Larvicides Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1 Billion |

| Market Size (2031) | USD 1.32 Billion |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

| Fastest Growing Market | South America |

| Largest Market | North America |

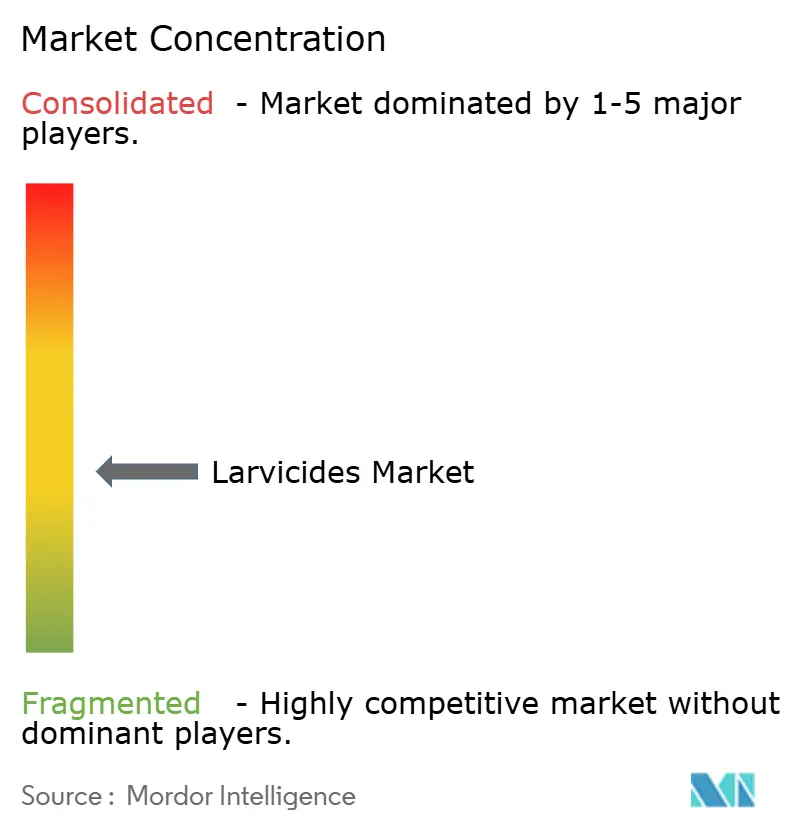

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Larvicides Market Analysis by Mordor Intelligence

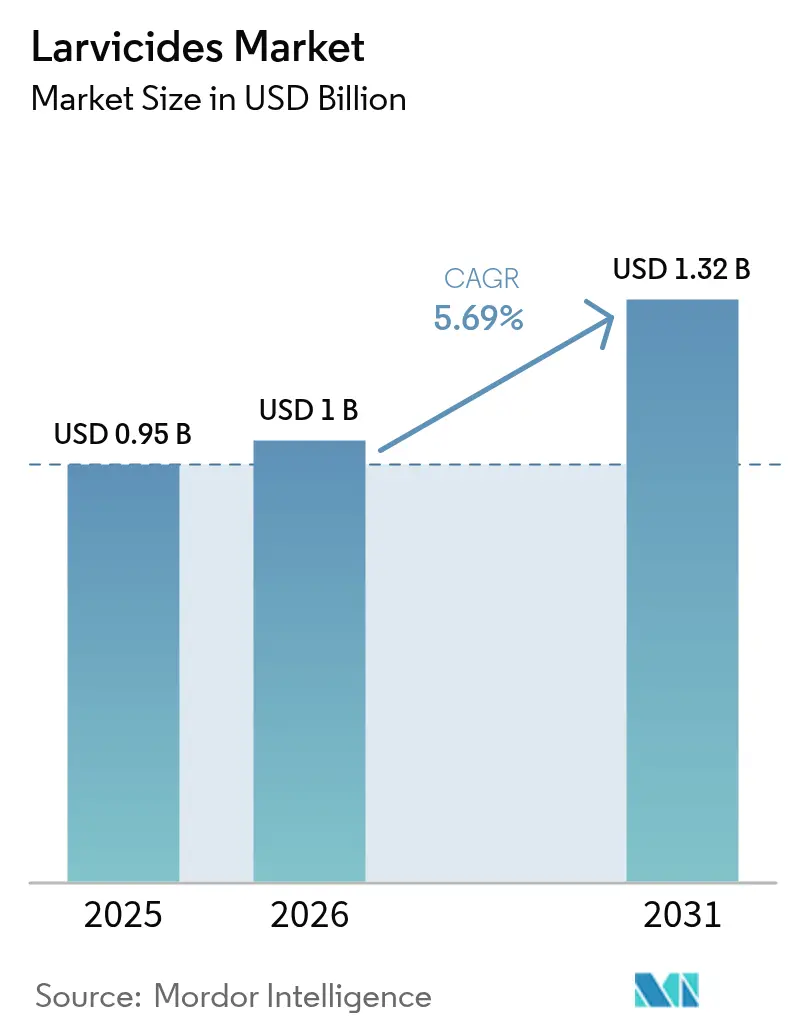

The Larvicides Market size was valued at USD 0.95 billion in 2025 and estimated to grow from USD 1 billion in 2026 to reach USD 1.32 billion by 2031, at a CAGR of 5.69% during the forecast period (2026-2031). The market growth is driven by several factors, like the increasing necessity to target mosquitoes in their larval stage due to reduced effectiveness of adult mosquito control methods, expanded healthcare budgets in the Americas, and continuous development of environmentally compatible bio-rational formulations. Additional growth drivers include extended mosquito breeding periods in temperate regions, persistent dengue outbreaks in tropical urban areas, and increased adoption of integrated rice-fish farming systems requiring aquaculture-safe larvicides. The market faces challenges including higher production costs for biological products, inconsistent application methods in rural areas, and requirements for GIS-based monitoring systems to enhance treatment efficiency.

Key Report Takeaways

- By product type, synthetic agents held 44.30% of the larvicides market share in 2025, whereas biological formulations are projected to expand at an 8.16% CAGR through 2031.

- By control method, chemical agents dominated revenue in 2025, yet insect growth regulators are on track for a 7.62% CAGR to 2031.

- By target insect, mosquitoes accounted for 64.40% share of the larvicides market size in 2025; the flies segment is forecast to grow at 6.34% CAGR.

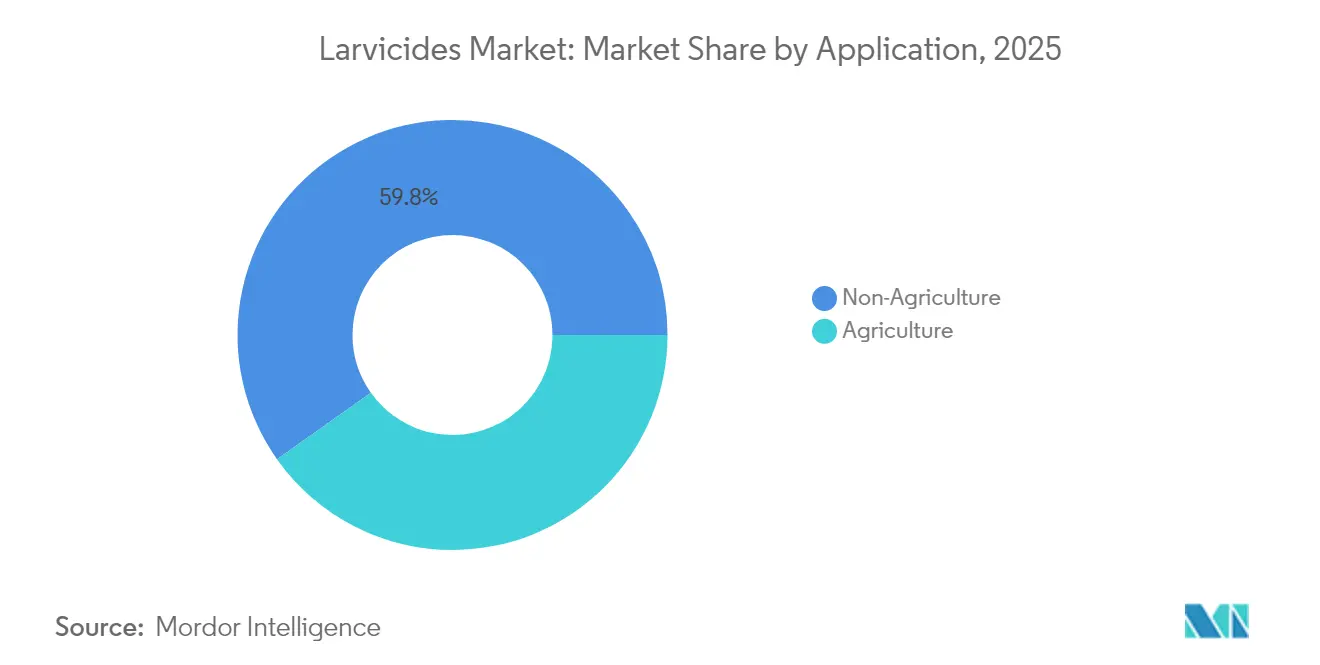

- By application, agricultural uses commanded 40.20% of the larvicides market size in 2025, while public-health programs are progressing at a 8.74% CAGR.

- By region, North America led revenue in 2025, whereas South America is advancing at the fastest pace on the back of urban dengue control campaigns.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Larvicides Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in insecticide-resistant adult mosquitoes accelerating larval-stage intervention | +1.2% | Global, with highest impact in Southeast Asia and Africa | Medium term (~ 3-4 yrs) |

| Roll-out of dengue & chikungunya prevention programs | +0.8% | South America, particularly Brazil and urban centers | Short term (≤ 2 yrs) |

| Climate-induced expansion of mosquito breeding seasons in temperate regions | +0.6% | North America, particularly northern United States and southern Canada | Medium term (~ 3-4 yrs) |

| Government subsidies for integrated rice–fish farming | +0.4% | Southeast Asia, particularly Indonesia, Vietnam, and Thailand | Long term (≥ 5 yrs) |

| Regulatory Policies on Larvicides | +0.7% | North America and Europe, with gradual adoption in Asia-Pacific | Medium term (~ 3-4 yrs) |

| Rapid scale-up of drone-based aerial application of larvicides | +0.9 | North America, Europe, and advanced Asian markets (Japan, South Korea, Singapore) | Short term (≤ 2 yrs) |

| Source: Mordor Intelligence | |||

Surge in Insecticide-Resistant Adult Mosquitoes Accelerating Larval-Stage Intervention

Mosquitoes develop resistance to insecticides through target-site insensitivity and metabolic detoxification. Anopheles and Aedes mosquitoes avoid chemical treatments through genetic adaptations, behavioral changes, and metabolic resistance. Vector control programs now focus on early-stage population control by targeting larvae in breeding sites, including stagnant water bodies and urban reservoirs. This approach prevents mosquitoes from reaching adulthood and interrupts disease transmission cycles. Vector control programs increasingly implement integrated strategies that rotate different active ingredients to reduce selective pressure on individual chemical classes. This shift is most visible where pyrethroid failure jeopardized emergency spraying budgets, encouraging municipalities to invest in season-long larvicide grids that protect floodwater pools and storm drains before adult swarms emerge.

Roll-out of Dengue and Chikungunya Prevention Programs

Latin American megacities are strengthening their dengue and chikungunya prevention programs in response to increased infection rates and urban mosquito populations. The World Health Organization (WHO) reports a significant increase in cases, particularly in Bolivia and Paraguay. Prevention strategies include Aedes aegypti mosquito control, public awareness initiatives, and integrated approaches combining sanitation, urban planning, and education. The Pan American Health Organization (PAHO) guides regional governments on implementing community-based measures to reduce disease transmission. In response to the 2024 dengue outbreak in Brazil, the World Mosquito Program (WMP) has partnered with Fiocruz to address mosquito-borne diseases across the country. The WMP is expanding its Wolbachia method, which introduces a natural bacterium into Aedes aegypti mosquitoes to prevent the transmission of dengue, Zika, and chikungunya.[1]World Mosquito Program (How Wolbachia is Turning the Tide Against Dengue in Brazil)

Climate-Induced Expansion of Mosquito Breeding Seasons in Temperate Regions

Rising average temperatures and changing precipitation patterns are extending the reproductive period for Culex species in northern latitudes. Habitat modeling studies indicate a significant northward range expansion by 2050, increasing demand for long-lasting methoprene pellets and briquets that maintain effectiveness throughout extended spring-to-autumn cycles. County vector control districts in Michigan, Wisconsin, and southern Canada are modifying their budgets to accommodate multiple application rounds, focusing on formulations that maintain stability during heavy rainfall. Vendors are prioritizing polymer-coated granules that provide consistent active ingredient release for up to 150 days, matching the extended mosquito season.

Government Subsidies for Integrated Rice–Fish Farming

India, Indonesia, Vietnam, and Thailand provide financial incentives to farmers who integrate rice paddies with fish ponds. This practice increases crop yields and reduces malaria vector larvae by up to 82%. Farmers must use selective larvicides that protect beneficial aquatic organisms, specifically Bti and Bacillus sphaericus strains, to qualify for subsidies. In India, the Pradhan Mantri Matsya Sampada Yojana (PMMSY) offers a 40% subsidy on approved project costs, with increased support of 60% for Scheduled Castes (SC), Scheduled Tribes (ST), and women beneficiaries. A 2024 study examined integrated rice-fish farming in Andhra Pradesh, India, under the Andhra Pradesh Community Managed Natural Farming (APCNF) program. This integrated approach combines rice cultivation with fish farming to enhance sustainability, biodiversity, and economic stability for small and marginal farmers.[2]CGIAR (Consultative Group on International Agricultural Research)

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent aquatic-toxicity thresholds under the US EPA Clean Water Act | −0.9% | North America and Europe | Short term (≤ 2 years) |

| Low adoption of GIS breeding-site mapping in rural Africa | −0.5% | Sub-Saharan Africa | Medium term (2–4 years) |

| Supply-chain volatility for Bacillus fermentation media | -0.6% | Global, with highest impact in emerging markets | Short term (≤ 2 yrs) |

| Public pressure against synthetic vector-control compounds | -0.4% | Europe, North America, and urban centers in developing regions | Medium term (~ 3-4 yrs) |

| Source: Mordor Intelligence | |||

Stringent Aquatic-Toxicity Thresholds

The 2026 Pesticide General Permit requires applicators to document the dosage, location, and non-target species monitoring when treating surface waters. Regulatory oversight of organophosphates, including temephos, has reduced available formulation options for floodwater marshes and urban catch basins. The increased compliance costs have led counties to shift from high-risk chemicals to biorational alternatives, despite their higher prices. While suppliers providing comprehensive toxicological data and digital application records maintain market advantages, the entry barriers affect small operators and limit local chemical larvicide distribution.

Low Adoption of GIS Breeding-Site Mapping

Limited digital infrastructure, high costs, and insufficient trained personnel prevent widespread adoption of GIS for identifying mosquito larval habitats across many regions. Effective larviciding depends on precise habitat identification, but numerous districts lack the geospatial tools needed to survey ponds, irrigation canals, and borrow pits. While community programs in Tanzania reduced Anopheles funestus adult populations by 46.3%, they required extensive manual habitat scouting, which increased labor costs and restricted scalability. In areas with limited electricity and internet connectivity, real-time mapping platforms cannot adequately support larvicide logistics, resulting in incomplete coverage and product waste. Addressing these challenges requires affordable mapping solutions, local technical training, and government-supported digital programs to enhance targeted larvicidal interventions across Africa.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biological Formulations Erode Synthetic Dominance

Synthetic larvicides account for 44.30% of the larvicides market share in 2025. Their market leadership stems from cost advantages and established procurement contracts. Biological products are growing at a higher rate of 8.16% CAGR, supported by government initiatives promoting integrated vector management approaches. Bacillus thuringiensis israelensis (Bti) demonstrates specific toxicity to mosquito larvae, blackflies, and fungus gnats. In 2023, the Kathmandu Metropolitan City (KMC) implemented bio-larvicide programs to control dengue outbreaks by targeting mosquito larvae. This organic solution eliminates mosquito larvae by disrupting their digestive systems while preserving other organisms.

The development of RNAi yeast larvicides in late-stage testing indicates potential market shifts, offering gene-specific control without affecting non-target species. Manufacturers are improving microencapsulation techniques to enhance product longevity and ease of use. Research in 2024 demonstrated the efficacy of botanical larvicides in crop protection, specifically marigold extracts. A study conducted by PES University in Bangalore revealed that Tagetes erecta and Tagetes patula contain thiophenes, which demonstrate significant larvicidal effects against crop pests Spodoptera litura and Corcyra cephalonica. These technological improvements, coupled with government incentives for environmentally sustainable products, enable biological larvicides to secure more municipal contracts.

By Control Method: IGRs Gain Momentum amid Resistance Concerns

Insect Growth Regulators (IGRs) have emerged as an effective larvicide control method, particularly in response to increasing resistance against conventional insecticides. IGRs disrupt mosquito development by inhibiting molting, reproduction, and metamorphosis, preventing larvae from reaching adulthood. While chemical contact poisons generated 54.10% of revenue in 2025, field studies indicate reduced effectiveness due to resistance development. Methoprene, a primary IGR compound, demonstrates effectiveness at concentrations of ≤ 10 ppb with minimal aquatic mobility.

Vector control programs are increasingly adopting IGR-based solutions, including pyriproxyfen and methoprene, due to widespread metabolic and behavioral resistance to pyrethroids and organophosphates. IGRs provide extended residual activity, reduced environmental impact, and lower resistance development risk, positioning them as integral components of sustainable mosquito control programs.

By Target Insect: Mosquito Focus Sustains Volume, While Flies Offer Adjacent Growth

Mosquito control accounted for 64.40% of larvicide sales in 2025, driven by the continued public health threats of dengue, malaria, and West Nile virus infections. The market benefits from consistent demand through sustained control campaigns, established multi-year budgets, and donor-funded intervention programs. The World Health Organization reported over 7.6 million global dengue cases as of April 2024, an increase of 3 million cases compared to the previous year. In agricultural environments, mosquito-borne diseases like West Nile, Dengue, Zika, and Malaria affect worker health rather than causing direct crop damage.

According to the World Mosquito Program, dengue fever causes approximately 36,000 deaths globally each year, while yellow fever accounts for about 30,000 annual deaths. This ongoing disease burden requires continuous investment in mosquito control programs across both developed and developing regions, sustaining market demand for mosquito-targeted larvicides. The mosquito segment is projected to maintain its dominance in the target insect category throughout the forecast period.

By Application: Public-Health Budgets Outpace Traditional Agriculture

Agriculture remains the primary revenue source in 2025, representing 40.20% of market share, as rice paddies, fishponds, and livestock operations incorporate larviciding into their standard practices. Municipal health agencies are increasing their investments at a faster rate. The Sacramento-Yolo Mosquito and Vector Control District has allocated USD 1.2 million for microbial larvicides and USD 1.2 million for biorationals in its 2024-2025 budget. Similar budget allocations in Florida, Texas, and Brazilian cities indicate sustained funding commitments.

Advanced delivery systems, including the In2Care trap, combine attractant, bio-agent, and automatic larvicide distribution to hard-to-reach areas. Implementation in residential areas enhances coverage efficiency, supporting higher price points. Throughout the forecast period, public health regulations will gradually alter volume distribution across channels, driving double-digit growth for specialized suppliers.

By Formulation: Tablets and Pellets Accelerate on Labor Savings

Liquid suspensions accounted for 45.30% of shipments in 2025, primarily due to their ease of tank mixing and versatility across different habitats. Controlled-release tablets and pellets are experiencing a 7.07% CAGR, driven by their ability to reduce repeated application labor in difficult-to-access habitats. Field trials in Vietnamese rice paddies demonstrated that floating tablets maintained over 70% efficacy for 21 days, exceeding sinking variants by 10.7%.

Manufacturers are developing biodegradable wax carriers that maintain buoyancy and protect spores from UV degradation. In 2024, the Town of Westerly conducted an aerial application of mosquito larvicide over Chapman Swamp to reduce mosquito-borne illnesses. The operation involved distributing pellets of Bacillus thuringiensis israelensis (Bti), a naturally occurring bacterium that specifically targets mosquito larvae without affecting humans or beneficial insects. The Rhode Island Department of Environmental Management (DEM) supervised the process.

Geography Analysis

North America generated the largest regional revenue in 2024, supported by structured vector-management frameworks and rising concern over West Nile and Eastern equine encephalitis. The United States is the primary user of larvicides for mosquito and larva control in North America. The Centers for Disease Control and Prevention (CDC) and local mosquito control districts implement vector control programs across the country. These programs incorporate larvicides within integrated mosquito management (IMM) strategies to prevent diseases such as West Nile virus, Zika, and other mosquito-borne illnesses.

The Environmental Protection Agency (EPA) endorses multiple larval mosquito control methods that target immature mosquitoes in their early stages. These methods include:- Bacterial insecticides (Bacillus thuringiensis israelensis and Bacillus sphaericus) that disrupt larval digestion - Insect growth inhibitors like methoprene that prevent development - Surface oils and films that cause larvae to drown. Environmental concerns have resulted in the discontinuation of certain control methods, particularly organophosphate insecticides. All control methods must comply with regulations to protect vulnerable populations. The EPA's 2026 Pesticide General Permit has established strict requirements for pesticide applications to surface waters, which shape product development throughout North America.

Asia presents a diverse mix; China and India anchor volume through agricultural applications, while Southeast Asian markets leverage subsidies that mandate biological larvicides in rice-fish systems. Simultaneously, Aedes aegypti resistance to organophosphates and pyrethroids forces councils in Indonesia to rotate IGRs and Bti combinations, underpinning incremental unit growth. The larvicide market share attributable to Asia will expand each year of the outlook, yet margins may stay compressed given price sensitivity in several economies.

South America demonstrates the highest growth rate, driven by public health crises related to dengue and chikungunya outbreaks. Brazil reported 7.25 million dengue cases in 2024, exceeding twice the number recorded in 2023, prompting increased Bti investments across federal, state, and municipal governments. Urban sanitation departments combine source reduction initiatives with weekly larvicide applications, ensuring consistent product demand that maintains distributor inventory levels.

Competitive Landscape

The market structure remains moderately concentrated, with BASF SE, Bayer AG, and Syngenta AG controlling over 50% of synthetic pesticide volume. These companies utilize multi-crop distribution networks and extensive product registrations as barriers to entry. In the biological segment, Valent BioSciences, Certis Biologicals, and Sumitomo Chemical Corporation (parent company of VectoBac) are increasing their capital investments to address growing demand. Valent's planned 2025 expansion of Bti fermentation facilities in the United States aims to ensure a reliable supply for Latin American contracts.

Strategic alliances emerge as a mechanism to blend formulation skills with market reach. Central Life Sciences licenses granular IGR technology to regional formulators that localize packaging sizes for African cooperatives. Several startups negotiate co-development agreements with genomic-editing firms to commercialize RNAi yeast larvicides, securing intellectual-property positions that differentiate from commoditized chemistries.

Research and development focus on improving long-term pest control effectiveness while meeting environmental safety standards. Field testing data supports regulatory approval applications, and securing early approvals can lead to long-term municipal contracts that strengthen market position. As a result, suppliers increasingly compete by providing comprehensive data demonstrating product performance in specific local breeding environments.

Larvicides Industry Leaders

Syngenta AG

BASF SE

Sumitomo Chemical Co.

Certis Biologicals

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: The US EPA issued the 2026 Pesticide General Permit detailing stricter monitoring for surface-water larvicide applications.

- May 2024: BASF introduced the insecticide Efficon in India to control sucking pests. The product targets multiple growth stages of pests, including aphids, jassids, and whiteflies during their larval development.

- May 2023: Valent BioSciences received approval from the Pest Management Regulatory Agency (PMRA) to conduct drone-based applications of its larvicides in Canada. The approval covers VectoBac 200G, VectoBac 1200L, and VectoLex CG products, enabling precise targeting of plant sucking mosquito and black fly populations in difficult-to-access areas.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the larvicides market as all chemical, biological, botanical, and insect-growth-regulator agents that are deliberately applied to water, soil, or crop substrates to kill insect larvae, predominantly mosquitoes, before adulthood. Value estimates cover finished formulations sold into agriculture and public-health channels across five regions and all major formulations, including granules, liquids, pellets, and powders.

Scope exclusion: Adult mosquito adulticides, fogging equipment, and physical traps are not part of this valuation.

Segmentation Overview

- By Product Type

- Synthetic Larvicides

- Biological Larvicides

- By Control Method

- Chemical Agents

- Biocontrol Agents

- Insect Growth Regulators (IGR)

- By Target Insect

- Mosquitoes

- Flies

- Beetles

- Ants

- By Application

- Agriculture

- Non Agriculture

- By Formulation

- Granules

- Liquids and Suspensions

- Pellets and Tablets

- Powders and Wettable Dusts

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Qatar

- Rest of Middle East

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured calls and short surveys with government mosquito-control officers, agronomists, formulators, and distributors across North America, Brazil, India, Kenya, and Indonesia helped us verify usage rates, channel margins, and emerging biological demand shifts, which then fine-tuned desk findings.

Desk Research

We began with publicly available vector-borne disease statistics from WHO, dengue and malaria program budgets published by PAHO and CDC, pesticide registration data on the US EPA and EU ECHA portals, trade flow series from UN Comtrade, and annual rainfall tables from FAO's climate database. Company sales splitouts were screened on D&B Hoovers and Dow Jones Factiva, while entomology papers in journals such as Parasites & Vectors guided biological-product efficacy assumptions. The listed sources are illustrative; many additional databases and country reports informed baseline numbers.

Market-Sizing & Forecasting

A top-down spend reconstruction starts with treated-area or population-at-risk pools by region, multiplies them by larvicide application frequency and average dose, then applies confirmed 2024 ASPs. Select bottom-up cross-checks, including supplier shipment samples and distributor revenue splits, anchor volume reasonableness. Key drivers inside the model include dengue incidence, government vector-control outlay, hectares under irrigated rice, registered biological active ingredients, and average annual precipitation. An ARIMA forecast links these variables to demand, and expert consensus moderates extreme scenarios. Gaps in granular shipment data are bridged by regional penetration proxies.

Data Validation & Update Cycle

Outputs move through variance scans against historical spend, currency movements, and patent-protected product launches. Senior analysts review anomalies, and re-contacts are triggered if deviations exceed preset bands. Figures refresh yearly, with interim corrections after material disease outbreaks or regulatory shifts.

Why Mordor's Larvicides Baseline Earns Reliable Trust

Published estimates often diverge because firms choose different inclusion rules, exchange-rate dates, and refresh cadences.

Key gap drivers include whether biological concentrates sold in bulk are counted, if public-health grants are booked at commitment or disbursement, and how fast ASP erosion is modeled. Mordor's disciplined scope alignment, annual refresh, and dual check of ASPs through distributor calls minimize these skews and give decision-makers a balanced middle path.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.95 B (2025) | Mordor Intelligence | - |

| USD 0.90 B (2024) | Regional Consultancy A | Excludes biological larvicides and uses constant 2020 FX rates |

| USD 0.92 B (2024) | Global Consultancy B | Counts bulk technical concentrates, not finished product value |

| USD 0.97 B (2024) | Industry Journal C | One-off survey, no bottom-up cross-check, three-year-old ASPs |

Taken together, the comparison shows that Mordor's blend of current ASP validation, explicit product boundaries, and yearly model audits yields the most transparent and reproducible baseline for strategic planning.

Key Questions Answered in the Report

What is the current size of the larvicides market and how fast is it growing?

The larvicides market is valued at USD 1 billion in 2026 and is on track to reach USD 1.32 billion by 2031, reflecting a 5.69% CAGR.

Which product type is expanding fastest within the larvicides industry?

Biological larvicides, particularly Bti formulations, are advancing at an 8.16% CAGR because they address resistance and comply with strict aquatic-toxicity requirements.

Why are insect growth regulators gaining popularity?

IGRs such as methoprene disrupt mosquito development without high acute toxicity, making them effective where resistance to conventional chemistries has emerged and helping programs meet environmental standards.

Which region offers the strongest growth prospects for larvicides suppliers?

South America, driven by large-scale dengue control campaigns in Brazil and neighboring countries, is the fastest-growing regional market over the 2026-2031 period.

How are regulatory changes influencing product development?

The US EPA’s tighter limits on aquatic toxicity under the Clean Water Act are accelerating industry investment in low-impact microbial and IGR solutions, encouraging suppliers to phase out higher-risk organophosphates.

What role does climate change play in larvicide demand?

Longer and warmer breeding seasons in temperate zones are extending treatment windows and increasing orders for sustained-release formulations that remain active for several months.

Page last updated on: