Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

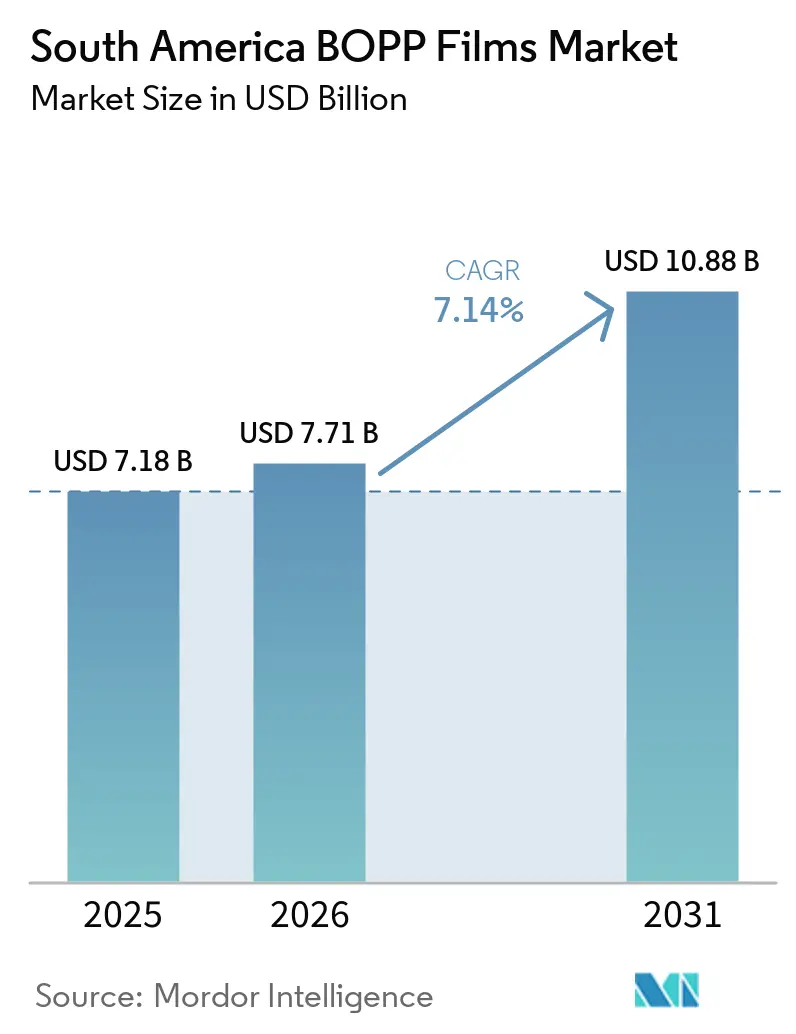

| Base Year Market Size (2025) | USD 7.18 Billion |

| Market Size (2026) | USD 7.71 Billion |

| Market Size (2031) | USD 10.88 Billion |

| Growth Rate (2026 - 2031) | 7.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America BOPP Films Market Analysis by Mordor Intelligence

The South America BOPP films market size was valued at USD 7.18 billion in 2025 and estimated to grow from USD 7.71 billion in 2026 to reach USD 10.88 billion by 2031, at a CAGR of 7.14% during the forecast period (2026-2031). Robust retail expansion, accelerating cross-border e-commerce activity, and exporters’ preference for lightweight mono-material packs together underpin volume gains. Transparent grades remain the workhorse of everyday food and label applications, while metallized and anti-fog variants capture sustainability premiums as brand owners pivot to recyclable structures. Brazil anchors regional demand, yet Peru, Chile, and Colombia are outpacing the average on the back of fresh-produce exports and cold-chain investments. Strategic capacity additions by large converters, coupled with new resin sourcing options, are reshaping bargaining power along the value chain.

Key Report Takeaways

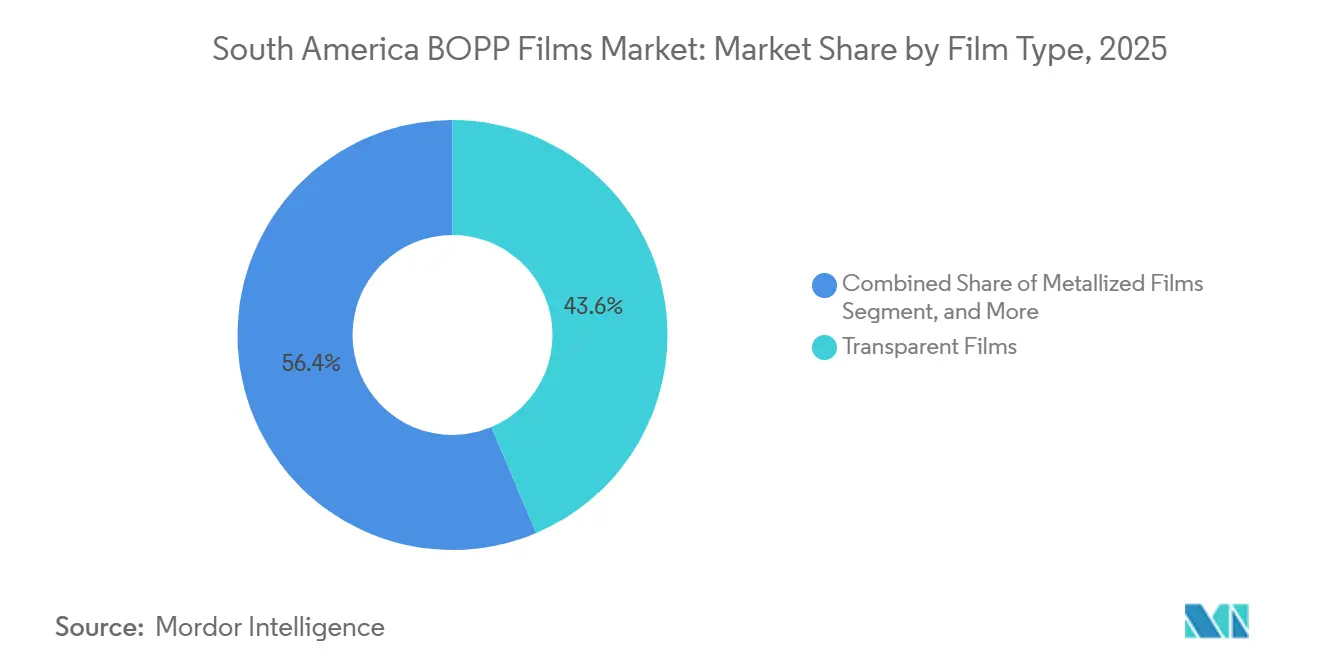

- By film type, transparent grades accounted for 43.63% of the South America BOPP film market share in 2025, while anti-fog and other functional grades are projected to advance at a 7.79% CAGR through 2031.

- By thickness, 20-30 µm films accounted for 39.39% share of the South America BOPP films market size in 2025, while films above 45 µm are forecast to post the fastest 8.01% CAGR to 2031.

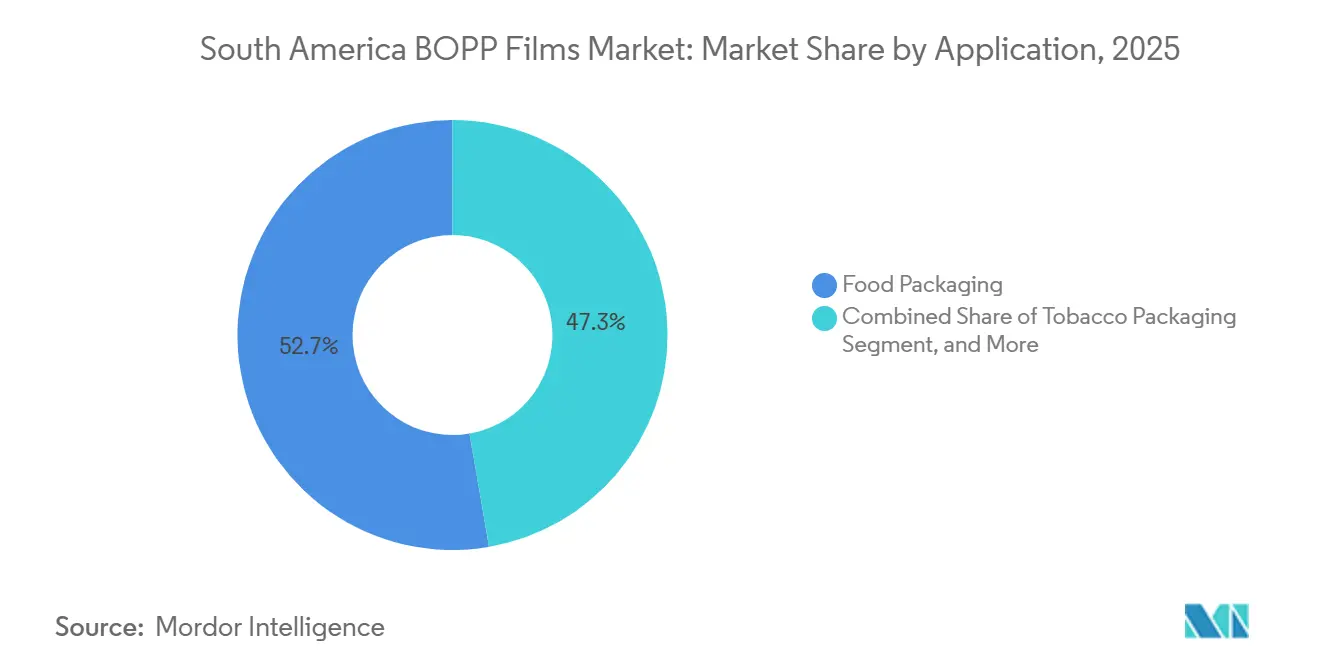

- By application, food packaging accounted for 52.72% of revenue in 2025; fresh produce liners are expected to expand at a 7.98% CAGR during 2026-2031.

- By end-user, food and beverage accounted for 57.39% of consumption in 2025, while personal care and cosmetics are set to grow at a 7.91% CAGR to 2031.

- By geography, Brazil led with 47.11% revenue share in 2025; Peru is projected to register a 7.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America BOPP Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food Retail Boom Pushing Demand for High-Clarity Flexible Packs | +1.8% | Brazil, Argentina, Colombia, Peru, Chile | Medium term (2-4 years) |

| Substitution of PVC and Cellophane with Cost-Efficient BOPP | +1.5% | Region-wide, strongest in Brazil and Argentina | Long term (≥4 years) |

| Rising E-Commerce Driving Demand for Label and Tape Films | +1.3% | Urban Brazil, Argentina, Chile, expanding to Colombia and Peru | Short term (≤2 years) |

| Brand Owners’ Shift Toward Mono-Material Recyclability | +1.2% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| Regional Sugar-Tax Policies Spurring Metallized Snack Packs | +0.7% | Brazil, Chile, Argentina | Short term (≤2 years) |

| Surge in Agro-Export Vacuum-Bag Liners Using Thick BOPP | +0.6% | Peru, Chile, Argentina | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Food Retail Boom Pushing Demand for High-Clarity Flexible Packs

Modern supermarkets and convenience chains continue to spread across metropolitan Brazil and secondary cities in Argentina and Colombia, widening shelf space for portion-controlled snacks that benefit from BOPP’s clarity and gloss.[1]Brazilian Packaging Association Reports Retail Shift,” ABRE, abre.org.br Consumers buying ready-to-eat bakery and confectionery products expect transparent windows that signal freshness while blocking moisture, a performance balance readily delivered by oriented polypropylene. Converters have responded by retrofitting older lines with enhanced pinning and thickness-control modules that allow down-gauging without sacrificing stiffness. Brazil’s largest line upgrade at Votorantim, completed in late 2024, produced higher-gloss films that are now making inroads into premium cookie wraps. With urban cold-chain networks still nascent in Peru and interior Colombia, pack integrity remains critical, further lifting demand for high-clarity films in those markets.

Substitution of PVC and Cellophane with Cost-Efficient BOPP

Regulators in Brazil and Chile tightened rules on chlorine-containing polymers, spurring converters to transition tobacco overwraps and candy twists from PVC to BOPP. BOPP also displaced imported cellophane in premium confectionery as local metallization capacity rose, narrowing cost gaps and improving supply security. The mono-material nature of metalized BOPP aids post-consumer sorting, a key requirement under extended producer responsibility laws taking effect in São Paulo state. Recent spot resin quotes for bioriented film grades ranged between USD 1,453 and USD 1,641 per metric ton in March 2026, reinforcing BOPP’s cost advantage over specialty cellulosics. As brand owners publicize recyclability targets, further PVC withdrawal is expected across secondary packaging formats.

Rising E-Commerce Driving Demand for Label and Tape Films

Parcel volumes handled by Brazilian couriers expanded by double digits in 2025, prompting fulfillment centers to stockpile BOPP-based carton-sealing tapes ahead of peak seasons. Label converters adopted thinner, high-tensile films below 20 µm to reduce material consumption while retaining stiffness required for automatic application. The same substrates allow crisp QR-code printing for track-and-trace systems mandated by large marketplaces. Argentina’s leading marketplace introduced recyclable mailers lined with two-layer BOPP labels that release cleanly during recycling, a feature now specified by several cross-border sellers. These developments create a fast-turnover outlet that absorbs clear film capacity even when food demand softens.

Brand Owners’ Shift Toward Mono-Material Recyclability

Major beverage, dairy, and snack companies signed public pledges to use recyclable packaging by 2030, triggering specification shifts toward metalized and coated BOPP that achieve barrier targets without PET or foil layers. Vitopel’s installation of the first BOBST EXPERT K5 metallizer in Brazil lifted national metalized output by 40%, shortening lead times for mono-material packs aimed at coffee, powdered milk, and edible oil sachets. Chilean retailers now favor shelf-ready snack bags certified as recyclable under local protocols, further validating this material shift. As more South American jurisdictions roll out eco-modulated fees, mono-material compliance is moving from optional to mandatory, cementing demand for functional BOPP.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Polypropylene Resin Pricing | -1.2% | Brazil, Argentina, with import dependency in Colombia, Chile, Peru | Short term (≤2 years) |

| Competition from BOPET in High-Barrier Niches | -0.8% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Limited Tenter-Frame Capacity South of Brazil | -0.6% | Argentina, Chile, Peru, Colombia | Long term (≥4 years) |

| Extended Truck Strikes Causing Logistics Bottlenecks | -0.5% | Brazil, Argentina | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Volatile Polypropylene Resin Pricing

Spot PP prices in Brazil fell 4% quarter over quarter in Q2 2025 as Asian oversupply reached local distributors, eroding converters’ margins on previously contracted film orders. Fluctuations complicate quarterly pass-through negotiations with food brands that demand stable input costs. Importers in Peru reported a 16.6% decline in delivered PP values during May 2025, but additional freight and tariff surcharges offset part of the savings. Currency depreciation in Argentina adds another layer of unpredictability, forcing some makers to hedge resin prices in U.S. dollars and hold higher stock levels. These swings delay capacity expansions because financing institutions seek predictable cash flows before releasing capital.

Competition from BOPET in High-Barrier Niches

Pharmaceutical blister suppliers and premium chocolate brands often specify BOPET where oxygen-transmission performance trumps cost sensitivity. Several Brazilian converters operate dual BOPP and BOPET lines, enabling them to propose polyester when customers demand longer shelf life for export-grade products. This option narrows BOPP’s addressable share in high-value niches, especially when resin price differentials shrink. Metallized BOPP is closing the gap, yet certain moisture-critical powders and effervescent tablets still default to multi-layer polyester structures. Continuous investment in metallization and AlOx coating is required for BOPP to remain competitive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Film Type: Functional Coatings Steer Premiumization

Transparent grades, accounting for 43.63% of the South America BOPP films market share in 2025, dominate shelf-stable snack and bakery wraps that demand aesthetic visibility and rapid line speeds. Metalized variants gained traction after domestic capacity rose in H2 2024, offering brand owners a recyclable alternative to foil laminates at comparable barrier levels. Anti-fog grades, projected to grow at a 7.79% CAGR, are gaining adoption in produce pouches shipped from Peru and Chile’s coastal valleys to North America and Asia, where humidity swings can trigger condensation.

Producers invest in plasma and vacuum metallizers that unlock value‐added surfaces resistant to grease migration, a priority for dairy powder sachets exported from Brazil’s Minas Gerais cluster. White and matt films, although niche, command price premiums in tobacco overwraps and gourmet confectionery that rely on light protection. This differentiated mix allows integrated groups to hedge against cyclical declines in commodity clear films, a strategy increasingly copied by mid-tier converters across Argentina and Colombia.

By Thickness: Heavy-Gauge Films Support Agro-Export Corridors

Standard 20-30 µm products captured 39.39% of the South America BOPP films market size in 2025 because they balance stiffness and yield on mainstream form-fill-seal lines. Thicker substrates above 45 µm, forecast to rise at an 8.01% CAGR, underpin vacuum bag liners for avocados, grapes, and seafood that endure puncture risks during refrigerated transit. Films in the 31-45 micrometer band address mid-range applications, including snack packaging, beverage labels, and tobacco overwraps.

Oben Group’s recent 12-meter-wide line in Monterrey runs at 700 m/min, enabling efficient production of 50 µm rolls targeted at export pack houses in Peru and Chile.[2]Oben Invests in 12-m BOPP Line,” Oben Group, obengroup.com Below-20 µm gauges are used in e-commerce tapes and wrap-around labels, where material reduction directly translates into lower shipping weight. Converters weigh the capital economics of stretching lines to run thicker films at slower speeds against the volume upside offered by fresh-produce exporters seeking robust barriers.

By Application: Produce and E-Commerce Lift Specialized Demand

Food packaging retained 52.72% share in 2025, with fresh fruit and vegetable liners poised for a 7.98% CAGR as anti-fog coatings become standard on bags destined for trans-equatorial shipments. Snack manufacturers in Brazil are switching to metalized mono-material packs to meet sugar-tax labeling requirements, adding impetus to the uptake of functional films.

Label and pressure-sensitive tapes stand out as the fastest e-commerce beneficiary, deploying ultra-thin yet high-tensile BOPP that seals millions of parcels dispatched daily from São Paulo hubs. Industrial users adopt thicker grades for pallet wrap and surface protection during appliance transport, broadening the material’s base beyond fast-moving consumer goods. This diverse matrix helps insulate the South America BOPP films market from single-segment downturns.

By End-User Industry: Personal Care Gains Momentum

Food and beverage companies accounted for 57.39% of total volume in 2025, driven by shelf-stable staples and powdered beverages that require cost-effective moisture barriers. Personal care brands are shifting shampoo sachets and wet-wipe outer wraps from rigid plastic to flexible formats, propelling a 7.91% CAGR through 2031. Other consumer goods encompass a wide range of applications, including stationery, gift wrap, and promotional materials.

Hygiene-focused consumers in Brazil favor resealable pouches for hair conditioners, creating openings for coextruded BOPP with improved hot-tack properties. Tobacco and logistics each preserve stable niches, while other consumer goods, such as stationery wrappers, absorb residual capacity during food-industry off-seasons. This end-user diversification enhances line utilization rates for integrated converters.

Geography Analysis

Brazil’s 47.11% revenue share mirrors its expansive retail network and resin self-sufficiency, enabling converters to run at higher plant utilizations than peers in neighboring countries. The August 2025 consolidation of Vitopel do Brasil under Oben Group deepened domestic scale, providing multinationals with a one-stop partner for regional supply. Argentina relies on imported specialty PP grades and faces currency volatility, yet maintains skilled operators and installed tenter-frame capacity that serve local snack brands.

Peru posts the fastest CAGR of 7.83%, supported by government-backed cold-chain corridors that expedite avocado and grape exports to the United States and East Asia. Local packers specify anti-fog BOPP liners to suppress condensation throughout the multiday voyage, pushing demand for functional films. Chile follows closely, leveraging its salmon and cherry export base to justify thicker, puncture-resistant films above 45 µm.[3]Chile Cold-Chain Investment Report,” Think Plastic Brasil, thinkplasticbrasil.com.br

Colombia and the Rest of South America clusters, including Ecuador and Uruguay, mainly import film but present growth headroom as retail formalization rises. Resin supplied from Brazil enjoyed a 19% quarter-over-quarter export jump in Q2 2025, reinforcing that country’s role as feedstock hub for the wider South America BOPP films market. Tariff hikes on imported PP into Brazil raised costs for Argentine and Chilean converters sourcing niche grades, nudging them toward long-term offtake contracts with Braskem or consideration of local polymerization investments.

Competitive Landscape

Regional concentration increased after Oben Group finalized its acquisition of Vitopel in August 2025, creating an 18-plant network that can optimize orders across Brazil, Peru, and Mexico. Post-merger, the combined entity accelerated R&D into high-barrier metalized films compliant with mono-material recycling protocols. Vitopel’s EXPERT K5 unit, commissioned in late 2024, lifted metalized output 40% and allowed domestic replacement of PET-foil laminates in dairy and coffee sachets.[4]Vitopel Adds First BOBST K5 in Brazil,” Think Plastic Brasil, thinkplasticbrasil.com.br

Second-tier players such as Polo Films and Papion Flexible Films differentiate through quick-color-match services and small-lot runs for regional snack start-ups. Larger groups, including Taghleef Industries and Jindal Poly Films Limited, operate dual hubs in the Americas and Asia, leveraging scale to arbitrage resin and shipping costs. Meanwhile, disruptive converters focus on digital printing and smart-label integration, catering to niche personal care brands that prize rapid artwork changes and traceability.

Investment patterns reveal a fork: high-volume, clear-film producers pursue ultra-wide lines to chase economies of scale, whereas functional-film specialists pour capex into metallizers, coating towers, and plasma chambers. Continuous upgrades, like Vitopel’s 2024 and scheduled 2025 control-system overhauls, point to an industry embracing automation to tame energy use and scrap rates.

South America BOPP Films Industry Leaders

Oben Holding Group

Amcor plc

Taghleef Industries

Polo Films

CCL Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Oben Group completed the acquisition of Vitopel do Brasil Ltda. following CADE clearance.

- June 2025: CADE issued unconditional approval for the Oben-Vitopel transaction.

- May 2025: Braskem reported a 4-point increase in utilization and a 19% surge in polypropylene exports to South America.

- March 2025: Oben Group executed a share-purchase agreement to acquire 100% of Vitopel do Brasil.

South America BOPP Films Market Report Scope

The South America BOPP Films Market analyzes the production, consumption, and trade of BOPP films in the region. These films are widely used in packaging applications due to their excellent clarity, strength, and barrier properties. The scope includes evaluating market trends, key drivers, challenges, and opportunities influencing the demand for BOPP films in South America.

The South America BOPP Films Market Report is Segmented by Film Type (Transparent, Metallized, White/Opaque/Matt, Anti-Fog and Other Functional Films), Thickness (Below 20 µm, 20-30 µm, 31-45 µm, and Above 45 µm), Application (Food Packaging, Beverage Packaging, Tobacco Packaging, Labels and Pressure-Sensitive Tapes, and Industrial and Other Applications), End-User Industry (Food and Beverage, Personal Care and Cosmetics, Tobacco, Industrial and Logistics, and Other Consumer Goods), and Geography (Brazil, Argentina, Colombia, Chile, Peru, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

By Film Type

| Transparent Films |

| Metallized Films |

| White / Opaque / Matt Films |

| Anti-Fog and Other Functional Films |

By Thickness

| Below 20 µm |

| 20–30 µm |

| 31–45 µm |

| Above 45 µm |

By Application

| Food Packaging | Confectionery |

| Snacks | |

| Bakery | |

| Fresh Produce | |

| Beverage Packaging | |

| Tobacco Packaging | |

| Labels and Pressure-Sensitive Tapes | |

| Industrial and Other Applications |

By End-User Industry

| Food and Beverage |

| Personal Care and Cosmetics |

| Tobacco |

| Industrial and Logistics |

| Other Consumer Goods |

By Country

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Film Type | Transparent Films | |

| Metallized Films | ||

| White / Opaque / Matt Films | ||

| Anti-Fog and Other Functional Films | ||

| By Thickness | Below 20 µm | |

| 20–30 µm | ||

| 31–45 µm | ||

| Above 45 µm | ||

| By Application | Food Packaging | Confectionery |

| Snacks | ||

| Bakery | ||

| Fresh Produce | ||

| Beverage Packaging | ||

| Tobacco Packaging | ||

| Labels and Pressure-Sensitive Tapes | ||

| Industrial and Other Applications | ||

| By End-User Industry | Food and Beverage | |

| Personal Care and Cosmetics | ||

| Tobacco | ||

| Industrial and Logistics | ||

| Other Consumer Goods | ||

| By Country | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the South America BOPP films market?

The South America BOPP films market is estimated at USD 7.71 billion in 2026, continuing the growth trajectory traced from USD 7.18 billion in 2025.

How fast will regional demand grow through 2031?

Market value is projected to reach USD 10.88 billion by 2031, reflecting a 7.14% CAGR over 2026-2031.

Which country shows the fastest volume expansion?

Peru is forecast to post a 7.83% CAGR, outpacing the regional average as fresh-produce exports require more functional films.

Which thickness band is gaining the most traction?

Films above 45 µm, used in vacuum liners and industrial packs, are expected to grow at an 8.01% CAGR through 2031.

Why are metallized BOPP grades in high demand?

Brand owners are replacing foil laminates with recyclable mono-material metallized BOPP to meet sustainability targets and sugar-tax packaging rules.

How has consolidation affected competitive dynamics?

Oben Group’s acquisition of Vitopel consolidated production across 18 plants, increasing bargaining power and accelerating functional-film innovation.

Page last updated on: