Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

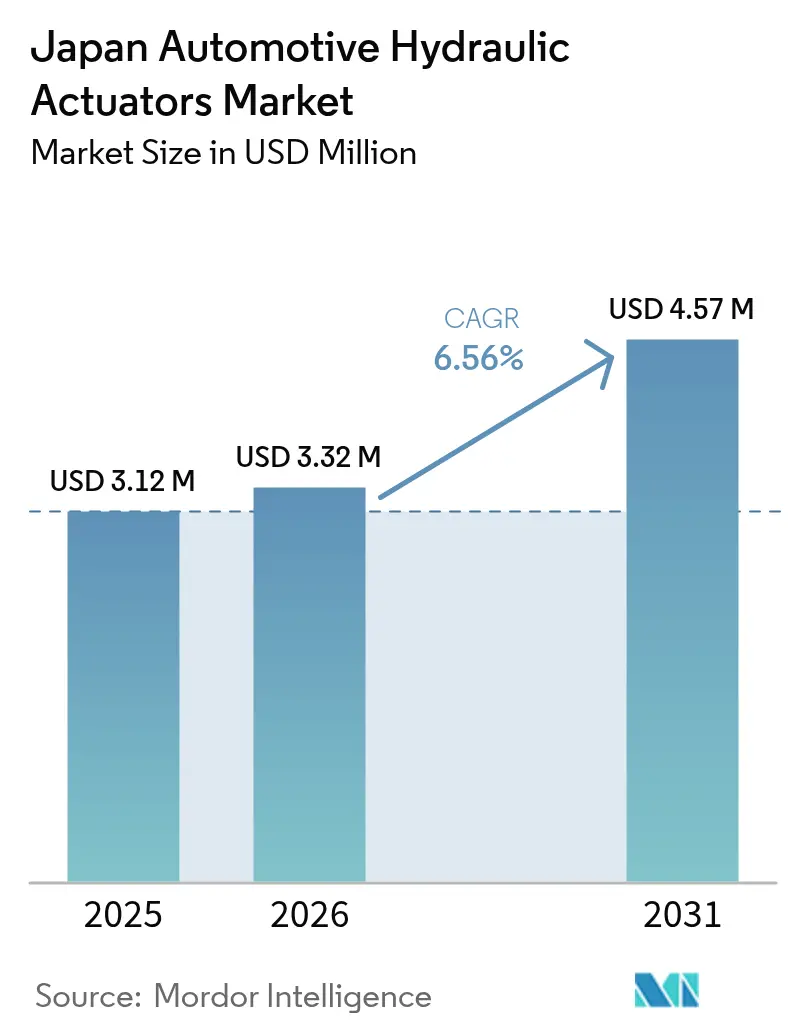

| Base Year Market Size (2025) | USD 3.12 Million |

| Market Size (2026) | USD 3.32 Million |

| Market Size (2031) | USD 4.57 Million |

| Growth Rate (2026 - 2031) | 6.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Automotive Hydraulic Actuators Market Analysis by Mordor Intelligence

The Japan automotive hydraulic actuators market size is expected to grow from USD 3.12 million in 2025 to USD 3.32 million in 2026 and is forecast to reach USD 4.57 million by 2031 at 6.56% CAGR over 2026-2031. Persistent demand for redundant brake circuitry outlined in the latest JIS D 0801 and UN R13-H rules sustains growth even as electrification advances. Government-backed hydrogen truck subsidies, rapid ADAS uptake, and predictive-maintenance adoption further bolster the Japan automotive hydraulic actuators market, while new 25% tariffs on parts imported into the United States and rising labor costs weigh on volumes. OEMs continue to favor hydraulic solutions in safety-critical functions because they deliver proven reliability under harsh duty cycles, especially in medium and heavy commercial vehicles that now qualify for sizable hydrogen incentives.

Key Report Takeaways

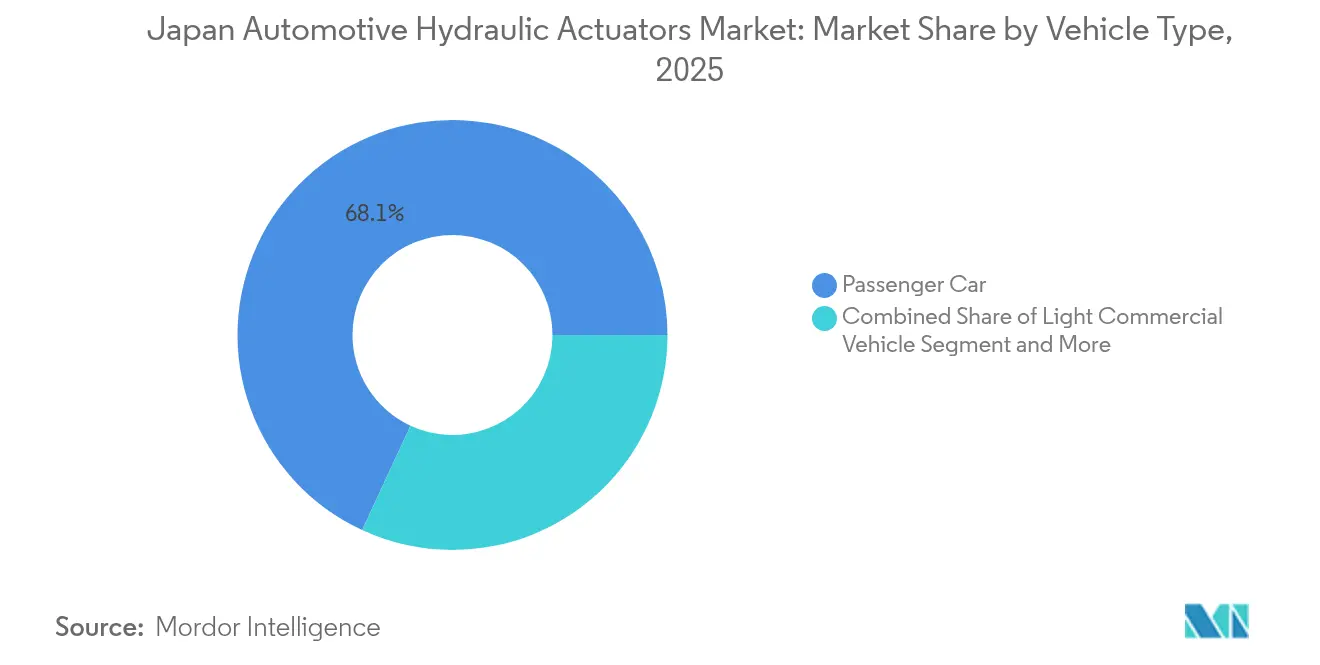

- By vehicle type, passenger cars led with a 68.10% revenue share of the Japan automotive hydraulic actuators market in 2025; medium and heavy commercial vehicles are projected to expand at an 7.78% CAGR through 2031.

- By application, brake actuators accounted for a 44.60% share of the Japan automotive hydraulic actuators market size in 2025 and remain the performance benchmark, while fuel-injection actuators are advancing at a 7.01% CAGR to 2031.

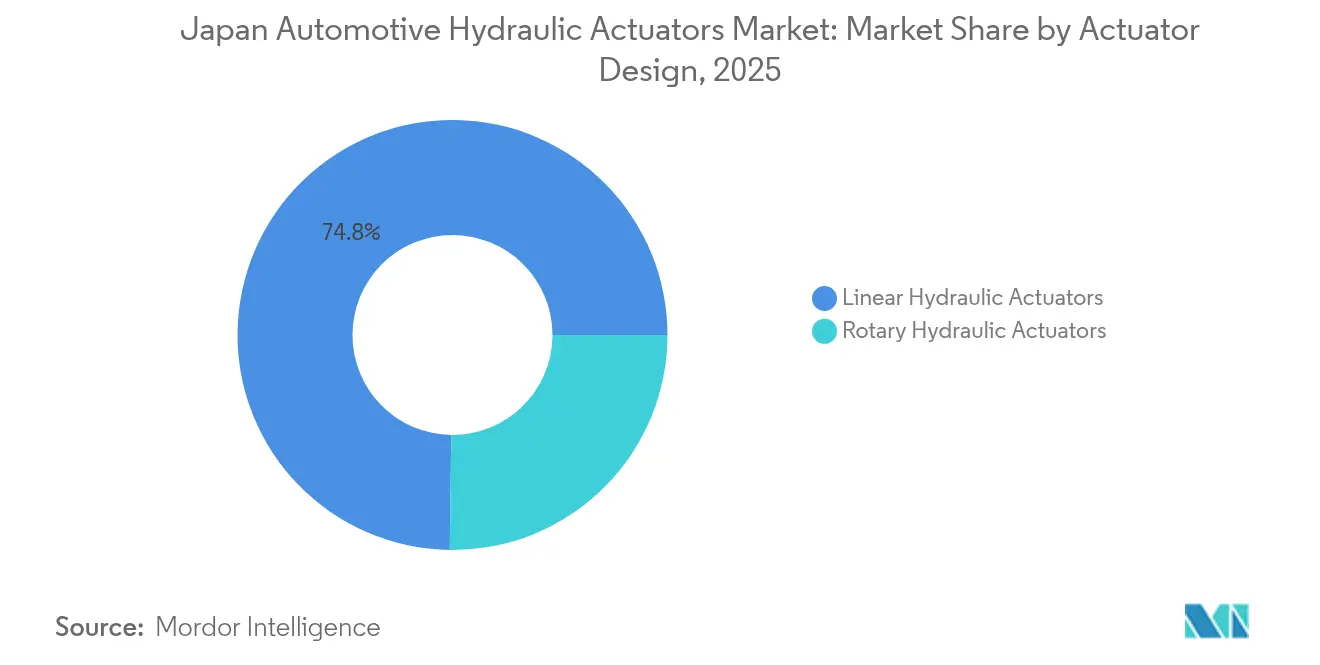

- By actuator design, linear units captured 74.80% of Japan automotive hydraulic actuators market share in 2025; rotary designs are poised for the fastest growth at an 8.02% CAGR through 2031.

- By sales channel, OEM distribution dominated with 90.85% share of the Japan automotive hydraulic actuators market size in 2025, whereas the aftermarket is set to grow at a 8.66% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Automotive Hydraulic Actuators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising ADAS Penetration | +1.8% | National, Tokyo-Osaka corridor | Medium term (2-4 years) |

| Stricter JIS D 0801 / UN R13-H Safety Rules | +1.5% | Nationwide compliance | Long term (≥ 4 years) |

| Passenger-car Production | +1.2% | Aichi, Hiroshima are production hubs | Short term (≤ 2 years) |

| Ageing Fleet Lengthens Replacement Cycles | +0.9% | Rural prefectures | Long term (≥ 4 years) |

| Smart-sensor-integrated Actuators | +0.8% | Kansai industrial clusters | Medium term (2-4 years) |

| Hydrogen Truck Subsidies | +0.7% | Tokyo Metro and ports | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising ADAS Penetration Calls for High-Response Hydraulic Brake Actuators

Automatic emergency braking is now mandatory across vehicle categories, creating a need for hydraulic brake actuators that achieve sub-50-ms response times. Hybrid brake-by-wire architectures keep hydraulic redundancy while enabling electronic precision, pushing suppliers to redesign units for seamless ECU integration. Forward-collision warning adoption reached 94% by model year 2023, and component makers that meet the tighter performance window command premium pricing. Bosch’s recent brake-by-wire rollouts illustrate how electronic control overlays still rely on hydraulic backup for fail-safe assurance [1]“Road Vehicle Safety Regulations Update,” Ministry of Land Infrastructure Transport and Tourism, mlit.go.jp.

Stricter JIS D 0801 / UN R13-H Safety Rules Raise Hydraulic Redundancy Needs

New braking rules require multi-circuit hydraulic systems able to retain residual pressure even under single-circuit failure. Compliance efforts spur uptake of tandem master cylinders, dual-pump boosters, and integrated pressure sensors. Component certification now involves tighter audit trails after widely publicized type-approval misconduct cases, giving incumbents with robust quality systems a competitive edge [2]“UN Regulation No. 13-H,” United Nations Economic Commission for Europe, unece.org.

Passenger-Car Production Rebound Boosts OEM Demand

Domestic passenger-car output recovered post-pandemic to 3.4 million units in 2024, directly lifting orders in the Japan automotive hydraulic actuators market. Although March 2025 output slipped 5.9% after US tariff impositions, OEMs are reshoring sub-assemblies worth JPY 220 billion to cushion supply risk. These capacity adjustments translate into steadier call-offs for hydraulic components in the near term while safeguarding long-term volumes [3]“Japan – Country Commercial Guide,” International Trade Administration, trade.gov.

Ageing Fleet Lengthens Replacement Cycles, Expanding Aftermarket Volumes

Average car age continues to climb as consumers delay new purchases, supporting a resilient aftermarket for hydraulic actuators. Obd-II-based inspections commencing October 2024 will flag worn brake cylinders and clutch masters more precisely, translating into predictable service demand at independent repairers. Japan’s vehicle-maintenance revenues reached JPY 5.7 trillion in 2024, and predictive-maintenance platforms tap sensor data to time replacements before failure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Shift toward Electro-mechanical Actuators | -2.1% | Urban centers | Long term (≥ 4 years) |

| Domestic Vehicle Production Decline | -1.3% | Aichi and adjacent prefectures | Short term (≤ 2 years) |

| Skilled-machinist Shortage | -0.8% | Kansai clusters | Medium term (2-4 years) |

| Oil-leak Environmental Penalties | -0.5% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV Shift Toward Electro-Mechanical Actuators Erodes Hydraulic Content

Battery-electric platforms increasingly specify electromechanical brakes and suspension, reducing hydraulic fitment. ZF won a 5 million-vehicle contract for full brake-by-wire systems that eliminate hydraulic lines entirely. Subsidies that favor BEVs and fuel-cell cars intensify the pivot, pushing incumbent hydraulic suppliers to diversify into electronic actuation.

Domestic Vehicle Production Decline Limits Volume Growth Potential

Recent 25% tariffs on Japanese auto parts bound for the United States and a strengthening yen threaten export competitiveness. March 2025 factory output fell the steepest since 2020, prompting OEMs to idle lines intermittently. Tight labor markets and rising borrowing costs compound the pressure, leaving the Japan automotive hydraulic actuators market more reliant on aftermarket resilience than on new-vehicle volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Vehicles Drive Growth Despite Passenger-Car Dominance

Passenger cars retained a 68.10% share of the Japan automotive hydraulic actuators market in 2025, reflecting entrenched personal-mobility demand. Yet medium and heavy commercial vehicles will record the highest 7.78% CAGR to 2031, buoyed by hydrogen-truck incentives that specify advanced hydraulic units with corrosion-resistant seals. This shift marginally dilutes passenger-car share over the forecast window but enlarges total output value because commercial vehicles carry higher actuator content per unit. Light commercial vans continue to see steady adoption as last-mile delivery expands.

The Japan automotive hydraulic actuators market gains strategic depth from commercial-vehicle requirements for long-life, serviceable designs that withstand high duty cycles. Fleet operators prioritize actuators with integrated condition monitoring to minimize downtime, propelling demand for sensorized units. Passenger cars, though slower growing, remain vital for volume stability and serve as a testbed for hybrid hydraulic-electronic systems that later migrate to heavier platforms.

By Application Type: Fuel-Injection Systems Emerge as Growth Leader

Brake actuators commanded 44.60% of the Japan automotive hydraulic actuators market size in 2025, sustained by safety regulations and near-universal fitment. However, fuel-injection actuators will be the fastest 7.01% CAGR through 2031 as OEMs refine combustion efficiency ahead of stricter emission caps. Embedded pressure and temperature sensors inside the injector actuator assembly enable predictive maintenance, reducing unplanned engine downtime.

HVAC blend-door and seat-adjustment systems add incremental volume, but their share trails powertrain and safety applications. Predictive maintenance also uplifts brake-actuator replacements because diagnostic data now pinpoints declining pressure build-up before pedal feel deteriorates, strengthening aftermarket sales.

By Actuator Design: Rotary Systems Gain Momentum in Active Applications

Linear actuators represented 74.80% of Japan's automotive hydraulic actuators market share in 2025, thanks to simple packaging in brakes and clutches. Rotary designs, though smaller in absolute numbers, will outpace at an 8.02% CAGR as active suspension and rear-wheel steering diffuses into premium and performance models. ClearMotion’s 40 Hz hydraulic rotary damper underscores the leap in frequency response now achievable with compact rotary units.

Growing interest in magnetorheological rotary dampers that deliver 600 Nm torque at sub-50 ms response highlights the trajectory toward fast, multi-axis motion control. Linear-actuator suppliers respond by adding smart-seal technology and low-viscosity fluids to retain their incumbency in mass-market segments.

By Sales Channel: Aftermarket Acceleration Reflects Fleet Aging

OEMs captured 90.85% of the Japan automotive hydraulic actuators market size in 2025 due to the tight integration between actuators and electronic control units during vehicle assembly. Yet the aftermarket will post a 8.66% CAGR as Japan’s median vehicle age climbs and OBD-II periodic inspections ramp up. Independent garages invest in hydraulic-test benches and data analytics subscriptions to service sensorized actuators, while parts distributors stock higher-margin remanufactured units that meet the latest JASO quality codes.

Longer ownership cycles also prompt fleets to retrofit predictive-maintenance kits onto legacy hydraulic circuits, widening the aftermarket revenue base. OEM-approved service networks dominate warranty repairs, but independent chains gain share in vehicles older than five years.

Geography Analysis

Japan’s automotive supply chain clusters in Aichi, Hiroshima, and northern Kyushu, with Aichi alone hosting at least 30% of the national vehicle output. Consequently, actuator demand mirrors line rates at Toyota, Aisin, and Denso facilities. The Tokyo–Osaka corridor, equipped with advanced ICT infrastructure, spearheads the adoption of sensorized hydraulic actuators that stream real-time data into fleet-management platforms. Hydrogen-truck pilots centered on Tokyo ports further amplify localized demand for corrosion-resistant units. Northern Kyushu’s ports also facilitate component export to Asian OEM plants, reinforcing localized supply loops.

Rural prefectures display a contrasting profile: older vehicle fleets, lower annual mileage, and heavier reliance on aftermarket service shops. These factors anchor stable replacement parts demand and shield the Japan automotive hydraulic actuators market from cyclical production swings. Government reshoring subsidies are channeling new machining capacity into northern Tohoku, diversifying production footprints, and shortening lead times. Environmental policies differ by municipality. Tokyo enforces stricter leak-prevention rules, compelling assembly plants to upgrade seals and adopt closed-loop hydraulic-fluid recycling. Western prefectures, led by Kansai, run predictive-maintenance sandboxes under Smart-Factory initiatives, accelerating edge-AI actuator deployment. The country’s island geography encourages OEMs to source actuators domestically to avoid logistics bottlenecks, benefiting local producers with rapid engineering-change capability. Future demand pockets align with fuel-cell truck corridors along the Shin-Tomei and Chuo Expressways, where hydrogen stations multiply under METI’s Green Growth Strategy. Suppliers able to certify actuators for hydrogen exposure are positioned to capture these emerging lanes.

Regulatory Landscape

Japan regulates automotive hydraulic actuators primarily through the Road Transport Vehicle Act and MLIT-administered type-approval frameworks that set technical and test requirements for safety-critical systems such as braking and steering. For brake-related hydraulic actuators, alignment with harmonized UN Regulations, including UN R13-H for braking, and the corresponding Japanese standards ecosystem (supported by bodies such as JASIC for standards internationalization) shapes design validation, documentation, and audit trails before parts are accepted into OEM builds.

Beyond safety performance, suppliers face strict liability exposure under the Product Liability Act (Act No. 85 of 1994), which reinforces quality management and traceability for both OEM and aftermarket channels. Environmental compliance requirements and municipal enforcement (notably stricter leak-prevention expectations in areas such as Tokyo) add further process controls around sealing, hydraulic-fluid handling, and end-of-life considerations, raising the compliance bar for new entrants and remanufacturers.

Value Chain Analysis

The value chain begins with inputs such as aluminum and steel housings, precision-machined pistons and valves, elastomer seals, hydraulic fluids, and, in sensorized designs, pressure and temperature sensing elements and ECUs. Tier suppliers in Japan, concentrated across Chubu and Kanto industrial corridors, handle precision machining, sealing and surface-treatment, assembly, and end-of-line testing before supplying OEMs through tightly controlled nomination and validation processes. This structure is consistent with the market where OEM distribution accounted for 90.85% share in 2025.

Supply-chain operating practices have increasingly emphasized resilience and standardization. In March 2026, JAMA highlighted securing stable procurement of resources and components as a priority challenge, and material and logistics pressures, including high aluminum prices linked to geopolitical disruption, have raised cost and availability risks for metal-intensive hydraulic parts. Suppliers and OEMs are therefore adjusting procurement and acceptance criteria to keep lines running, while strengthening local machining capacity, standardized specifications, and multi-sourcing for critical subcomponents such as seals and castings.

Competitive Landscape

Domestic champions such as Denso, Aisin, KYB, and Hitachi Astemo leverage long-standing OEM ties, vertically integrated production, and deep hydraulic know-how to maintain leading positions in the Japan automotive hydraulic actuators market. Hitachi Astemo targets USD 14.8 billion revenue by FY 2025, earmarking USD 100 million for US plant upgrades that support global demand for smart actuators. KYB’s weekly output of 1 million shock absorbers underscores scale advantages and provides a launchpad for hybrid hydraulic-electronic product lines.

European multinationals Bosch, Continental, and ZF compete on next-generation brake-by-wire and steer-by-wire systems that still retain hydraulic safety backups. ZF’s 5-million-vehicle contract showcases its capacity to integrate electro-mechanical and hydraulic subsystems at scale. Patent data reveal intensifying R&D in fusion hybrid linear actuators, magnetorheological fluids, and edge-AI sensor packages—areas where collaboration with Japanese electronics giants offers differentiation.

Market entry barriers remain high: stringent certification tests, capital-heavy machining, and proprietary OEM software interfaces deter new players. Nonetheless, white-space opportunities emerge in predictive-maintenance services, where data analytics rather than hardware margins drive profitability. Actuator makers partnering with cloud platforms capture annuity revenues tied to uptime guarantees.

Japan Automotive Hydraulic Actuators Industry Leaders

Denso Corporation

Aisin Corporation

Hitachi Astemo Ltd.

Robert Bosch GmbH

Continental AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity sits in hybrid electro-hydraulic architectures that preserve hydraulic redundancy while integrating tighter ECU control demanded by mandatory safety functions and rising ADAS penetration. The need to meet JIS D 0801 and UN R13-H-driven multi-circuit braking performance requirements supports demand for higher-response brake actuators and integrated pressure sensing, creating whitespace for suppliers that can deliver validated sensorized hydraulic assemblies with documentation aligned to MLIT type-approval and OEM audit trails.

The market also offers room for growth in service-oriented offerings tied to an aging vehicle parc and more data-driven inspections. With OBD-II-based inspections commencing in October 2024 and predictive-maintenance adoption expanding, actuator makers and distributors can bundle diagnostics, test-bench procedures, and remanufactured units that meet JASO quality expectations, supporting the aftermarket channel where growth is strongest within the report scope. At the same time, supplier portfolio moves toward electrified actuation in adjacent domains, including Nabtesco announcing mass production plans for all-electric power steering for large commercial vehicles beginning in 2027, reinforce the need for hydraulic actuator specialists to differentiate around safety-critical redundancy, harsh-duty commercial applications, and sensor-integrated reliability rather than competing head-on with fully electromechanical substitutions.

Recent Industry Developments

- May 2026: Nabtesco announced plans to start mass production of fully electric power steering systems for large commercial vehicles from 2027. The announcement points to accelerating electrification in heavy-vehicle subsystems and increases competitive pressure on hydraulic actuation suppliers to strengthen hybrid electro-hydraulic and safety-redundant positioning in adjacent chassis applications.

- January 2025: ZF secured a brake-by-wire contract to equip nearly 5 million vehicles, combining electro-mechanical actuation with hydraulic redundancy to meet safety requirements. The award highlights how advanced chassis control programs can still pull through hydraulic actuator content where fail-safe operation and residual braking capability are required.

- October 2024: Japan commenced OBD-II-based vehicle inspections that improve detection of wear and performance degradation in safety-related systems, including hydraulic circuits. The change supports more consistent identification of brake and clutch hydraulic issues during periodic checks, reinforcing demand visibility for replacement hydraulic actuators and related service tooling in the aftermarket.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market covers revenues earned from automotive hydraulic actuators sold and used in Japan, across OEM fitment and aftermarket replacement, where hydraulic force is the main actuation method in vehicle systems.

Scope exclusions: We exclude non-automotive hydraulic actuators, pneumatic actuators, and purely electric actuator units even when they serve similar vehicle functions.

Segmentation Overview

- By Vehicle Type

- Passenger Car

- Light Commercial Vehicle

- Medium and Heavy Commercial Vehicle

- Buses and Coaches

- By Application Type

- Brake Actuator

- Throttle Actuator

- Seat Adjustment Actuator

- Closure Actuator

- Fuel-Injection Actuator

- HVAC Blend-Door Actuator

- Others

- By Actuator Design

- Linear Hydraulic Actuators

- Rotary Hydraulic Actuators

- By Sales Channel

- OEM

- Aftermarket

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clean fact base on Japan vehicle production, parc direction, and component demand signals, and then aligning the definitions used across sources so the model stays consistent year to year. Public sources such as Japan transport and safety regulators, Ministry of Economy, Trade and Industry releases, Japan Customs trade statistics, JAMA publications, and technical papers in SAE-style journals were used to anchor volumes, adoption context, and technology shifts.

Along with these, we review company filings, investor presentations, association updates, and reputable press coverage to track platform changes, localization trends, and pricing direction. Select paid subscriptions are also used for company financials and intelligence, patent mapping, and shipment-level import and export checks where public data is too aggregated to be useful. These desk research sources are illustrative only, and many other references were used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test assumptions that cannot be read directly from public series, especially where hydraulic content per vehicle changes by platform and feature mix. We spoke with a mix of actuator suppliers, vehicle system integrators, aftermarket-focused stakeholders, and independent engineering experts across Japan, and then used follow-ups to confirm adoption rates, typical pricing ranges, and channel splits.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 13% | |

| Mid tier: 59% | Functional/Unit leaders: 30% | |

| Smaller Players: 16% | Managers: 57% |

Market-Sizing & Forecasting

Sizing begins with a top-down build where Japan vehicle production, vehicle parc service patterns, and system-level fitment rates are used to reconstruct the addressable demand pool for hydraulic actuators in vehicles. Once that demand pool is shaped, it is translated into value using modeled average selling prices that reflect mix by application, actuator design (linear or rotary), and sales channel (OEM versus aftermarket).

To keep totals realistic, we also run selective bottom-up approximations, such as sampled unit volumes by application multiplied by typical price bands gathered from interviews, and then check directionally against supplier revenue exposure and trade flow signals where applicable. In the model, inputs that matter most include passenger versus commercial production mix, replacement cycle timing, content per vehicle for brake and throttle related systems, platform shifts that change hydraulic versus non-hydraulic usage, and raw material and machining cost pressure that influences pricing. Forecasts are built using scenario analysis, where base demand follows expected vehicle output and replacement patterns, and price and penetration assumptions are adjusted based on what interviewees consider feasible under different technology adoption paths. Where granular splits are missing, gaps are handled by using clearly stated proxy ratios from similar applications and then rechecked through primary feedback before finalizing.

Data Validation & Update Cycle

Outputs are validated through a set of cross-checks that compare implied units and value with independent signals, such as production direction, trade indicators, and channel-side feedback from interviews. When a variance looks abnormal, assumptions are reopened and the underlying drivers are traced back until the mismatch is explained or corrected, followed by a second analyst review before sign-off.

The report is refreshed annually, and interim updates are done when material events can shift demand or pricing expectations. Before delivery, a final fresh pass is completed so the numbers reflect the latest available public releases and any new primary feedback that affects key assumptions.

Mordor Intelligence's Japan Automotive Hydraulic Actuators Market Size Measured Against Other Published Estimates

It is normal to see different market values published for the same topic because each study draws the market boundary differently and then applies its own mix and pricing logic. Differences also show up when base years vary, when OEM and aftermarket treatment is inconsistent, or when currency timing is not aligned across estimates.

By tracking fitment rates by application and sales channel, and then refreshing price bands through follow-up checks, Mordor Intelligence keeps the Japan total tied to hydraulic-only actuator demand rather than adjacent actuator technologies that can inflate value in broad actuator studies.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.12 M (2025) | |

| Industry Publisher A | USD 3.80 M (2025) | Uses a broader application mapping and sub-region build that can pull in additional actuator use cases, and the higher total can also come from a more aggressive price and penetration progression across the forecast window. |

| Research Publisher B | USD 1.51 B (2023) | The magnitude suggests a much wider scope that likely blends multiple actuator types or wider automotive component buckets, and it also uses a different base year and growth window, which changes currency timing and mix assumptions. |

Taken together, the spread is mainly explained by scope control and how unit demand is translated into value through price and mix assumptions. Our approach stays repeatable because each step is traceable to vehicle output, channel split, fitment rates, and interview-checked pricing, which makes it easier for buyers to understand what is included and why the totals move.

Key Questions Answered in the Report

What is the current size of the Japan automotive hydraulic actuators market?

The market stood at USD 3.32 million in 2026.

What compound annual growth rate is forecast for the market through 2031?

It is projected to grow at 6.56% CAGR, reaching USD 4.57 million by 2031.

Which vehicle category is expanding fastest?

Medium and heavy commercial vehicles lead with an 7.78% CAGR, thanks to hydrogen-truck incentives.

Why are rotary hydraulic actuators gaining popularity?

Active suspension and rear-wheel steering programs demand compact rotary units that offer faster 40 Hz response than traditional linear designs.

Page last updated on: