Intensive Care Unit (ICU) Beds Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

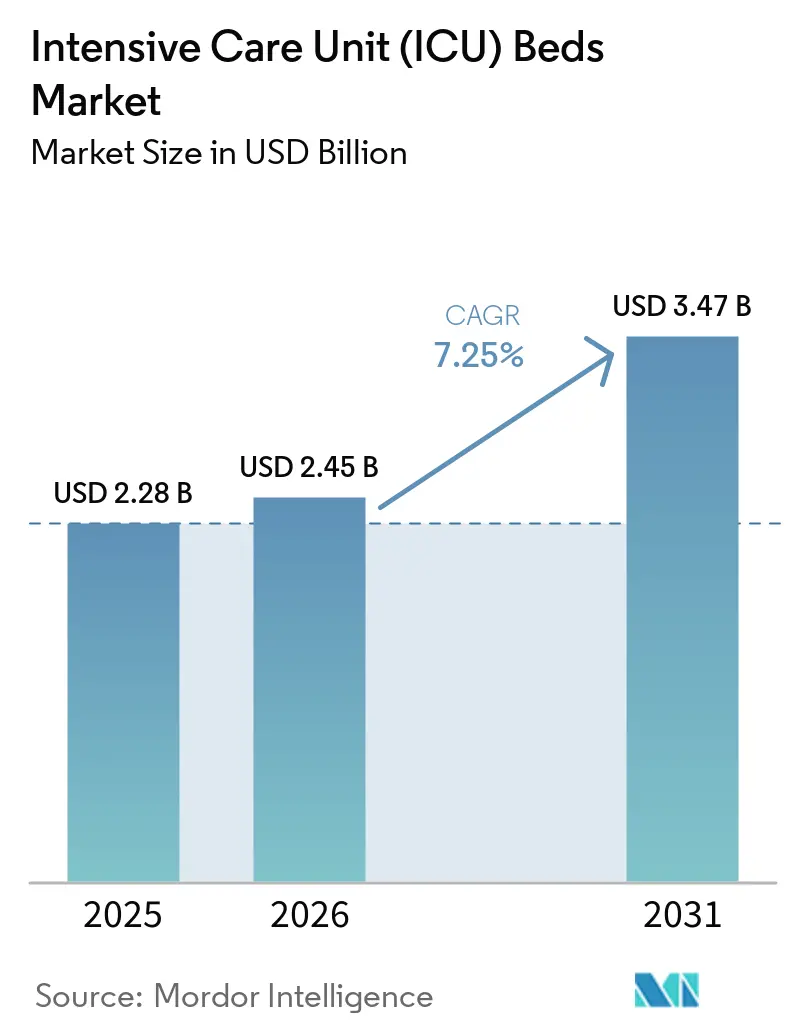

| Market Size (2026) | USD 2.45 Billion |

| Market Size (2031) | USD 3.47 Billion |

| Growth Rate (2026 - 2031) | 7.25% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

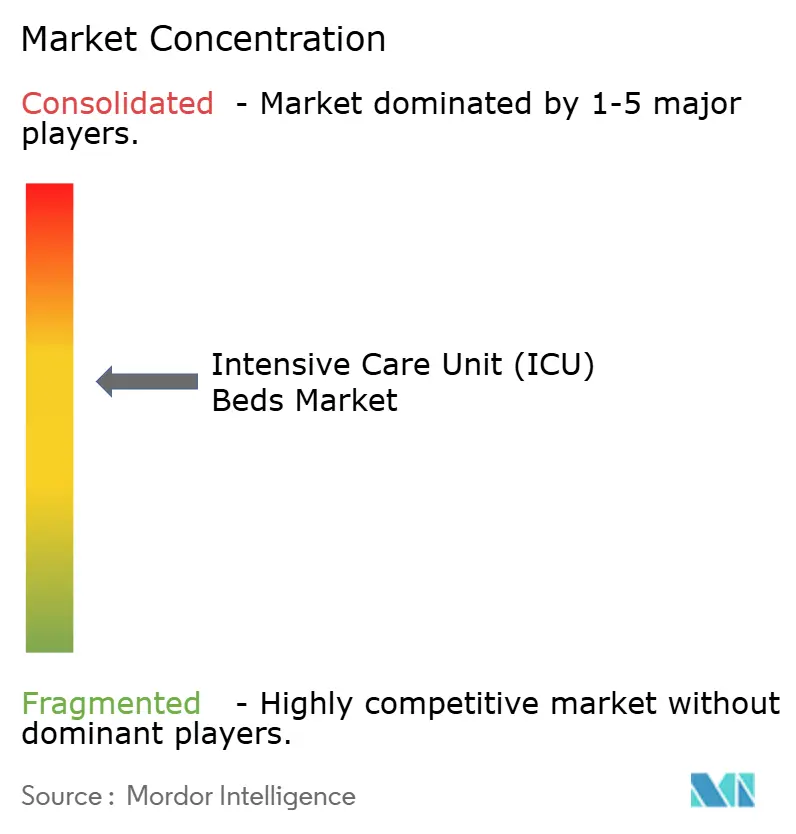

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intensive Care Unit (ICU) Beds Market Analysis by Mordor Intelligence

The Intensive Care Unit (ICU) Beds Market size is expected to increase from USD 2.28 billion in 2025 to USD 2.45 billion in 2026 and reach USD 3.47 billion by 2031, growing at a CAGR of 7.25% over 2026-2031.

The market reflects sustained capital spending by health systems that are managing a larger flow of critically ill patients, and that demand is tied more to long disease trends than to short funding cycles. A 2025 Journal of the American College of Cardiology analysis reported 626 million prevalent cardiovascular disease cases worldwide, while a 2025 Nature Medicine study reported 569.2 million chronic respiratory disease cases and 4.2 million related deaths, which keeps pressure on critical care capacity across regions. The ICU beds market is also being shaped by a clearer move toward connected and higher specification beds, because hospitals now want equipment that supports monitoring integration, workflow efficiency, and safer patient handling. Regional expansion remains uneven, with North America leading on installed capacity and modernization, while Asia-Pacific is expanding faster as new hospitals and critical care units come online in China, India, and Southeast Asia. The ICU beds market also shows moderate concentration, as large multinational suppliers keep widening their product and service capabilities, while cost pressure, reimbursement friction, and facility retrofit limits still slow procurement in more budget sensitive settings.

Key Report Takeaways

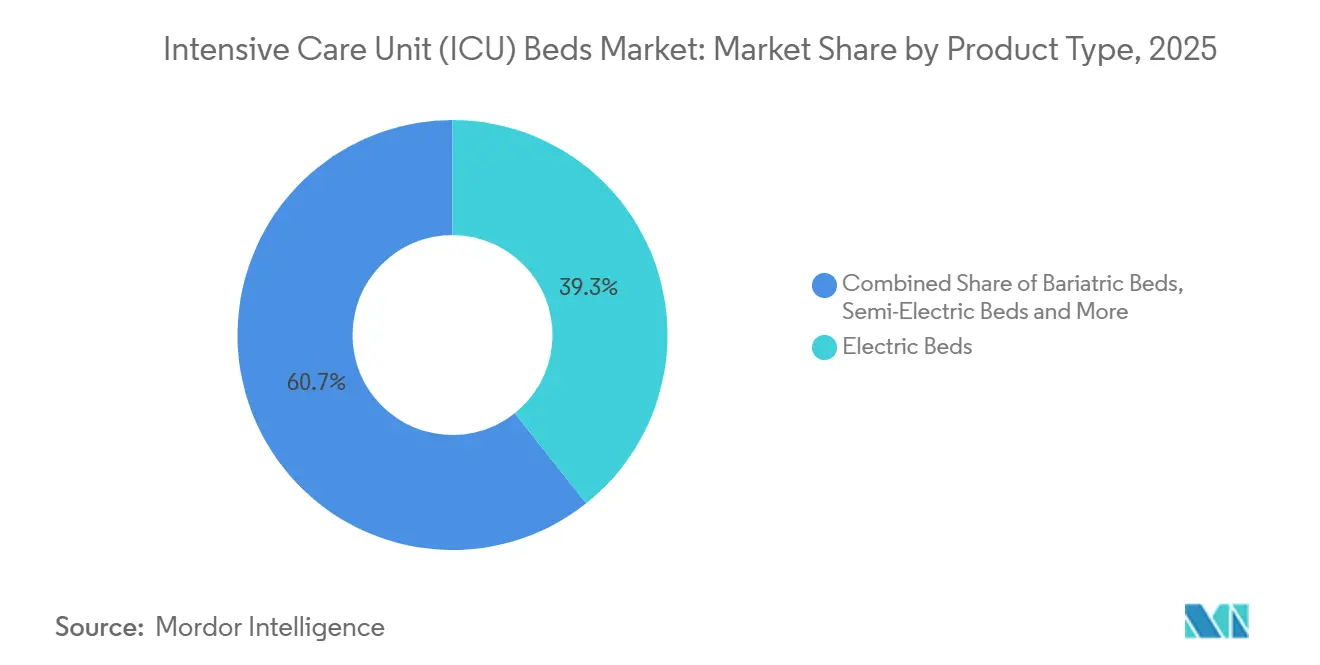

- By product type, electric beds held 39.31% of the ICU beds market share in 2025, while bariatric beds are projected to expand at 8.38% CAGR through 2031.

- By application, specialized ICUs accounted for 35.24% share in 2025, while pediatric and neonatal ICUs are forecast to grow at 9.52% CAGR through 2031.

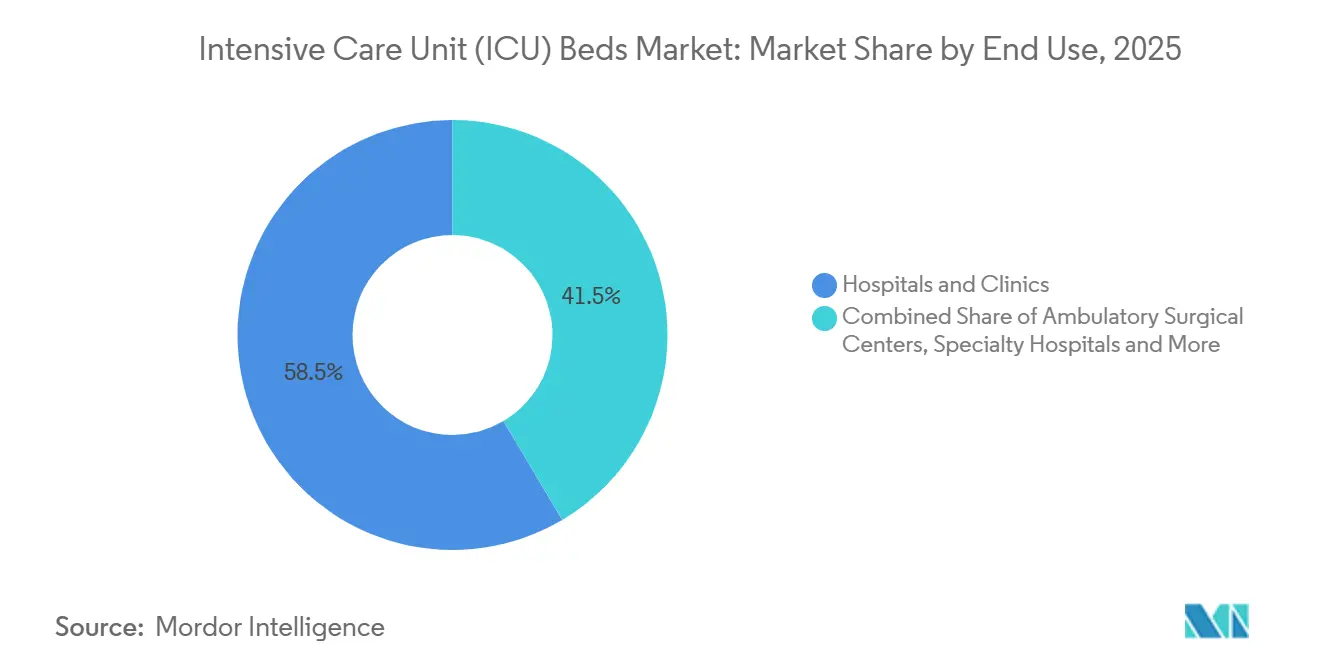

- By end use, hospitals and clinics held 58.52% share in 2025, while ambulatory surgical centers are projected to advance at 9.25% CAGR through 2031.

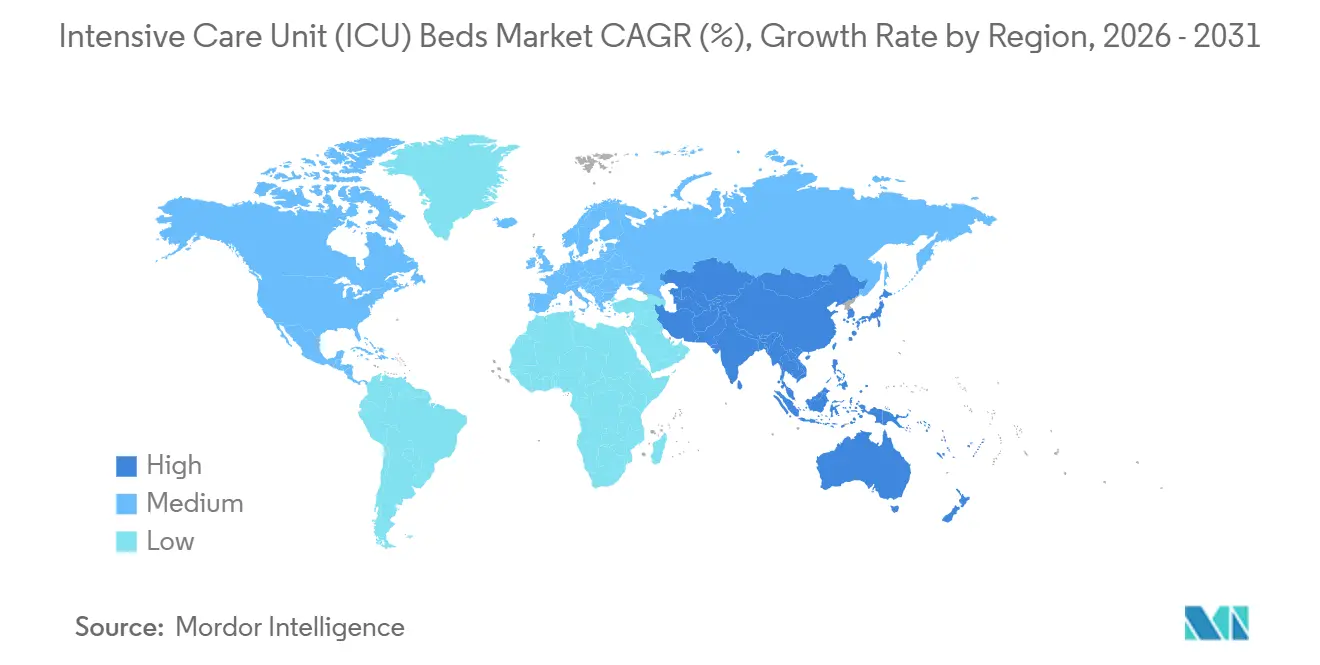

- By geography, North America held 35.22% of the ICU beds market share in 2025, while Asia-Pacific is projected to grow at 9.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Intensive Care Unit (ICU) Beds Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing ICU Demand From Chronic Disease Burden | +1.5% | Global, concentrated in North America, Europe, South & East Asia | Long term (≥ 4 years) |

| Hospital Digitization Pulls Demand Toward Smart ICU Beds | +1.2% | North America & Western Europe leading, APAC accelerating | Medium term (2-4 years) |

| ICU Capacity Expansion in Emerging Care Networks | +1.3% | APAC core, spill-over to MEA and South America | Medium term (2-4 years) |

| Shorter Bed Turnaround Time Through Infection Control Design | +0.6% | Global, early mandate compliance in Australia and the Netherlands | Medium term (2-4 years) |

| Rising Focus on Staff Ergonomics and Safe Patient Handling | +0.5% | Japan, Germany, Scandinavia, Australia | Long term (≥ 4 years) |

| Procurement Shift Toward Modular Beds With Upgradeable Interfaces | +0.5% | North America & EU procurement reform markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing ICU Demand From Chronic Disease Burden

The ICU beds market is being pushed by a disease burden that is both large and persistent across major healthcare systems. A 2025 Journal of the American College of Cardiology analysis reported 626 million cardiovascular disease cases worldwide, and a 2025 Nature Medicine study reported 569.2 million chronic respiratory disease cases with 4.2 million deaths, which keeps a high baseline of patients flowing into high dependency and intensive care settings. The demand effect is stronger when cardiovascular and respiratory conditions overlap, because those patients often require longer ICU stays and more constant monitoring, which reduces functional capacity even when the physical bed count does not change. In England, the UK Office for Health Improvement and Disparities reported 873,461 emergency respiratory admissions in the financial year ending 2025, including more than 56,000 influenza admissions, which shows that pressure is still visible even in a well funded health system[1]UK Office for Health Improvement and Disparities, “Respiratory Disease Profile, Statistical Commentary, May 2026,” UK Government, gov.uk. WHO Europe also stated in 2025 that chronic respiratory disease remains a major long term burden in the region, which supports continued replacement and expansion demand in the ICU beds market. This keeps the ICU beds market tied to a structural care need rather than a short procurement cycle.

Hospital Digitization Is Pulling Demand Toward Smart ICU Beds

The ICU beds market is also moving toward beds that work as connected clinical platforms rather than as stand alone furniture. A 2025 Frontiers in Digital Health study showed that SmartICU frameworks combining real time data integration, predictive analytics, and workflow automation reduced average bed replacement intervals from 1.7 days to near real time in a São Paulo hospital pilot. The same study reported 56 minutes saved per patient per day through digitized nursing documentation, and it linked digital ICU models to prior studies that showed 12% lower mortality, which gives hospital buyers a clearer operational and clinical case for connected beds. Machine learning sepsis prediction models cited in that research achieved an AUROC of 0.952 and flagged onset up to 4 hours before clinical presentation, which strengthens the case for beds that can transmit continuous patient data into broader ICU systems. In practice, this means hospitals are screening out lower specification products at the tender stage when they lack sensor integration, connectivity pathways, or electronic medical record compatibility. That shift supports pricing strength in the ICU beds market because value is now tied more closely to interoperability and workflow support.

ICU Capacity Expansion in Emerging Care Networks

The ICU beds market is gaining volume from new build hospitals and brownfield critical care expansions across both emerging and mature systems. India’s National Health Authority reported that AB-PMJAY had impaneled 27,742 hospitals with 1.33 million beds, including ICU capacity, as of October 2024, which points to a broad and still developing care network that can absorb new critical care equipment. In the United States, Northwestern Memorial Hospital is pursuing a USD 95.5 million project that adds 42 ICU beds at the Galter Pavilion, and the filing tied this plan to emergency department backlogs linked directly to ICU capacity shortfalls. Mount Sinai Health System is also building a new 21-bed ICU at Mount Sinai Queens, nearly tripling critical care capacity at that site and showing that expansion demand is still active in major urban systems. What matters for the ICU beds market is that new capacity projects are increasingly specifying digital and higher value beds from the start, which lifts average selling values rather than only unit volumes. This pattern keeps growth broad based because it combines infrastructure expansion with a product mix upgrade.

Shorter Bed Turnaround Time Through Infection-Control Design

The ICU beds market is also being influenced by how infection control design affects day to day bed availability. The Society of Critical Care Medicine’s 2024 adult ICU design guidelines recommended stronger infection prevention features and single patient room design principles, which gave hospital planners a more formal basis for specification upgrades in intensive care projects. A 2024 Frontiers in Medicine systematic review and meta analysis found that single patient room ICU design reduced nosocomial infection risk, which supports faster turnover and lower cleaning related disruption between critically ill patients. Australia’s Health Facility Guidelines update in April 2026 also tightened isolation room engineering and design requirements, which adds a compliance element to replacement and retrofit decisions in public hospital networks. Beds designed for easier decontamination and alignment with newer room standards can reduce idle time between patients, and that matters in units where capacity is already stretched. This gives the ICU beds market another operational reason to shift toward upgraded products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost Limits Replacement Cycles in Budget Constrained Hospitals | -1.0% | Europe (Eastern Europe, Germany), South America, MEA | Long term (≥ 4 years) |

| Certification, Tender, and Reimbursement Friction Slows Adoption | -0.8% | Europe (EU MDR), Southeast Asia, South America | Medium term (2-4 years) |

| Biomedical Maintenance and Spare Part Dependence Raises Total Cost of Ownership | -0.6% | South Asia, MEA, Sub-Saharan Africa | Long term (≥ 4 years) |

| ICU Space Constraints Reduce Retrofit Feasibility in Legacy Facilities | -0.4% | Europe (aging hospital stock), North America (pre-1990 campuses) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Limits Replacement Cycles in Budget-Constrained Hospitals

The ICU beds market still faces a clear funding barrier because full electric and connected ICU beds cost much more than manual or semi electric products. This cost gap matters most in hospitals that are trying to preserve capital while still managing high occupancy and staffing pressure. In those settings, buyers often delay replacement, split tenders across specification tiers, or reserve premium beds for new or renovated units rather than extending them across the full ICU fleet. That behavior slows the speed at which the ICU beds market can move toward higher value configurations even when clinical need is already present. It also creates a two track market in which premium suppliers compete for selective projects while lower specification products remain relevant in budget limited systems.

Certification, Tender, and Reimbursement Friction Slows Adoption

The ICU beds market also slows when regulatory approval, hospital tender cycles, and reimbursement rules do not move at the same pace. The EU MDR requirements have lengthened qualification timelines for some manufacturers, which delays product rollouts and can defer replacement programs in Europe. Public sector tendering in South America and other budget controlled systems adds another layer of delay because procurement tends to move in irregular multi quarter cycles rather than in steady annual refreshes. In the United States, CMS expanded ambulatory surgical center reimbursement support by raising ASC payment rates by 2.6% and adding 573 procedures to the Covered Procedures List, but the reimbursement path for higher acuity recovery use cases is still developing[2]Centers for Medicare & Medicaid Services, “CY 2025 Medicare Hospital Outpatient Prospective Payment System and Ambulatory Surgical Center Payment System Final Rule,” Centers for Medicare & Medicaid Services, cms.gov. This means the ICU beds market can see demand signals before buying decisions fully translate into orders, especially in newer end use channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Electric Beds Define the Standard; Bariatric Configurations Rise Fastest

Electric beds held 39.31% of the ICU beds market share in 2025, which made them the default specification in acute care settings that need continuous repositioning, pressure injury prevention, and stronger caregiver support. Their role is supported by the way hospitals are standardizing around better ergonomics, broader patient monitoring integration, and higher safety expectations in critical care units. This part of the ICU beds market also benefits from the fact that electric systems fit more easily into digitized care environments, where workflow efficiency and patient handling are being treated as procurement priorities rather than as optional upgrades. Semi electric and manual beds still retained a role in cost sensitive markets, especially where public procurement budgets remain tight and the installed base is already large. That keeps the product mix broad, even though the center of gravity in the ICU beds market is still moving toward powered configurations.

The ICU beds market size for bariatric beds is projected to expand at 8.38% CAGR through 2031, making this the fastest growing product segment. Demand is rising because hospitals need beds that can safely manage higher weight loads while still providing articulation, positioning support, and staff safety in high acuity care. Manufacturers are responding with designs that combine high weight ratings, full electric movement, integrated lateral tilt, and onboard weighing capability, which lifts clinical utility beyond basic structural support. This matters because bariatric beds can also support pressure injury prevention and early mobilization for patients who may not be well served by standard ICU configurations. As a result, the ICU beds market is seeing a segment where premium pricing is easier to defend because the clinical and operational value is more specific.

By Application: Specialized ICUs Lead; Pediatric and Neonatal Units Grow Fastest

Specialized ICUs accounted for 35.24% share of the ICU beds market size in 2025, which placed them ahead of other application categories. This lead reflects the higher clinical complexity found in cardiac, neurological, burn, and respiratory critical care settings, where beds must support more dedicated interfaces with monitoring systems, ventilators, and life support equipment. The ICU beds market therefore captures a higher average selling value in specialized units because product specifications are tighter and replacement decisions are less flexible. General ICUs still represent a large base of demand, especially in mature systems that are replacing older fleets and in expanding systems that need broad capacity first. Even there, hospitals are moving toward connectivity ready frames so current purchases do not block later digital upgrades.

The ICU beds market size for pediatric and neonatal ICUs is projected to expand at 9.52% CAGR through 2031, which makes this the fastest growing application area. India’s National Health Mission allocated USD 1.2 billion for 500 district hospital NICUs between 2024 and 2026, which points to direct policy support for neonatal critical care infrastructure. That kind of investment creates demand for beds and surfaces designed around thermoregulation compatibility, low profile caregiver access, and smaller footprints that fit neonatal care layouts. The growth case is also supported by the fact that pediatric and neonatal units face tighter product requirements, which can shorten replacement cycles when hospitals update clinical standards. For the ICU beds market, this segment brings both new capacity demand and a higher specification profile.

By End Use: Hospitals Anchor Demand; ASCs Emerge as the Fastest-Growing Channel

Hospitals and clinics held 58.52% of the ICU beds market in 2025, which confirms that the hospital setting remains the core location for critical care delivery. This position is reinforced by the infrastructure, staffing depth, and reimbursement structures needed to operate high acuity beds at scale. Specialty hospitals within this broad channel are also supporting demand as providers invest in purpose built critical care units for cardiac, oncology, neurological, and other advanced services. The ICU beds market stays anchored in this end use because hospitals still absorb most of the sickest patient volumes and most of the large capital projects. That gives the hospital channel a durable replacement cycle even when procurement timing varies across regions.

Ambulatory surgical centers are projected to grow at 9.25% CAGR through 2031, which makes them the fastest growing end use. CMS support for ASC reimbursement is widening through higher payment rates and a larger Covered Procedures List, which is helping more complex procedures move away from traditional inpatient settings. As that migration continues, the ICU beds market is gaining a new pocket of demand for ICU capable observation beds and post anesthesia step down configurations that many ASCs did not meaningfully procure before 2020. The opportunity is still developing because reimbursement rules for higher acuity pathways are maturing, but the direction of travel is clear. This gives the ICU beds market a new growth lane that complements hospital based demand rather than replacing it.

Geography Analysis

North America held 35.22% of the ICU beds market in 2025, which made it the largest regional segment. The region benefits from a deep installed ICU base, active replacement cycles, and the financial ability to move earlier toward connected and higher specification products. Mount Sinai Health System is building a new 21-bed ICU at Mount Sinai Queens, which will nearly triple the hospital’s critical care capacity and shows that capacity expansion remains active in a major urban market in 2026. Northwestern Memorial Hospital is also pursuing a 42-bed ICU expansion tied to emergency department backlogs, which points to a direct connection between hospital flow pressure and critical care investment. Europe remained the second largest regional cluster, where mature hospital systems and tighter device standards support demand for more advanced products even when procurement timing is uneven.

Asia-Pacific is projected to expand at 9.65% CAGR through 2031, giving it the fastest regional growth in the ICU beds market. This pace reflects government led healthcare expansion, rising chronic disease prevalence, and stronger private hospital investment across China, India, and Southeast Asia. India’s broad hospital network under AB-PMJAY and continued critical care buildout support volume growth, while Stryker’s June 2025 launch of the APAISER X1 for the Indian market shows that global suppliers are localizing products for this opportunity[3]National Health Authority of India, “AB-PMJAY Hospital Impanelment Data,” National Health Authority of India, pmjay.gov.in. Japan also remains important in the ICU beds market, where Paramount Bed introduced an Arius ICU bed with powered transport assistance in June 2025 to address nursing workload and mobility needs. These examples show that Asia-Pacific growth is not only about adding units, it is also about moving toward more specialized and better integrated products.

The Middle East and Africa region is growing steadily in the ICU beds market, supported by healthcare infrastructure programs in the Gulf and by private hospital investment in key urban centers. Demand in this region is often strongest for specialty ICU and bariatric configurations where hospitals are trying to align capacity with premium care offerings and medical tourism strategies. South Africa remains an anchor for sub-Saharan procurement because private hospital groups typically move faster on capital projects than many public systems. South America continues to offer a meaningful installed base, especially in Brazil, but procurement timing is often shaped by public tender cycles and reimbursement fragmentation, which keeps growth below the pace seen in Asia-Pacific. This leaves the ICU beds market with a regional profile in which North America leads on current scale, Asia-Pacific leads on growth, and the rest of the world adds selective but still important demand pockets.

Competitive Landscape

The ICU beds market shows moderate concentration, with a core group of multinational companies including Stryker Corporation, Baxter International through Hillrom, LINET Group SE, Medline Industries, Getinge AB, and Paramount Bed Co. shaping much of the premium and mid market supply base. Competition has moved beyond frame mechanics alone, because hospitals now evaluate beds in the context of connectivity, monitoring compatibility, workflow support, and post sale service reach. That shift favors larger companies that can pair hardware with software links, accessory ecosystems, and stronger biomedical support networks. It also makes it harder for smaller suppliers to compete only on price when tenders require broader product capability and long term service reliability. The ICU beds market therefore remains open to regional players, but the highest value contracts increasingly reward scale and system level integration.

Several strategic moves in 2025 and 2026 show how leading suppliers are defending or extending their position in the ICU beds market. Getinge stated in its 2025 annual reporting that it delivered organic growth across all business areas, and in 2026 it is guiding for 3% to 5% organic growth while continuing to expand its acute care platform. Getinge also received CE Mark certification at the end of March 2026 for a new generation ECLS system, which supports its strategy of building a broader acute care ecosystem around hospital customers. Stryker’s India launch of the APAISER X1 in June 2025 shows a different but related strategy, where product localization is being used to capture faster growing critical care demand in Asia. Paramount Bed’s June 2025 launch of a transport assist ICU bed points to the same competitive theme, which is solving staff workload and mobility problems with more differentiated product design.

The ICU beds market also leaves room for mid market and domestic suppliers, especially in tenders where buyers need lower cost electric products or modular upgrade paths. That opportunity is strongest in tier 2 and tier 3 hospitals across Asia-Pacific and parts of the Middle East and Africa, where hospitals want monitoring ready infrastructure but still face capital limits. At the same time, more stringent design expectations around infection control, staff safety, and digital compatibility are raising the minimum bar for all competitors. This means the ICU beds market is unlikely to become highly fragmented at the premium end, because the investment needed to stay relevant is becoming broader and more expensive. The result is a competitive field where scale, compliance readiness, and the ability to support higher specification care models matter more each year.

Intensive Care Unit (ICU) Beds Industry Leaders

Stryker Corporation

Baxter International Inc.

Getinge AB

LINET Group SE

Medline Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Mount Sinai Health System broke ground on a new 21-bed ICU at Mount Sinai Queens, nearly tripling the hospital's critical care capacity from 8 to 21 beds. The project, funded jointly by New York City (USD 7 million allocated by the Queens Borough President), New York State (USD 6 million via the State Senate Deputy Leader), and Mount Sinai capital resources, includes a class 2 procedure room enabling fluoroscopy-guided interventions on-site, reducing patient transfers and expanding complex procedural capability within the borough.

- January 2026: The Illinois Health Facilities and Services Review Board considered Northwestern Memorial Hospital's application for a USD 95.5 million project adding 42 ICU beds at the Galter Pavilion in Chicago, addressing 10,000 emergency department backlogs directly attributable to ICU capacity shortfalls and expected to complete in June 2028.

Global Intensive Care Unit (ICU) Beds Market Report Scope

As per the scope of the report, an Intensive Care Unit (ICU) bed is a specialized hospital bed designed for patients requiring intensive medical care and close monitoring. These beds are part of the ICU, which is equipped with advanced technology and medical equipment to support critically ill patients.

The segmentation of the ICU beds market is categorized by product type, application, end use, and geography. By product type, the market includes electric beds, semi-electric beds, manual beds, bariatric beds, and pediatric beds. By application, it is segmented into general ICUs, specialized ICUs, pediatric and neonatal ICUs, cardiac ICUs, and other applications. By end use, the market is divided into hospitals and clinics, ambulatory surgical centers, specialty hospitals, and others. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Electric Beds |

| Semi-Electric Beds |

| Manual Beds |

| Bariatric Beds |

| Pediatric Beds |

| General ICUs |

| Specialized ICUs |

| Pediatric and Neonatal ICUs |

| Cardiac ICUs |

| Other Applications |

| Hospitals and Clinics |

| Ambulatory Surgical Centers |

| Specialty Hospitals |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Electric Beds | |

| Semi-Electric Beds | ||

| Manual Beds | ||

| Bariatric Beds | ||

| Pediatric Beds | ||

| By Application | General ICUs | |

| Specialized ICUs | ||

| Pediatric and Neonatal ICUs | ||

| Cardiac ICUs | ||

| Other Applications | ||

| By End Use | Hospitals and Clinics | |

| Ambulatory Surgical Centers | ||

| Specialty Hospitals | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of ICU beds demand by 2031?

The ICU beds market is forecast to reach USD 3.47 billion by 2031, rising from USD 2.45 billion in 2026 at a 7.25% CAGR over 2026-2031.

Which product category leads ICU beds demand today?

Electric beds led with 39.31% share in 2025 because they fit acute care needs for repositioning, pressure management, and caregiver support.

Which application is expanding the fastest through 2031?

Pediatric and neonatal ICUs are projected to grow at 9.52% CAGR through 2031, supported by continued investment in neonatal critical care capacity.

Why are ambulatory surgical centers becoming more important for suppliers?

ASCs are projected to grow at 9.25% CAGR through 2031 as more complex procedures move into outpatient settings and create demand for ICU capable recovery beds.

Which region offers the strongest growth outlook?

Asia-Pacific has the fastest regional outlook with a 9.65% CAGR through 2031, supported by hospital expansion, chronic disease burden, and localized supplier activity.

What is the main challenge slowing replacement cycles?

High upfront pricing for full electric and connected ICU beds still delays replacement in budget constrained hospitals, especially where tendering and reimbursement are slow.

Page last updated on: