Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

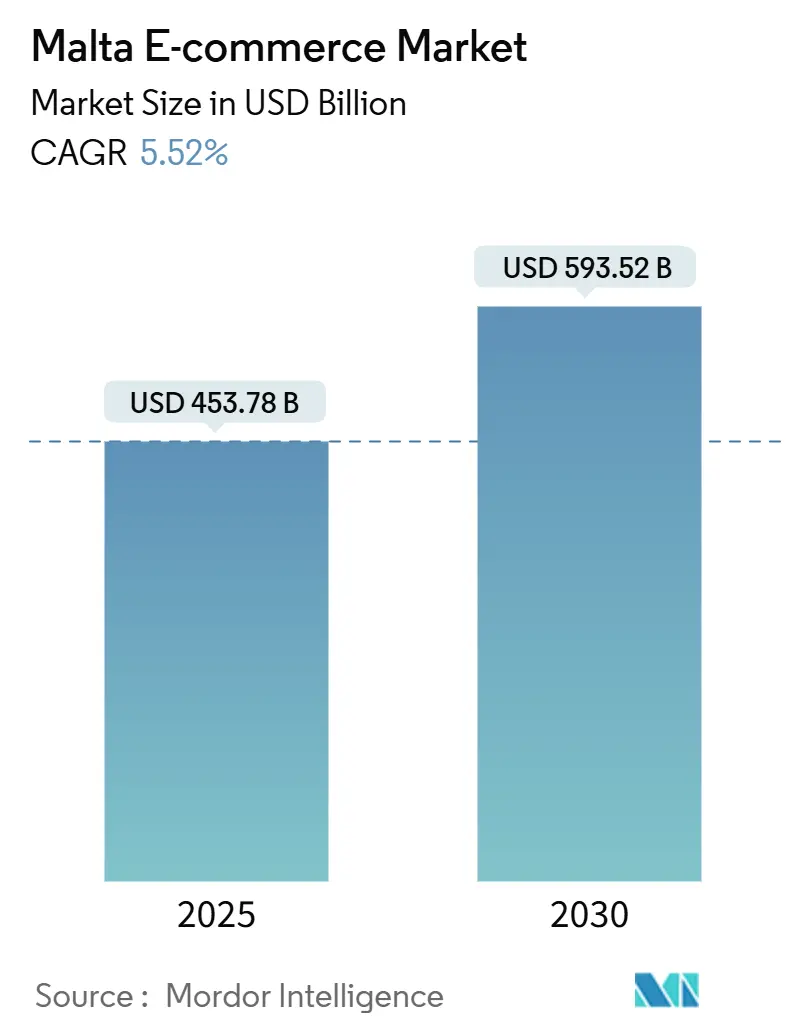

| Market Size (2025) | USD 453.78 Billion |

| Market Size (2030) | USD 593.52 Billion |

| Growth Rate (2025 - 2030) | 5.52% CAGR |

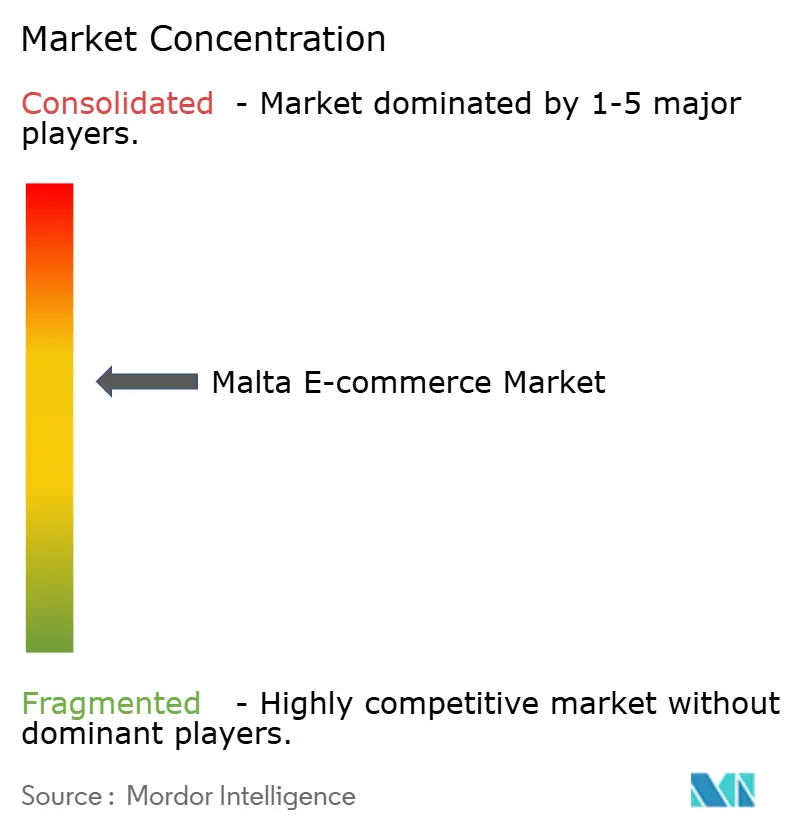

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Malta E-commerce Market Analysis by Mordor Intelligence

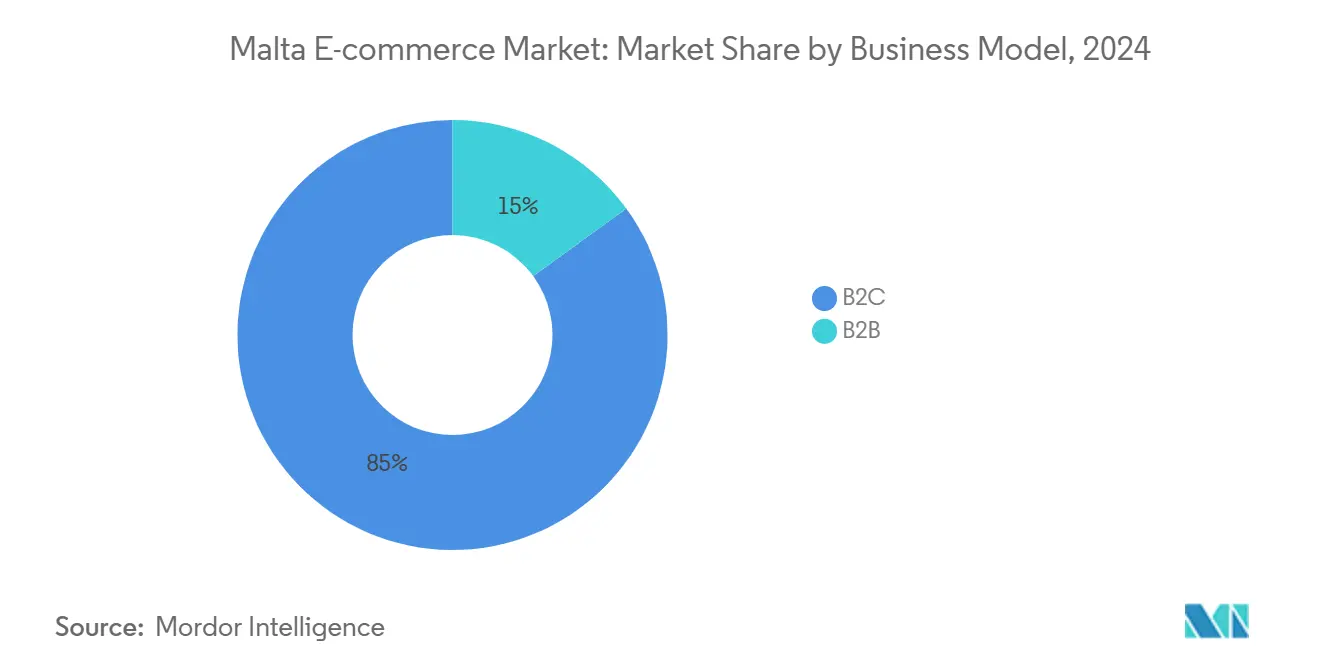

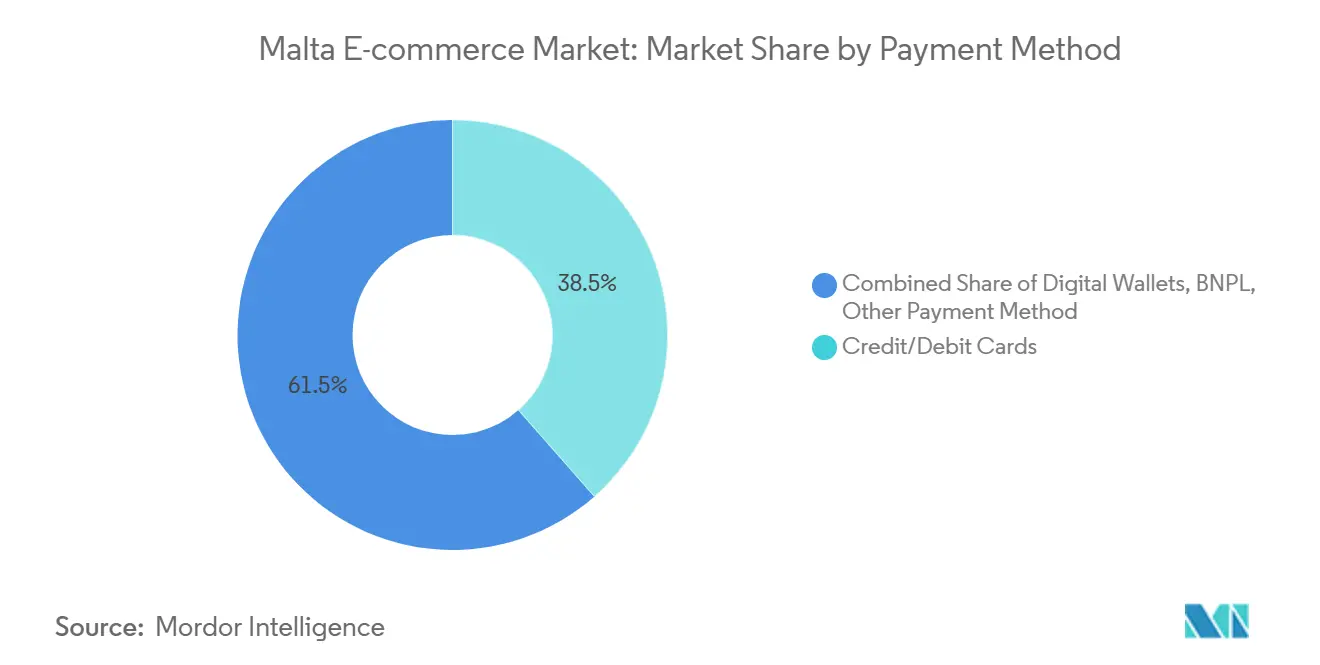

The Malta e-commerce market is valued at USD 453.78 million in 2025 and is on course to reach USD 593.52 million by 2030, translating into a 5.52% CAGR. This momentum reflects Malta’s advantageous Mediterranean location, nationwide fibre broadband that already covers 95% of households, and its sixth-place ranking in the EU Digital Economy and Society Index, all of which enable seamless cross-border trade.[1]European Commission, “Digital Economy and Society Index 2024,” ec.europa.eu Strong English proficiency, a digital-nomad inflow that injected USD 132 million into the economy in 2024, and an EU-aligned payments regime further widen the addressable customer base. Business-to-consumer (B2C) transactions hold 85.02% of the Malta e-commerce market, while business-to-business (B2B) spending is accelerating at 7.21% CAGR through 2030 as Maltese SMEs digitalise under the National eCommerce Strategy 2024-2030.[2]Malta Today, “Malta tops EU cross-border shopping league,” maltatoday.com.mt Mobile commerce now captures 68.04% of all online orders, driven by median mobile speeds of 96 Mbps and widespread 5G availability. Credit and debit cards remain the leading payment option, yet buy-now-pay-later (BNPL) usage is rising at 8.59% CAGR, signalling a shift toward flexible financing.

Key Report Takeaways

- By business model, the B2C segment held 85.02% of the Malta e-commerce market share in 2024; B2B is projected to expand at a 7.21% CAGR to 2030.

- By device type, smartphones accounted for 68.04% of the Malta e-commerce market size in 2024 and are advancing at a 6.46% CAGR through 2030.

- By payment method, credit and debit cards controlled 38.52% of transactions in 2024, while BNPL is the fastest-growing option at 8.59% CAGR to 2030.

- By B2C product category, beauty and personal care led with 25.98% revenue share in 2024; food and beverages will record the highest projected CAGR at 7.03% to 2030.

Malta E-commerce Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nationwide Fibre Broadband Coverage Reaching 95% of Households | +1.2% | National, concentrated in urban centers | Medium term (2-4 years) |

| National eCommerce Strategy 2024–2030 Offering VAT Incentives to SMEs | +0.8% | National, with spillover to EU cross-border | Long term (≥ 4 years) |

| Strong Expat & Digital-Nomad Population Boosting Cross-Border Basket Values | +1.5% | National, with international purchasing patterns | Short term (≤ 2 years) |

| High English Proficiency Enabling Adoption of International Platforms | +0.9% | National, facilitating global platform integration | Medium term (2-4 years) |

| PSD2-Driven Instant Payments Increasing Shopper Trust | +0.6% | National, aligned with EU regulatory framework | Short term (≤ 2 years) |

Source: Mordor Intelligence

Nationwide fibre broadband coverage reaching 95% of households

Investment in gigabit networks has lifted fixed download speeds to 182 Mbps and mobile speeds to 96 Mbps, comfortably above the EU average. High-capacity links remove latency concerns for video-rich catalogues and same-day delivery tracking, enlarging the Malta e-commerce market by bringing late adopters online. Operators also offer competitively priced unlimited plans that appeal to digital nomads who rely on sustained connectivity for remote work. The infrastructure upgrade narrows the urban–rural digital divide, allowing merchants to penetrate smaller towns without additional fulfilment hubs.

National eCommerce Strategy 2024-2030 offering VAT incentives to SMEs

Only 14% of Maltese firms had an online storefront when the strategy launched, so targeted VAT rebates and the MicroInvest tax-credit scheme are critical to onboarding 6,000 additional SMEs by 2027.[3]Malta Enterprise, “Accelerate 2024 scheme,” maltaenterprise.com Grants of up to EUR 100,000 (USD 100,000) under the Accelerate 2024 programme help companies migrate to cloud commerce suites, while the eBiznify eLearning platform builds digital skills. Wider merchant participation fosters price competition, bringing back the 55% of consumers who previously bought abroad due to cost or assortment gaps.

Strong expat & digital-nomad population boosting cross-border basket values

The Digital Nomad Visa admits professionals earning at least EUR 2,700 (USD 2,700) per month and contributed USD 132 million in local spend during 2024. Their preference for premium electronics, wellness items and co-working subscriptions lifts average order values across international marketplaces. First-year tax exemptions free additional disposable income that flows directly into the Malta e-commerce market. Their influence is immediate because nomads transact almost exclusively online and favour retailers offering fast EU-wide shipping and BNPL flexibility.

High English proficiency enabling adoption of international platforms

English is an official language, letting Maltese customers shop on Amazon, eBay and Zalando without localisation hurdles. Merchants likewise access Amazon Seller Central to reach 300 million global buyers, sidestepping translation expenses that slow peers in non-English EU states. B2B suppliers use English documentation to simplify cross-border procurement, supporting the rapid expansion of the Malta e-commerce industry into professional segments.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Domestic Warehouse Space Driving Reliance on Overseas Fulfilment | -1.1% | National, affecting local and international retailers | Medium term (2-4 years) |

| Persistent Cash-on-Delivery Preference | -0.7% | National, particularly in rural areas | Long term (≥ 4 years) |

| Rising Card-Not-Present Fraud Incidents | -0.4% | National, with EU-wide implications | Short term (≤ 2 years) |

Source: Mordor Intelligence

Limited domestic warehouse space driving reliance on overseas fulfilment***

Scarce industrial land keeps rents high and forces merchants to stock inventory in Italy or Germany, adding 2-3 days to standard delivery windows. DHL’s cross-border network handled 1.6 billion parcels in 2023, a 45% uplift since 2019, reflecting rising dependence on foreign hubs. Furniture, DIY and bulky goods sellers face the steepest cost penalty because split consignments cannot exploit local consolidation. Without concerted logistics-park investment, the Malta e-commerce market forfeits speed advantages enjoyed by continental peers.

Persistent cash-on-delivery preference

Maltese shoppers average 2.26 payment cards per capita, yet many businesses stipulate a EUR 5–10 minimum for electronic payments, encouraging cash use. Food-delivery couriers report revenue-share tensions and wage variability linked to cash collections, signalling operational drag. Settling orders at the door raises reversal risk, delays merchant cash flow and complicates fraud checks, trimming the Malta e-commerce market’s margin profile.

Segment Analysis

By Business Model: B2C Entitlement Meets Emerging B2B Upside

Dominant consumer spending positioned the B2C segment at 85.02% of the Malta e-commerce market size in 2024, while the B2B arena is forecast to log a 7.21% CAGR through 2030. High cross-border inclination—89% of Maltese residents buy from other EU sellers—continues to funnel volume toward large international storefronts that exploit Malta’s EU VAT harmonisation. Competitive pressures from Amazon and eBay offer Maltese consumers lower prices and broader SKUs than many domestic merchants can sustain.

Yet demand diversification is surfacing. SMEs eager to secure resilient supply chains now procure software subscriptions, office equipment and financial services online. Government stimulus of EUR 336 million (USD 336 million) under the Recovery and Resilience Plan channels grants into cloud resource planning, catalysing digital procurement cycles. Payment processor RS2 p.l.c. increased revenue to EUR 19.1 million (USD 19.1 million) in 2024 by onboarding regional financial institutions, proving the commercial validity of vertical B2B marketplaces. This structural tailwind suggests double-digit growth pockets even as B2C demand moderates post-pandemic.

For B2C operators, localisation remains the differentiator. Maltasupermarket.com widened its grocery assortment by synchronising with local wholesalers, while Forestals Group bundles after-sales services that overseas sellers cannot replicate cost-effectively. These moves encourage customers to repatriate spend, especially for perishables and white goods. In parallel, B2B platforms leverage Malta’s euro-denominated economy and English documentation to integrate seamlessly with pan-European supply hubs. As the number of VAT-compliant Maltese webshops climbs under the National eCommerce Strategy, a more balanced business-model split will emerge, raising the competitive bar for legacy B2C incumbents.

By Device Type: Smartphone Supremacy Shapes Checkout Design

Smartphones generated 68.04% of orders and are forecast to increase their grip by adding a 6.46% CAGR through 2030, elevating the Malta e-commerce market trajectory. Malta’s median 5G download speed of 206 Mbps enables immersive video demos and augmented-reality try-ons, reducing return rates for apparel and cosmetics. Digital-nomad cohorts using pay-monthly eSIMs transact mainly via mobile wallets, reinforcing the channel’s primacy.

Desktop still holds relevance for multi-SKU B2B orders and high-ticket electronics where spec comparison is critical. Tablet adoption is steady among senior citizens attracted by larger interfaces, supporting inclusion and incremental volume. Smart-TV shopping—while nascent—gains visibility through retailer ad placements during peak streaming hours. Retailers optimise for responsive design and single-click authentication, traits that shorten checkout to under 80 seconds on average.

UX investments are compulsory. Wolt embedded an “Add-to-Basket” widget in its branded app update, boosting mobile conversion by 18%. Similarly, Revolut’s in-app BNPL option pre-populates card details, trimming form-fill friction. As biometric login under PSD2 becomes ubiquitous, device-agnostic security will underpin further smartphone-centric expansion, inscribing mobile as the default journey within the Malta e-commerce market.

By Payment Method: Cards Hold, BNPL Disrupts

Cards owned a 38.52% stake in 2024 transaction value, yet buy-now-pay-later is compounding at 8.59% CAGR, injecting choice into the Malta e-commerce market. BNPL providers exploit PSD2 open-banking APIs to conduct real-time credit scoring, delivering approval in under 30 seconds. Younger shoppers embrace monthly instalments for mid-priced electronics and fashion, while expatriates appreciate the budgeting flexibility during short-term stays.

Digital wallets piggyback on rapid contactless uptake across brick-and-mortar sites, weaving omnichannel loyalty loops. Revolut Business broke the EUR 296 million (USD 296 million) monthly turnover threshold in Malta by bundling FX-free spending, disposable cards, and subscription analytics. For legacy issuers, tokenised credentials and interchange-based incentives keep plastic cards relevant, though margin compression may arise from interchange caps foreseen in forthcoming EU regulations.

Cash-on-delivery endures, especially for groceries and C2C parcels in rural pockets where unbanked rates are elevated. However, courier platforms test “Cash Pick-Up” modules, where drivers reconcile deposits at day-end, reducing float days for merchants. This hybrid system hedges risk in a market that still values physical tender while inching toward a cash-light future.

Note: Segment shares of all individual segments available upon report purchase

By B2C Product Category: Beauty Leadership, Food Momentum

Beauty and personal care owned 25.98% of spend in 2024, confirming Malta’s appetite for premium international labels. Online tutorials and influencer partnerships launch limited-edition drops that sell out within hours, affirming a high-engagement funnel. The Malta e-commerce market size for beauty is forecast to top USD 180 million by 2030, aided by duty-free pricing parity with mainland Europe.

Food and beverages, although just 12.4% of value, will climb at a 7.03% CAGR, the swiftest of any vertical. Wolt’s new gifting feature and partnership with artisanal bakers showcase how logistics innovation can unlock fresh use-cases. Consumers also lean on online grocers for specialty products that reflect Malta’s cosmopolitan palate—gluten-free, vegan and organic items rank among the fastest movers.

Electronics retain outsized share due to cross-border warranty harmonisation and small-parcel dimensions that circumvent warehouse constraints. Furniture sales trail because overseas fulfilment inflates shipping surcharges, yet AR room-planning apps are shrinking decision cycles and may nudge penetration up. Collectively, category dynamics compel merchants to orchestrate flexible sourcing and last-mile alliances if they wish to capture a larger slice of the Malta e-commerce market.

Geography Analysis

Total domestic online expenditure equalled USD 453.78 million in 2025, but 89% of Maltese consumers shop across EU borders and 62% purchase from non-EU sites, embedding the Malta e-commerce market within continental trade lanes. Proximity to Italian and German fulfilment hubs compresses delivery to 2–4 days for most SKUs, although large-format goods can extend to a week.

Malta’s role as a digital conduit in the Mediterranean strengthens regional commerce because its English-language services reduce frictions felt by neighbouring markets. DHL’s 2024 decision to sequence Valletta as a node in its “Med-Hub” program underlines the island’s strategic parcel flow relevance. Shipping-rate normalisation will distil further upside as volumes grow.

Globally, Maltese merchants experiment with US marketplace listings to mitigate domestic scale constraints. Fintech leadership, highlighted by RS2’s tie-up with ACI Worldwide on real-time clearing, equips sellers with bank-agnostic settlement, expediting earnings repatriation. This outward orientation ensures the Malta e-commerce market maintains above-EU-average growth even as more mature economies plateau.

Competitive Landscape

International giants such as Amazon, eBay and Zalando capitalise on cross-docking networks and zero language barriers to anchor top-of-mind awareness among Maltese shoppers. Local specialists—including Maltasupermarket.com in grocery, Forestals Group in appliances, and Scan Malta in IT hardware—craft niche defensibility by offering same-day urban delivery and service add-ons. Consequently, the Malta e-commerce market exhibits moderate fragmentation, with the top five players controlling roughly 55% of GMV.

Technology differentiation drives rivalry. Wolt rolled out a tiered rewards scheme in April 2025 that gamifies order frequency, aiming to lift annual customer value by double digits. Shopify’s SaaS platform wins SME loyalty through one-click EU VAT compliance, while Trust Payments bundles PSD2-ready checkout and in-store terminals under a single contract.

Entry barriers arise from high logistics costs and stringent data-protection norms. However, white-space remains in cross-border returns management, BNPL underwriting tuned to short-stay expatriates, and B2B e-catalogues for the marine and aviation supply segments. Strategic alliances—RS2’s real-time payment project and Revolut’s merchant-acquiring push—signal that infrastructure players will continue to shape competitive outcomes in the Malta e-commerce market.

Malta E-commerce Industry Leaders

-

YellowBit IT Solutions

-

Shein

-

Amazon.com Inc.

-

Zalando SE

-

Apple Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Wolt introduced its gifting module in Malta, allowing customers to append digital cards and schedule deliveries. The feature extends lifetime value by capturing occasion-based purchases and positions Wolt as a diversified lifestyle platform rather than a pure food courier.

- February 2025: Malta’s Digital Nomad Visa generated USD 132 million in 2024, underscoring the strategic importance of high-income expatriates for premium-category GMV. The inflow validates government policy that links residency incentives to digital-services demand and enlarges merchant AOV targets.

- September 2024: Revolut Business crossed EUR 450 million (USD 450 million) in global revenue, with EUR 296 million (USD 296 million) transacted monthly in Malta. The result demonstrates the firm’s success in monetising SME FX and treasury needs, thereby deepening fintech penetration in the Malta e-commerce market.

- August 2024: RS2 p.l.c. lifted turnover to EUR 19.1 million (USD 19.1 million) after partnering with ACI Worldwide on instant payment rails, enhancing merchant authorisation rates and export readiness.

Malta E-commerce Market Report Scope

E-commerce is the purchasing and selling of products and services over the Internet. It is conducted over computers, mobiles, tablets, and other smart devices. There are primarily two types of e-commerce, including Business-to-Consumer (B2C) and Business-to-Business (B2B).

The Malta E-commerce Market is segmented into B2C E-commerce (Beauty and Personal Care, Consumer Electronics, Fashion and Apparel, Food and Beverage, Furniture and Home), and B2B E-commerce.

| By Business Model | B2C |

| B2B | |

| By Device Type | Smartphone / Mobile |

| Desktop and Laptop | |

| Other Device Types | |

| By Payment Method | Credit / Debit Cards |

| Digital Wallets | |

| BNPL | |

| Other Payment Method | |

| By B2C Product Category | Beauty and Personal Care |

| Consumer Electronics | |

| Fashion and Apparel | |

| Food and Beverages | |

| Furniture and Home | |

| Toys, DIY and Media | |

| Other Product Categories |

By Business Model

| B2C |

| B2B |

By Device Type

| Smartphone / Mobile |

| Desktop and Laptop |

| Other Device Types |

By Payment Method

| Credit / Debit Cards |

| Digital Wallets |

| BNPL |

| Other Payment Method |

By B2C Product Category

| Beauty and Personal Care |

| Consumer Electronics |

| Fashion and Apparel |

| Food and Beverages |

| Furniture and Home |

| Toys, DIY and Media |

| Other Product Categories |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Malta e-commerce market?

The Malta e-commerce market is valued at USD 453.78 million in 2025 and is projected to grow to USD 593.52 million by 2030.

Which segment holds the largest Malta e-commerce market share?

B2C transactions dominate with 85.02% of value in 2024, reflecting strong consumer appetite for cross-border shopping.

How fast is mobile commerce growing in Malta?

Smartphones already account for 68.04% of orders and are expanding at a 6.46% CAGR through 2030.

Why is BNPL important for Maltese retailers?

Buy-now-pay-later is the fastest-growing payment method at 8.59% CAGR, helping merchants lift conversion among younger and expatriate shoppers.

What are the main barriers to faster e-commerce growth in Malta?

Warehouse scarcity, persistent cash-on-delivery use, and rising card-not-present fraud currently drag on the market’s full potential.

How does the Digital Nomad Visa influence online retail?

Visa holders spend USD 132 million annually, skewing demand toward premium products and accelerating adoption of international platforms.

Page last updated on: June 27, 2025