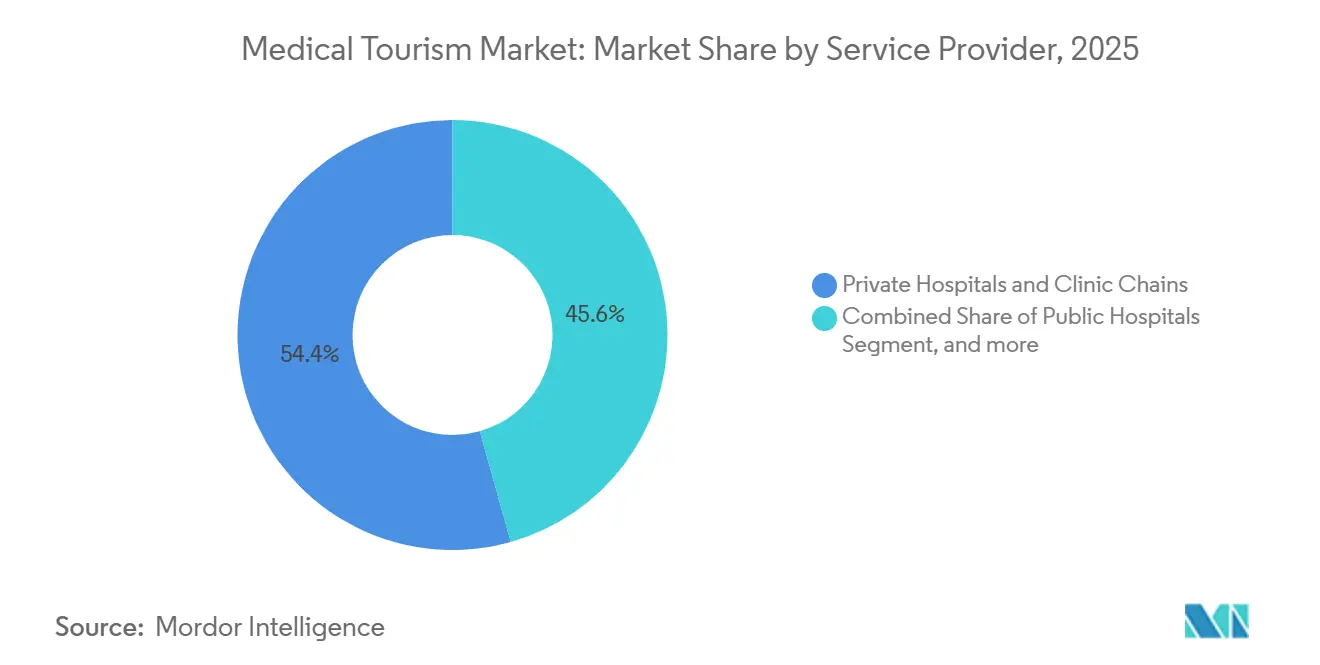

- By service provider, private hospitals and clinic chains captured 54.32% of the revenue in 2025 and are projected to advance at a 21.32% CAGR through 2031.

- By type, inbound international travel accounted for 63.45% of the value in 2025 and is growing at a 20.54% CAGR through 2031.

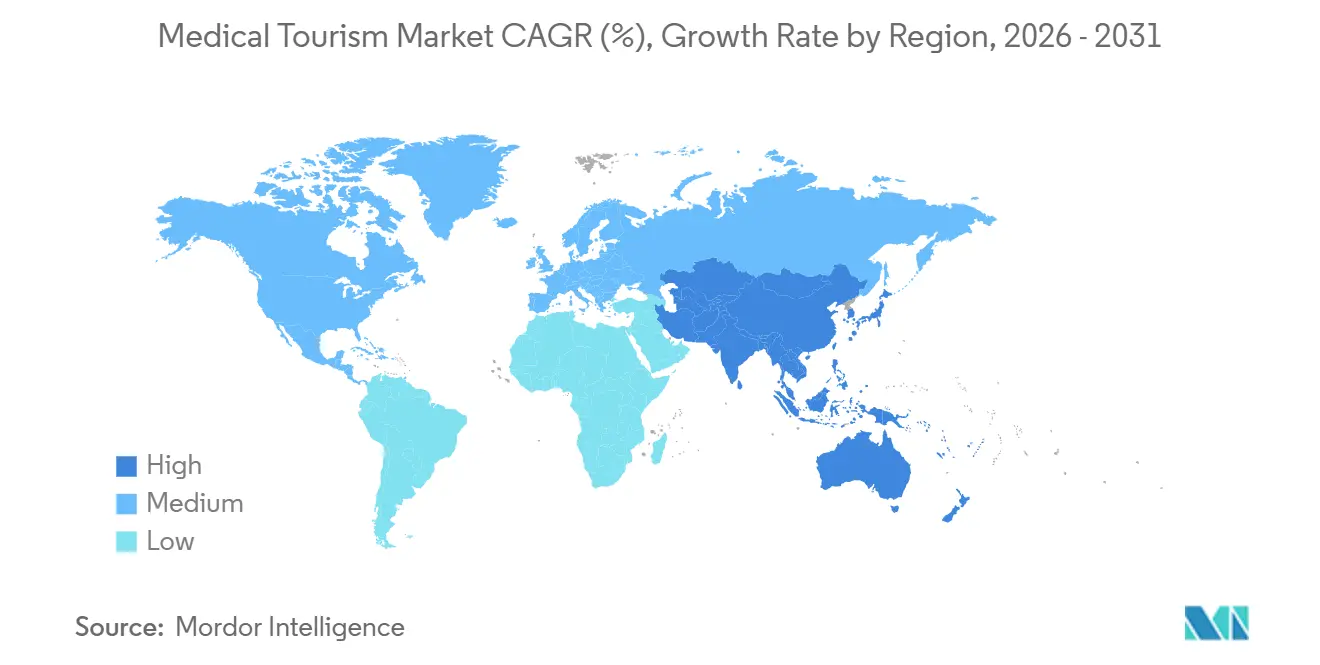

- By geography, the Asia-Pacific region secured 46.43% of global revenue in 2025 and is projected to grow at a 19.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Tourism Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Treatment and Insurance Costs in High-Income Nations | +4.2% | North America, Europe | Long term (≥ 4 years) |

| Expansion of Internationally Accredited Specialty Hospitals | +3.8% | Asia-Pacific core, spillover to Middle East | Medium term (2–4 years) |

| Reduced Waiting Lists for Elective Surgeries Abroad | +3.1% | Europe (UK, Ireland), Canada | Short term (≤ 2 years) |

| Growing Adoption of Advanced Medical Technologies in Destination Countries | +2.9% | Asia-Pacific, Middle East | Medium term (2–4 years) |

| Integration of AI-Enabled Virtual Second-Opinion Platforms | +1.6% | Global, early adoption in North America and Asia-Pacific | Short term (≤ 2 years) |

| Emergence of Faith-Based Halal and Wellness-Centric Healthcare Clusters | +1.4% | Middle East, Malaysia, Indonesia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Treatment and Insurance Costs in High-Income Nations

U.S. per-capita health spending reached USD 12,555 in 2022, nearly twice Canada’s USD 6,207, a gap that has not narrowed because administrative overhead and pharmaceutical pricing in North America remain structurally higher. Rising deductibles and co-pays are prompting insured and self-pay patients to consider bundled packages overseas, where a bariatric procedure in Mexico costs USD 4,000–8,000, compared to USD 15,000–25,000 in the United States, resulting in a 60–70% savings after accounting for airfare. Dental crowns exhibit parallel trends, underscoring the high volume of dental tourists traveling to Mexico, Turkey, and Costa Rica. Because this pressure is systemic rather than cyclical, outbound patient volumes from high-income countries are unlikely to recede during the forecast period, reinforcing medical tourism market growth..

Expansion of Internationally Accredited Specialty Hospitals

The number of Joint Commission International (JCI)-accredited facilities in the Asia-Pacific and Middle East regions has doubled since 2020, indicating the widespread adoption of universal infection-control and patient-safety protocols[1]Joint Commission International, “Accredited Organizations Directory,” JCI, jci.org. Hospitals that secure early accreditation, such as Bumrungrad International, which treats 600,000 patients from 190 countries annually, leverage that badge to command premium pricing and partner with global insurers. Cleveland Clinic Abu Dhabi and Riyadh’s King Salman Medical City are following a similar approach, positioning Gulf Cooperation Council hubs to attract oncology and cardiac cases from Europe and Africa, further strengthening the medical tourism market.

Reduced Waiting Lists for Elective Surgeries Abroad

Median wait times at the U.K. National Health Service reached 25 weeks for total knee replacement in 2024, prompting patients to self-fund surgeries in India or Thailand, where scheduling occurs within four weeks[2]NHS England, “Consultant-led Referral to Treatment Waiting Times,” NHS, nhs.uk. Thailand extended its medical visa to 90 days in 2024, while Singapore’s 2025 medical visa now processes in 48 hours, institutionalizing time-arbitrage as a competitive lever. Capacity expansions India’s private sector will add 34,000 beds by fiscal 2029 ensure destination availability aligns with rising outbound demand and sustained medical tourism market growth.

Growing Adoption of Advanced Medical Technologies in Destination Countries

Robotic platforms now support 30% of surgeries in India’s private sector, and Thailand aims to equip 100 public hospitals with robots by 2026. Apollo Hospitals commissioned South Asia’s first proton-therapy center in 2024, matching modalities once exclusive to U.S. or EU academic centers. Technology parity eliminates a historic rationale for staying domestic, steering higher-acuity oncology and neurology cases toward the medical tourism market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-Procedure Continuity of Care Challenges | −1.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Cross-Border Medical Record Interoperability Gaps | −1.3% | Asia-Pacific to North America/Europe corridors | Medium term (2–4 years) |

| Rising International Scrutiny of Cosmetic Surgery Carbon Footprint | −0.9% | Global, most pronounced in Europe and North America | Short term (≤ 2 years) |

| Increasing Visa Policy Uncertainty in Key Destination Markets | −1.0% | Asia-Pacific, Middle East | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Post-Procedure Continuity of Care Challenges

A 2024 survey showed 62% of U.S. orthopedic surgeons decline follow-up for procedures done abroad, citing implant quality and liability concerns[3]American Academy of Orthopaedic Surgeons, “Post-Travel Patient Care Survey 2024,” AAOS, aaos.org. Destination hospitals are mitigating this via 90-day virtual follow-ups bundled in their packages; Apollo and Fortis embed video consults and remote monitoring devices to bridge the gap. Yet insurance exclusions for complications remain common, deterring older or comorbid patients and capping the upper end of the medical tourism market.

Cross-Border Medical Record Interoperability Gaps

The EU’s Electronic Health Data Space regulation, effective March 2025, mandates the exchange of pan-EU International Patient Summaries by 2029, thereby easing intra-European clinical travel. Outside the bloc, patients still courier CDs and paper summaries, risking transcription errors that delay care. Estonia’s blockchain-enabled e-health keys and Taiwan–Philippines pilots confirm the technical viability, but global coverage remains distant, sustaining an administrative drag on the medical tourism industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segmentation

By Treatment Type: Oncology Dominates, Orthopedics Accelerates

Cancer treatment accounted for 18.54% of 2025 revenue, underscoring patient willingness to travel for proton therapy and precision radiotherapy, which remain scarce in many home markets. Orthopedic procedures exhibit the fastest expansion, with a 20.45% CAGR, because robotic joint replacement shortens recovery windows and aligns with active lifestyle priorities. The medical tourism market size for orthopedic care is projected to increase sharply as Thailand deploys 100 robotic platforms and Indian chains expand their capacity. Cardiovascular care remains steady as Narayana Health and Bumrungrad perform complex surgeries at 30–40% of U.S. price points while retaining JCI accreditation. Cosmetic and fertility treatments contribute volume, but escalating sustainability scrutiny and regulatory divergence shape moderate single-digit growth trajectories.

Leading destination hospitals now promote multidisciplinary sequencing—for instance, combining oncology surgery with postoperative immunotherapy—extending length of stay and per-patient revenue. Neurology procedures, such as deep brain stimulation, are emerging niches, supported by Apollo’s Gamma Knife suite and Bangkok Hospital’s specialized centers. By integrating post-operative tele-rehabilitation, chains improve outcomes and mitigate continuity-of-care constraints that once discouraged high-acuity travel. As technology parity becomes ubiquitous, the decision matrix tilts toward recovery experience, accreditation depth, and bundled pricing, reinforcing incumbent advantages in Asia-Pacific hubs.

By Service Provider: Private Chains Control Capital Flow

Private hospitals held 54.32% of 2025 revenue and are advancing at a 21.32% CAGR, reflecting their agility in raising debt and equity to finance high-ticket modalities. Apollo’s plan to add up to 4,300 beds and Fortis’ 2,200-bed expansion underpin a widening capacity moat relative to public systems. The medical tourism market share controlled by private chains is supported by concierge desks, multilingual care teams, and AI-enabled patient-coordination apps that compress booking cycles. Public hospitals, although significant domestically, lag in luxury amenities and direct-booking interfaces. However, Thailand’s push for robotic surgery across 100 public facilities is narrowing this service gap.

Facilitator agencies that once commanded 10–15% commissions are being disintermediated as hospitals deploy direct-to-patient portals and governments publish accredited directories. In higher-acuity oncology and neurology segments, patients now book directly with flagship chains, valuing transparency over marginal savings. However, facilitators remain relevant in dental and cosmetic niches, where price sensitivity is higher, and brand loyalty is lower. Over the forecast horizon, capital-intensive private chains will consolidate mid-tier clinics, utilizing their scale purchasing power to compress input costs and enhance price competitiveness.

By Type: Inbound Flows Outpace Domestic and Outbound

Inbound international travel represented 63.45% of medical tourism market value in 2025 and is expanding at a 20.54% CAGR, sustained by destination-country policies that treat clinical care as an export. Thailand’s target of 3.1 million medical tourists in 2025, up from 2.6 million in 2024, exemplifies this export mindset. Singapore’s 48-hour visa and the UAE’s bundled Emirates-DHA packages further institutionalize inbound flows. Outbound travel from source markets grows, but at a slower clip as the U.K. and Canada add domestic elective capacity. Domestic medical tourism within federated nations like India is rising, but remains smaller because internal travel offsets some of the perceived cultural and continuity-of-care risks.

Destination governments are increasingly integrating visa, hotel, and insurance elements into single-window portals, reinforcing their dominance in the inbound flow. This structural tilt suggests inbound volumes will remain above 60% of the medical tourism market size through 2031, even as domestic systems in source countries accelerate incremental capacity additions.

Geography

Asia-Pacific accounted for 46.43% of 2025 revenue and is expected to grow at a 19.45% CAGR, cementing its leadership in the medical tourism market. Thailand’s THB 165 billion (USD 4.9 billion) revenue goal for 2025 aligns with visa extensions that allow 90-day recoveries. Singapore’s ambition to reach 1 million arrivals by year-end, alongside a SGD 3 billion (USD 2.2 billion) revenue target, reflects its pivot toward complex oncology and cardiology. India’s private chains, buoyed by 34,000 new beds, report international patient ARPOB surges that outpace domestic growth. Malaysia leverages Halal-certified clusters to attract Middle Eastern clientele, reinforcing the Asia-Pacific region’s multi-segment appeal.

The Middle East and Africa trail but are expected to accelerate: the UAE welcomed 679,000 medical tourists in 2023 and aims to reach 1 million by 2027 through oncology and orthopedic centers linked to Emirates’ bundled fare programs. Saudi Arabia’s Vision 2030 pegs a 500,000-patient goal, anchored by the 5,000-bed King Salman Medical City. Europe’s intra-regional flows gain efficiency from the 2025 EHDS regulation, but cost advantages remain narrower than those in the Asia-Pacific region. North America remains a net exporter; however, select U.S. academic centers capture a significant portion of inbound Latin American demand for high-acuity cancer and cardiac care.

South America’s niche—cosmetic surgery in Brazil and Colombia—faces competition from lower-cost Mexico and efficacy-focused Asian clinics. Network effects in Asia-Pacific—capacity expansion funding, further marketing, and technology upgrades, which in turn attract more patients—create a self-reinforcing leadership loop unlikely to be disrupted before 2031.

Competitive Landscape

Global revenue remains fragmented, with no single chain holding more than 5%, assigning the sector a moderate concentration profile. Competitive vectors are shifting toward technology intensity and accreditation scope. Apollo Hospitals’ proton-therapy launch in 2024 offers a seven-year regional lead, drawing oncology cases willing to pay premiums for targeted radiotherapy. Bumrungrad and Bangkok Hospital leverage their early JCI accreditation and multilingual staff to retain loyalty among the combined 2.1 million international patients they annually. Fortis Healthcare’s network-wide robotic roll-out underscores a capital arms race that widens capability gaps between top chains and tier-2 facilities.

Emerging disruptors include AI-driven platforms like SmartClinix, which stitch the pre-op, in-hospital, and post-op phases into a unified digital pathway, thereby diluting the historical advantage of in-market facilitators. Blockchain-based record interoperability trials in Estonia offer a glimpse of patient-controlled data exchange that could erode one of the sector’s key friction costs. Investors scanning white spaces find neurology and sub-Saharan geographies underserved; no accredited pan-African hospital chain exists today, implying first-mover potential for operators willing to navigate regulatory ambiguity.

Medical Tourism Industry Leaders

Klinikum Medical Link

Apollo Hospitals

KPJ Healthcare Behard

Healthbase

Fortis Healthcare Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Malaysia Healthcare Travel Council (MHTC) announced the winner of its Flagship Medical Tourism Hospital (FMTH) Programme. This milestone highlights Malaysia's efforts to strengthen its position as a leading medical tourism destination. The initiative aims to showcase top hospitals and enhance Malaysia's global reputation in healthcare travel.

- September 2025: The Patra Bali Resort & Villas partnered with Bali International Hospital (BIH) to introduce a Medical Tourism program. The initiative targets Pertamina Group officers and the general public, combining tourism with healthcare services. This program offers guests the opportunity to enjoy a vacation while receiving comprehensive health checkups, promoting integrated tourism and healthcare.

- June 2025: Vaidam Health, a leading Indian medical tourism company, acquired MediJourney, a digital platform for international patient facilitation incubated by Ferns N Petals. The all-cash deal aims to help Vaidam expand its global reach, boost technology, and enhance patient services. This strategic move strengthens Vaidam's position in the international healthcare market.

Global Medical Tourism Market Report Scope

As per the scope of the report, medical tourism (also called medical travel, health tourism) is a term used to describe the rapidly growing practice of traveling across international borders to seek healthcare services.

The Medical Tourism Market Report is Segmented by Treatment Type (Dental, Cardiovascular, Orthopedic, Cosmetic & Aesthetic, Fertility, Cancer, Neurology, Bariatric, Ophthalmic, and Other Treatments), Service Provider (Public Hospitals, Private Hospitals & Clinic Chains, and Facilitator & Concierge Agencies), Type (Inbound, Outbound, and Domestic), and Geography (North America, Europe, Asia-Pacific, Middle East And Africa, and South America). Market Forecasts are Provided in Terms of Value (USD). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Dental Treatment |

| Cardiovascular Treatment |

| Orthopedic Treatment |

| Cosmetic & Aesthetic Treatment |

| Fertility Treatment |

| Cancer Treatment |

| Neurology Treatment |

| Bariatric Treatment |

| Ophthalmic Treatment |

| Other Treatments |

| Public Hospitals |

| Private Hospitals & Clinic Chains |

| Facilitator & Concierge Agencies |

| Inbound International Medical Tourism |

| Outbound International Medical Tourism |

| Domestic Medical Tourism |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East And Africa | GCC |

| South Africa | |

| Rest Of Middle East And Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Treatment Type | Dental Treatment | |

| Cardiovascular Treatment | ||

| Orthopedic Treatment | ||

| Cosmetic & Aesthetic Treatment | ||

| Fertility Treatment | ||

| Cancer Treatment | ||

| Neurology Treatment | ||

| Bariatric Treatment | ||

| Ophthalmic Treatment | ||

| Other Treatments | ||

| By Service Provider | Public Hospitals | |

| Private Hospitals & Clinic Chains | ||

| Facilitator & Concierge Agencies | ||

| By Type | Inbound International Medical Tourism | |

| Outbound International Medical Tourism | ||

| Domestic Medical Tourism | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East And Africa | GCC | |

| South Africa | ||

| Rest Of Middle East And Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

How large will the medical tourism market be by 2031?

It is projected to reach USD 258.32 billion, growing at an 18.41% CAGR between 2026 and 2031.

Which region leads in medical tourism revenue?

Asia-Pacific held 46.43% of 2025 revenue and is forecast to grow the fastest through 2031.

What treatment segment is growing the quickest?

Orthopedic procedures, supported by robotic-surgery adoption, are advancing at a 20.45% CAGR to 2031.

Why do patients choose overseas care despite travel costs?

Savings of 40-70% on complex procedures, shorter wait times, and availability of advanced technologies offset travel expenses.

How are hospitals addressing post-operative continuity issues?

Leading chains bundle 90-day tele-follow-ups and collaborate with local clinics to ensure seamless recovery support.

Page last updated on: