Market Overview

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 7.16 Billion |

| Market Size (2030) | USD 10.13 Billion |

| Growth Rate (2025 - 2030) | 7.17% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mass Spectrometry Market Analysis by Mordor Intelligence

The Mass Spectrometry Market size is estimated at USD 7.16 billion in 2025, and is expected to reach USD 10.13 billion by 2030, at a CAGR of 7.17% during the forecast period (2025-2030).

Momentum stems from rising biologics characterization, tighter food-safety oversight, miniaturized point-of-care systems, artificial-intelligence (AI) data analytics, and multi-omics funding. North America’s mature research ecosystem and stringent regulatory framework keep the region at the forefront, yet Asia-Pacific’s double-digit trajectory signals a geographical power shift. Competitive differentiation is gravitating toward software-hardware integration, as user demand for real-time, high-throughput insights eclipses pure instrument specifications. Meanwhile, capital constraints in developing-country academic facilities and persistent talent gaps temper adoption, underscoring the need for creative financing and training programs.

Key Report Takeaways

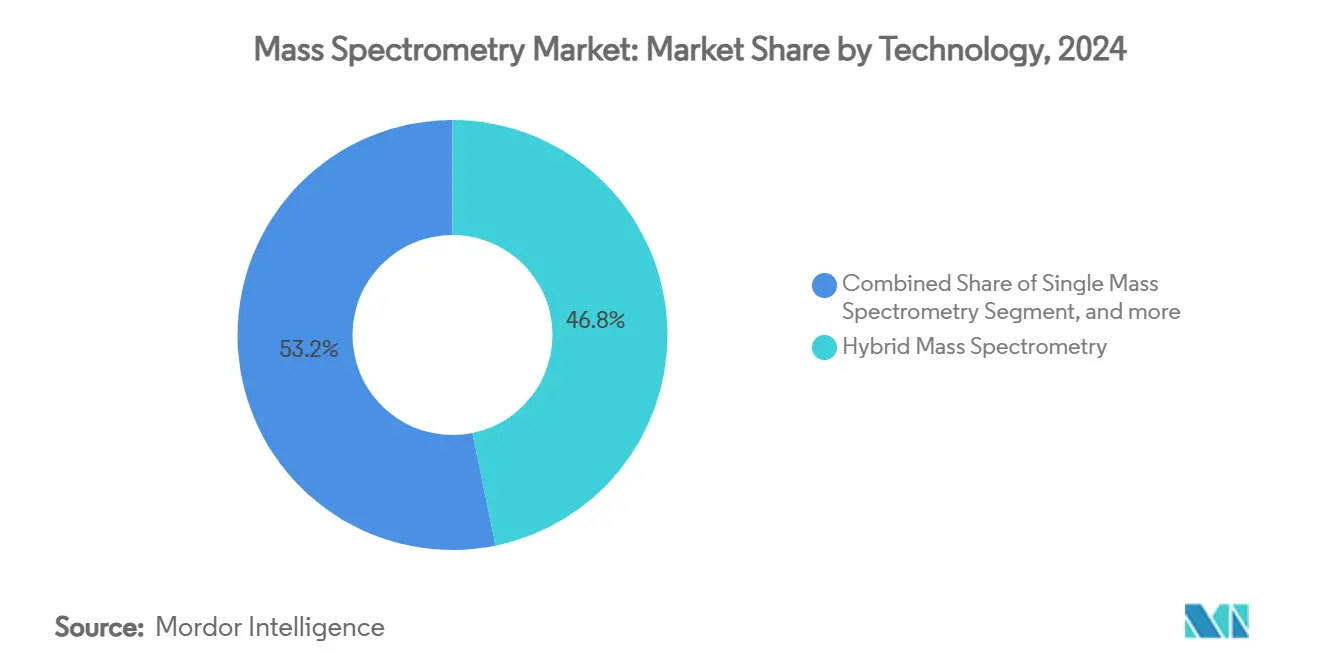

- By technology, hybrid mass spectrometry commanded 46.82% of the mass spectrometry market share in 2024, while matrix-assisted laser desorption/ionization time-of-flight (MALDI-TOF) is projected to accelerate at an 11.45% CAGR to 2030.

- By component, instruments held 71.27% of the mass spectrometry market in 2024; software and informatics represent the fastest growth path, with a 12.16% CAGR through 2030.

- By application, the pharmaceutical and biotechnology segment led with 34.71% revenue share in 2024; clinical diagnostics and proteomics are advancing at a 12.83% CAGR to 2030.

- By geography, North America retained 35.19% of the mass spectrometry market in 2024, whereas Asia-Pacific is on track to expand at a 10.38% CAGR between 2025 and 2030.

Global Mass Spectrometry Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Evolving biologics & large-molecule characterization needs | +1.4% | Global | Long term (≥ 4 years) |

| Stringent food-safety regulations accelerating adoption | +1.2% | North America, Europe | Short term (≤ 2 years) |

| Miniaturization & high-throughput screening demand in diagnostics | +1.1% | Global | Medium term (2-4 years) |

| Rising multi-omics research funding | +1.0% | Global | Long term (≥ 4 years) |

| Increasing R&D expenditure by public & private organizations | +0.9% | North America, Asia-Pac | Medium term (2-4 years) |

| Emergence of ambient & portable mass spectrometry technologies | +0.8% | Asia-Pac, North America | Short term (≤ 2 years) |

Source: Mordor Intelligence

Understand The Key Trends Shaping This Market

Download PDF

Evolving Biologics & Large-Molecule Characterization Needs

Demand for ultra-high-resolution instruments is soaring as drug developers pivot toward monoclonal antibodies and cell-based therapies. Post-translational modification mapping and higher-order structure verification now require hybrid platforms incorporating electron capture dissociation to preserve fragile bonds during fragmentation.[1]Agilent Technologies, “Electron Capture Dissociation Cell Enhances Biotherapeutics Analysis,” agilent.com Manufacturers that can streamline complex protein workflows are well-positioned to capture future revenue.

Stringent Food-Safety Regulations Accelerating Adoption

The US EPA’s 2024 designation of PFOA and PFOS as hazardous substances drove a wave of liquid chromatography-tandem mass spectrometry upgrades across environmental and food laboratories. Comparable policy moves in Europe under ECHA continue to tighten detection limits, propelling instrument placements and method-development services. The food industry's response includes adopting novel approaches like Extractive-liquid sampling electron ionization-mass spectrometry (E-LEI-MS), which enables real-time identification of pesticides on fruit peels without sample preparation, significantly reducing analysis time from hours to minutes.

Miniaturization & High-Throughput Screening Demand in Clinical Diagnostics

Bruker’s MALDI Biotyper sirius now processes up to 600 isolates per hour, illustrating a paradigm shift in clinical microbiology throughput.[2]Bruker Corporation, “MALDI Biotyper sirius Extends Throughput to 600 Isolates per Hour,” Bruker, bruker.com Portable designs targeting emergency departments and operating rooms aim to embed mass-spectrometric decision support directly at the point of care. The integration of mass spectrometry with artificial intelligence is further accelerating clinical applications, with deep learning frameworks like IDSL_MINT enhancing the annotation rates of MS/MS spectra for previously unidentified compounds.

Rising Multi-omics Research Funding

Thermo Fisher Scientific’s Orbitrap Astral system realized breakthrough peptide coverage in just 30 minutes, underscoring the growing capital allocation to integrative omics programs.[3]Thermo Fisher Scientific, “Orbitrap Astral Mass Spectrometer Accelerates Deep Proteome Coverage,” Thermo Fisher Scientific, thermofisher.com Academic-industry consortia seek end-to-end platforms that cross proteome, metabolome, and lipidome boundaries. The Astral mass analyzer represents a quantum leap in microbiome research, achieving over 122,000 unique peptides and 38,000 protein groups in just 30 minutes of analysis time, dramatically accelerating functional analysis of complex microbial communities

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-expenditure constraints in developing-country academia | −1.3% | Asia-Pac, LatAm, Africa | Short term (≤ 2 years) |

| Shortage of experienced mass-spectrometrists | −1.1% | Global | Medium term (2-4 years) |

| Data-management & standardization challenges in large-scale omics | −0.9% | Global | Long term (≥ 4 years) |

| Lengthy instrument validation & regulatory approval cycles | −0.7% | North America, Europe | Medium term (2-4 years) |

Source: Mordor Intelligence

Capital-Expenditure Constraints in Academic Core Facilities Across Developing Countries

High-end systems range from USD 500,000 to USD 1.5 million, with grant scarcity forces shared-resource centers to postpone upgrades, reducing instrument access for regional researchers. This financial barrier is compounded by ongoing operational costs, including maintenance contracts and consumables, which can represent 15-20% of the initial investment annually. The situation is particularly challenging for core facilities that serve multiple research groups, as they must balance acquisition costs against user fees that remain affordable for local researchers.

Shortage of Experienced Mass-Spectrometrists in Emerging Markets

A global skills survey found serious gaps in spectral interpretation and data-quality assessment among metabolomics practitioners. Vendor-led training and intuitive software help, yet talent cultivation remains slower than demand growth. This skills shortage is particularly acute in clinical settings, where the transition from research applications to diagnostic workflows requires specialized knowledge at the intersection of analytical chemistry and medical practice. The complexity of modern mass spectrometry systems, which increasingly incorporate artificial intelligence and machine learning components, further elevates the expertise required for optimal operation.

Segment Analysis

By Technology: MALDI-TOF Reshapes Clinical Workflows

Hybrid architectures continued to dominate 46.82% of the mass spectrometry market share in 2024, yet MALDI-TOF platforms exhibit the steepest trajectory, posting an 11.45% CAGR outlook. MALDI-TOF’s rapid microbial identification slashed diagnostic turnaround to minutes, lowering hospitalization costs. Beyond microorganisms, MALDI HiPLEX-IHC now delivers multiplexed intact-protein imaging at 5 µm spatial resolution, enabling spatial proteomics in oncology tissue sections.

Second-generation MALDI units also tackle rapid microbiota classification with near-90% accuracy, broadening usage in gut-microbiome studies. Integration with machine-learning algorithms automates spectral-fingerprint libraries, a key differentiator as hospital laboratories scale throughput demands.

Note: Segment shares of all individual segments available upon report purchase

By Component: Software Unlocks Analytical Value

Instruments constituted 71.27% of the mass spectrometry market for components in 2024, yet software and informatics projected to register a 12.16% CAGR between 2025 and 2030. Empower, adopted in 80% of 2023 novel-drug filings, illustrates the regulatory confidence vendors capture through validated data-handling platforms.

MZmine 3 harmonizes inputs from ion-mobility, time-of-flight, and orbitrap instruments into a single workspace, breaking down vendor silos and elevating user productivity. Looking forward, AI-driven annotation engines anticipate expanding the accessible chemical space, compressing data-review timelines, and freeing capacity for higher-value interpretation.

By Application: Diagnostics Surges Ahead

Pharmaceutical and biotechnology laboratories retained 34.71% revenue in 2024, but clinical diagnostics and proteomics are advancing at a brisk 12.83% CAGR. In onychomycosis detection, MALDI-TOF reached 95.4% sensitivity and 97.5% specificity, highlighting disruptive accuracy over culture-based assays.

Minimal residual disease tracking in multiple myeloma reveals another leap: the EXENT automated MALDI-TOF system identified low-level M-proteins even when standard serum electrophoresis missed them. Such use cases underline the clinical imperative for precise, high-throughput, and cost-effective mass spectrometry diagnostics.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America contributed 35.19% to the mass spectrometry market in 2024, owing to strong National Institutes of Health funding, a vibrant biotech pipeline, and stringent environmental regulations. The United States Environmental Protection Agency’s PFAS mandates require lower detection limits, driving instrument refresh cycles, and specialized consumables. Canada is following up with updated drinking-water quality guidelines, spurring provincial tenders.

Asia-Pacific is forecast to expand at a 10.38% CAGR to 2030 and is central to future volume growth. China’s manufacturers secured venture funding to commercialize miniaturized direct-ionization devices, aiming to address domestic demand and export opportunities. Parallel expansion of contract development and manufacturing organizations (CDMOs) in India and South Korea creates recurring demand for compliance-ready platforms.

Europe remains a stable, high-value market, anchored by stringent EFSA and EMA regulations. The ECHA’s continuously evolving chemical-safety framework necessitates frequent method-validation updates, sustaining service revenue streams. Middle East & Africa and South America, though smaller in total addressable revenue, exhibit momentum through GCC public-health investments and Brazil’s agrochemical-residue monitoring programs, respectively.

Competitive Landscape

Competition centers on five global leaders: Thermo Fisher Scientific, Agilent Technologies, Waters Corporation, Bruker Corporation, and Danaher (SCIEX). Together, they capture the largest share, with Thermo Fisher solidifying its edge via the 2024 Stellar platform that unites fast throughput with translational-omics versatility.

Agilent’s ExD Cell retrofit strategy lets users bolster legacy LC/Q-TOFs for complex biotherapeutic characterization, illustrating the value of modularity. Waters focuses on workflow-centric software; Empower’s regulatory track record increases customer stickiness. Bruker’s majority purchase of RECIPE brings ready-to-run diagnostic kits that simplify triple-quad deployment in routine clinical labs. Danaher’s SCIEX unit emphasizes differentiated analytical-service contracts that guarantee uptime.

Emerging challengers attack niches, portable formats, AI-augmented data mining, and modular detector add-ons rather than trying to out-spec incumbents on resolution. Patent filings such as Thermo Fisher Bremen’s time-of-flight peak-deconvolution algorithm confirm that proprietary computation is joining ion source design as a primary competitive frontier.

Mass Spectrometry Industry Leaders

-

Thermo Fisher Scientific Inc.

-

Agilent Technologies Inc.

-

Danaher Corporation (SCIEX)

-

Waters Corporation

-

Bruker Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Bruker has announced the majority acquisition of RECIPE, a leading provider of mass spectrometry-based diagnostic assay kits. This strategic move strengthens Bruker's position in the field of therapeutic drug monitoring (TDM). The two companies are collaborating to pioneer the high-throughput, "chrom-free" ClinDART triple-quad mass spectrometry (MS) platform, designed to deliver robust and cost-effective TDM assays. This advancement aims to improve clinical diagnostics by offering more efficient and accessible monitoring solutions for therapeutic drug levels, benefiting both healthcare providers and patients.

- June 2024: Thermo Fisher Scientific launched the Stellar mass spectrometer at the ASMS conference, emphasizing fast throughput, high sensitivity, and ease of use for translational omics research. It integrates with the Ardia platform and Vanquish Neo UHPLC system.

- June 2024: Bruker Corporation introduced the Neoflex Imaging Profiler, a MALDI-TOF/TOF mass spectrometry system for tissue imaging. It features a 10-kHz smart beam 3D laser and enhanced imaging detectors to transition from discovery imaging to clinical tissue research.

- June 2024: Agilent Technologies announced the launch of the 7010D Triple Quadrupole GC/MS System and the ExD Cell for the 6545XT AdvanceBio LC/Q-TOF at the ASMS 2024 conference. These systems target food, environmental markets, and complex biotherapeutics analysis.

Global Mass Spectrometry Market Report Scope

As per the scope of this report, mass spectrometry (MS) is an analytical chemistry technique used to identify the amount and type of chemical species present in a sample, by measuring the mass-to-charge ratio and abundance of gas-phase ions.

The Mass Spectrometry Market is Segmented by Technology (Hybrid Mass Spectrometry (Triple Quadrupole (Tandem), Quadrupole TOF (Q-TOF), and FTMS (Fourier Transform Mass Spectrometry), Single Mass Spectrometry (ION Trap, Quadrupole, and Time-of-Flight (TOF)), and Inductively Coupled Plasma Mass Spectrometry), Application (Chemical Industry, Academic Research, Pharmaceutical and Biotechnology Companies, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers the value (in USD million) for the above segments.

| By Technology | Hybrid Mass Spectrometry | Triple Quadrupole (LC-MS/MS) | |

| Quadrupole Time-of-Flight (Q-TOF) | |||

| Fourier-Transform (FT-MS) | |||

| Single Mass Spectrometry | Quadrupole | ||

| Time-of-Flight (TOF) | |||

| Ion Trap | |||

| MALDI-TOF Mass Spectrometry | |||

| Inductively Coupled Plasma Mass Spectrometry (ICP-MS) | |||

| Others | |||

| By Component | Instruments | ||

| Ionization Sources | |||

| Detectors & Analyzers | |||

| Software & Informatics | |||

| Services | |||

| By Application | Pharmaceutical & Biotechnology | ||

| Clinical Diagnostics & Proteomics | |||

| Food & Beverage Testing | |||

| Environmental Testing | |||

| Chemical & Petrochemical | |||

| Forensic & Toxicology | |||

| Academia & Research Institutes | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest of Middle East & Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

By Technology

| Hybrid Mass Spectrometry | Triple Quadrupole (LC-MS/MS) |

| Quadrupole Time-of-Flight (Q-TOF) | |

| Fourier-Transform (FT-MS) | |

| Single Mass Spectrometry | Quadrupole |

| Time-of-Flight (TOF) | |

| Ion Trap | |

| MALDI-TOF Mass Spectrometry | |

| Inductively Coupled Plasma Mass Spectrometry (ICP-MS) | |

| Others |

By Component

| Instruments |

| Ionization Sources |

| Detectors & Analyzers |

| Software & Informatics |

| Services |

By Application

| Pharmaceutical & Biotechnology |

| Clinical Diagnostics & Proteomics |

| Food & Beverage Testing |

| Environmental Testing |

| Chemical & Petrochemical |

| Forensic & Toxicology |

| Academia & Research Institutes |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the mass spectrometry market?

The mass spectrometry market size stands at USD 7.16 billion in 2025 and is projected to reach USD 10.13 billion by 2030.

Which technology segment is growing the fastest?

MALDI-TOF leads with an expected 11.45% CAGR to 2030 thanks to rapid microbial-identification and tissue-imaging applications.

Why is Asia-Pacific considered the most attractive growth region?

Expanding pharmaceutical manufacturing bases, stricter environmental policies, and rising clinical adoption drive a 10.38% CAGR forecast for Asia-Pacific.

How are software tools influencing buyer decisions?

Validated informatics suites like Empower and MZmine 3 enable regulatory-grade data handling and multimodal analysis, making software a key purchase determinant.

What factors inhibit wider mass spectrometry uptake in developing nations?

High capital costs, limited grant funding, and shortages of trained mass-spectrometrists constrain instrument deployment in emerging markets.

Which clinical application areas show the greatest promise?

Point-of-care pathogen identification and minimal residual disease monitoring in oncology are among the fastest-expanding diagnostic opportunities for mass spectrometry.

Page last updated on: March 18, 2025