Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.65 Billion |

| Market Size (2026) | USD 0.79 Billion |

| Market Size (2030) | USD 2.08 Billion |

| Growth Rate (2026 - 2031) | 21.16% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Modular Kitchen Market Analysis by Mordor Intelligence

India modular kitchen market size is expected to increase from USD 0.653 billion in 2025 to USD 0.790 billion in 2026 and reach USD 2.08 billion by 2031, growing at a CAGR of 21.16% over 2026-2031. Urbanization is compressing living spaces and pushing households toward modular solutions that optimize every square foot while maintaining visual appeal. Compliance also matters in India’s modular kitchen market as BIS storage-unit certification under IS 17634:2022 moves to full enforcement over 2026, promoting quality assurance and shifting procurement toward certified vendors. Omnichannel experiences and digital configurators are compressing decision cycles and expanding access in Tier-2 and Tier-3 cities, boosting brand-led penetration in India’s modular kitchen market beyond traditional metro cores.

Key Report Takeaways

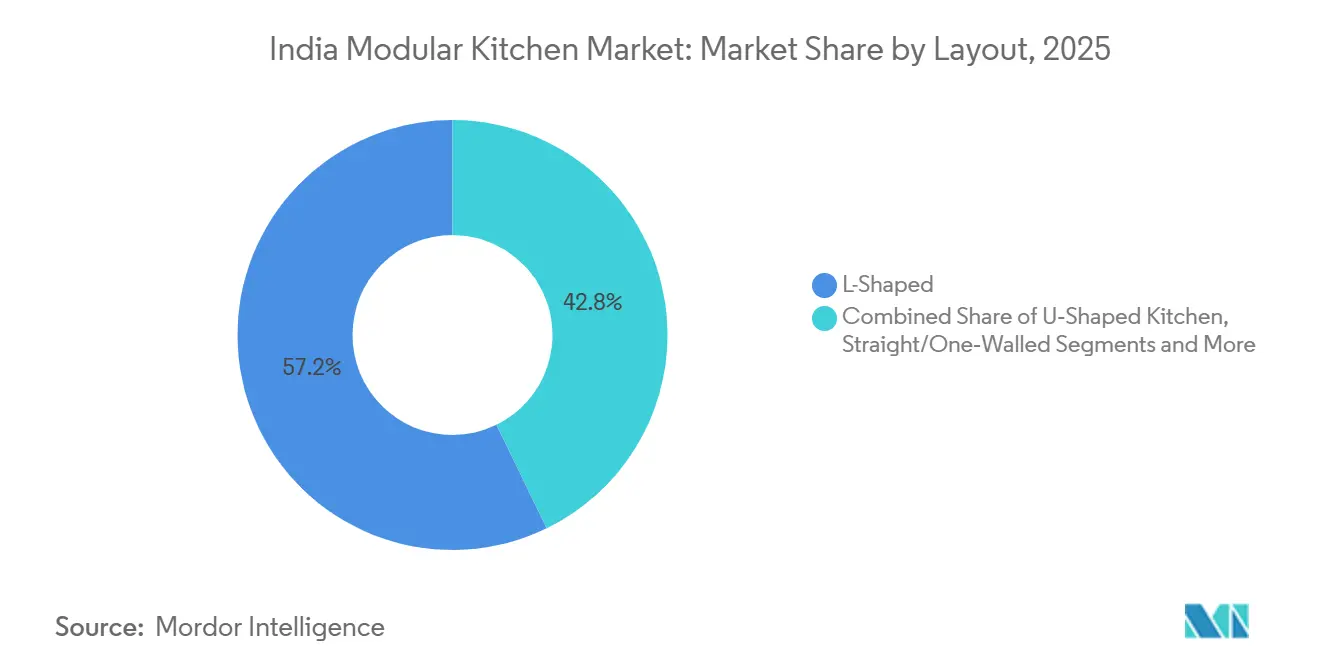

- By design, L-shaped layouts led with 57.23% revenue share in 2025, while parallel or galley configurations are poised to expand at a 24.12% CAGR through 2031.

- By structure, the unorganized segment held 68% share in 2025, whereas the organized segment is projected to compound at a 23.31% CAGR through 2031 as BIS certification tightens procurement.

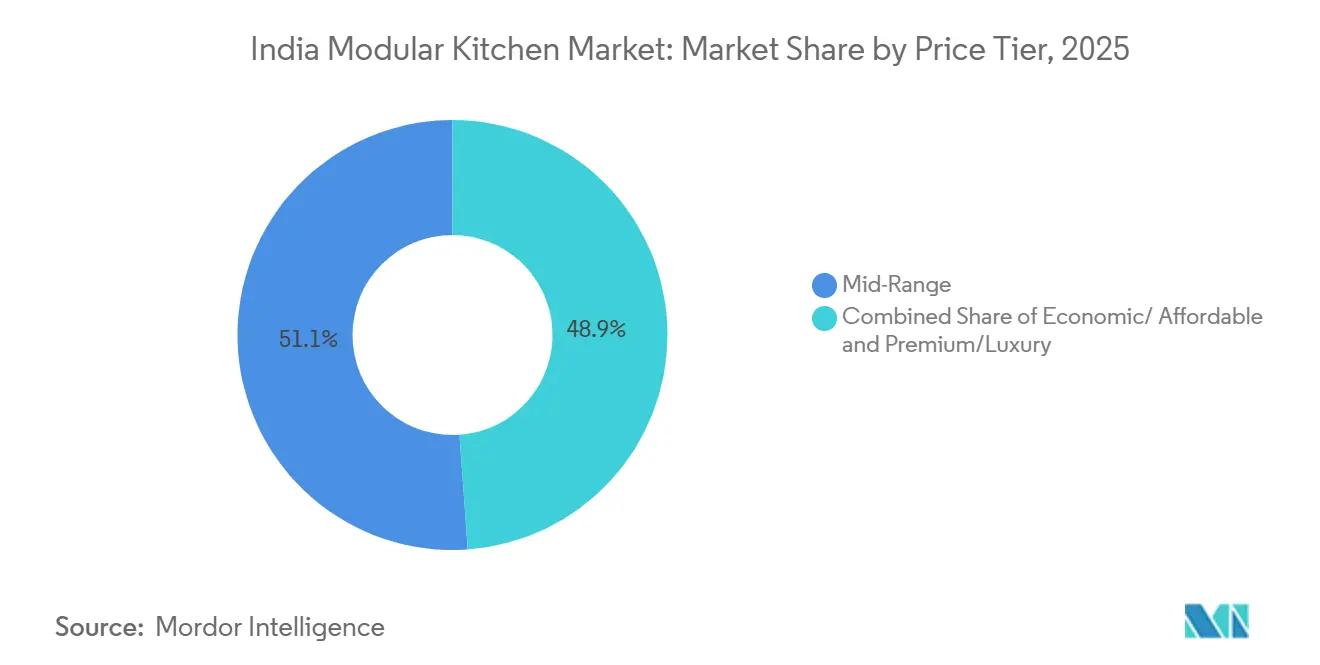

- By pricing tier, the mid-range bracket accounted for 51.13% of market share in 2025, while the premium tier posted the fastest 23.34% CAGR through 2031.

- By end user, residential buyers commanded 78.23% share in 2025, with residential demand set to grow at a 21.80% CAGR through 2031.

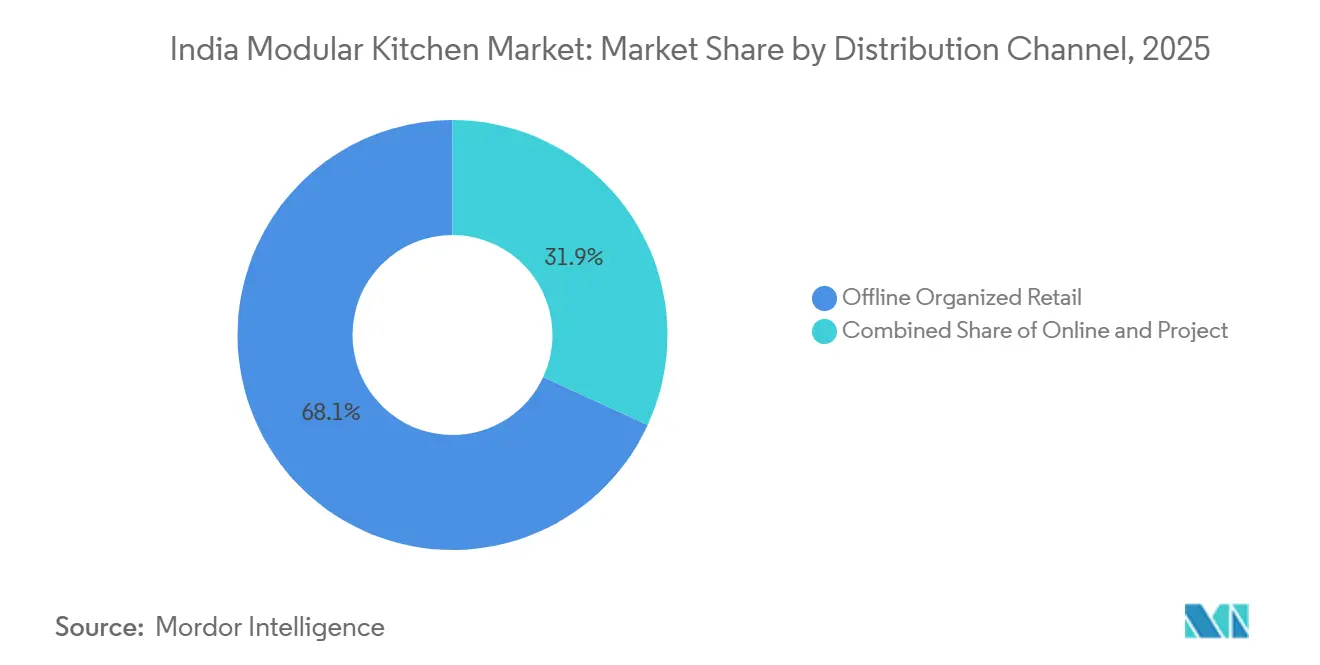

- By distribution channel, offline organized retail captured 68.12% share in 2025, and online platforms are forecast to post a 22.33% CAGR through 2031.

- By region, North India led with 31.23% share in 2025, while East India is projected to advance at a 22.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Modular Kitchen Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Apartment Handovers And Urban Home Upgrades Catalyzing Turnkey Kitchen Adoption In Tier 1–2 Cities | +4.8% | North and West, including Delhi NCR, Mumbai, Pune, with South metro spillover | Medium term (2-4 years) |

| Organized Brands and Omnichannel Expansion Into Tier 2/3 Improving Access And Standardization | +3.9% | East and North-East plus Tier-2 and Tier-3 clusters nationwide | Medium term (2-4 years) |

| Residential Renovations and Premiumization Lifting Modular Kitchen Attach Rates | +3.2% | Metro cores and affluent suburbs | Short term (≤ 2 years) |

| Integrated Built-In Appliances and Smart Features Necessitating Modular Cabinetry Ecosystems | +4.5% | Urban centers with higher connected-appliance adoption | Long term (≥ 4 years) |

| Builder–Developer Bundling of Modular Kitchens in the Project Channel Improving Base Install Rates | +2.8% | PMAY-U geographies and metro peripheries, expanding Tier-2 cities | Medium term (2-4 years) |

| Localization of Components And Assemblies to De‑Risk Imports and Cut Lead Times | +2.1% | National, with hubs in Gujarat, Maharashtra, Madhya Pradesh | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Apartment Handovers and Urban Home Upgrades Catalyzing Turnkey Kitchen Adoption in Tier 1-2 Cities

Developer bundling has changed the rhythm of purchase decisions in India’s modular kitchen market as project-channel share rose to 35% of organized volumes in 2026 from 24% a year earlier. Builders have begun to treat turnkey kitchens as a sales differentiator that reduces post-occupancy service issues and drives consistent finish quality in new apartments. Organized brands have aligned installation windows to possession schedules, with seven-day builds now a prominent promise in metros and larger Tier-2 cities. PMAY-U 2.0 requirements for functional kitchens in Affordable Housing in Partnership units are shaping baselines across subsidized projects and encouraging standardized specifications that align with modular designs. As Tier-2 demand scales, India’s modular kitchen market benefits from earlier showroom entry, structured installation networks, and developers who now integrate branded kitchens into model flats to accelerate bookings.

Organized Brands and Omnichannel Expansion Into Tier 2-3 Improving Access and Standardization

In smaller cities, showroom density and omnichannel design tools have become the core enablers of reach and conversion for India’s modular kitchen market. Godrej Interio has targeted Tier-2 and Tier-3 demand through expanded kitchen galleries and dealer investments that strengthen local availability and after-sales support. IKEA India’s online channel contributes a growing share of sales and demonstrates how 3D configurators and remote consultations reduce decision friction before a store visit. BIS storage-unit certification under IS 17634:2022 is moving to stricter enforcement, and compliance is increasingly a selection criterion for government procurement and quality-conscious retail buyers. Together, these shifts are raising the predictability of quality and service in India’s modular kitchen market and are narrowing the perceived risk gap with unorganized alternatives.

Residential Renovations and Premiumization Lifting Modular Kitchen Attach Rates

Renovation cycles in 7- to 10-year-old apartments are now a key driver of growth in India’s modular kitchen market, as homeowners replace site-built carpentry to achieve fit-and-finish consistency, warranties, and faster installation. Premium tiers are outperforming, supported by demand for integrated appliances, smooth-motion hardware, and surface finishes that align with open-plan living. The premium bracket is tracking a 23.34% growth trajectory through 2031, above the overall market rate and reflecting rising aspirations in larger cities. Entry-level planning and assembly packages from large-format retailers, which start under INR 9,999 (USD 120.5), help first-time buyers cross the threshold and build trust in modular solutions. Localization of hardware and component sourcing by leading brands is reducing lead times and forex exposure, thereby improving inventory availability of premium finishes and fittings across urban markets.

Integrated Built-in Appliances and Smart Features Necessitating Modular Cabinetry Ecosystems

Connected-appliance adoption is influencing base-unit depths, service clearances, and ventilation paths, which strengthens the case for standardized modular cabinetry in India’s modular kitchen market. Buyers expect seamless appliance integration, soft-close mechanisms, and concealed cable runs that require precise cutouts and predictable tolerances. Organized brands partner with appliance makers earlier in the design process to test fit, airflow, and acoustic performance so that installers can deliver the promised noise and heat profiles in finished kitchens. Hardware portfolios are evolving in step, with locally made hinges and runners designed for frequent use and silent operation, which increases perceived quality in everyday interaction. These integration and hardware trends reinforce the platform-like nature of India’s modular kitchen market, where cabinetry, appliances, and fittings must interoperate reliably over multi-year service lives.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost versus site-built carpentry in a price-sensitive market | -4.2% | Pan-India, acute in Tier-2 and Tier-3 cities | Medium term (2-4 years) |

| Fragmented, unorganized sector and service inconsistencies | -3.6% | Tier-2 and Tier-3 cities, rural peripheries | Medium term (2-4 years) |

| Skilled designer-installer shortages are affecting timelines and quality | -2.1% | Nationwide, more acute in emerging clusters | Short term (≤ 2 years) |

| Hardware and surface supply volatility and forex exposure are inflating BOM costs | -1.9% | Import-exposed brands, late localizers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Versus Site-Built Carpentry in a Price-Sensitive Market

Affordability remains a core friction in India’s modular kitchen market, where organized solutions often cost more than site-built carpentry, especially in cities with lower labor costs. Brands have introduced standardized entry lines that compress starting prices for basic L-shaped modules to improve access for first-time buyers. Financing access outside metro areas remains limited compared with large cities, widening the barrier to adoption in areas where cash-flow flexibility is more important. The unorganized sector’s low compliance costs allow informal pricing that undercuts BIS-certified options and sustains share in budget-sensitive segments. As compliance and consumer education improve, brand-led offerings that combine warranties, predictable installation schedules, and financing are better positioned to close the gap in India’s modular kitchen market.

Fragmented Unorganized Sector and Service Inconsistencies

A large, unorganized base continues to serve most installations and competes via customization, proximity, and flexible payment arrangements that organized players cannot always match in smaller cities. Service predictability remains a challenge because informal networks are less likely to offer long-duration warranties or consistent after-sales support. Organized brands are responding with 10-25-year cabinet and hardware guarantees in order to signal long-term reliability to risk-averse buyers. BIS certification under IS 17634:2022 is raising the compliance bar for vendors and installers, likely consolidating procurement toward certified brands over the next two to four years. As enforcement improves, India’s modular kitchen market will see more consistent quality, faster replacement cycles, and clearer service accountability anchored by brand-backed networks.

Segment Analysis

By Design: Parallel Layouts Outpace Traditional L-Shapes in Compact Urban Units

L-shaped designs accounted for 57.23% of installations in 2025, while Parallel or Galley formats are projected to register a 24.12% CAGR through 2031 as compact homes prioritize corridor efficiency. This pattern reflects smaller carpet areas and the need to avoid dead corners, which encourages straight runs and balanced work triangles in India’s modular kitchen market. Brands are expanding parallel-ready module sets that fit 8- to 10-foot walls and integrate chimney ducting and deep drawers for staples. Digital configurators now show buyers how a galley layout can preserve walkway clearance and storage in a single view, speeding decisions for first-time buyers. PMAY-U 2.0 implementation has codified basic kitchen amenities in affordable housing, which favors predictable module footprints that work across thousands of units.

India’s modular kitchen market also benefits from tiered pricing, enabling smaller homes to adopt straight and parallel options without the delays associated with customization. Large-format retailers offer parallel kits starting at INR 2 lakh (USD 2,400), including installation, providing an attractive starting point for buyers who want warranties and quick handovers. As space-optimized apartments spread into Tier-2 cores, demand for parallel and straight formats in India’s modular kitchen market will continue to outpace traditional L-shaped designs, even as L-shapes retain a dominant share today. Project bundling in new towers further increases the presence of standardized layouts that installation crews can complete within one week.

By Structure: BIS Mandates Propel Organized Segment Past Unorganized Laggards

Unorganized carpenters retained a 68% share of installations in 2025, yet the organized segment is on track for 23.31% growth as certified products and warranties become selection filters. This transition is central to India’s modular kitchen market because BIS certification requirements under IS 17634:2022 now shape procurement choices in government projects and quality-led retail. Organized players are using omnichannel design, curated finishes, and assured timelines to take share in cities where unlicensed workshops previously dominated. This mix shift supports higher service consistency in India’s modular kitchen market and tends to reduce rework since certified installers follow standardized fit protocols.

Brands with in-house or partner academies for installers are building an execution moat and are positioned to lead organized penetration across project channels. Digital configurators and factory pre-assembly reduce on-site error rates and keep installs within seven days, which builds confidence among developers and retail buyers. As BIS enforcement scales, India’s modular kitchen market will direct a greater share of spend to certified modules and licensed hardware suppliers that can document compliance. The organized cohort will therefore expand its contribution to India’s modular kitchen market faster than its unorganized peers, especially in cities where project bundling is rising.

By Pricing Tier: Premium Brackets Outpace Mid-Range Despite Affordability Pressures

Mid-Range kitchens held 51.13% share in 2025, supported by balanced value, finish durability, and warranty coverage, while the Premium tier is projected to grow at 23.34% through 2031. Premium buyers prioritize integrated appliances, quiet-motion hardware, and longer guarantees, which reward organized brands with higher average order values. Retailers are lowering adoption barriers by offering packaged planning and assembly priced under ₹9,999 (USD 120.5), introducing modular quality to first-time buyers. As aspirational finishes and handleless designs gain traction, India’s modular kitchen market will see higher specification levels in metro and upper-tier suburbs.

Entry-level offerings serve as on-ramps, with standardized L-shaped modules positioned at INR 1.25 lakh (USD 1.5 thousand), which is compelling for households that value speed, predictability, and warranties. Localization in hardware and surface components is improving feature availability within Mid-Range price points and reducing foreign exchange risk for vendors. The Premium tier’s outperformance is likely to continue as integrated design and open-plan layouts elevate the kitchen’s role in home life in India’s modular kitchen market.

By End User: Residential Renovations Lift Attach Rates Beyond New-Build Installations

Residential buyers commanded a 78.23% share in 2025, and Residential demand is set to expand at a 21.80% CAGR through 2031 as renovation cycles replace aging carpentry in 7- to 10-year-old homes. Retrofit customers increasingly value rapid installation, warranty coverage, and integrated appliances, which align with organized-channel strengths. Digital-led design journeys and omnichannel consultations encourage faster conversion for homeowners who have already experienced service issues with earlier site-built cabinetry. This dynamic improves brand-led share in India’s modular kitchen market by enabling organized vendors to manage surveys, customizations, and installations under a single SLA.

Commercial demand, led by hospitality, workplace, and cloud kitchens, is also rising as standardized modules improve hygiene and speed to service. B2B channels help scale and provide repeatable specifications that installers can deliver quickly at a portfolio level. Vertical integration and factory pre-assembly further compress field timelines and reduce complexity for both Residential and Commercial buyers in India’s modular kitchen market. As these operational advantages compound, the Residential segment will continue to account for the majority of India’s modular kitchen market throughout the forecast.

By Distribution Channel: Online Configurators Disrupt Offline Retail’s Showroom Dominance

Offline Organized Retail captured 68.12% share in 2025 and remains the primary route for high-involvement purchases that benefit from tactile validation of finishes and mechanisms. Online Platforms are growing at a 22.33% CAGR as configurators translate floor plans into options that buyers can quickly compare and then complete via remote consultations. Project channels have accelerated because developers use bundled modular kitchens to differentiate apartments and reduce handover friction. These changes reinforce an omnichannel customer journey in India’s modular kitchen market, where discovery and design can occur online while installation and service are coordinated locally.

Showroom investments continue as brands seek design hubs where measurements, finishes, and appliance pairings are finalized before production. Dealer networks are expanding into Tier-2 and Tier-3 centers to pre-empt unorganized competitors and to improve service coverage for project handovers. As BIS enforcement scales, organized routes will capture more spend in India’s modular kitchen market because compliance becomes a gating criterion in both public and private procurement.

Geography Analysis

North India held 31.23% share in 2025, supported by higher concentrations of premium apartments and dual-income households that value integrated appliances and long warranties. PMAY-U 2.0 has reinforced standardized kitchen baselines in the North’s affordable projects and influenced specification norms that favor modular designs. East India is set to advance at a 22.41% CAGR as showroom density rises in Tier-2 state capitals and as project bundling accelerates in growing urban corridors. These patterns signal the broadening footprint of India’s modular kitchen market beyond traditional metros and support deeper brand penetration in emerging cities.

West India’s momentum is anchored by Mumbai and Pune, where high-rise handovers and renovation cycles yield steady demand for modular upgrades. Builders in the West are also using turnkey kitchens to differentiate inventory, which further supports organized share in India’s modular kitchen market. South India maintains a lead in technology-friendly households and shows faster uptake of integrated appliances that require standard cabinet depths and solid ventilation design. Together, these regions reflect varied starting points but a common tilt toward certified, warranty-backed modular solutions.

North-East India is a smaller base today, but it is recording steady compounded gains as showrooms and trained installers enter Guwahati and nearby clusters. Enforcement timelines for BIS storage-unit certification are strongest in major metros. They are cascading outward, creating a staggered yet consistent path for organized consolidation in India’s modular kitchen market. Dealer expansion in West and Central India shows how mid-market brands lock in distribution before premium players deepen their presence, thereby sustaining the channel foundation required for project bundling growth.

Competitive Landscape

India’s modular kitchen market remains fragmented as compliance and project bundling raise barriers to entry. Legacy furniture and home brands leverage captive manufacturing and nationwide stores to scale installations, while digital-first platforms compete with design software, remote consultations, and speed of decision. Developer partnerships have emerged as a priority route that delivers volume predictability and single-point accountability, which improves after-sales economics for brands. These strategies align with rising expectations for seven-day installations and warranty-backed service that mark the organized proposition in India’s modular kitchen market.

Compliance is a catalyst, since BIS storage-unit certification under IS 17634:2022 is tightening eligibility for government procurement and pushing certified options into mainstream retail. Localization intensifies this consolidation as new facilities expand domestic capacity for runners, hinges, and drawers, which cuts lead times and forex sensitivity. Hettich’s Indore plant, part of a broader India investment plan, exemplifies this shift and adds hardware depth for modular brands that commit to weekly installation schedules. Premium segments also benefit from appliance-cabinet alignment, which differentiates organized players that co-design with appliance makers early in the project cycle.

Investments in installer training are now a core capability that pushes organized brands ahead on error rates and repeatability at scale. Factory pre-assembly reduces field complexity and supports faster handovers, increasing referrals and raising Net Promoter Scores in India’s modular kitchen market. Capital inflows into mid-market brands are accelerating showroom rollouts in Tier-2 and Tier-3 markets and are aimed at capturing early-mover advantages before premium incumbents expand their dealer networks. This evolving mix across manufacturing, channels, and capability-building defines near-term competition and underlines how India’s modular kitchen industry is maturing into a more standardized, service-centric ecosystem.

India Modular Kitchen Industry Leaders

Godrej Interio

Sleek (Asian Paints)

Livspace

HomeLane

IKEA India

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Hettich India inaugurated a new automated manufacturing plant in Indore’s Pithampur Industrial Area dedicated to undermount drawer runners, adding significant local capacity as part of a broader INR 2,000 crore program, with the Indore site investment at INR 700 crore. This expansion strengthens domestic supply for premium motion hardware used in modular kitchens.

- February 2026: Würfel became the first Indian modular kitchen brand to win the prestigious Good Design Award 2025 for its Katha Kitchen Series, and announced participation as the first Indian kitchen OEM at EuroCucina (part of Salone del Mobile) in April 2026, elevating India's design credentials on the global stage and signaling premiumization ambitions through European craftsmanship and lifetime warranties

- September 2025: CARYSIL Limited announced a INR 25 crore expansion at its Bhavnagar facility to boost kitchen appliance production capacity by 50,000 units annually (raising total capacity to 150,000 units), including a new factory building and an integrated Glass Processing Plant funded through QIP and internal accruals, with commercial production targeted for Q1 FY2026-27 to strengthen its position in the home appliance market

India Modular Kitchen Market Report Scope

Modular kitchen designs break down large systems into essential parts to meet various customer needs, replicating flexibility and agility at the installation site. These layouts maximize efficiency and elegantly supplement storage systems by utilizing every nook and corner of the area in context. The study briefly describes the India modular kitchen market and includes details on modular kitchen market size, investment by the manufacturers, and technological innovations in modular kitchens. The India modular kitchen market is segmented by product, by end-user, and by distribution channel. By product, the market is segmented into floor cabinets and wall cabinets, tall storage cabinets, and others. By end user, the market is segmented into residential, and commercial. By distribution channel, the market is segmented into offline which is further segmented into contractors, builders, and others, and by online. The report also covers the market sizes and forecasts for the India modular kitchen market in value (USD) for all the above segments.

By Design

| L-Shaped Kitchen |

| U-Shaped Kitchen |

| Straight/One-Walled Kitchen |

| Parallel Shaped Kitchen |

By Structure

| Organized |

| Unorganized |

By Pricing Tier

| Economic/ Affordable |

| Mid/Range |

| Premium/Luxury |

By End User

| Residential |

| Commercial |

By Distribution Channel

| Retail | Offline |

| Project |

By Region

| North |

| West |

| East |

| South |

| By Design | L-Shaped Kitchen | |

| U-Shaped Kitchen | ||

| Straight/One-Walled Kitchen | ||

| Parallel Shaped Kitchen | ||

| By Structure | Organized | |

| Unorganized | ||

| By Pricing Tier | Economic/ Affordable | |

| Mid/Range | ||

| Premium/Luxury | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | Retail | Offline |

| Project | ||

| By Region | North | |

| West | ||

| East | ||

| South | ||

Key Questions Answered in the Report

What is the current size and growth outlook for India’s modular kitchen market to 2031?

The market is expected to increase from USD 0.65 billion in 2025 to USD 0.79 billion in 2026 and reach USD 2.08 billion by 2031, at a 21.16% CAGR.

Which design formats are leading and growing fastest in India’s modular kitchen market?

L-shaped layouts led with 57.23% share in 2025, while Parallel or Galley formats are projected to grow at a 24.12% CAGR through 2031.

How is compliance affecting competition in India’s modular kitchen market?

BIS storage-unit certification under IS 17634:2022 is tightening eligibility for procurement and accelerating the shift toward certified brands with standardized quality and warranties.

Where is geographic growth most pronounced for India’s modular kitchen market?

East India shows the fastest trajectory with a projected 22.41% CAGR (2026-2031), while North India led by share at 31.23% in 2025.

What is changing on routes to market for India’s modular kitchen market

The project channel expanded to 31.88% of organized volumes in 2026, and online platforms are scaling as configurators compress decision cycles while offline organized retail remains the primary touchpoint.

Page last updated on: