Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

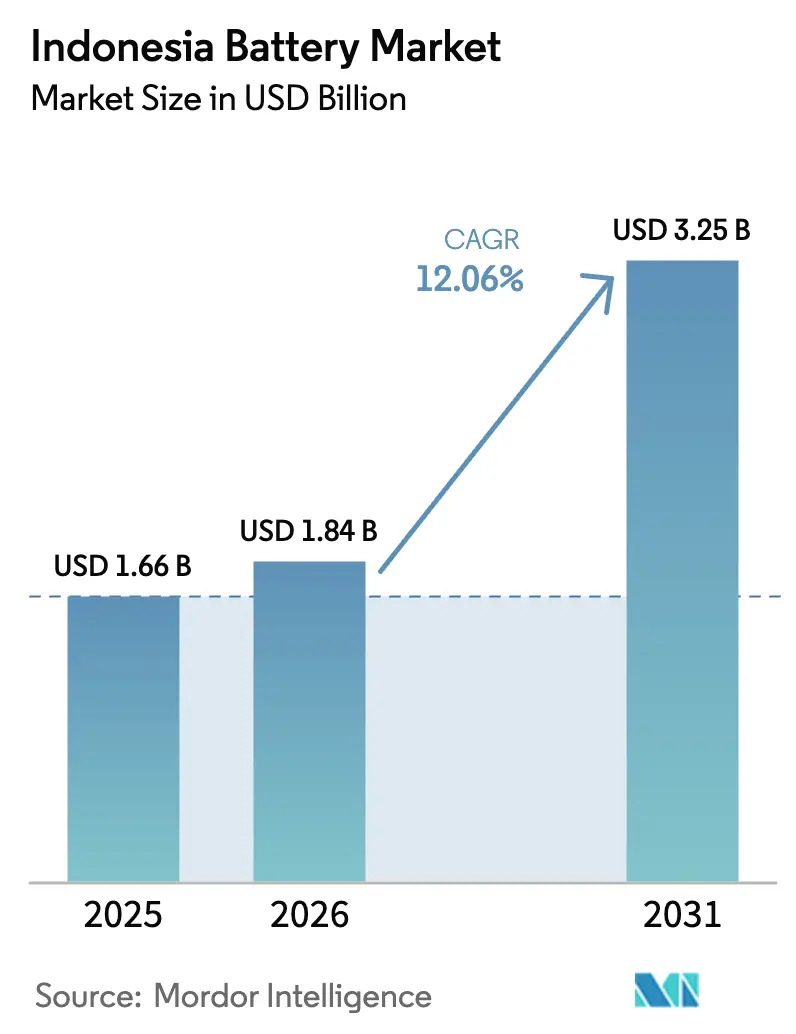

| Base Year Market Size (2025) | USD 1.66 Billion |

| Market Size (2026) | USD 1.84 Billion |

| Market Size (2031) | USD 3.25 Billion |

| Growth Rate (2026 - 2031) | 12.06% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Battery Market Analysis by Mordor Intelligence

The Indonesia Battery Market size was valued at USD 1.66 billion in 2025 and is estimated to grow from USD 1.84 billion in 2026 to reach USD 3.25 billion by 2031, at a CAGR of 12.06% during the forecast period (2026-2031).

The growth path reflects Jakarta’s move from raw-ore exporter toward integrated cell manufacturing, underpinned by 55 million t of nickel reserves, aggressive electric-vehicle (EV) targets, and steady utility-scale storage auctions.[1]U.S. Energy Information Administration, “International Energy Outlook 2025,” eia.gov Secondary batteries captured 91.3% value in 2025; lithium-ion technology led with 60.2%, while solid-state pilots signal the next step in energy-density gains. Automotive demand is scaling fastest as fiscal incentives reshape two-wheel and four-wheel assembly economics. Competitive intensity stays moderate: Chinese groups finance 61% of nickel refining and most gigafactory projects, whereas South Korean and Japanese peers recalibrate strategy after LG Energy Solution’s April 2025 exit.

Key Report Takeaways

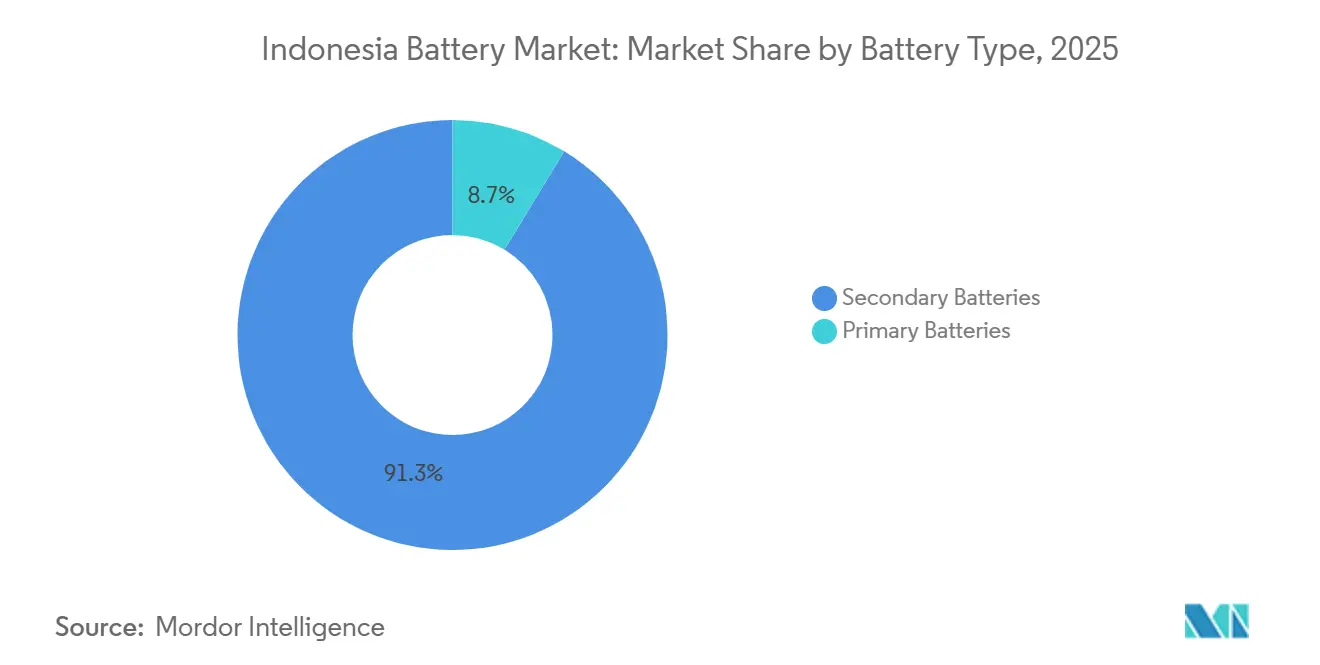

- By battery type, secondary batteries held 91.3% of Indonesia's battery market share in 2025, and the segment will rise at a 13.1% CAGR to 2031.

- By technology, lithium-ion technology led with 60.2% share in 2025; while solid-state is forecast to post the fastest growth, advancing at a 20.9% CAGR from a small 2025 base.

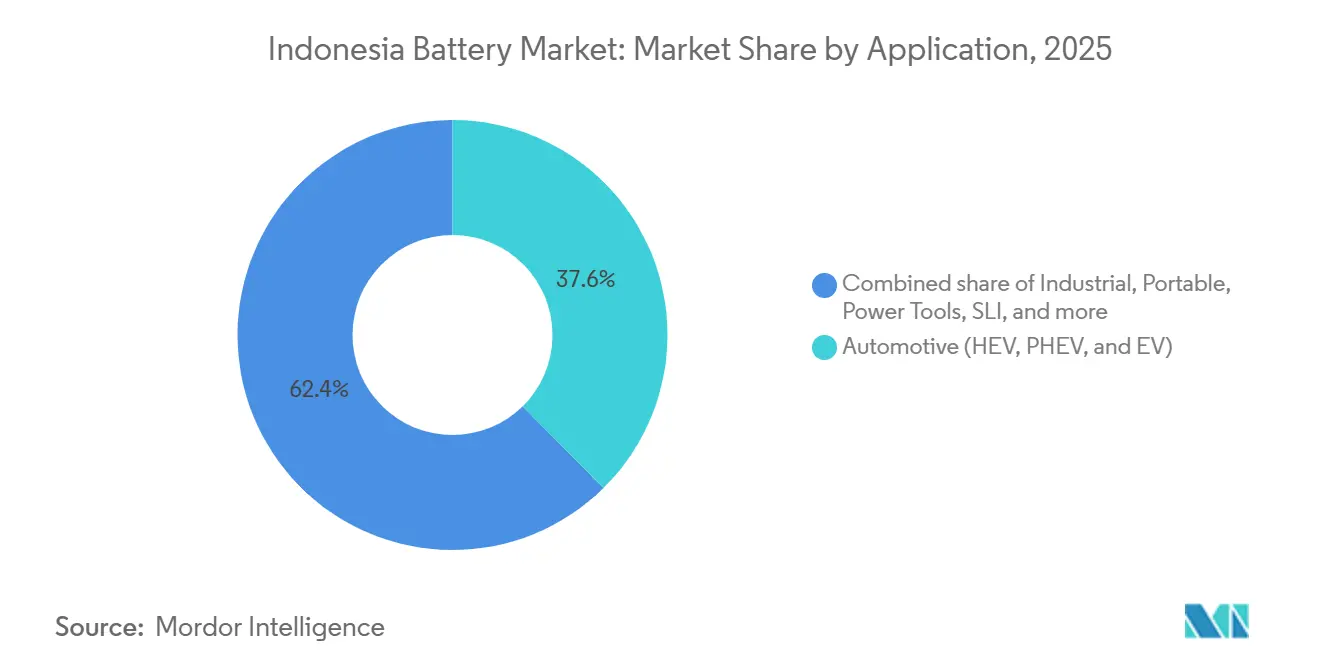

- By application, automotive commanded a 37.6% value in 2025, and the same is set to deliver a 15.5% CAGR through 2031.

- North Maluku and Central Sulawesi host 59% of the country's mined nickel output, anchoring long-term downstream value capture.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Abundant domestic nickel resources enabling downstreaming policy | +3.2% | North Maluku, Central & Southeast Sulawesi | Long term (≥ 4 years) |

| Surge in EV and e-motorcycle investments backed by fiscal incentives | +2.8% | Greater Jakarta, Bandung, Surabaya | Medium term (2-4 years) |

| Rapid uptake of consumer electronics and IoT devices | +1.5% | Java, Bali, major Sumatra cities | Short term (≤ 2 years) |

| Utility-scale energy-storage tenders to balance renewables | +2.1% | Priority PLN grid zones | Medium term (2-4 years) |

| Battery-as-a-Service swap-station roll-outs by ride-hailing firms | +1.3% | Java corridor, eight pilot cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Abundant Domestic Nickel Resources Enabling Downstreaming Policy

Indonesia produced 2.2 million t of nickel in 2024, equal to 59% of global output, while its 2020 ore-export ban forced in-country processing, expanding smelter count from 2 to 44 within eight years. The policy attracted USD 32 billion in pledged battery-chain capital but concentrated 61% of refining capacity with Chinese firms, creating dependency on foreign know-how. ESG pressure around HPAL’s 20–25 kg CO₂-equivalent profile now compels renewable power integration, increasing project capex.[2]Government of Indonesia, “Mineral Downstream Roadmap,” go.id CATL’s USD 6 billion Karawang complex illustrates the shift, linking nickel feed through closed-loop recycling to meet strict export-market traceability rules.

Surge in EV & e-Motorcycle Investments Backed by Fiscal Incentives

Jakarta allocated IDR 7 trillion subsidies, cut VAT from 11% to 1%, and waived import duties for qualifying models, lifting 2024 EV sales 73% year-over-year to 44,557 units. Yet total cost-of-ownership parity still needs 84 km daily mileage versus the current 34 km average, so up-front subsidies stay critical. TKDN thresholds jump to 60% in 2027 and 80% in 2030, pushing OEMs to localize packs and motors; Hyundai-LG’s 10 GWh line and BYD’s 150,000-unit plant are early movers. Ride-hailing fleets showcase battery-swap viability, with Grab and Gojek fielding 10,000+ two-wheel EVs across eight cities, supported by 1,200 swap stations.

Rapid Uptake of Consumer Electronics and IoT Devices

Indonesia’s smartphone and connected-device boom supports steady demand for small-format lithium-ion cells even as global share tilts to EVs. PT International Chemical Industry shifted from alkaline staples to lithium production under the ABC brand, mirroring wider retooling among legacy dry-cell makers. Domestic pack assembly benefits from supply-chain diversification out of North-East Asia, yet a lack of local lithium and cathode precursor production caps upstream gains.

Utility-Scale Energy-Storage Tenders to Balance Renewables

PLN’s 2025-2034 plan calls for 10.3 GW storage, with 3.5 GW to be online by 2030, spurring bids from CATL, Rept Battero, and CLOU Electronics. A 50 MW solar-plus-14.2 MWh BESS project in Nusantara proved cost savings of 30-40% on diesel peaking. Still, the absence of a capacity market forces merchant-risk models, delaying green-island deployments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on imported lithium salt & precursor chemicals | -1.8% | National, affecting all battery manufacturers | Long term (≥ 4 years) |

| Patchy charging / swap infrastructure outside Java corridor | -1.2% | Sumatra, Kalimantan, Sulawesi, Papua, Nusa Tenggara | Medium term (2-4 years) |

| ESG scrutiny of HPAL nickel processing raising financing risk | -1.5% | National, concentrated in North Maluku, Central Sulawesi smelting zones | Long term (≥ 4 years) |

| Commodity-price volatility eroding margin planning | -1.0% | National, with spillover effects on export-oriented manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Dependence on Imported Lithium Salt & Precursor Chemicals

With no economic lithium reserves, manufacturers import carbonate and hydroxide mainly from China and, since August 2025, Australia, exposing cost bases to price swings that ranged USD 6,000–83,000 t between 2020 and 2024.[3]International Renewable Energy Agency, “Lithium-ion supply–demand update 2025,” irena.org CATL’s Karawang hub can process 30,000 t cathode annually but still needs imported feed, limiting margins. China’s graphite export controls add another layer of supply-chain fragility, prompting UNOPS to urge stockpiling and recycling mandates, none legislated yet.

Patchy Charging / Swap Infrastructure Outside Java Corridor

Indonesia had only 588 public chargers nationwide by end-2022, mostly in Jakarta, Bandung, and Surabaya, versus PLN’s 7,146-unit goal for 2030. A 2024 PwC survey showed 65% of consumers see limited infrastructure as the top EV barrier. Swap networks mitigate urban anxiety but require land, cooling, and battery inventory, making payback tough in low-density regions. Grid codes for third-party chargers remain unpublished, delaying private investment beyond Java.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Rechargeable Cells Dominate Value and Volume

Rechargeable cells secured 91.3% of the Indonesian battery market share in 2025 and will expand at a 13.1% CAGR to 2031, lifted by EV mandates and renewable-balancing storage. Primary formats face structural decline as consumers migrate to USB-rechargeable devices. CATL, Hyundai-LG, and BYD installations bring Indonesia's battery market size for secondary cells toward the government's 140 GWh 2030 target, though lithium-import exposure endures. Regulation No. 69/2024 raises safety hurdles for primary cells, accelerating consolidation among low-cost importers.

Legacy dry-cell leader PT Intercallin hedged by adding lithium output, while niche primary use persists in remote controls and medical devices. Yet rechargeable uptake in off-grid solar lanterns and rural devices erodes even these pockets. Pressure on lead-acid starter-battery lines also rises as premium car segments adopt lithium-ion SLI replacements.

By Technology: Lithium-Ion Leads, Solid-State Emerges as Long-Term Disruptor

Lithium-ion held a 60.2% share in 2025 and anchors most near-term growth; Indonesia's battery market size for lithium-ion packs will expand as Karawang and Karawang-adjacent clusters ramp to 26.9 GWh by 2026. Lead-acid units retain dominance in aftermarket SLI but cede ground in motive and renewable storage due to lower energy density. Solid-state prototypes, though nascent, register a 20.9% CAGR on pilot shipments, hinting at 400–500 Wh/kg horizons by decade-end.

National Battery Research Institute prioritizes solid-state R&D, yet commercial tooling hurdles, high sintering temperatures, and dendrite management delay mass rollout. Sodium-ion has the potential to cut lithium dependence as soda ash is plentiful, but 95% of global capacity announcements sit in China, leaving Indonesian access uncertain. Flow batteries and sodium-sulfur remain niche for >4-hour grid use, adopted case-by-case in isolated diesel grids under donor funding.

By Application: Automotive Segment Outpaces Industrial and Portable

Automotive batteries captured 37.6% value in 2025 and are set for a 15.5% CAGR to 2031, the quickest across end uses. Indonesia's battery market share for EV packs will climb as Hyundai-LG, BYD, and Polytron escalate localized sourcing. The industrial (motive, telecom, UPS) segment sees mid-single digit growth, while portable devices gradually cede volume share as packs become non-replaceable.

Government targets of 600,000 electric cars and 13 million e-motorcycles by 2030 equate to 36.8 GWh annual pack demand, dwarfing the 10 GWh operational capacity in 2025. Polytron's battery-subscription SUVs illustrate how lower entry costs can unlock middle-class demand, though dependence on Chinese LFP cells limits deep local value capture. Power-tool battery growth hinges on industrial diversification, yet no Indonesian cell maker has announced dedicated high-drain cylindrical lines, keeping imports high.

Geography Analysis

Java dominates production, hosting CATL, Hyundai-LG, BYD, and Polytron facilities, thanks to ports, skilled labor, and proximity to auto OEMs. Upstream nickel lies 1,500 km east in North Maluku and Central Sulawesi, forcing inter-island logistics that inflate costs and carbon footprints. CATL’s dual-site model moves mixed hydroxide precipitate by sea to Karawang, balancing ore proximity with downstream clustering.

Sumatra and Kalimantan lag in both factories and chargers, yet they have high renewable potential suitable for microgrids. PLN’s 10.3 GW storage goal directs initial deployments to diesel-heavy outer islands, but tariff frameworks remain undefined, slowing build-out. Government swap-station targets imply eventual spread beyond the current eight-city footprint, but capital recovery remains uncertain in sparsely populated provinces.

Export-oriented growth depends on meeting EU battery passport and U.S. IRA rules. Heavy Chinese investment complicates North American market access, while EU carbon-footprint caps raise pressure for renewable-powered smelting. Indonesia Battery Corporation is courting non-Chinese partners to diversify offtake and mitigate tariff risk, though no deals were confirmed by end-2025.

Competitive Landscape

Chinese firms control 61% of nickel refining and most announced gigafactory capacity, positioning CATL, BYD, Huayou Cobalt, CNGR, and Rept Battero as dominant investors. South Korean and Japanese incumbents retain expertise but reassess exposure after LG Energy Solution’s USD 9.8 billion pull-out, replaced by Huayou Cobalt in April 2025. Domestic entrants leverage state incentives: Polytron’s SUV line and Indonesia Battery Corporation’s swap-station alliances seek share in value-sensitive segments, though each relies on foreign cell technology.

White-space opportunities include sodium-ion production, hard-carbon anodes from biomass, and digital battery-passport services. BTR New Materials' 80,000 t anode plant at Morowali sets a precedent for upstream materials localization, yet graphite export curbs add volatility. Certification complexity under IEC 62133 and differing national deviations still raises costs for mid-tier Indonesian exporters, incentivizing bundled testing services by TÜV Rheinland and SGS.[4]TÜV Rheinland Indonesia, “Battery Certification Pathways 2025,” tuv.com

Indonesia Battery Industry Leaders

GS Yuasa Corporation

PT Century Batteries Indonesia (Nipress)

CATL

PT Indonesia Battery Corporation (IBC)

PT Motobatt Indonesia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: In Karawang District, West Java Province, the largest integrated electric vehicle battery ecosystem project in Southeast Asia has been inaugurated. The groundbreaking ceremony, spearheaded by the ANTAM–IBC–CBL consortium, took place at Artha Industrial Hills in Karawang, West Java.

- June 2025: Ningbo Contemporary Brunp Lygend Co., Ltd. (CBL), a subsidiary of Guangdong Brunp Recycling Technology Co., Ltd (Brunp) and part of the Contemporary Amperex Technology Co., Limited (CATL) family, has teamed up with PT Aneka Tambang Tbk (ANTAM) and Indonesia Battery Corporation (IBC) to launch the Indonesia Battery Integration Project. The groundbreaking ceremony took place in Karawang, located in Indonesia's West Java Province. The ambitious project, set to span over 2,000 hectares, comes with a hefty planned investment of nearly USD 6 billion.

- February 2025: Merdeka Battery Materials secured environmental approval for its USD 1.8 billion HPAL plant aimed at 120,000 t/y mixed hydroxide precipitate output, with COD in 2028.

Indonesia Battery Market Report Scope

An electric battery is an electrical power source consisting of one or more electrochemical cells connected to external connections for powering electrical devices. When a battery supplies power, its positive terminal serves as the cathode, and its negative terminal serves as the anode.

The market is segmented by battery type, technology, and application. By battery type, the market is segmented into primary batteries and secondary batteries. By technology, the market is segmented into lead-acid, Li-ion, nickel-metal hydride, nickel-cadmium, sodium-sulfur, solid-state, flow battery, and emerging chemistries. By application, the market is segmented into automotive, industrial, portable, power tools, SLI, and other applications. For each segment, the market sizing and forecasts have been done on the basis of revenue.

By Battery Type

| Primary Batteries |

| Secondary Batteries |

By Technology

| Lead-acid |

| Li-ion |

| Nickel-metal hydride |

| Nickel-cadmium |

| Sodium-sulfur |

| Solid-state |

| Flow Battery |

| Emerging chemistries |

By Application

| Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) |

| Portable (Consumer Electronics, etc.) |

| Power Tools |

| SLI |

| Other Applications |

| By Battery Type | Primary Batteries |

| Secondary Batteries | |

| By Technology | Lead-acid |

| Li-ion | |

| Nickel-metal hydride | |

| Nickel-cadmium | |

| Sodium-sulfur | |

| Solid-state | |

| Flow Battery | |

| Emerging chemistries | |

| By Application | Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) | |

| Portable (Consumer Electronics, etc.) | |

| Power Tools | |

| SLI | |

| Other Applications |

Key Questions Answered in the Report

How fast is battery demand growing in Indonesia?

Industry revenue is rising at a 12.06% CAGR from 2026 to 2031, reaching USD 3.25 billion by the end of 2031.

Which chemistry leads Indonesia's cell shipments today?

Lithium-ion batteries held 60.2% market share in 2025, driven by EV and utility-scale storage projects.

What hurdles slow EV adoption beyond Java?

Limited public chargers and swap stations outside major Java cities remain the primary bottleneck to wider EV uptake.

Why is solid-state technology important for Indonesia?

Solid-state prototypes show the fastest CAGR at 20.9%, promising higher energy density and improved safety over liquid-electrolyte cells.

How dependent are local plants on imported feedstock?

All domestic gigafactories still rely on imported lithium salt and anode materials, exposing them to global price volatility.

Who are the leading investors in Indonesia's gigafactory pipeline?

Chinese companies such as CATL, BYD, and Huayou Cobalt headline capacity announcements, while Hyundai-LG anchors South Korean participation.

Page last updated on: