Market Overview

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 4.91 Trillion |

| Market Size (2030) | USD 6.04 Trillion |

| Growth Rate (2025 - 2030) | 4.23% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hospitality Real Estate Sector Market Analysis by Mordor Intelligence

The hospitality real estate sector market was valued at USD 4.91 trillion in 2025; it is projected to reach USD 6.04 trillion by 2030, implying a 4.23% CAGR during the 2025-2030 period. Solid recovery in international arrivals, the return of corporate events, and steady capital inflows into hotel assets underpin this expansion. Inbound investment remains concentrated in Europe and the Middle East, where gateway cities capture significant cross-border capital seeking stable yields. Urban properties lead RevPAR growth because business travel rebounded faster than anticipated, while resorts benefit from the rise of experiential and wellness-driven tourism. Institutional investors are consolidating portfolios through selective acquisitions, adopting AI-driven revenue systems that lift room revenue by up to 10%. Cost inflation and rising construction expenses, however, continue to squeeze margins and temper the growth trajectory of the hospitality real estate sector market.

Key Report Takeaways

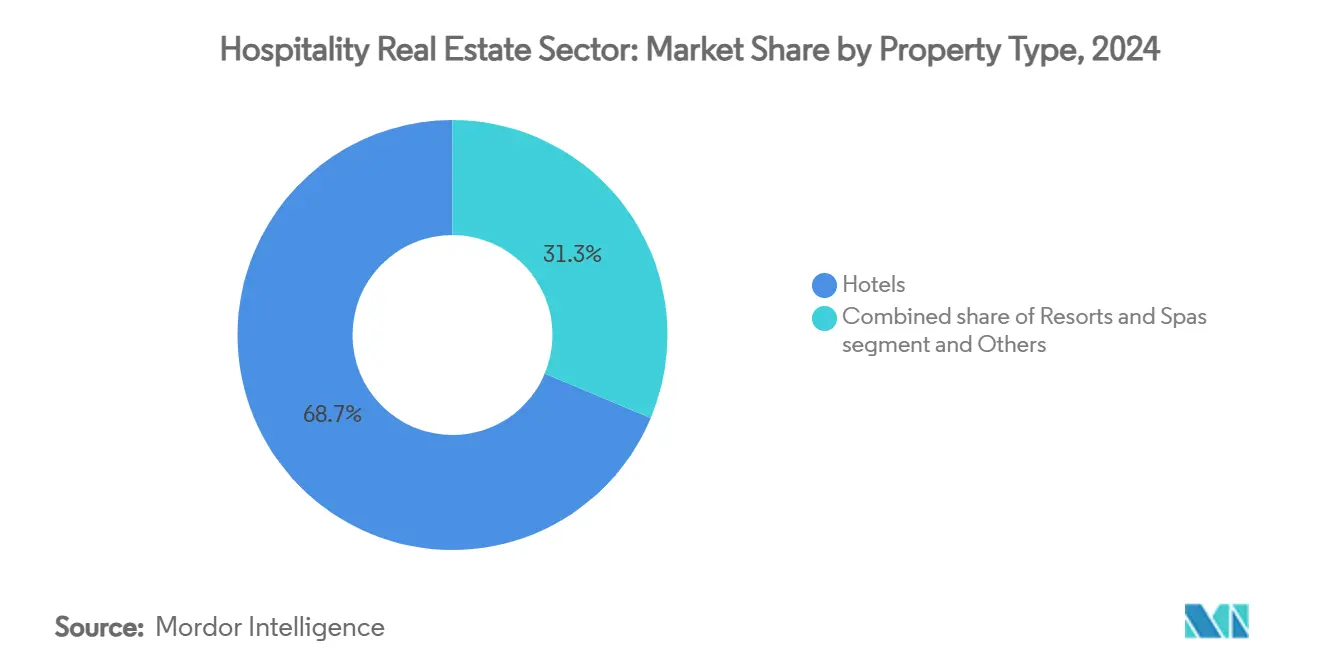

- By property type, hotels held 68.7% of the hospitality real estate sector market share in 2024. The hospitality real estate sector market for resorts & spas is forecast to register a 4.94% CAGR through 2030.

- By type, chain hotels commanded a 61.2% share of the hospitality real estate sector market size in 2024. The hospitality real estate sector market for independent hotels is expected to advance at a 5.21% CAGR between 2025-2030.

- By asset class, midscale properties accounted for 42.3% share of the hospitality real estate sector market size in 2024. The hospitality real estate sector market for luxury assets is projected to grow at 5.35% CAGR during 2025-2030.

- By geography, Asia-Pacific dominated with 38.8% of the hospitality real estate sector market revenue share in 2024. The hospitality real estate sector market for the Middle East & Africa region is set to post the fastest 6.14% CAGR to 2030.

Global Hospitality Real Estate Sector Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Significant rebound in global tourism and corporate travel activity | +1.2% | Global, with strongest impact in Europe, Middle East, and Asia-Pacific | Medium term (2-4 years) |

| Rising investments from REITs, private equity, and institutional investors | +0.9% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Increase in cross-border hotel transactions across major gateway cities | +0.8% | North America, Europe, and Asia-Pacific gateway cities | Short term (≤ 2 years) |

| Strong performance metrics like RevPAR and ADR in urban and leisure markets | +0.6% | Global, with urban markets outperforming | Medium term (2-4 years) |

| Rapid adoption of smart technologies in hotel operations and guest experiences | +0.4% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Shift in capital allocation favoring hospitality over traditional CRE sectors | +0.3% | Global, particularly in North America and Europe | Medium term (2-4 years) |

Source: Mordor Intelligence

Significant Rebound in Global Tourism and Corporate Travel Activity

Global tourism surpassed pre-pandemic levels in 2024, with 1.4 billion international arrivals and USD 1.6 trillion in receipts, lifting demand across every major lodging segment[1]Zurab Pololikashvili, “Tourism Barometer Q1-2025,” United Nations World Tourism Organization, unwto.org. Corporate travel spending is recovering in tandem, aided by postponed conferences and an uptick in blended business-leisure trips. China’s vast domestic market, together with resurgent outbound travel, is expected to anchor regional performance over the forecast horizon[2]Lindsey Upton, “Global BTI Outlook 2025,” Global Business Travel Association, gbta.org. Extended-stay formats gain traction because longer work trips persist amid flexible office policies, bolstering occupancy in select-service properties. The sustained rebound serves as the single largest volume driver for the hospitality real estate sector market.

Increase in Cross-Border Hotel Transactions Across Major Gateway Cities

Cross-border deal volume returned swiftly in 2024 as investors pursued stable income streams in globally recognized destinations. The EMEA region drew 74% of inbound capital, led by U.S. funds targeting London, Paris, and Madrid for currency and diversification advantages. Asia-Pacific recovered to 90% of 2019 investment levels, with Japan absorbing roughly half of regional inflows on the back of consistent tourism policy and yield visibility. Full-service hotels dominated 87% of transactions because they deliver multiple revenue sources and flexible asset-management levers. Anticipated interest-rate moderation in 2025 should accelerate deal velocity, lifting the broader hospitality real estate sector market.

Strong Performance Metrics Like RevPAR and ADR in Urban and Leisure Markets

Urban hotels delivered RevPAR gains of 2.8% for 2025, surpassing leisure resorts as group events and corporate meetings filled weekday calendars. Host Hotels & Resorts reported 7.0% comparable RevPAR growth in Q1 2025, confirming the pricing momentum in primary cities. High-tier brands preserved tariff leadership, signaling effective revenue-management discipline even as alternative lodging expanded. Urban RevPAR is projected to stand 16.6% above 2019 by year-end 2025, supporting valuations and reinforcing investor appetite for well-located assets. This revenue resilience strengthens the growth profile of the hospitality real estate sector market.

Rising Investments from REITs, Private Equity, and Institutional Investors

In 2024, publicly listed hotel REITs actively pursued consolidation, investing USD 1.5 billion in acquisitions. Apple Hospitality REIT showcased the benefits of operational discipline, boosting its 2024 net income by 20.6%. Meanwhile, private equity groups, buoyed by easing rate risks, are shifting their focus. They're increasingly eyeing upper-upscale and luxury assets, drawn by their potential for significant total returns. This strategic pivot from private equity, backed by institutional capital, ensures a steady influx of liquidity, bolstering the upward trajectory of the hospitality real estate market.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating operational costs impacting hotel profitability | -0.7% | Global, with acute impact in North America and Europe | Short term (≤ 2 years) |

| Growing competition from alternative lodging platforms and short-term rentals | -0.6% | Global, concentrated in urban and leisure markets | Long term (≥ 4 years) |

| High construction and renovation costs limiting new supply | -0.5% | Global, particularly in developed markets | Medium term (2-4 years) |

| Macroeconomic and geopolitical risks affecting investor sentiment | -0.4% | Global, with regional variations | Short term (≤ 2 years) |

Source: Mordor Intelligence

Escalating Operational Costs Impacting Hotel Profitability

Labor expenses, utilities, and food costs are rising faster than room revenue, applying margin pressure across most operating statements. Midscale properties feel the squeeze most acutely because rate elasticity constrains their ability to pass through higher expenses. Operators, therefore, accelerate the deployment of automation, energy-management tools, and lean service models to preserve profitability. Margin erosion stimulates consolidation, as smaller owners lacking scale often choose to divest. Persistent cost escalation thus tempers near-term upside in the hospitality real estate sector market.

Growing Competition from Alternative Lodging Platforms and Short-Term Rentals

Short-term rental demand expanded 6.0% in 2024, dwarfing the 0.1% uptick in hotel demand. Platforms such as Airbnb erode hotel profits, especially in price-sensitive urban corridors, by widening lodging supply and undercutting ADRs[3]William Thompson, “Hotel Transaction Tracker 2025,” U.S. Bureau of Labor Statistics, bls.gov. Travelers increasingly value localized experiences that traditional hotels struggle to replicate at scale, compelling brands to re-engineer service delivery around authenticity and personalization. While upscale and luxury chains retain differentiation, budget and midscale operators face intensified competitive pressure. This dynamic moderates the pace at which the hospitality real estate sector market expands.

Segment Analysis

By Property Type: Hotels Retain Scale Leadership, Resorts Accelerate

Hotels dominated the hospitality real estate sector, contributing a substantial 68.7% market share. Their dominance is bolstered by globally recognized brands, extensive distribution networks, and a balanced demand mix that mitigates cyclical shocks. Conversion activities, flag upgrades, and AI-driven revenue systems further support steady performance and stable cash flows. In contrast, resorts and spas, while generating a significant share, are projected to grow at a 4.94% CAGR through 2030. A rising preference for health-centric vacations and experiential stays fuels this growth. Operators are capitalizing on this trend, enhancing average daily rates (ADRs) and extending guest stays through wellness amenities, culinary tourism, and curated activities. This strategy not only boosts revenue per available unit but also uplifts the entire hospitality real estate sector.

Serviced apartments and boutique inns, as complementary formats, cater to extended-stay professionals and authenticity-seeking tourists, respectively. Their modular designs and compact footprints often yield superior operating margins while addressing the unique needs of travelers. An increasing focus on sustainability and local sourcing amplifies the allure of boutiques for eco-conscious visitors. Consequently, investors find a balanced mix of yield stability and growth potential in the hospitality real estate sector by diversifying their portfolios across widely appealing hotels and high-growth resort assets.

Note: Segment shares of all individual segments available upon report purchase

By Type: Chain Consistency Versus Independent Differentiation

Chain hotels raked in a staggering revenue, commanding a dominant 61.2% share of the hospitality real estate sector. Corporate accounts and loyalty programs guarantee a steady stream of room bookings. Meanwhile, centralized procurement and advanced technology help in reducing operating costs. Brand mandates play a pivotal role in maintaining quality consistency, a key factor in attracting repeat visits from cautious travelers. On the other hand, independent hotels project a robust 5.21% CAGR from 2025 to 2030, outpacing their chain counterparts. This surge is driven by consumers' growing appetite for local experiences and unique design stories. Digital platforms are broadening the horizons for independents, allowing them to tap into global markets. Furthermore, asset-light management contracts grant them access to advanced distribution channels without compromising their independence. By leveraging data-driven revenue strategies and emphasizing genuine storytelling, many independents are carving out a larger slice of the hospitality real estate pie.

The dynamic interplay between chain and independent hotels fosters a vibrant, competitive landscape. While chains hone their service efficiencies to safeguard margins amidst inflationary pressures, independents are boldly pushing the boundaries of creativity and experience. Investors find themselves at a crossroads, weighing the reliability of cash flows from established brands against the potential rewards of unique, tailored offerings. This delicate balance not only enriches the diversity of offerings in the hospitality real estate sector but also ensures continued engagement from travelers.

By Asset Class: Luxury Drives Premium Growth, Midscale Commands Volume

Midscale lodging generated the majority of revenue in 2024, implying a 42.3% slice of the hospitality real estate sector market size. Its appeal lies in balanced amenities and approachable rates that resonate with families, small businesses, and tour groups. Operators emphasize functional design, limited food services, and efficient staffing models to protect profitability amid cost inflation. Luxury assets, while smaller in footprint, are set to expand at a robust 5.35% CAGR through 2030 thanks to steady spend by high-net-worth guests and renewed interest in signature experiences. Upper-tier brands wield meaningful pricing power, often achieving RevPAR premiums of 30% over upscale peers, reinforcing their strategic importance to diversified portfolios within the hospitality real estate sector market.

Affordable segments face mounting substitution risk from short-term rentals that mimic local authenticity at comparable price points. Operators respond by modernizing guest rooms, integrating self-service technology, and nurturing partnerships with last-mile platforms to elevate convenience. Luxury developers, conversely, incorporate branded residences, medical wellness, and high-touch concierge services to deepen ancillary revenue channels. Asset-class specialization thus shapes capital-allocation decisions and ultimately broadens the value proposition of the hospitality real estate sector market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific held 38.8% of global revenue in 2024, reflecting its status as the principal growth engine for the hospitality real estate sector market. Japan alone captured nearly 50% of regional cross-border flows, buoyed by investor trust in its legal framework and inbound visitor momentum. China’s domestic tourism, enhanced by large-scale rail and airport expansions, continues to swell occupancy across tier-one and emerging provincial cities. India follows a comparable trajectory as rising middle-class incomes stimulate domestic weekend travel, expanding the audience for branded upper-midscale hotels. Investors target value-add plays that involve rebranding, capex upgrades, and ESG retrofits to unlock yield premiums in these high-growth settings.

The Middle East & Africa are primed for the fastest 6.14% CAGR between 2025 and 2030. Saudi Arabia’s Vision 2030 funnels unprecedented public capital into tourism districts. The UAE cements its gateway-hub reputation through large-event calendars that sustain year-round demand and bolster ADRs. RevPAR in the region now stands 28% above 2019, a performance that attracts global operators eager to expand flag footprints. Government-backed finance vehicles and favorable free-zone regulations further reduce entry barriers, encouraging fresh supply and intensifying competition in the hospitality real estate sector.

North America and Europe maintain heavyweights’ status through their extensive infrastructure, deep talent pools, and diverse leisure and corporate demand generators. London reclaimed the top spot for hotel investment in 2024, while New York and Washington, D.C. show resilient group-booking pipelines driven by trade conventions and pro-tourism policies. European hotel cap rates compressed amid ample liquidity, prompting many investors to pursue refurbishment and ESG upgrades as routes to incremental yield. North American REITs deploy capital toward urban luxury repositioning and destination resorts, aiming for double-digit unlevered IRRs. Together, these mature regions provide stability that balances the high-growth allure of emerging markets, creating a complementary global footprint for participants in the hospitality real estate sector market.

Competitive Landscape

The hospitality real estate sector market reveals a moderate concentration pattern. The top five REITs and large private equity platforms cumulatively own the majority of premium urban properties, affording them meaningful scale in procurement, branding, and distribution. Host Hotels & Resorts controls 81 hotels with 43,400 rooms and maintains investment-grade credit, enabling low-cost capital access to fund growth. Apple Hospitality REIT deepened portfolio quality through selective acquisitions while exiting non-core assets, illustrating prudent capital recycling. Ryman Hospitality Properties focuses on group-oriented resorts that secure bookings and thereby dampen earnings volatility.

Rising tech adoption adds a new axis of competition. AI chatbots trim direct-booking friction and raise conversion rates by 25%, while intelligent pricing engines lift total room revenue by up to 10%. Energy-optimization platforms reduce utility spend and assist owners in meeting ESG mandates. Independent operators exploit cloud-based property-management systems to match the digital sophistication of chains without surrendering design autonomy. The surge of alternative lodging platforms keeps ADR discipline intact, pressuring conventional hotels to elevate experiential elements and loyalty benefits. Market participants that blend high-touch service with data-powered efficiency stand best positioned to capture incremental gains in the hospitality real estate sector.

White-space opportunities multiply in under-supplied geographies such as secondary Saudi cities, northern Indian tourist circuits, and select African coastal hubs where new international-standard inventory remains sparse. Flexible-stay concepts, hybrid coworking-hotel spaces, and branded residences offer further avenues to diversify income and extend customer lifetime value. Competitive success will hinge on risk-adjusted location selection, brand clarity, and technology investments that future-proof assets against evolving traveler demands. These strategic imperatives collectively reinforce the resilience of the hospitality real estate sector market.

Hospitality Real Estate Sector Industry Leaders

-

Marriott International Inc.

-

Hilton Worldwide Holdings Inc.

-

InterContinental Hotels Group PLC

-

Accor S.A.

-

Wyndham Hotels & Resorts Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Ryman Hospitality Properties acquired JW Marriott Phoenix Desert Ridge Resort for USD 865 million at a 12.7x adjusted EBITDA are multiple.

- February 2025: Host Hotels & Resorts completed USD 1.5 billion of 2024 acquisitions including a dual-hotel Nashville complex at a 7.4% cap rate.

- January 2025: Apple Hospitality REIT closed two acquisitions for USD 117 million and divested six non-core hotels for USD 63 million.

- May 2024: Henderson Park bought the Arizona Biltmore for USD 705 million, underlining persistent investor appetite for iconic resort assets.

Global Hospitality Real Estate Sector Report Scope

In real estate, hospitality consists of a wide range of product types, including hotels, travel centers, water parks, amusement facilities, golf courses, cruise ships, and restaurants.

The Hospitality Real Estate Market is segmented by property type (hotels and accommodations, spas and resorts, and other themed properties) and geography (Asia-Pacific, North America, Europe, Latin America, Middle-East, and Africa). The report offers market size and forecasts for the hospitality real estate sector in value (USD) for all the above segments.

The report provides a comprehensive background analysis of the hospitality real estate sector. It also covers the current market trends, market dynamics, technological updates, and detailed information on various segments and the industry’s competitive landscape. Additionally, the COVID-19 impact is also incorporated and considered during the study.

| By Property Type | Hotels | ||

| Resorts & Spas | |||

| Others (Serviced Apartments, boutique inns, etc) | |||

| By Type | Chain Hotels | ||

| Independent Hotels | |||

| By Asset Class | Affordable/Budget | ||

| Midscale | |||

| Luxury | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Middle East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| Rest of Middle East and Africa | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

By Property Type

| Hotels |

| Resorts & Spas |

| Others (Serviced Apartments, boutique inns, etc) |

By Type

| Chain Hotels |

| Independent Hotels |

By Asset Class

| Affordable/Budget |

| Midscale |

| Luxury |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East and Africa | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the hospitality real estate sector market?

The hospitality real estate sector market size reached USD 4.91 trillion in 2025 and is expected to hit USD 6.04 trillion by 2030.

Which region leads the hospitality real estate sector market?

Asia-Pacific leads with 38.8% global revenue share in 2024, driven by robust investment and domestic tourism growth.

What property type holds the largest hospitality real estate sector market share?

Hotels dominate with 68.7% share, supported by broad brand distribution and strong corporate demand pipelines.

Which asset class is projected to grow fastest through 2030?

Luxury hotels should expand at a 5.35% CAGR because affluent travelers continue to prioritize premium experiences.

How are alternative lodging platforms affecting traditional hotels?

Short-term rentals captured demand growth of 6.0% versus 0.1% for hotels in 2024, pressuring ADRs and prompting hotels to enhance technology and service personalization to compete effectively.

What technological tools are boosting hotel revenue performance?

AI-driven revenue management systems raise room revenue by 6-10%, and chatbots increase direct bookings by 25%, improving profitability for operators who adopt these solutions.

Page last updated on: July 7, 2025