Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 9.16 Billion |

| Market Size (2026) | USD 9.66 Billion |

| Market Size (2031) | USD 12.56 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Oil And Gas Market Analysis by Mordor Intelligence

Malaysia Oil And Gas Market size in 2026 is estimated at USD 9.66 billion, growing from 2025 value of USD 9.16 billion with 2031 projections showing USD 12.56 billion, growing at 5.42% CAGR over 2026-2031.

The strong growth outlook for the Malaysia oil and gas market stems from sizable investments in deep-water exploration, downstream petrochemical integration, and an expanding carbon management pipeline. Petronas’ integrated value-chain footprint secures feedstock reliability, while Production Sharing Contract (PSC) revisions continue to attract international partners. Offshore basins in Sarawak and Sabah are set to deliver incremental volumes, and new LNG supply deals preserve Malaysia’s role as a regional gas hub. Meanwhile, constructive fiscal terms and project-ready infrastructure in Peninsular Malaysia accelerate petrochemical capacity additions and reinforce the Malaysia oil and gas market as a Southeast Asian energy pivot. [1]Petroliam Nasional Berhad, “Annual Report 2025,” petronas.com

Key Report Takeaways

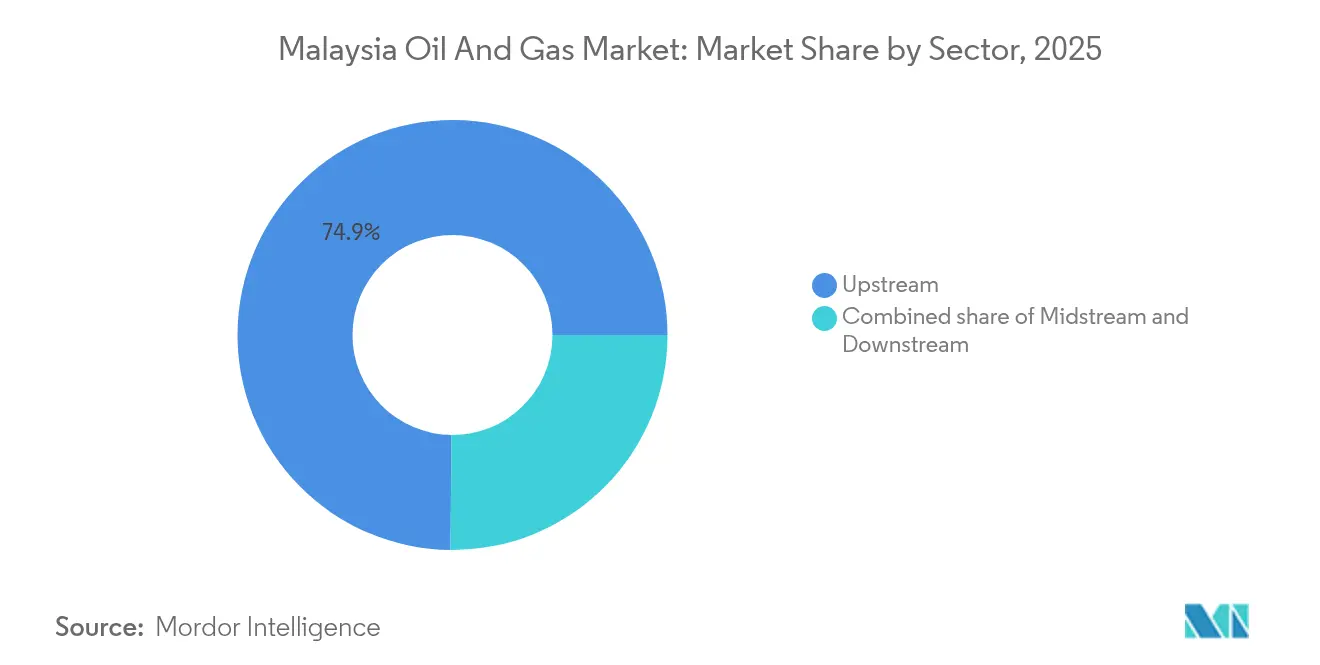

- By sector, upstream commanded 74.85% of the Malaysia oil and gas market share in 2025 and is projected to record the fastest 5.63% CAGR through 2031.

- By location, offshore operations accounted for a 71.10% share of the Malaysia oil and gas market size in 2025 and are expected to advance at a 5.51% CAGR to 2031.

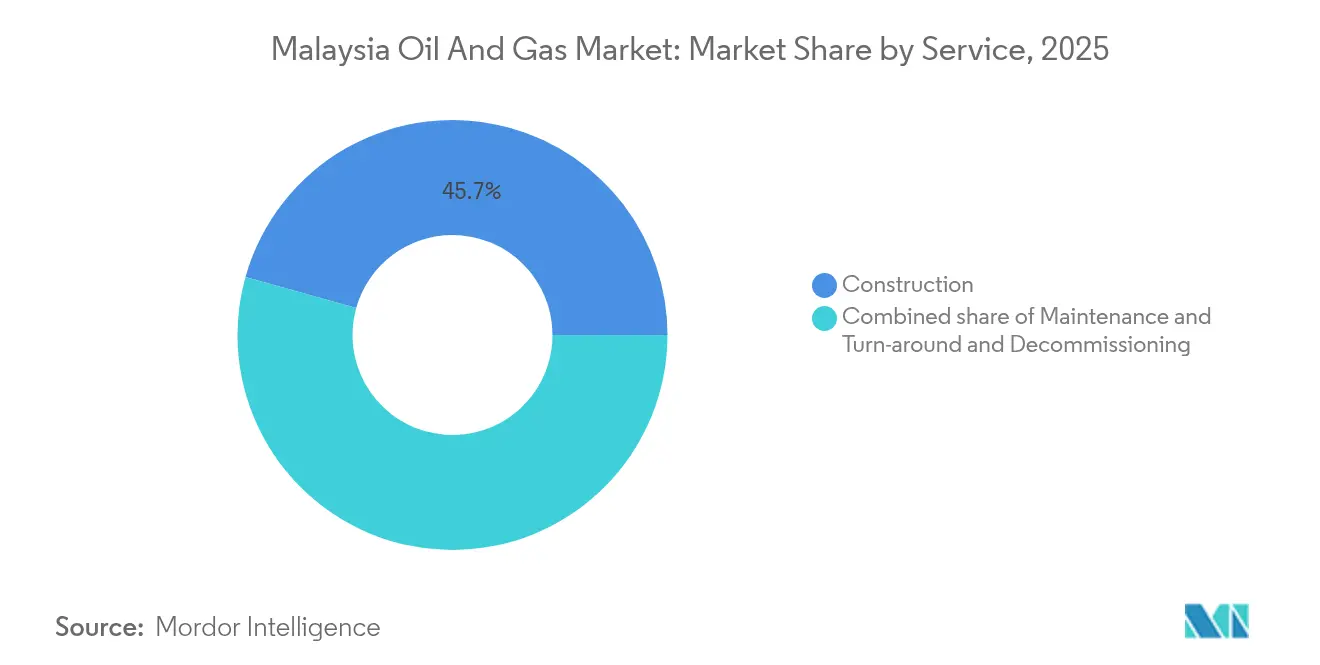

- By service, construction services led with 45.65% revenue share in 2025, while maintenance and turn-around services are forecast to grow at a 5.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Oil And Gas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for refined petroleum products | +1.2% | ASEAN core markets with spillover to broader Asia Pacific | Medium term (2-4 years) |

| Untapped deep-water reserves (Sarawak & Sabah) | +1.8% | East Malaysia offshore basins with regional supply implications | Long term (≥ 4 years) |

| Rising Asian LNG demand lifting Malaysian exports | +1.1% | Regional ASEAN and Northeast Asia markets | Medium term (2-4 years) |

| Incentive-driven PSC revisions & fiscal terms | +1.0% | National with focus on frontier and marginal field development | Short term (≤ 2 years) |

| Downstream petrochemical integration momentum | +1.3% | Peninsular Malaysia with Pengerang hub as primary focus | Medium term (2-4 years) |

| CCUS & blue-hydrogen project pipeline | +0.9% | National with early deployment in Peninsular Malaysia industrial clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Refined Petroleum Products

Regional fuel consumption recovery and new mobility trends stimulate refinery utilization rates across Southeast Asia. The Pengerang Integrated Complex entered commercial service in November 2024 with 300,000 barrels-per-day capacity, underpinning Peninsular Malaysia’s aspiration to supply deficit markets in Indonesia, Vietnam, and the Philippines. Petronas Chemicals is constructing a 33,000-tonnes-per-annum chemical recycling plant due in 2026, embedding circular-economy practices into the downstream landscape. These projects lock in crude intake for upstream producers and frame Malaysia as a processing hub rather than a pure exporter of crude.

Untapped Deep-Water Reserves in Sarawak & Sabah

Frontier acreage in the Langkasuka and Layang-Layang clusters offers sizable gas and condensate potential that requires high-spec rigs, subsea tie-backs, and floating LNG solutions. The Malaysia Bid Round 2025 listed five exploration blocks and three Development and Risk-sharing Option clusters to catalyze investment. ConocoPhillips and Shell have shifted portfolio capital toward gas-weighted developments to maximize LNG feedstock security. The stable PSC framework and Petronas’ role as resource custodian shorten lead times from discovery to first gas, enhancing the long-term competitiveness of the Malaysia oil and gas market.

Rising Asian LNG Demand Lifting Malaysian Exports

Industrial activity and power-sector switching in North Asia sustain a premium on spot LNG, reinforcing Malaysia’s status as the fifth-largest global LNG exporter. The Bintulu complex’s 30 million-tonnes-per-annum capacity allows flexible cargo scheduling that supports both regional spot sales and term contracts. Petronas’ agreement discussions with Commonwealth LNG secure destination diversity, while the Trans Thailand-Malaysia Gas Pipeline offers swing gas between domestic and export markets. Stable LNG margins enable reinvestment in feed-gas fields and new floating regas assets, supporting broader resilience in the Malaysia oil and gas market.

Downstream Petrochemical Integration Momentum

Peninsular Malaysia hosts the RAPID refinery-petrochemical complex that blends crude processing with aromatics and olefins output. New derivative units such as specialty elastomers enhance value capture across the chain. Investor confidence was demonstrated by a USD 3.5 billion project financing closed in December 2024 for the Pengerang Energy Complex, which focuses on paraxylene and benzene streams for Asian polyester demand. Integrated assets drive economies of scale, attract feedstock from East Malaysian fields, and underpin sustained product exports.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High crude-price volatility | -0.8% | Global commodity markets affecting Malaysian operations | Short term (≤ 2 years) |

| Global energy-transition investment shift | -1.1% | International capital markets with domestic policy spillovers | Medium term (2-4 years) |

| ESG-driven capital access constraints | -0.9% | International financing markets affecting major project funding | Medium term (2-4 years) |

| Aging offshore infrastructure & OPEX escalation | -1.0% | Malaysian offshore basins with highest impact on mature fields | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Crude-Price Volatility

Brent fluctuations between USD 70-90 per barrel in 2024-2025 disrupted cash-flow planning, deferred some final investment decisions, and raised borrowing costs. Marginal field economics remain sensitive to price dips, particularly where enhanced recovery requires costly gas lift or chemical injection.[2]The Edge Malaysia, “Volatile Oil Prices Keep Spending in Check,” theedgemalaysia.com The Malaysian Oil, Gas and Energy Services Council’s appeal for fiscal relief underscores exposure to market swings. While hedging and cost optimization help, sustained volatility may temper the pace of deep-water and decommissioning commitments.

Global Energy-Transition Investment Shift

Institutional investors now benchmark portfolios on Scope 1-3 emissions, prompting higher hurdle rates for green-field hydrocarbons. Development banks have tightened lending criteria, favoring renewables and energy-storage projects. Petronas responded with a RM 15 billion diversification pledge toward low-carbon businesses, balancing decarbonization with core hydrocarbon cash generation. Although the Malaysia oil and gas market remains investible, heightened ESG scrutiny lengthens due diligence cycles and raises capital costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Upstream Dominance Drives Growth

The upstream segment captured 74.85% of the Malaysia oil and gas market size in 2025, buoyed by robust PSC activity and Petronas’ project pipeline. Jerun, Kasawari, and Gumusut-Kakap Redevelopment sustain plateau output while offsetting natural decline rates. The Malaysian oil and gas market share leadership in upstream activities reflects a geology rich in gas-condensate plays and a supportive fiscal regime that accelerates field monetization.

Upstream investment momentum will likely continue through 2031 as international operators secure acreage in deep-water wells and marginal redevelopments. Concurrently, midstream operators face rerouting challenges once the Sabah-Sarawak Gas Pipeline retires in 2027, requiring alternative evacuation for East Malaysian gas. Downstream players benefit from new feedstock when upstream debottlenecking releases incremental condensate volumes that feed into Pengerang’s reformers.

By Location: Offshore Leadership Reflects Resource Geography

Offshore production accounted for 71.10% of 2025 volumes and underpins the Malaysian oil and gas market, thanks to mature shelf fields and frontier deep-water discoveries. Subsea tie-backs optimize utilization of a 10,000-kilometer pipeline grid and 380 fixed platforms, enabling quick commercialization of satellite finds.

Decommissioning adds momentum as 37 platforms and 153 wells are slated for removal by 2027, creating revenue streams for plug-and-abandonment contractors. Onshore output, although smaller, remains competitive due to lower lifting costs in mature Peninsular clusters. Cross-border assets such as the Trans Thailand-Malaysia line demonstrate how onshore corridors complement offshore hubs by providing evacuation flexibility.

By Service: Maintenance Gains as Infrastructure Ages

Construction services accounted for 45.65% of the market in 2025, driven by EPC activity on RAPID, Kasawari, and shallow-water redevelopment projects. However, maintenance and turnaround services are anticipated to grow at a rate of 5.72% annually through 2031, mirroring the asset integrity challenges posed by aging infrastructure. Petronas’ RM 4 billion Asset Integrity Backlog Clearance program anchors a multiyear maintenance backlog that spans corrosion mitigation, pipeline pigging, and topside refurbishment.

Specialized decommissioning firms are gaining traction as 56% of Malaysia’s offshore installations exceed their design life. Integrated lifecycle offerings that combine production units with plug-and-abandonment scope, such as T7 Global’s mobile offshore production solution, illustrate service evolution. Digital twins and AUV-based inspection further widen opportunities for technology vendors in the Malaysia oil and gas market.

Geography Analysis

Peninsular Malaysia and the East Malaysian states of Sarawak and Sabah collectively anchor the Malaysia oil and gas market through complementary resource and infrastructure advantages. Peninsular Malaysia is home to the Pengerang Integrated Complex, several legacy refineries, and cross-border gas connections that facilitate supply to Singapore and Thailand. East Malaysia, by contrast, hosts prolific offshore gas plays that feed the Bintulu LNG complex, sustaining export volumes despite rising domestic demand. The differing profiles create intra-country synergies as pipelines and shipping lanes integrate resource flows.

East Malaysian basins attract the bulk of exploration capital due to their deep-water potential, lower sulfur content, and adjacency to North Asian LNG buyers. Petronas and its partners leverage floating production and subsea tie-backs to minimize time to market, while concession terms encourage marginal field clustering, which improves project economics. The Malaysia oil and gas market, therefore, benefits from scale efficiencies in logistics, subsea fabrication, and well services that are concentrated around Labuan and Miri service hubs.

Infrastructure renewal remains a key challenge, particularly the planned decommissioning of the Sabah-Sarawak Gas Pipeline in 2027. Soil instability and geohazard risks have forced repeated shutdowns since 2014, signaling the need for alternative evacuation routes, such as new offshore pipelines or expanded LNG trucking capacity. On Peninsular Malaysia’s west coast, brownfield refineries are upgrading units to Euro 5 specifications, supporting regional product trade and reinforcing Malaysia's oil and gas market as an ASEAN distribution node.

Regulatory Landscape

Malaysia's upstream oil and gas activities are governed by the Petroleum Development Act 1974 (PDA 1974), under which Petroliam Nasional Berhad (Petronas) is the sole custodian of the nation's petroleum resources. Malaysia Petroleum Management (MPM), a unit within Petronas, administers exploration, development, and production through Petroleum Arrangement Contracts (PACs), including PSC variants used for deepwater, late-life assets, and small fields. This determines how international operators and independents access acreage and commercialize resources.

Across the broader value chain, the Petroleum Regulatory Division under the Ministry of Domestic Trade and Cost of Living (KPDN) oversees the marketing, distribution, and export of petroleum products. The Energy Commission (Suruhanjaya Tenaga) regulates downstream gas supply and electricity. Supplier participation is also shaped by Petronas licensing requirements. In April 2026, Petronas issued its License and Registration General Guidelines v15.0, reinforcing standardized online vendor application and registration practices via its licensing system, which affects how oilfield services and equipment providers qualify for upstream work.

Competitive Landscape

Malaysia's oil and gas sector exhibits moderate concentration, primarily driven by Petronas' vertically integrated structure, which spans exploration, pipelines, LNG, and retail. International majors, such as Shell, ExxonMobil, Chevron, and BP, retain PSC stakes that deliver technology transfer and capital inflows, while independents focus on monetizing marginal fields. Digitalization has emerged as a competitive lever: Petronas deploys cloud-native subsurface analytics through AWS and Geoteric, SLB operates an Innovation Factori in Kuala Lumpur, and Halliburton enables real-time drilling advisory systems.

White-space prospects are evident in carbon capture and decommissioning. Kasawari CCS represents a first-mover template, providing Petronas with the opportunity to offer hub services to regional emitters. Service providers with well-plugging expertise, including T7 Global and EPIC OG, capture early contracts as the decommissioning wave accelerates. Midstream consortia explore the feasibility of a hydrogen corridor, signaling a diversification pathway under Malaysia's National Energy Transition Roadmap.

Petronas sustains a competitive advantage through economies of scale, local supplier networks, and preferential access to acreage. However, the high-grading of international operators' portfolios and their finance discipline intensify bidding competition for high-return assets. Domestic service players respond by forming alliances with technology vendors, extending scope from construction to full asset lifecycle management, and leveraging digital platforms to cut costs. These shifts collectively reinforce resilience and innovation across the Malaysia oil and gas market.

Malaysia Oil And Gas Industry Leaders

Shell Plc.

Petroliam Nasional Berhad (Petronas)

Exxon Mobil Corp.

Sapura Energy Bhd

Hibiscus Petroleum Bhd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace in upstream is focused on monetizing discovered and ready-to-develop resources, and on capability demand tied to complex offshore execution. Petronas launched Malaysia Bid Round 2026 in February 2026, featuring Discovered Resource Opportunities (DRO). It indicates an active pathway for contractors and partners to secure work around appraisal-to-development, brownfield tie-backs, and production optimization in offshore Sarawak and Sabah. This also supports demand for remedial sand control, tubular running, and integrity programs as operators push recovery from mature and marginal assets while managing declining baselines.

On transition-linked projects, policy and program anchors are creating investable adjacencies around low-carbon fuels and carbon management, without displacing the core hydrocarbons value chain. The National Energy Transition Roadmap (NETR) frames three CCUS hubs by 2030 (two in Peninsular Malaysia and one in Sarawak), with an indicated 15 MTPA CO2 storage capacity. This supports opportunities for subsurface evaluation, compression and transport, and hub services around industrial clusters and gas developments such as Kasawari. Downstream diversification is also becoming more concrete: in November 2025, Pengerang Biorefinery Sdn. Bhd. (a JV between Petronas, Enilive, and Euglena) broke ground on a biorefinery in Pengerang, Johor, designed for 650,000 tonnes per year of renewable feedstock. That adds demand for logistics, storage, and integration services across the Pengerang complex.

Recent Industry Developments

- July 2026: Reservoir Link Energy Bhd secured a five-year contract from PETRONAS Carigali Sdn Bhd to provide remedial sand control equipment and services, with the contract starting May 21, 2026. The award underscores continued spending on production optimization and well intervention solutions across Malaysia's offshore portfolio, supporting demand for specialized oilfield services.

- June 2026: Petronas and Eni established Searah as a 50:50 joint venture covering selected assets in Malaysia and Indonesia. The move consolidates operational focus and portfolio management across the region and affects upstream investment prioritization and the pipeline of work for engineering, operations, and maintenance contractors supporting these assets.

- May 2026: Shell Malaysia Trading Sdn Bhd broke ground for the expansion of the Westport Fuels Terminal at Port Klang, Selangor, adding three new gasoline and diesel storage tanks, with completion targeted for early 2028. The project strengthens downstream storage and distribution resilience around a key logistics node, supporting fuel supply continuity and higher throughput capability for domestic and regional trade flows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the Malaysia oil and gas market is sized as the value generated from upstream, midstream, and downstream activities that support producing, moving, processing, and supplying crude oil and natural gas within Malaysia.

Scope exclusions: Retail fuel marketing margins and broad petrochemicals that are not directly linked to oil and gas chain activities are excluded where they cannot be cleanly attributed.

Segmentation Overview

- By Sector

- Upstream

- Midstream

- Downstream

- By Location

- Onshore

- Offshore

- By Service

- Construction

- Maintenance and Turn-around

- Decommissioning

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base on Malaysia production, trade, and operating activity before assumptions were built. We leaned on public statistics and technical releases that can be checked and repeated, such as Malaysia energy ministry publications, the national statistics department, customs and trade data portals, and global energy agencies that publish country energy balances.

To translate activity into market value, additional context was taken from items such as public company annual reports, investor presentations, project announcements, and reputable industry press. In a few cases, paid subscriptions for company financials and for shipment-level trade intelligence were used to sanity-check revenues, import flows, and timing of major equipment or service demand. These examples are illustrative only, and many other sources were also referred to for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work was run to confirm what the secondary data could not explain clearly, especially the split of spending across offshore and onshore activity, project timing, and typical price movements in services and processing. We spoke with a mix of asset operators, EPC and service providers, logistics and terminal stakeholders, and downstream participants, and then used their inputs to validate assumptions across Malaysia and the key trading corridors linked to its LNG and crude flows.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 21% | |

| Mid tier: 51% | Functional/Unit leaders: 35% | |

| Smaller Players: 22% | Managers: 44% |

Market-Sizing & Forecasting

Sizing started with a top-down build where Malaysia oil and gas activity indicators were converted into value using realistic price and cost relationships. For upstream, the demand pool was tied to crude and gas production levels, offshore versus onshore activity mix, and the pace of development and maintenance work. For midstream and downstream, throughput and utilization signals were used where available, and then the model was aligned with observable trade and supply patterns.

Those totals were then checked through selective bottom-up approximations, including sampled service-rate benchmarks multiplied by activity units, and roll-ups from disclosed revenue exposure for relevant business lines when the disclosures were clear. When a segment had limited direct disclosure, we used proxy variables, such as active rig and vessel support needs, LNG cargo trends, refinery run rates, and the project pipeline timing, and then adjusted ranges based on what interviewees said was realistic.

For forecasting, scenario analysis was used so the outlook could respond to commodity price ranges, expected project sanctioning, and policy or regulatory signals that affect activity levels. The final forecast path was chosen after comparing scenario outputs with expert expectations on production outlook, planned shutdown schedules, and the likely pace of new capacity additions.

Data Validation & Update Cycle

Outputs were triangulated through multiple checks, where model totals were compared against independent signals like production series, trade flows, and known project milestones. Outliers were investigated, and where gaps were driven by timing or classification differences, the assumptions were revised and then re-tested so the logic stayed consistent across the time series.

Before sign-off, the model and narrative go through multi-step analyst review, including variance checks across segments and cross-validation against interview notes. Reports are refreshed annually, and interim updates are triggered when material events occur, such as large project sanctions, major outages, or sharp price shifts. Right before delivery, a final data pass is completed so clients receive the latest view available.

Mordor Intelligence's Malaysia Oil and Gas Market Estimate Compared With Other Published Estimates

Published market sizes for Malaysia oil and gas often look different because the scope boundary is not the same, and because each publisher uses its own mix of activity indicators and pricing assumptions. Timing also matters since some estimates anchor on a different base year and then apply a single growth path across the value chain.

Key gaps usually come from whether downstream products and petrochemical-linked value are blended into the total, how LNG and export-linked volumes are priced, and whether the model counts only Malaysia-located activity or also includes value created outside the country for exported barrels. Currency conversion timing and refresh cadence can widen the spread further, especially in years with big commodity price swings.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.66 B (2026) | |

| Industry Publisher A | USD 11.44 B (2024) | This figure appears to anchor on a different base year and it also describes a broader value chain that can blend in refining and petrochemical-linked value, which lifts the total versus activity that is strictly attributable to Malaysia oil and gas chain work. |

| Industry Publisher B | USD 11.00 B (2024) | This estimate is presented at an integrated sector level and may apply wider category coverage across products and compliance buckets, with less visibility on how prices and volumes were converted into USD for the sizing year. |

The table shows that the spread is largely explained by base-year choice and what is counted inside the total, and in Mordor Intelligence's model the value is tied back to sector activity indicators and segment-level volume signals rather than bundling in adjacent downstream product value when attribution is unclear.

Key Questions Answered in the Report

How large is the Malaysia oil and gas market in 2026?

The Malaysia oil and gas market size is USD 9.66 billion in 2026.

What is the expected CAGR for Malaysian oil and gas through 2031?

The market is forecast to grow at 5.42% annually through 2031.

Which segment holds the largest share of Malaysia’s hydrocarbon value chain?

Upstream activities accounted for 74.85% share in 2025.

What drives investment in offshore Sarawak and Sabah?

Untapped deep-water reserves and supportive PSC terms attract international operators.

How is Malaysia addressing asset-end-of-life challenges?

Petronas has launched a multi-year decommissioning program covering 153 wells and 37 platforms, creating opportunities for specialist service providers.

Page last updated on: