IT & Telecom Discrete Semiconductor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

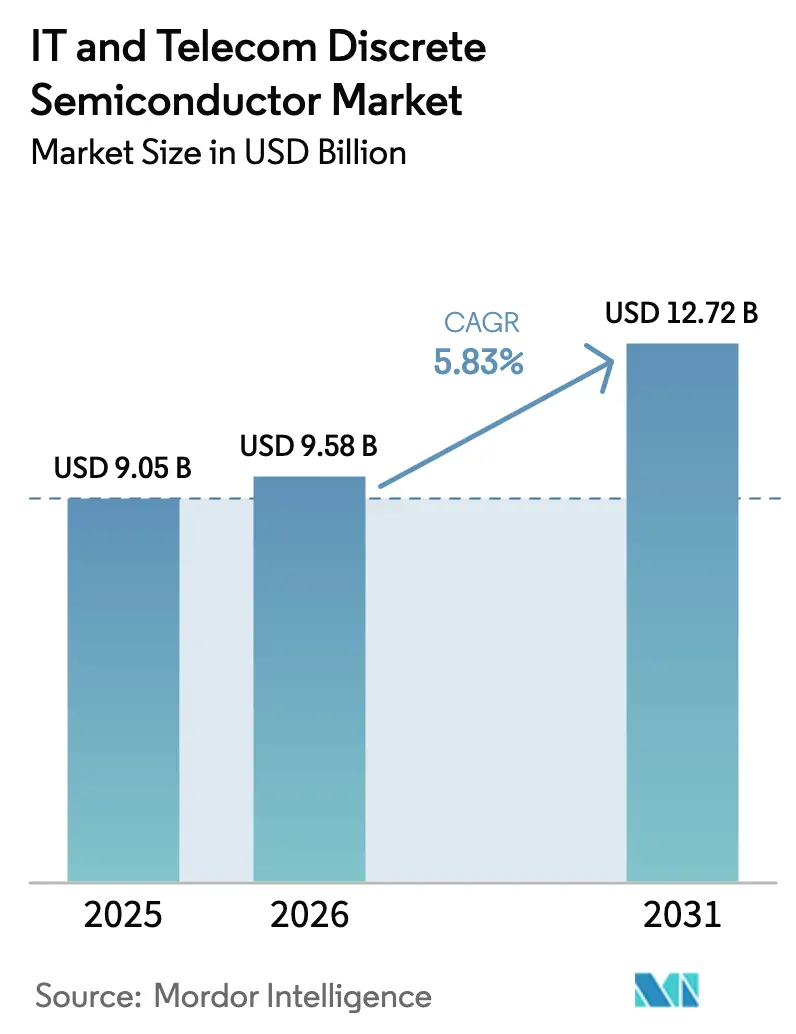

| Market Size (2026) | USD 9.58 Billion |

| Market Size (2031) | USD 12.72 Billion |

| Growth Rate (2026 - 2031) | 5.83% CAGR |

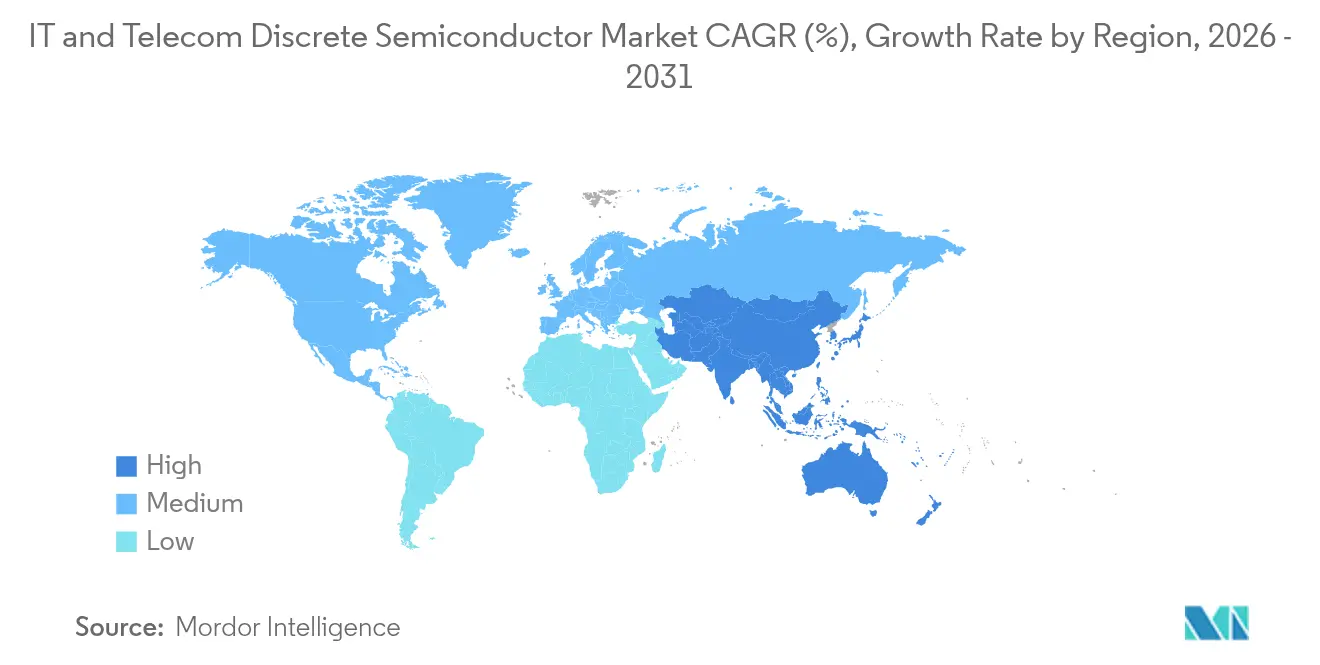

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IT & Telecom Discrete Semiconductor Market Analysis by Mordor Intelligence

The IT and Telecom Discrete Semiconductor market size is expected to grow from USD 9.05 billion in 2025 to USD 9.58 billion in 2026 and is forecast to reach USD 12.72 billion by 2031 at 5.83% CAGR over 2026-2031. A resilient demand base continued 5G network densification, and sustained capital spending on hyperscale data-centre power upgrades underpinned this outlook despite supply-chain volatility. Wide-bandgap adoption lifted average selling prices and created new addressable opportunities in high-voltage infrastructure, while mounting energy-efficiency mandates influenced purchasing criteria toward SiC and GaN devices. Localized manufacturing strategies in Asia-Pacific buffered geopolitical export controls and helped companies shorten cycle times. Simultaneously, packaging advances such as chip-scale and wafer-level options supported ultra-compact RF front ends for smartphones and small-cell radios. Together, these forces established a balanced growth path for the IT and Telecom Discrete Semiconductor market.

Key Report Takeaways

- By product type, power transistors led with 60.80% of the IT and Telecom Discrete Semiconductor market share in 2025 and posted a 9.65% CAGR outlook to 2031.

- By material, silicon held 81.90% revenue share in 2025, whereas SiC is projected to expand at a 23.1% CAGR through 2031.

- By power rating, medium-voltage devices accounted for 45.90% of the IT and Telecom Discrete Semiconductor market size in 2025, while high-voltage parts are forecast to grow 10.8% annually to 2031.

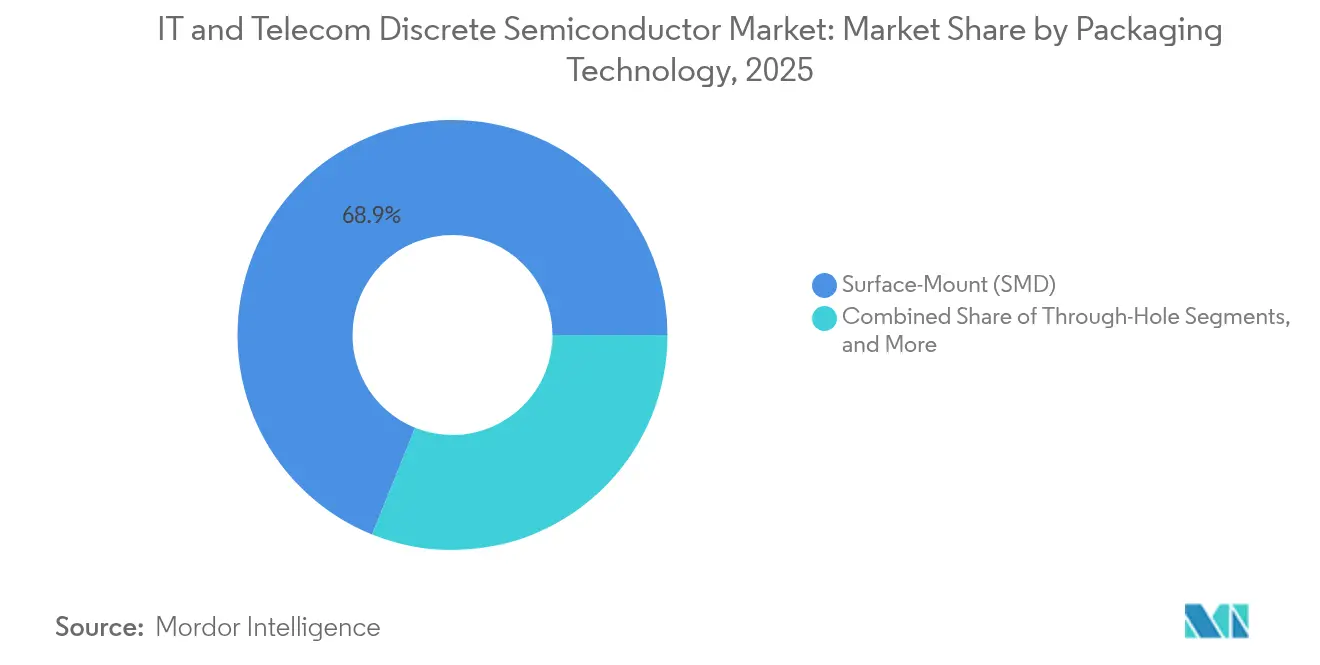

- By packaging technology, surface-mount dominated with 68.90% share in 2025; chip-scale and wafer-level options are poised to record a 12.7% CAGR.

- By application, smartphones commanded 37.90% share of the IT and Telecom Discrete Semiconductor market size in 2025; telecom infrastructure equipment is advancing at 10.4% CAGR to 2031.

- By geography, Asia-Pacific captured 35.90% revenue in 2025; the same geography is expected to post the fastest 9.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global IT & Telecom Discrete Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G base-station rollouts accelerating high-voltage GaN and SiC device adoption | +1.8% | Asia-Pacific with spillover to North America and Europe | Medium term (2-4 years) |

| Hyperscale data-centre expansion requiring low-loss power MOSFETs | +1.2% | North America with a secondary impact in Europe and Asia-Pacific | Short term (≤ 2 years) |

| Edge-AI and IoT proliferation driving demand for ultra-low-leakage small-signal diodes | +0.9% | Europe and North America are expanding into the Asia-Pacific region | Medium term (2-4 years) |

| Rapid fibre-optic upgrades are boosting high-speed PIN and avalanche photodiodes | +0.7% | Global with a focus on North America and Asia-Pacific | Medium term (2-4 years) |

| Telecom operators’ net-zero targets lifting SiC Schottky rectifier deployment | +0.6% | Middle East and Africa with global extension | Long term (≥ 4 years) |

| Miniaturization of smartphone RF front ends spurring RF discrete switch volumes | +0.5% | Asia-Pacific, notably China, with global implications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

5G Base-Station Rollouts Accelerating High-Voltage GaN and SiC Device Adoption in Asia

Operators scaling out massive MIMO radios reported power budgets roughly double those of legacy 4G units, a shift that moved procurement toward GaN-on-SiC HEMT power amplifiers capable of 50 W saturated output while sustaining 50 V rails.[1]Guerrilla RF, “GRF0020D and GRF0030D GaN-on-SiC HEMT Power Amplifiers Press Release,” guerrilla-rf.com Regional makers invested in local foundry lines to offset export controls, quickening lead-time advantages for domestic customers. Multichip GaN front-end modules also replaced discrete LDMOS stages, reducing footprint and simplifying thermal spreaders in densely packed macro radios. Network equipment vendors translated these device-level gains into total cost of ownership savings by trimming cabinet cooling loads. As governments linked spectrum licences to energy targets, carriers locked in volume commitments for SiC rectifiers and GaN drivers to keep carbon metrics on plan.

Hyperscale Data-Centre Expansion Requiring Low-Loss Power MOSFETs in North America

AI training clusters were forecast to lift global data-centre electricity demand past 1,000 TWh in 2026, prompting operators to migrate from 12 V to 48 V and 800 V bus architectures. New server backplanes featuring T10 PowerTrench MOSFETs trimmed switching losses by 50% and conduction losses by 30%, unlocking annual site savings near 10 TWh. The Open Rack V3 specification set an aggressive 97.5% conversion efficiency floor that mainstreamed SiC MOSFET packaging with top-side cooling plates. Suppliers responded by offering turnkey power-stage reference designs that bundled gate drivers, EMI filters, and digital telemetry rather than discrete dies alone. These module-level solutions accelerated rack qualification cycles and tightened defensibility for vendors with vertical integration across substrate, die, and packaging.

Edge-AI and IoT Proliferation Driving Demand for Ultra-Low-Leakage Small-Signal Diodes in Europe

Strict energy-design regulations pushed European OEMs to specify leakage below 1 nA at 25 °C for coin-cell-powered sensor nodes Mouser. Device makers extended diode guard-ring structures and leveraged trench isolation to meet those thresholds without sacrificing reverse-voltage ratings. Simultaneously, hardware-root-of-trust solutions integrated discrete TPMs that employed dedicated transistors and zener references to protect secure boot keys. Harsh-environment installations, from smart grids to predictive-maintenance systems, require coated packages and enhanced avalanche capability to survive transients. Component vendors capturing these sockets emphasized dual-sourcing policies to mitigate customs delays and ensure field-replaceable continuity across a projected 15-year equipment life.

Rapid Fiber-Optic Network Upgrades Fueling High-Speed PIN and Avalanche Photodiode Consumption

Worldwide adoption of 400 G and 800 G coherent optics shifted demand toward 25 GHz-bandwidth photodiodes with <0.5 pA/√Hz noise density. Stand-alone PIN and APD dies were frequently co-packaged with transimpedance amplifiers, shrinking receiver cards, and raising assembly yield. Cost-optimised variants targeted fibre-to-the-home rollouts, where operating temperatures could exceed 85 °C without active cooling. Specialized vendors gained share from large monolithic suppliers by tailoring bond pad geometry for next-generation silicon-photonic engines. The same supply base expanded into data-centre artificial-intelligence clusters, positioning high-speed photodiodes as a bridge between pluggable optics today and co-packaged optics deployments after 2027.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integrated power modules replacing stand-alone discrete in 5G macro radios | -0.6% | Global with a focus on Asia-Pacific and North America | Medium term (2-4 years) |

| Supply-chain volatility for SiC substrates is limiting device availability | -0.4% | Global with notable impact in Europe and North America | Short term (≤ 2 years) |

| Rising R&D costs to meet telecom-grade reliability standards | -0.3% | Global | Long term (≥ 4 years) |

| Stringent export controls on advanced GaN devices constrain market access | -0.2% | China with chain-reaction effects worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integrated Power Modules Replacing Stand-Alone Discrete in 5G Macro Radios

Radio OEMs condensed multi-chip drivers, FETs, and protection networks into single transfer-molded modules that delivered 10% higher output at 200 W, lower loss. The approach cut board footprint by up to 40 % and eased thermal interface attachment, but it displaced discrete MOSFET and IGBT sockets traditionally served by commodity suppliers. Without comparable packaging capabilities, pure-play discrete vendors risked revenue erosion as system engineers gravitated toward plug-and-play power stages pre-certified for electromagnetic compliance. Adoption accelerated in regions with dense 5G macro deployments, compressing the available window for standalone device differentiation.

Supply-Chain Volatility for SiC Substrates Limiting High-Power Device Availability

Demand for 6-inch and emerging 8-inch SiC wafers outpaced capacity, forcing allocation programmes that favoured incumbents and delayed design wins for new entrants. Lead-time uncertainty encouraged some OEMs to re-specify advanced silicon super junction MOSFETs in medium-voltage slots, marginally tempering SiC unit growth. Substrate producers announced multibillion-dollar expansions, yet the 18-24 month equipment ramp meant tight conditions persisted through 2026. European and North American device houses without captive crystal operations bore higher wafer costs, pressuring gross margins until adequate internal boule capacity came online.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Power Transistors, Anchor Market Leadership

Power transistors captured 60.80% revenue in 2025, and the IT and Telecom Discrete Semiconductor market size for this product family is slated to climb at 9.65% CAGR to 2031. Momentum stemmed from MOSFET replacements in 48 V server converters and IGBT penetration into high-power telecom rectifiers. Infineon’s OptiMOS 6 80 V series, tuned for AI servers, extended conduction-loss leadership in the medium-voltage window. RF and microwave discrete formed a smaller but faster block as 5G macro and small-cell shipments scaled. Guerrilla RF’s 50 W GaN-on-SiC dice illustrated the pivot toward wide-bandgap parts for saturated power gains in high-frequency infrastructure.

The broader mix of small-signal devices retained relevance for IoT sensor-nodes, where leakage defined battery life targets. Thyristors preserved niche share in surge-protection circuits, with SLKOR Micro reporting new design activity in industrial Ethernet gateways. SiC rectifier attach rates rose inside network-power shelves, allowing operators to downsize heatsinks. Collectively, heightened specialization shifted pricing power toward vendors offering application-tuned discrete portfolios rather than broad commodity catalogs, supporting value capture as unit demand secularly expanded.

By Material: Silicon Carbide Disrupts Traditional Hierarchies

Silicon retained 81.90% share in 2025 as the foundation of cost-efficient low- and medium-voltage devices, yet the IT and Telecom Discrete Semiconductor market witnessed SiC accelerating at 23.1% CAGR. Infineon shipped the first 200 mm SiC wafers in early 2025, halving the die cost per ampere and activating new high-voltage design-ins. GaN, meanwhile, secured footholds in RF PAs and server power factor-correction stages after the company unveiled 300 mm GaN processes capable of 2.3 times higher die per wafer than 200 mm lines.

Second-tier materials such as gallium oxide remained developmental, but prototype vertical MOSFETs suggested headroom for future displacement in ultra-high-voltage regimes. Material selection thus evolved into an application-specific calculus balancing thermal headroom, switching speed, and cost per watt rather than defaulting to legacy silicon. Vendors that controlled substrate supply secured competitive insulation from wafer price swings and locked in multi-year sourcing agreements with telecom OEMs.

By Power Rating: High-Voltage Segment Accelerates Infrastructure Evolution

Medium-voltage devices (41–600 V) represented 45.90% of the IT and Telecom Discrete Semiconductor market size in 2025, anchored by 48 V data-centre architectures and 400 V rectifier shelves. Taiwan Semiconductor’s 600 V super-junction MOSFETs improved the figure of merit by 15% and enabled smaller magnetic components in VRMs. The >600 V bracket, though smaller, grew fastest at 10.8% CAGR as data-centre operators and transmission-backhaul providers embraced 800 V HVDC rails. Infineon’s joint work with NVIDIA on rack-scale HVDC distribution highlighted a shift toward centralized high-voltage inputs feeding multiphase point-of-load converters.

Low-voltage parts (≤ 40 V) continued to evolve for wearable and IoT designs, featuring ultra-low-gate-charge MOSFETs that cut standby current. Radiation-tolerant P-channel variants targeted LEO communication satellites, supporting telecom payload power switches. Overlaps between voltage tiers rose as suppliers introduced scalable silicon and SiC families spanning 40 V to 1,200 V, letting hardware teams maintain architectural consistency across access, edge, and core network elements.

By Packaging Technology: Chip-Scale Innovation Drives Miniaturization

Surface-mount packages still contributed 68.90% revenue in 2025 due to their proven manufacturability, yet chip-scale and wafer-level formats expanded at 12.7% CAGR to serve 5G handsets and massive-MIMO radios. March 2025 academic reviews traced packaging’s progression from ceramic can enclosures to Die-Sized SAW packages that freed precious board area in RF front ends. Infineon’s top-side-cooled D^2PAK packages boosted thermal resistance performance and gave designers headroom to raise switching frequency without enlarging heat spreaders.

Through-hole styles held residual share in legacy macro radios, where designers valued easy visual inspection and field-service soldering. Increasingly, however, multi-die power modules blurred the line between “discrete” and “integrated” as embedded passives and lead frame copper coins compressed Z-height. Telecom OEMs rewarded suppliers capable of co-designing mechanical form factors that fit narrow pluggable power shelves, further entwining packaging expertise with device-level performance roadmaps.

By Application: Telecom Infrastructure Accelerates Past Consumer Electronics

Telecom infrastructure equipment outpaced all segments with a 10.4% CAGR outlook, fuelled by densified 5G rollouts and early 6G trials demanding high-voltage efficiencies. Onsemi quantified that 5G base stations drew more than twice the power of 4G units and therefore benefited sharply from GaN and SiC MOSFET adoption. Smartphones and tablets still led overall revenue at 37.90% in 2025, capitalizing on persistent RF switch content growth as handset makers supported sub-6 GHz and millimetre-wave bands.

Data centres and cloud servers formed the next high-growth cohort as AI workloads surged. The IT and Telecom Discrete Semiconductor market size for power discrete used in 800 V rack architectures is projected to scale in lockstep with GPU counts. Network security equipment preserved a niche but consistent pull for avalanche-rated rectifiers and ultra-fast recovery diodes. Edge-device proliferation broadened the long-tail of low-power discrete, although unit economics remained sensitive to coin-cell lifetime guarantees.

Geography Analysis

Asia-Pacific sustained the largest 35.90% revenue slice in 2025 and was projected to post a 9.05% CAGR through 2031 as Chinese, Japanese, and Indian policy programmes poured subsidies into fabs, substrates, and advanced packaging lines. Export controls accelerated indigenous tool and epi-wafer development rather than derailing growth trajectories, especially in RF front-end production hubs. Japan stayed pivotal as a materials innovator, with ROHM targeting a 30% SiC share by 2027, while India extended USD-denominated incentives to lure foundry consortia and anchor a domestic supply chain.

North America harnessed CHIPS Act funding, announcing more than USD 450 billion of planned capacity that sought to triple national wafer output by 2032. Hyperscale data-centre clusters in the Pacific Northwest and Texas committed purchase orders for SiC and GaN devices to meet scope-2 carbon pledges. Canada and Mexico attracted backend assembly investments that complemented US front-end fabs, yet a looming 67,000-worker talent shortfall threatened ramp schedules and underscored the necessity of vocational pipelines.

Europe pursued a 20% global semiconductor share target by 2030 under the EU Chips Act, emphasizing industrial and automotive verticals that demanded high-reliability discrete. Germany earmarked up to EUR 50 billion (USD 57.39 billion) for Saxony-centric fabs, while France and Italy advanced grant schemes for power-device epi facilities. Energy-efficiency regulations aligned with SiC and GaN roadmaps, giving local device houses a regulatory tailwind. The Middle East and Africa leveraged telecom net-zero mandates to pilot SiC rectifier-rich power shelves, positioning the region as an early adopter of ultra-efficient infrastructure designs. Latin American markets such as Brazil gained traction as operators upgraded optical backbones, indirectly boosting discrete component demand in power and photonics modules.

Competitive Landscape

The IT and Telecom Discrete Semiconductor market displayed moderate concentration: the top five vendors controlled major revenue share, while dozens of specialists addressed niche voltage or frequency needs. Acquisition strategies favoured capability gaps over scale; Renesas moved for Transphorm to enrich GaN IP, and Onsemi purchased SiC JFET assets from Qorvo for USD 118.8 million in January 2025.[4]Onsemi, “Form 10-K Filing – Acquisition of SiC JFET Technology from Qorvo,” onsemi.com KPMG’s 2024 semiconductor M&A update cited resurging deal volumes focused on wide-bandgap fields, where design-in cycles promised premium margins.

Vertical integration emerged as a key differentiator. Wolfspeed invested heavily in SiC crystal growth, granting device subsidiaries stable wafer allocation. Infineon’s leap to 300 mm GaN and 200 mm SiC lines reinforced cost leadership and buffered substrate shortages. Meanwhile, module-oriented newcomers fused discrete dies with drivers and digital telemetry, targeting telecom OEM pain points around footprint and design resources. Traditional pure-play discrete providers responded by partnering with OSATs to co-develop low-inductance packages and retain socket relevance.

White-space opportunities clustered around heterogeneous integration, where co-packaged power stages replaced banks of parallel transistors. Equipment vendors signalled a preference for solution-level suppliers capable of firmware, analog control, and mechanical thermal design. As a result, competitors invested in reference designs that shortened customer NPI timelines and locked in subsequent consumable demand for replacement modules or derivative parts.

IT & Telecom Discrete Semiconductor Industry Leaders

Infineon Technologies AG

STMicroelectronics NV

Onsemi Corporation

Vishay Intertechnology Inc.

Toshiba Electronic Devices & Storage Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Infineon Technologies launched CoolSiC MOSFET 750 V G2 parts featuring R_DS(on) as low as 4 mΩ.

- May 2025: Infineon and NVIDIA announced an 800 V HVDC power architecture for AI data centers.

- April 2025: Microchip Technology broadened connectivity, storage, and power portfolios for AI-centric data centers.

- March 2025: Infineon extended radiation-tolerant P-channel MOSFETs for LEO satellites.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the IT & telecom discrete semiconductor market as revenue generated from sales of single-function, packaged devices, such as diodes, rectifiers, signal and power transistors, thyristors, and RF or microwave discretes, specifically designed into smartphones, data-center servers, switching and routing hardware, base-station radios, and edge/IoT nodes. According to Mordor Intelligence, the market was valued at USD 9.05 billion in 2025 and is projected to reach USD 12.05 billion by 2030, growing at 5.9 % CAGR.

Scope exclusion: modules that bundle multiple dies, passive components, or integrated circuits with discretes for automotive, industrial, or consumer white goods applications sit outside this assessment.

Segmentation Overview

- By Product Type

- Diodes

- Rectifiers

- Small-Signal Transistors

- Power Transistors

- MOSFET

- IGBT

- Bipolar Power Transistor

- Thyristors

- RF and Microwave Discretes

- Other Types

- By Material

- Silicon

- Silicon Carbide (SiC)

- Gallium Nitride (GaN)

- Others

- By Power Rating

- Low (≤ 40 V)

- Medium (41 V – 600 V)

- High (> 600 V)

- By Packaging Technology

- Through-Hole

- Surface-Mount (SMD)

- Chip-Scale and Wafer-Level

- By Application

- Smartphones and Tablets

- Data Centre and Cloud Servers

- Telecom Infrastructure Equipment

- Network Security and Routing

- IoT and Edge Devices

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed fabrication engineers, component distributors, telecom OEM procurement heads, and regional carrier network planners across North America, Asia-Pacific, and Europe. These discussions clarified average selling price movements, silicon-to-SiC mix changes, and realistic lead-time expectations, letting us refine penetration rates and stress test early desk assumptions.

Desk Research

We began with open-source pillars such as the International Telecommunication Union, GSM Association, World Semiconductor Trade Statistics, and customs-level export data, which help us size device flow into carrier and data-center supply chains. Complementary insights were drawn from annual reports and 10-Ks of key device makers, earnings transcripts of hyperscale cloud operators, peer-reviewed IEEE papers on wide-bandgap adoption, and patent analytics from Questel to gauge material shifts.

Commercial news aggregators like Dow Jones Factiva and company-level screens from D&B Hoovers assisted in spotting capacity additions and design wins, anchoring price and volume trend lines. This list is illustrative; numerous other public and paid sources informed data validation and context building.

Market-Sizing & Forecasting

A top-down addressable equipment build, derived from smartphone shipments, 5G base-station rollouts, server rack deployments, and broadband CPE installations, sets the demand pool. Select bottom-up checks, channel sell-through audits, and sampled ASP × volume for power MOSFETs and RF discretes calibrate totals before finalization. Key variables inside our multivariate regression forecast include 5G subscriber additions, average data-center power density, wafer starts by material, and capital spending of Tier-1 carriers, which together explain over 85 % of historical variance. Gaps where shipment data is thin are bridged using carrier capex proxies aligned with distributor feedback.

Data Validation & Update Cycle

Outputs pass three-layer reviews: automated variance flags, peer analyst cross-checks, and final sector lead approval. Models refresh annually, with ad hoc revisions when supply chain shocks, policy shifts, or major technology introductions materially alter assumptions.

Why Our IT & Telecom Discrete Semiconductor Baseline Commands Reliability

Published estimates seldom match because providers measure different device families, customer sets, and years. Mordor's disciplined scoping to telecom and IT hardware, coupled with yearly refreshes, positions our baseline as the most decision-ready view.

Competing figures diverge mainly from bundling all end markets, projecting aggressive silicon carbide ramps without corroborating fab capacity, or rolling vendor revenues straight through to market size without channel normalization.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 9.05 B (2025) | Mordor Intelligence | - |

| USD 43.84 B (2025) | Regional Consultancy A | Tracks every end-use vertical and folds analog IC revenue into discrete totals, yielding a broader base |

| USD 50.10 B (2023) | Trade Journal B | Relies on vendor revenue roll-ups; lacks telecom-specific breakouts and material-level cross-checks |

In summary, variations stem from scope width, device taxonomy, and validation rigor. By aligning variables to actual telecom hardware demand and vetting each step through industry dialogues, Mordor delivers a transparent, repeatable baseline clients can trust.

Key Questions Answered in the Report

What was the IT and Telecom Discrete Semiconductor market size in 2026 and how fast is it growing?

The market generated USD 9.58 billion in 2026 and is projected to expand at a 5.83% CAGR, reaching USD 12.72 billion by 2031.

Which product type holds the largest share of the IT and Telecom Discrete Semiconductor market?

Power transistors led with 60.80% revenue share in 2025, reflecting their central role in power conversion for telecom and data-centre hardware.

Why are SiC devices gaining popularity in telecom infrastructure?

SiC devices offer superior thermal conductivity and efficiency at high voltages, helping operators meet strict energy-efficiency and net-zero targets while shrinking cooling requirements.

How will 5G network expansion influence discrete semiconductor demand?

5G base-station rollouts require high-voltage GaN and SiC power amplifiers, driving incremental demand for wide-bandgap discrete with robust growth cantered in Asia-Pacific.

What impact do integrated power modules have on discrete semiconductor suppliers?

Integrated modules that merge MOSFETs, drivers and protection circuits reduce board space and simplify design, potentially displacing standalone discrete sockets and pressuring vendors lacking module capabilities.

Which region is projected to grow the fastest through 2031?

Asia-Pacific is forecast to post a 9.05% CAGR, propelled by large-scale manufacturing investments, domestic innovation and continuing 5G infrastructure expansion.

Page last updated on: