Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

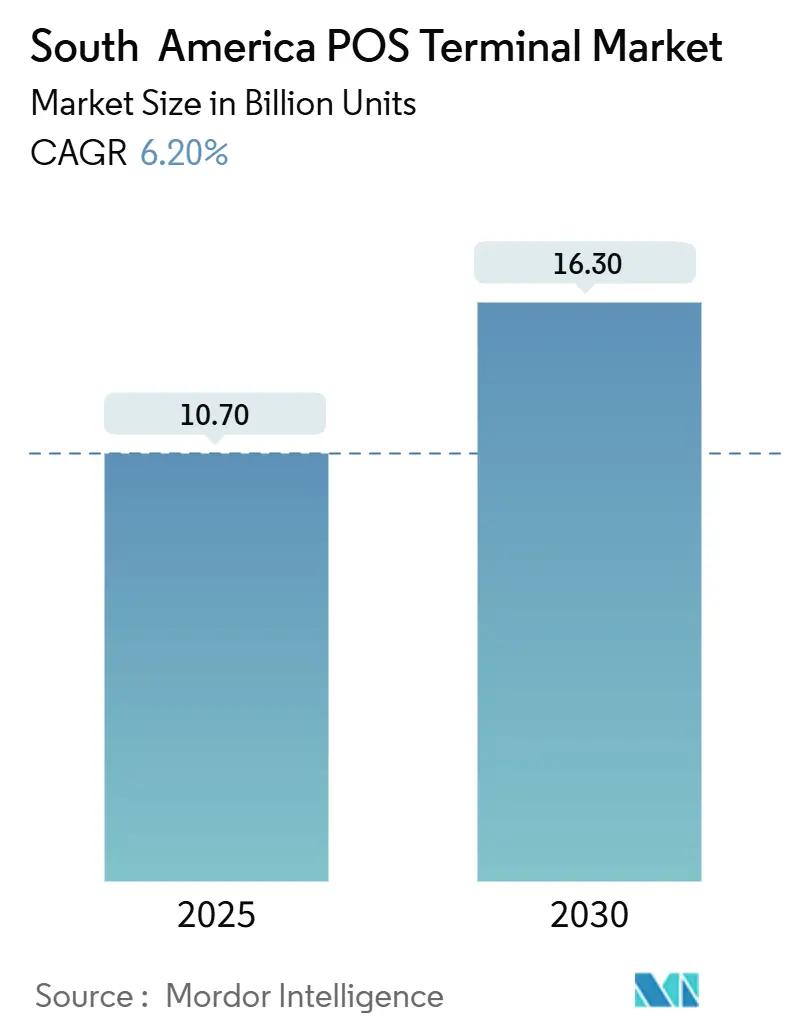

| Market Volume (2025) | 10.70 Billion units |

| Market Volume (2030) | 16.30 Billion units |

| Growth Rate (2025 - 2030) | 6.20% CAGR |

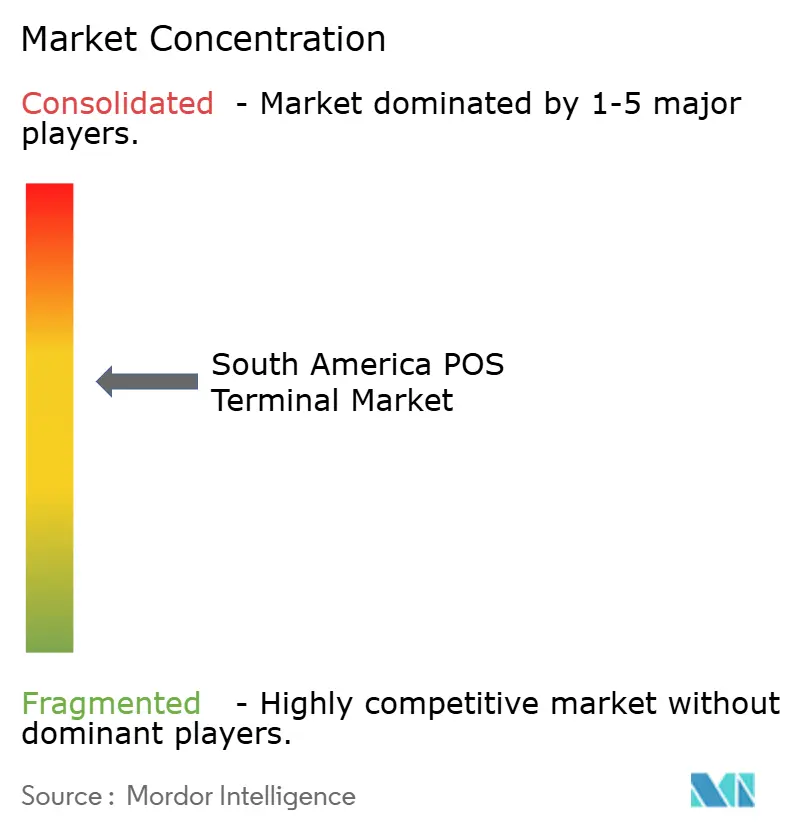

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America POS Terminal Market Analysis by Mordor Intelligence

The South America POS Terminal Market size is estimated at 10.70 billion units in 2025, and is expected to reach 16.30 billion units by 2030, at a CAGR of 6.20% during the forecast period (2025-2030). The expansion is fueled by government instant-payment schemes such as Brazil’s PIX and Mexico’s DiMo, rapid contactless adoption, and fintech-led merchant digitization initiatives. Android-based smart terminals are shifting merchant expectations from simple payment acceptance to full-service business hubs, while transit agencies deploy unattended validators that open new hardware niches. Competitive strategies are increasingly centered on software ecosystems, driving recurring revenue beyond interchange fees. Meanwhile, pricing pressure from account-to-account (A2A) rails and rising PCI-DSS compliance costs temper hardware margins but also accelerate product differentiation as vendors bundle value-added services.

Key Report Takeaways

- By mode of payment, mobile and portable POS systems led with 63.72% South America POS Terminal market share in 2024.

- By pos type, mobile units generated 63.72% of 2024 shipments and are forecast to post a 7.65% CAGR through 2030.

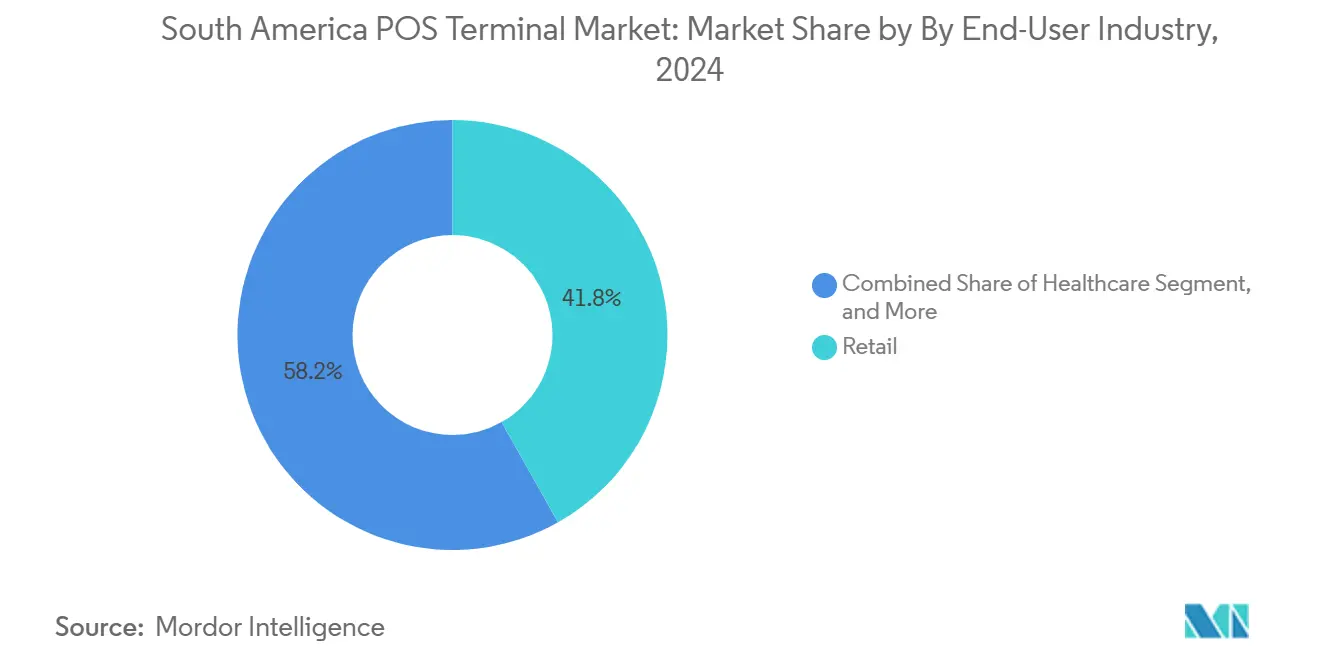

- By end-user, retail captured a 41.83% share of the South America POS Terminal market size in 2024, while transportation and logistics advanced at a 6.99% CAGR through 2030.

- By country, Brazil held 34.72% revenue share in 2024; Argentina is forecast to expand at a 7.1% CAGR to 2030.

- PAX Technology, Ingenico, and VeriFone collectively controlled about 65% of unit shipments across South America in 2024.

South America POS Terminal Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lower total cost of ownership than cash handling | +1.2% | Brazil, Mexico, Colombia | Medium term (2-4 years) |

| Contactless and mobile payment surge post-pandemic | +1.8% | Brazil, Argentina | Short term (≤2 years) |

| Mandatory digitization of micro-merchant payments | +1.5% | Brazil, Mexico, Argentina | Long term (≥4 years) |

| Expansion of fintech acquirers and payment aggregators | +1.1% | Mexico, Chile, Peru | Medium term (2-4 years) |

| Android smart POS becoming merchant business hub | +0.9% | Brazil, Mexico, Argentina | Long term (≥4 years) |

| Urban transit roll-outs of unattended validators | +0.7% | Panama, Uruguay, Costa Rica | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lower total cost of ownership than cash handling

Modern terminals reduce cash-management losses, automate settlement, and integrate inventory functions. Castles Technology’s Android units tripled merchant productivity in pilot programs, resulting in over 4 million fintech-deployed terminals in Mexico, compared to 1.4 million bank devices. Hardware vendors now bundle analytics dashboards and working-capital loans that convert one-time sales into subscription revenue, reinforcing adoption momentum among micro-merchants.

Contactless and mobile payment surge post-pandemic

COVID-19 shifted consumer behavior toward tap-and-go and QR code payments. NFC transactions now account for more than 50% of face-to-face card volumes in Brazil, and PIX Contactless has been live since February 2025, combining instant settlement with touch-free convenience, thereby increasing merchant demand for dual-interface devices.[1]Banco Central do Brasil, “PIX Statistics,” BCB.GOV.BR Argentina’s interoperable QR framework logged a 278% year-over-year growth in April 2024, confirming a sustained preference for contactless payment acceptance.

Mandatory digitization of micro-merchant payments

Regulators tie tax collection and financial-inclusion goals to merchant digitization. PIX handled 42 billion transactions in 2024, while Argentina’s Transferencias 3.0 caps merchant fees at 0.07%, pushing even street vendors to install POS readers. Mexico’s DiMo option on SPEI rails complements CoDi QR to cover all instant-payment use cases, embedding POS deployment into compliance checklists for small businesses.

Expansion of fintech acquirers and payment aggregators

API-first fintechs simplify onboarding, undercut legacy acquiring fees, and embed value-added software. tapi’s 1,000% revenue spike in 2024 underscores how cloud-native platforms scale merchant networks rapidly. Their open SDKs favor Android smart terminals, pressuring traditional vendors to launch app marketplaces and revenue-sharing models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security and PCI-DSS Compliance Costs | -0.8% | Regional, with highest impact in Brazil, Mexico | Long term (≥ 4 years) |

| High Informality and Cash Preference in Rural Areas | -1.2% | Peru, Colombia rural areas, Mexico interior | Long term (≥ 4 years) |

| Supply-chain Volatility for Secure Chipsets | -0.6% | Global supply chain affecting all countries | Medium term (2-4 years) |

| Aggressive Pix/A2A Pricing Eroding Card-POS Economics | -0.9% | Brazil, Argentina, with expansion to Mexico, Colombia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cybersecurity and PCI-DSS compliance costs

PCI-DSS v4.0.1 expands authentication, key management, and monitoring mandates, driving recurring audit expenses that small merchants struggle to afford. Terminal manufacturers must secure firmware updates and maintain device attestation, which raises bill-of-materials costs and complicates rollouts in fragmented regulatory environments.

High informality and rural cash preference

Rural economies rely on cash due to patchy connectivity and cultural habits. Informality trims financial-account penetration by up to 12 percentage points in Peru, shrinking the addressable POS base. In Colombia’s countryside, cash remains the dominant payment method in more than 60% of transactions, despite the increasing adoption of digital wallets in urban areas. Vendors address the gap with 4G-enabled mini POS devices and offline-capable QR readers, but profitability remains challenging.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment Acceptance: Contact-based strength amid contactless surge

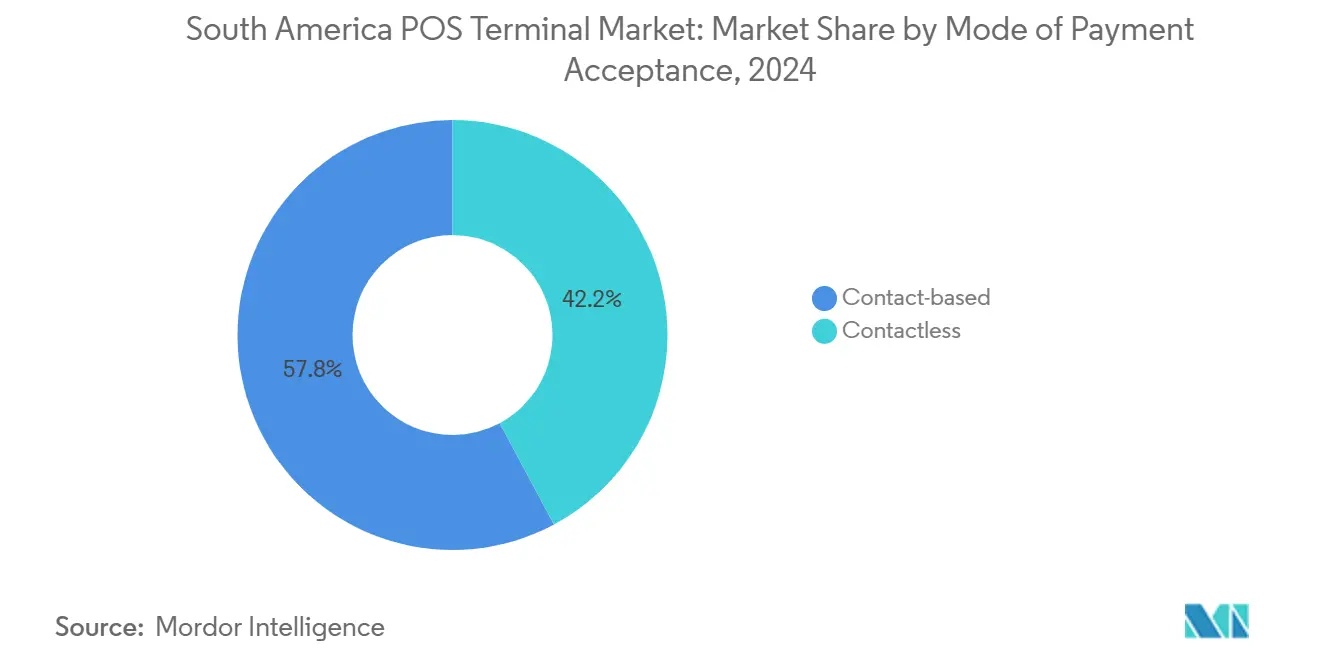

Contact-based EMV transactions accounted for 57.83% South America POS Terminal market share in 2024, reflecting entrenched chip-card infrastructure. Yet contactless volumes grow at a 7.23% CAGR as NFC cards and digital wallets proliferate. Argentina’s unified QR scheme handled 35.7 million transactions in April 2024, while Brazil’s PIX Contactless is set to accelerate NFC adoption further. Merchants increasingly demand dual-interface readers to future-proof investments and capture both traditional card and instant-payment traffic. Device vendors bundle QR scanners and large touchscreens, allowing software-switchable acceptance modes without additional hardware swaps.

Second-order effects include acquirers reshaping fee models as contactless A2A rails undercut interchange economics. Some Brazilian merchants already route low-ticket items to PIX to avoid MDR fees, while high-value purchases stay on credit card installments. Terminal providers respond with dynamic routing engines at the device level, maximizing savings for merchants and cementing hardware relevance in an omnipayment world.

By POS Type: Mobile and portable systems redefine merchant workflows

Mobile units generated 63.72% of 2024 shipments and are forecast to post a 7.65% CAGR through 2030, highlighting how merchants value portability and app ecosystems. Smart devices like PAX’s A920 combine barcode scanners, cameras, and LTE modules, letting vendors upsell inventory or delivery apps post-deployment. For large retailers, fixed terminals remain essential for cash drawers and receipt printers; however, the focus shifts to tablet-style systems that sync with cloud-based ERP systems. Logistics firms utilize handheld readers for proof-of-delivery payments, while table-service restaurants employ portable terminals to expedite checkout time and increase table turnover.

Security enhancements, including fingerprint login, point-to-point encryption, and secure-boot chips, counter rising fraud threats and satisfy stringent Brazilian and Mexican cybersecurity norms. Battery life and ruggedness also improve as vendors target outdoor markets, such as food trucks and event merchants.

By End-User Industry: Retail dominance faces transit-driven growth

Retail held 41.83% South America POS Terminal market size in 2024, benefiting from dense merchant bases and multi-lane checkout needs. Nonetheless, transportation registers the highest 6.99% CAGR, powered by open-loop fare collection across metros and bus operators. Panama Metro’s contactless deployment, Mexico City Metro’s validator upgrades, and Costa Rica’s SINPE-TP integration illustrate mobility’s appetite for specialized POS hardware. Hospitality follows closely as table-side ordering integrates with payment in one workflow, boosting average ticket sizes and tipping transparency.

Healthcare deployments gain momentum via teleconsultation kiosks and clinics seeking compliant card-on-file capabilities. Meanwhile, micro-verticals such as education and government service centers tap unattended payment kiosks to reduce cash handling, adding long-tail demand for industrial-grade terminals.

Geography Analysis

Brazil generated 34.72% of regional revenue in 2024 and is forecast at a steady 6.89% CAGR as replacement cycles dominate. The South America POS Terminal market size in Brazil benefits from PIX-driven software upgrades rather than greenfield installs. PAX enjoys a roughly 50% market share, underpinned by a deep reseller network and domestic manufacturing incentives. Argentina, in contrast, grows at 7.1% CAGR thanks to Transferencias 3.0 and QR interoperability, which push merchants to install camera-equipped smart POS. Mexico mirrors Argentina’s fintech dynamic, with 4 million aggregator-deployed terminals eclipsing bank devices. Colombia, Chile, and Peru sit at earlier adoption curves but gain policy tailwinds such as Colombia’s Bre-B instant-payment launch in May 2025 that portend rapid uptake.

Brazil remains the anchor of the South America POS Terminal market, leveraging 42 billion PIX transactions in 2024 to justify ongoing device refreshes and app upgrades. The upcoming contactless PIX capability requires NFC-enabled readers, prompting 2025 procurement cycles among the 9 million active merchants. Tax credits on locally manufactured electronics bolster domestic assembly lines for PAX and Ingenico, providing inventory resilience amid global chipset shortages.

Argentina’s regulatory push makes QR- and NFC-ready hardware table stakes. Monthly interoperable transactions exceeded 100 million by December 2024 as merchants embraced capped fees and instant settlement, driving twin-digit shipment growth for smart POS vendors. Currency volatility also nudges consumers toward wallet balances, reinforcing digital acceptance expansion.

Mexico’s fintech ecosystem transforms the country into the second-largest South America POS Terminal market. Aggregators like Mercado Pago and Clip prioritize Android-based devices that embed loyalty and credit offers, displacing legacy bank-locked terminals. DiMo’s phone-number payment rail expands acceptance beyond QR to USSD-light experiences, requiring firmware updates rather than new hardware, thereby extending device life cycles while locking merchants into software subscriptions.

Secondary markets such as Colombia and Peru record accelerating wallet penetration. Colombia processed COP 332 trillion through digital wallets in 2024, and the Bre-B scheme aims to replicate PIX’s adoption curve, implying a near-term spike in low-cost mobile POS demand.[2]Bold, “Bold Fintech Colombia Digital Payments Growth,” BOLD.CO Peru’s rural cash holdout slows penetration, but government connectivity programs and 4G expansion create inflection points for micro-merchant onboarding.

Competitive Landscape

Established hardware leaders PAX Technology, Ingenico, and VeriFone hold a combined 65% unit share, giving the South America POS Terminal market a moderate concentration profile. PAX exploits regional manufacturing hubs and mid-tier price points to dominate Brazil and gain traction in Argentina and Chile. Ingenico counters with high-spec Android terminals and alliances with acquirers like Fiserv, securing premium segments that value reliability and compliance. VeriFone leverages its Carbon series for multilane retailers but faces share erosion in micro-merchant niches captured by fintech bundles.

Fintech-driven entrants, including Mercado Pago, Clip, and PagSeguro, reset competitive benchmarks through vertically integrated offerings. Their ability to subsidize hardware by acquiring or lending revenue compresses average selling prices and forces incumbents to pivot toward software ecosystems. Chinese OEMs such as Newland win contracts on price and rapid customization, as evidenced by its CIELO supplier award in Brazil.[3]Newland Payment Technology, “Newland Payment clinches Best Supplier Award,” NEWLANDNPT.COM

Strategic moves center on platform economics. PAX opened an app marketplace that shares subscription revenue with ISVs, while Ingenico pilots Device-as-a-Service plans bundling hardware, warranty, and cloud POS in a single monthly fee. Partnerships between acquirers and transit integrators, like SONDA with local banks, signal vertical diversification to capture fare-collection budgets.

South America POS Terminal Industry Leaders

VeriFone System Inc.

Ingenico S.A.

Castles Technology Co., Ltd.

NCR Corporation

BBPOS Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Brazil’s central bank launched PIX Contactless, enabling NFC-based instant transfers at the point of sale.

- February 2025: tapi and Mercado Pago formed a strategic alliance to scale SME acceptance in Mexico.

- January 2025: Argentina’s BCRA set April 2025 launch for debit-card QR payments under Transferencias 3.0.

- July 2024: Itaú Unibanco acquired NCR Atleos retail software assets to deepen in-house POS capabilities.

South America POS Terminal Market Report Scope

The POS Terminals market captures revenues generated from hardware, software, and services that facilitate transactions during the sale of a product or service. It helps to store, capture, share, and report data related to sales transactions.

The South America POS Terminal Market Report is Segmented by Mode of Payment Acceptance (Contact-Based and Contactless), POS Type (Fixed Point-Of-Sale Systems, and Mobile/Portable Point-Of-Sale Systems), End-User Industry (Retail, Hospitality, Healthcare, Transportation and Logistics, and Other End-User Industries), by Country (Brazil, Argentina, Colombia, Chile, Peru, Rest of South America). The Market Forecasts are Provided in Terms of Value (Units).

It enhances the shopping experience and helps expedite the checkout process, ultimately resulting in customer satisfaction. Inventory management, stock on hand, product availability, and pricing information are primary data acquired from the systems. The study also covers the impact of COVID-19 on the market and its affected segments.

By Mode of Payment Acceptance

| Contact-based |

| Contactless |

By POS Type

| Fixed Point-of-Sale Systems |

| Mobile / Portable Point-of-Sale Systems |

By End-User Industry

| Retail |

| Hospitality |

| Healthcare |

| Transportation and Logistics |

| Other End-User Industries |

By Country

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Mode of Payment Acceptance | Contact-based |

| Contactless | |

| By POS Type | Fixed Point-of-Sale Systems |

| Mobile / Portable Point-of-Sale Systems | |

| By End-User Industry | Retail |

| Hospitality | |

| Healthcare | |

| Transportation and Logistics | |

| Other End-User Industries | |

| By Country | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is the current value of the South America POS Terminal market?

The market stands at USD 10.7 billion Units in 2025 and is forecast to reach USD 16.3 billion Units by 2030.

Which POS segment is growing fastest in South America?

NFC-enabled contactless terminals are advancing at a 7.23% CAGR through 2030.

How significant is Brazil within South America’s POS landscape?

Brazil accounts for 34.72% of revenue and drives upgrade demand via PIX Contactless and domestic production incentives.

Which companies lead the South America POS Terminal competitive field?

PAX Technology, Ingenico, and VeriFone together command roughly 65% of shipments across the region.

What regulatory changes impact POS adoption in Argentina?

Argentina’s Transferencias 3.0 mandates QR interoperability with capped merchant fees, spurring rapid smart POS deployment.

Why are mobile POS devices favored by South American merchants?

They offer portability, integrated business apps, and LTE connectivity that align with micro-merchant needs and fintech acquiring models.

Page last updated on: