India Anchors And Grouts Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

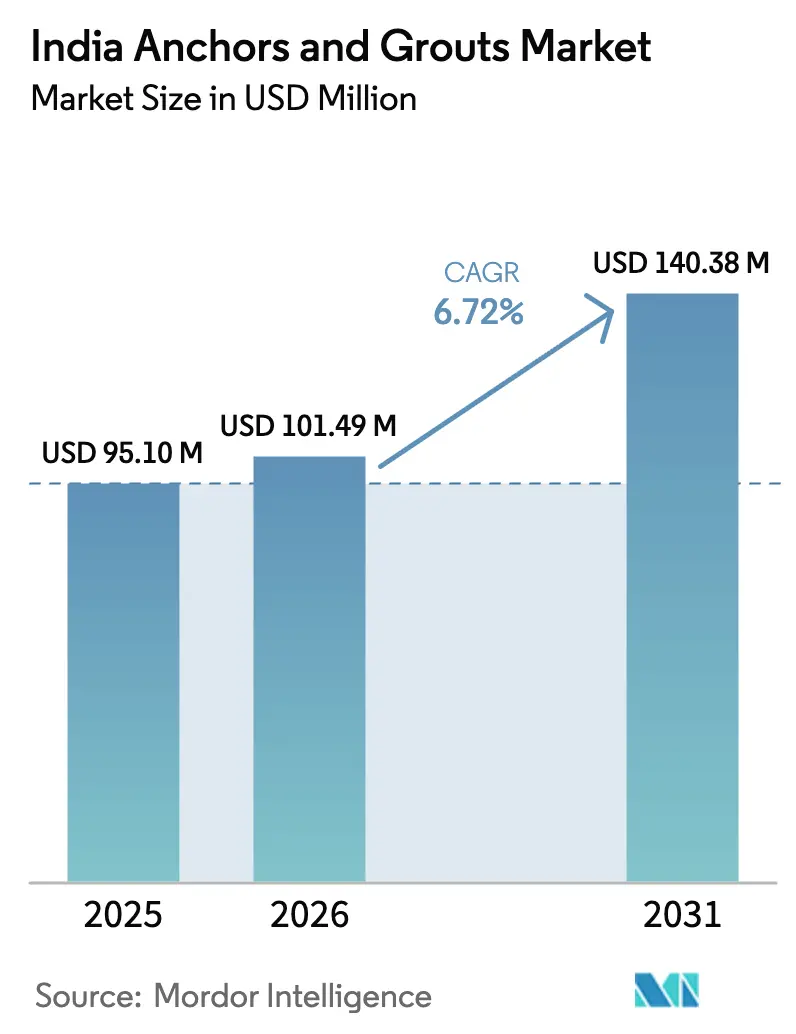

| Base Year Market Size (2025) | USD 95.10 Million |

| Market Size (2026) | USD 101.49 Million |

| Market Size (2031) | USD 140.38 Million |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

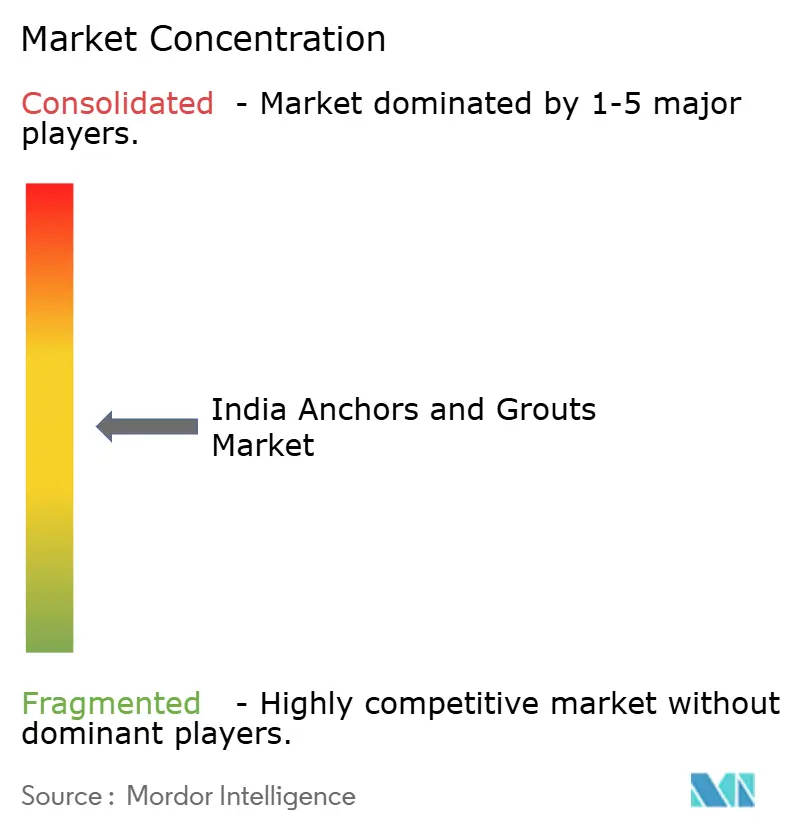

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Anchors And Grouts Market Analysis by Mordor Intelligence

The India Anchors and Grouts Market size in 2026 is estimated at USD 101.49 million, growing from 2025 value of USD 95.10 million with 2031 projections showing USD 140.38 million, growing at 6.72% CAGR over 2026-2031. Rapid infrastructure modernization, surge in high-rise construction, and government capital expenditure of INR 11.2 trillion for FY 2025-26 are propelling demand for advanced anchoring and grouting materials that can meet stringent load, seismic, and durability requirements[1]“Union Budget 2025-26,” indiabudget.gov.in. Resin-based systems, particularly epoxy formulations, continue to displace mechanical fixings in mega projects because they deliver superior bond strength, corrosion resistance, and a faster installation speed. At the same time, cementitious grouts remain relevant in cost-sensitive residential and light commercial jobs where fire resistance and familiarity sway contractor choice. Competitive dynamics are intensifying as multinational suppliers deepen R&D investment in low-VOC chemistries and automated mixing technologies, while domestic producers emphasize price, local service, and region-specific technical support. The interplay between premium specification demand and cost-focused procurement maintains a balanced price realization, sustaining healthy—but not excessive—margin potential across the value chain.

Key Report Takeaways

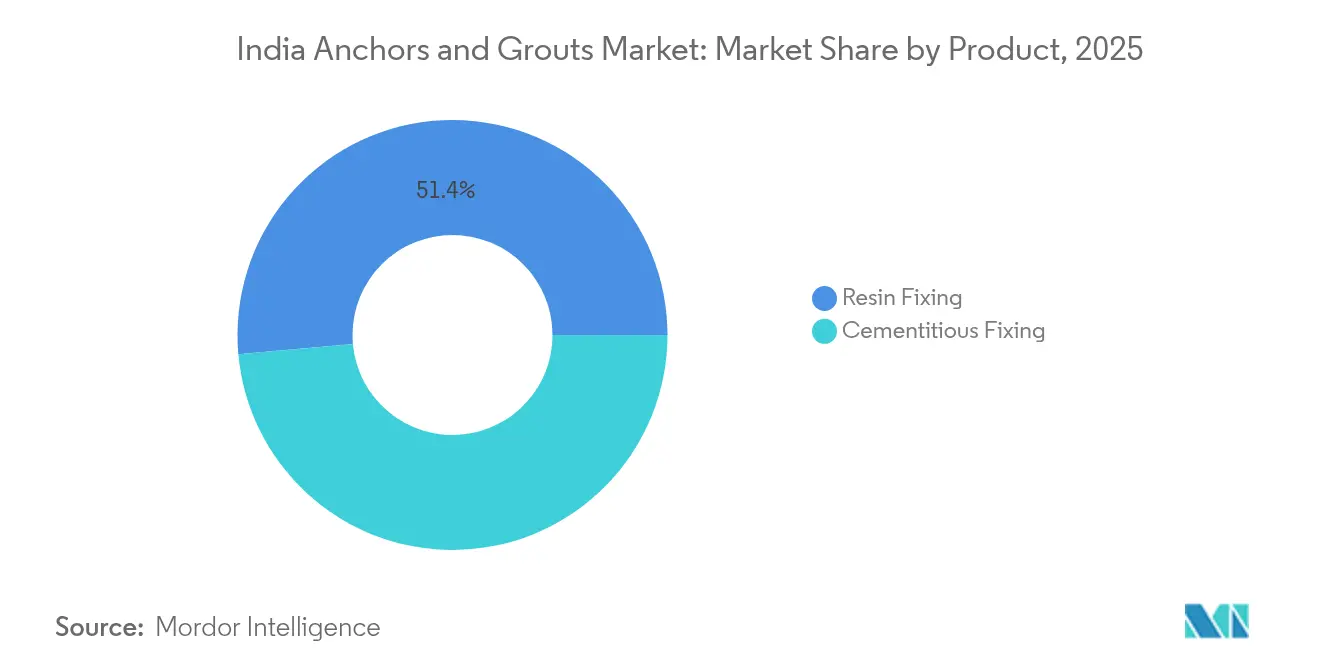

- By product category, resin fixing captured 51.43% of the India anchors and grouts market share in 2025 while advancing at an 7.89% CAGR through 2031.

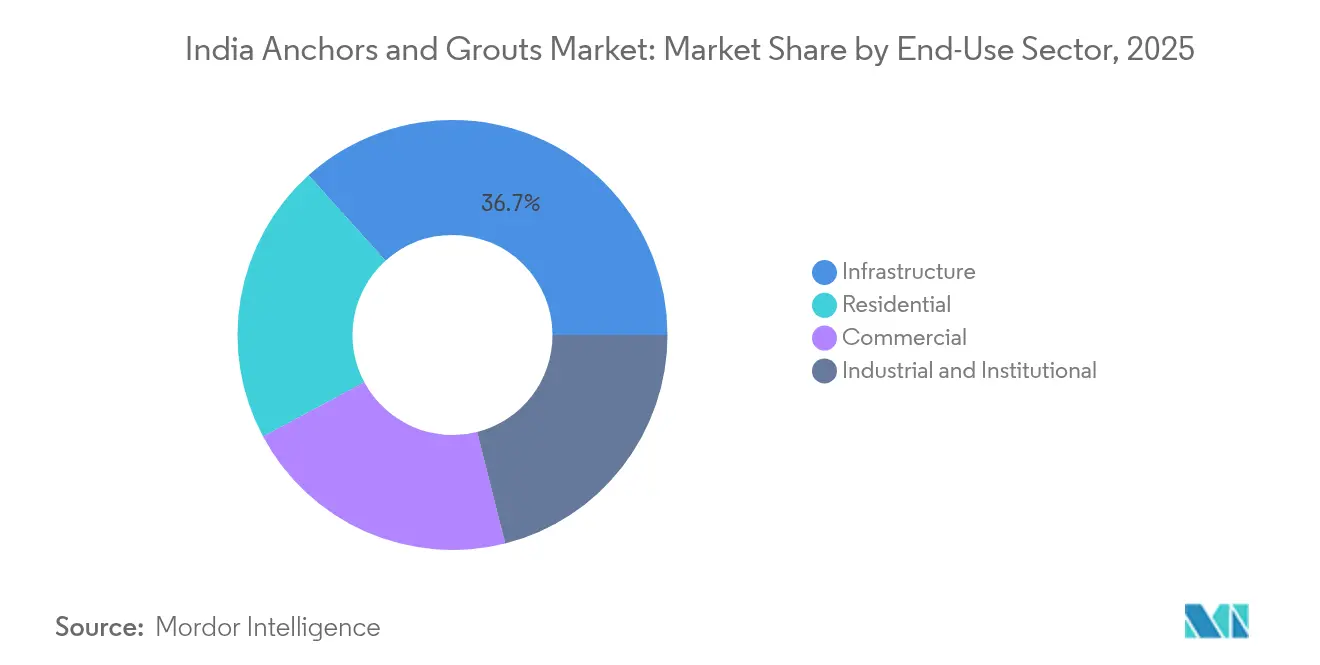

- By end-use, infrastructure accounted for 36.68% of the India anchors and grouts market size in 2025 and is projected to grow at a 7.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Anchors And Grouts Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mega-infrastructure investments across the nation | +2.1% | National, with concentration in Maharashtra, Gujarat, Tamil Nadu | Long term (≥ 4 years) |

| Commercial real-estate and industrial-corridor expansion | +1.8% | Urban clusters: Mumbai, Delhi NCR, Bangalore, Chennai, Pune | Medium term (2-4 years) |

| Increasing demand for seismic-resistant chemical materials | +1.4% | Seismic zones III-V: North India, Western Ghats, Northeast | Medium term (2-4 years) |

| Green, low-VOC resin formulations driving demand | +0.9% | Metro cities with GRIHA/LEED compliance requirements | Short term (≤ 2 years) |

| Automated digital injection-grouting systems on metro projects | +0.7% | Metro construction hubs: Mumbai, Delhi, Bangalore, Chennai, Hyderabad | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mega-infrastructure investments across the nation

India’s National Infrastructure Pipeline, Bharatmala highways program, and Sagarmala port initiative collectively translate into thousands of bridges, tunnels, and elevated corridors, each requiring chemically anchored rebar, rock bolts, and large-volume grout injections. Maharashtra alone has INR 8 lakh crore worth of works under execution, led by the Mumbai Trans Harbour Link and Mumbai–Nagpur expressway, generating sustained resin demand throughout their multi-year build cycles. Freight-dedicated rail corridors and the 508 km Mumbai–Ahmedabad high-speed rail demand anchors capable of resisting fatigue and thermal movement, opening a premium niche for high-modulus epoxies. Renewable energy parks, especially in Gujarat and Rajasthan, specify ground-screw anchors and microfine cement grouts that tolerate aggressive soil chemistry over 25-year lifespans[2]Ministry of New and Renewable Energy, “Renewable Park Allocations,” mnre.gov.in. Because these projects are milestone-based, procurement is evenly phased, creating predictable order visibility for suppliers until at least 2030.

Commercial real-estate and industrial-corridor expansion

Data-center capacity is set to more than double from 0.9 GW in 2023 to 2.0 GW by 2026, each facility demanding hundreds of chemical anchors for raised-floor systems, UPS skids, and cooling towers, and valuing vibration-damping grouts to protect mission-critical hardware. Government incentives worth INR 76,000 crore for semiconductor fabs have triggered anchor-intensive cleanroom construction in Gujarat, Tamil Nadu, and Andhra Pradesh, where epoxy formulations with very low chloride content and exacting creep performance command premiums up to 35% over commodity blends. Warehousing and logistics parks tied to the National Logistics Policy increasingly adopt automated storage and retrieval systems that impose dynamic point loads, making high-strength resin anchors mandatory for floor tracks. As hydrogen and green ammonia plants emerge, chemical-resistant anchoring systems that can withstand aggressive alkaline electrolyzer environments are becoming a specification norm, unlocking higher-margin niche volumes by 2028.

Increasing demand for seismic-resistant chemical materials

Nearly half of India’s landmass falls within seismic Zones III–V, prompting design consultants to specify anchors tested under cyclic loading in accordance with the revised IS 16700:2023 tall-building code. Recent tremors in the Himalayan and northeast belts have sharpened stakeholder focus on ductile performance, accelerating the shift from wedge anchors to injectable epoxies with high elongation at break. The Mumbai Metro Line 4A requires bored piles socketed into basalt rock using high-modulus thixotropic grout that resists vibration and water ingress. Precast-assembly growth also fuels chemical anchor demand because tolerances are tight and on-site welding is restricted in dense urban cores. Insurers now factor certified seismic anchoring into premium calculations, nudging developers toward tested systems that can document displacement capacity during earthquake events.

Green, low-VOC resin formulations driving demand

GRIHA and LEED teams now award credit for anchoring products with volatile organic compound content below 50 g/L, pushing manufacturers to reformulate with benzyl-alcohol-free hardeners. MAPEI’s “Zero Line” range offsets cradle-to-gate emissions and has been adopted in premium corporate campuses in Bengaluru and Hyderabad, commanding 15-25% higher pricing while shortening approvals due to EPD documentation. Public-sector procurement, including CPWD tenders, increasingly stipulates low-VOC certificates, giving early movers preferential bid scores. ]. Industrial by-product–based microfine grouts, such as Ambuja’s Alccofine, cut cement clinker content by up to 40% and deliver higher early strength, aligning with the government’s decarbonization roadmap for construction materials. Over the next two years, metro-station fit-outs and airport modernizations are expected to switch to such sustainable chemistries as part of ESG reporting commitments by project SPVs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material cost volatility (epoxy, fillers) | −1.6% | National, with higher impact in import-dependent regions | Short term (≤ 2 years) |

| Skilled-installer deficit causing anchor failures | −1.2% | Tier-2 and Tier-3 cities where training infrastructure is limited | Medium term (2-4 years) |

| Lengthy BIS approvals for new anchoring products | −0.8% | National, affecting time-to-market for suppliers across all regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-material cost volatility (epoxy, fillers)

Global BPA-based epoxy supply disruptions and anti-dumping actions have increased landed resin costs since late 2024, squeezing converter margins, especially for SME formulators reliant on spot imports. Domestic anti-dumping investigation outcomes remain uncertain, causing buyers to hedge inventory or sign variable-price contracts that discourage competitive bidding on fixed-rate infrastructure tenders. Cementitious grout producers also face volatility as bagged cement prices jumped INR 5-30 in April 2025, following strong housing demand. While tier-1 suppliers partly offset spikes in costs through raw-material hedging and backward integration, smaller firms with limited working capital struggle, which raises the risk of project delays and market consolidation over the next two seasons.

Skilled-installer deficit causing anchor failures

Fast-paced construction has outpaced the availability of trained applicators proficient in chemical anchor installation. Surveys by the Water Management & Plumbing Skill Council reveal that fewer than 20% of the 257,643 workers trained since 2021 have undergone specialty anchoring modules. Inadequate hole cleaning, incorrect cartridge dispensing, and premature load application have resulted in documented anchor pull-outs on flyover parapet panels in Rajasthan and facade brackets in tier-3 malls, eroding confidence among specifiers. Large contractors now require Original Equipment Manufacturer (OEM)-supervised demonstrations and digital torque logging for acceptance, but smaller builders often skip these steps due to cost. Without scalable training, recurring installation defects could hinder the growth of the India anchors and grouts market in fast-urbanizing regions until at least 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Resin Systems Lead Technical Evolution

Resin fixing contributed 51.43% to the India Anchors and Grouts market size in 2025 and is forecast to rise at an 7.89% CAGR, fueled by code-driven demand for higher load capacity in sea-facing bridges, metros, and clean-room installations. Within this segment, epoxy formulations account for more than three-quarters of the revenue due to their high bond strength-to-diameter ratio, while polyurethane variants gain share in thermal-cycling applications, such as steel roofs in coastal logistics parks. The segment’s value proposition is reinforced by lower rework costs and reduced anchorage lengths, which offset a price premium of 30-50% compared to mechanical anchors.

A second growth lever is the rapid adoption of dispenser guns with dynamic mixing nozzles and foil-pack formats, which cut cartridge waste by almost 20%. This appeals to contractors under pressure to maintain tight margins. Conversely, cementitious fixing remains the economical choice for fire-rated staircases, cable-tray supports, and non-critical façade anchors, where the ultimate capacity outweighs the initial cost. Despite a slower growth outlook, cementitious products secure volume dominance in tier-3 housing and public-sector buildings that specify conventional construction methods. Innovation in this sub-segment centers on geopolymer and microfine blends that deliver early-strength gains, a feature highly valued in precast yard turnarounds and rapid transit station retrofits.

By End-Use Sector: Infrastructure Dominance Reflects National Priorities

Infrastructure accounted for 36.68% of the India Anchors and Grouts market size in 2025 and is expected to expand at a 7.45% CAGR, in tandem with record investments in roads, rail, ports, and renewable energy. Tunnel projects, such as Zojila and Silkyara, require self-drilling anchor bolts and high-thixotropy grouts that can bond in fractured rock and sub-zero conditions, thereby extending product performance envelopes and ticket sizes. The metro ecosystem alone expects to consume 22,000 tons of chemical grout between 2025 and 2030 as five cities transition to deeper twin-bore alignments.

Commercial real estate exhibits a faster revenue CAGR but starts from a smaller base, so absolute volume growth tends to favor infrastructure. New-age office campuses, hospitality refurbishments, and premium retail fit-outs call for no-odor, fast-curing resins that enable overnight installations. Industrial and institutional demand aligns with the PLI-driven manufacturing push in electronics, pharma, and vehicles, where vibration-damping anchors protect precision machinery and clean-environment certifications limit solvent content. Residential uptake, although high in terms of units, lags in value as cost-sensitive developers opt for mechanical fixings, except for balconies, curtain walls, and solar mounting systems in mid-rise towers.

Geography Analysis

Western India spearheads consumption: Maharashtra, buoyed by INR 8 lakh crore infrastructure projects, accounts for nearly one-fifth of India's anchors and grouts market size, driven by landmark builds like the Mumbai Trans Harbour Link and Coastal Road Package IV. Gujarat ranks second as a semiconductor fab, and 30-GW renewable parks around Khavda demand anti-corrosion anchoring systems tailored to saline desert conditions. Tamil Nadu follows, with automotive hubs in Sriperumbudur and metro line extensions driving steady resin uptake across industrial and urban infrastructure sites.

Northern corridors, dominated by the Delhi–Mumbai Expressway, Ganga Expressway, and RRTS, witness the rapid adoption of hybrid anchors that simplify staging over wide-flange steel girders. Uttar Pradesh’s expressway boom alone could add 1.1 million linear meters of chemical anchoring through 2030, elevating the region’s share despite a lower starting base. Meanwhile, the north-eastern cluster—Arunachal’s Siang hydropower cascade and Assam’s inland-waterway jetties—creates demand spikes for microfine and marine-grade grouts, though logistics constraints and higher freight costs temper near-term volume.

Southern tech cities present high-value opportunity pockets. Bengaluru’s Whitefield data-center belt specifies fire-rated, smoke-tested epoxies, boosting per-project spend by 1.7 times compared to non-critical uses. Hyderabad’s Pharma City highlights the need for chemical-resistant anchors that are compatible with aggressive solvents. Eastern metros, such as Kolkata and Bhubaneswar, source cementitious blends locally, but the rising number of high-rise starts and elevated corridor retrofits indicates a progressive shift toward resin solutions as installers mature. Pan-India, demand remains closely linked to the health and execution efficiency of state budgets, with private-sector PPP activity supplementing central allocations in most high-ranking states.

Competitive Landscape

The India Anchors and Grouts market features a moderate level of concentration. Global manufacturers emphasize R&D-driven differentiation, leveraging global formulations, automated dispensing tools, and accredited installer networks. Price competition lingers in cementitious sub-segments, but total-installed-cost arguments favor premium resin systems where rework could cripple project timelines. Entry barriers remain moderate because BIS certification is process-oriented and access to raw materials is free trade in resin intermediates; yet, reputation and warranties keep repeat business clustered among incumbents.

India Anchors And Grouts Industry Leaders

Saint-Gobain

Sika AG

Thermax Limited

MYK LATICRETE India

Mapei S.p.A

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Walplast, a manufacturer of construction material in India, launched Homesure TileEx Cementitious Tile Grout. With this polymer-modified cement-based grout, the company aims to provide a durable and aesthetically pleasing alternative for jointing tiles.

- April 2024: Fischer India unveiled the FSU – Undercut anchor, tailored for high-load applications in concrete. It introduces enhanced installation efficiency with its self-undercutting capability.

India Anchors And Grouts Market Report Scope

Commercial, Industrial and Institutional, Infrastructure, Residential are covered as segments by End Use Sector. Cementitious Fixing, Resin Fixing are covered as segments by Sub Product.| Cementitious Fixing | |

| Resin Fixing | Epoxy-based |

| Polyurethane-based | |

| Other Types |

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Residential |

| By Product | Cementitious Fixing | |

| Resin Fixing | Epoxy-based | |

| Polyurethane-based | ||

| Other Types | ||

| By End-Use Sector | Commercial | |

| Industrial and Institutional | ||

| Infrastructure | ||

| Residential | ||

Market Definition

- END-USE SECTOR - Anchors and grouts consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of anchors and grouts such as cementitious fixing, resin fixing polyurethane, resin fixing epoxy, and other types are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms