Market Overview

| Study Period | 2020 - 2030 |

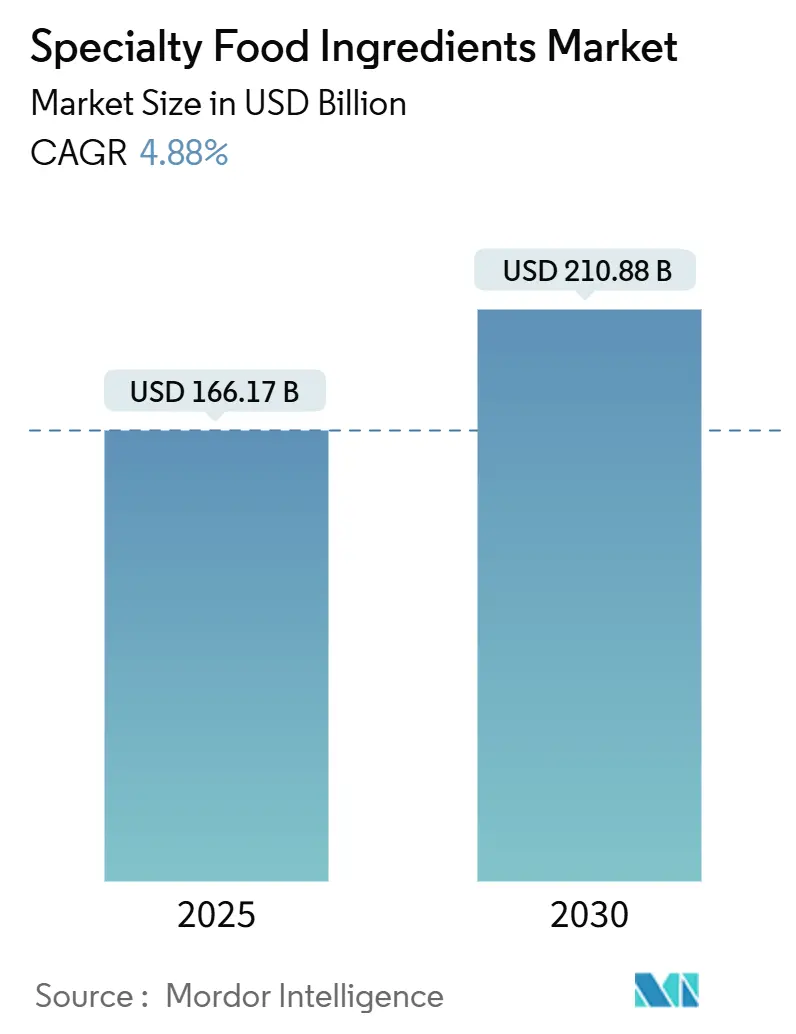

| Market Size (2025) | USD 166.17 Billion |

| Market Size (2030) | USD 210.88 Billion |

| Growth Rate (2025 - 2030) | 4.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Specialty Food Ingredients Market Analysis by Mordor Intelligence

The specialty food ingredients market is valued at USD 166.17 billion in 2025 and is projected to reach USD 210.88 billion by 2030, registering a CAGR of 4.88%. The market is growing due to rising health-conscious eating, clean-label preferences, and advancements in precision fermentation, enabling animal-free proteins and bioactive compounds with reduced environmental impact. Consumers demand natural, minimally processed ingredients, transparent labeling, and functional foods with less sugar and better nutrition. The U.S. FDA's plan to phase out synthetic dyes by 2026 has accelerated the use of natural colorants from fruits, vegetables, and botanicals. Enzyme engineering advancements support gluten-free, dairy-free, and protein-rich product formulations. Growth is further driven by increasing disposable incomes in emerging economies, especially in Asia-Pacific, with rising demand for probiotics, dietary supplements, and functional food ingredients.

Key Report Takeaways

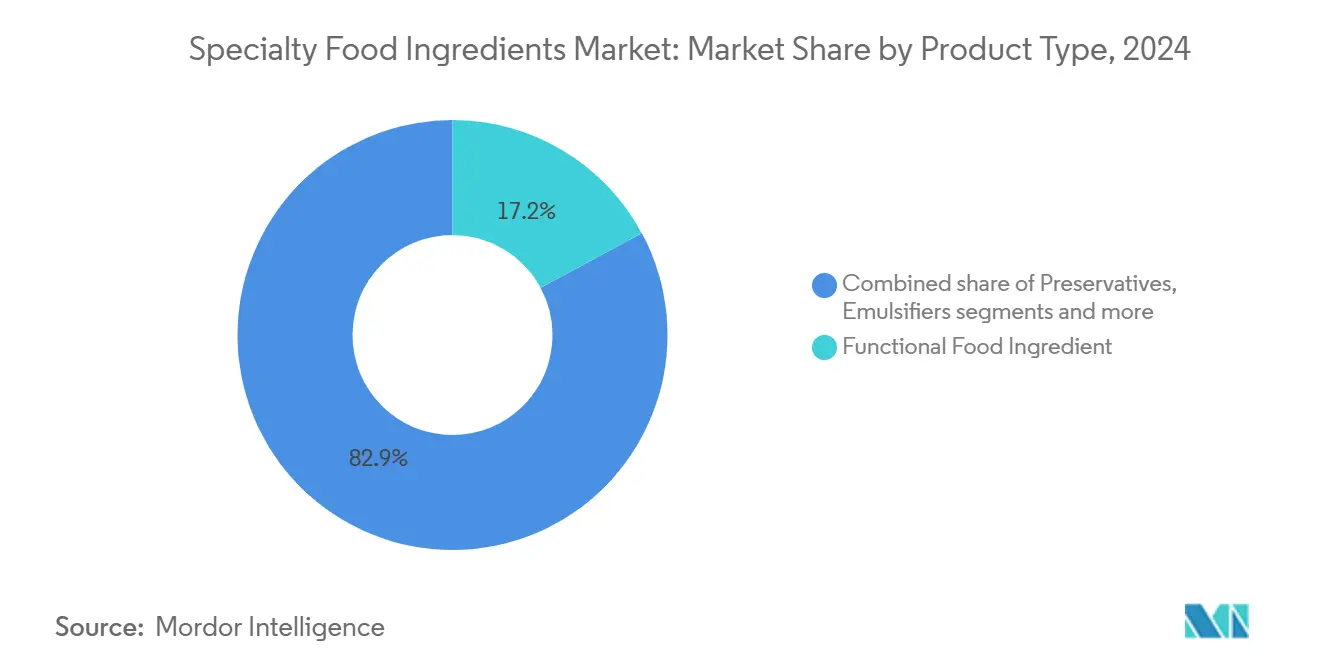

- By product type, functional food ingredients led with 17.15% revenue share in 2024; the specialty fats and oils are projected to expand at a 7.38% CAGR through 2030.

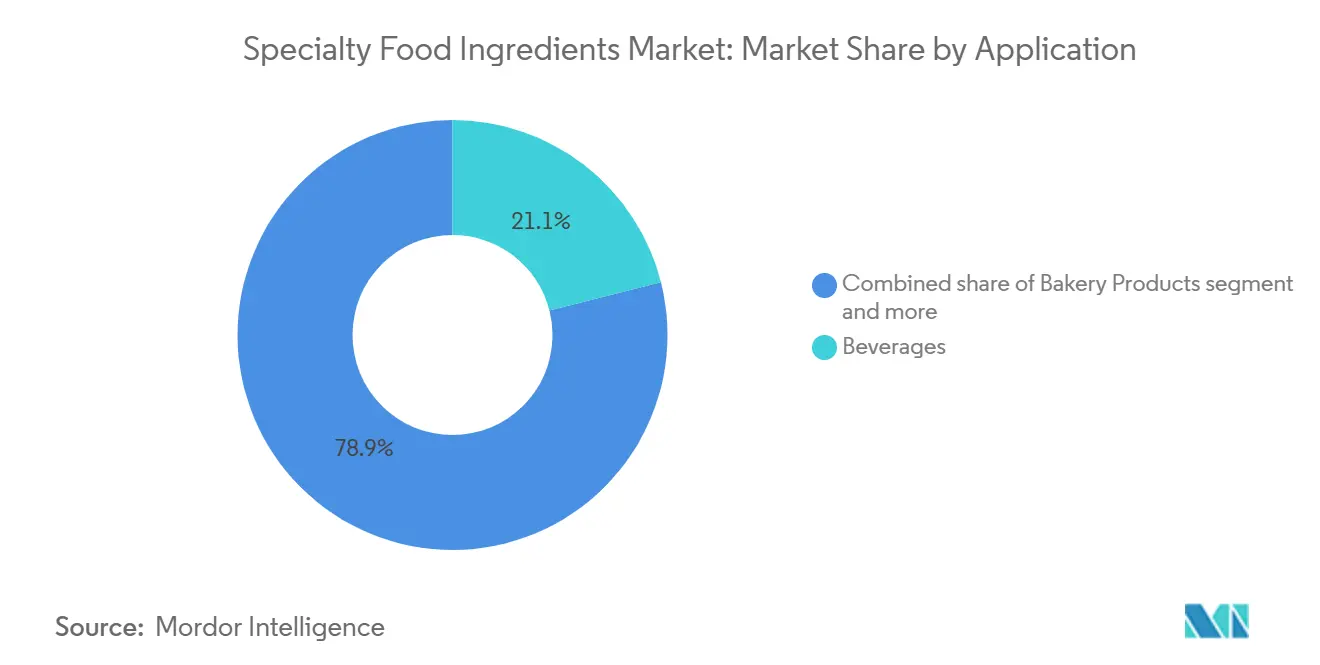

- By application, beverages held 21.06% of the specialty food ingredients market share in 2024, while plant-based food and beverage applications are set to grow at a 6.68% CAGR to 2030.

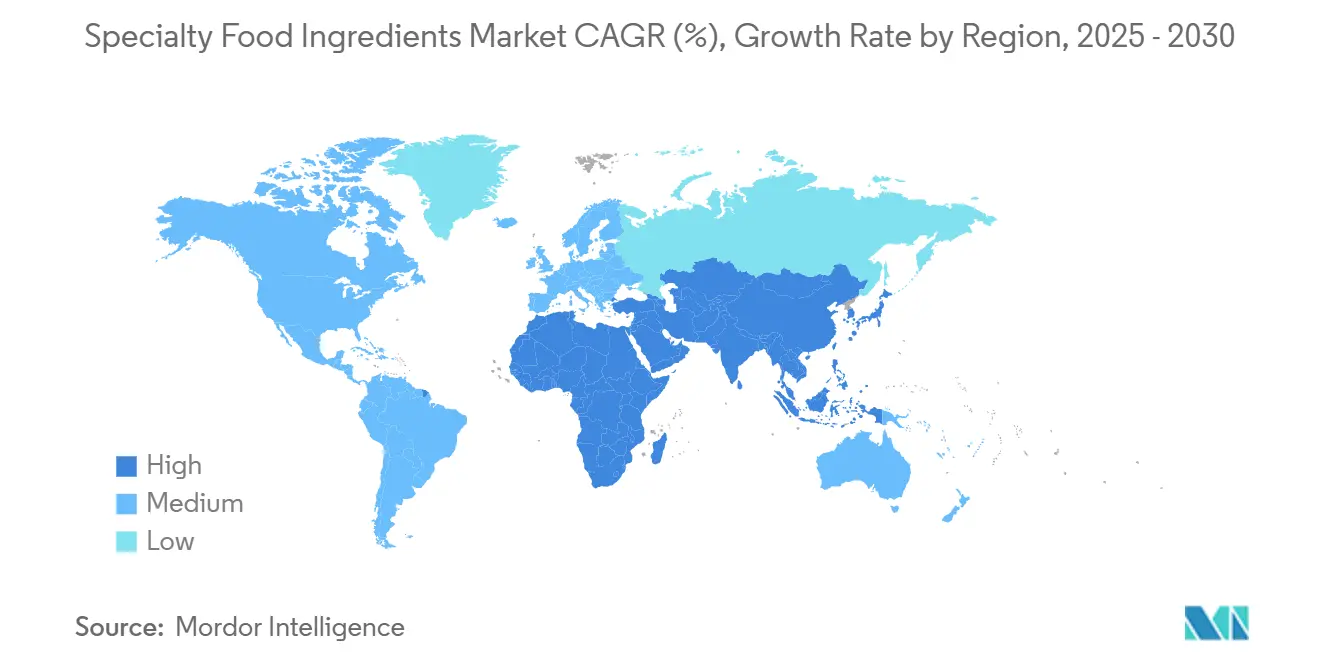

- By geography, North America accounted for 31.38% of 2024 sales, whereas Asia–Pacific is poised for the fastest growth at a 6.04% CAGR to 2030.

Global Specialty Food Ingredients Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of plant-based food sector | +1.2% | Global, with early gains in North America and Europe | Medium term (2-4 years) |

| Rise in demand for processed/packaged food | +0.8% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Premiumization of food products | +0.6% | North America and Europe | Short term (≤ 2 years) |

| Shift towards low-glycemic and diabetic-friendly products | +0.5% | Global | Medium term (2-4 years) |

| Technological advancement in fermentation and enzyme production | +0.9% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Rise in demand for functional foods | +0.7% | Global | Medium term (2-4 years) |

Source: Mordor Intelligence

Growth of Plant-Based Food Sector

The growing plant-based food market demands specialty ingredients that replicate animal-based functionalities while meeting clean-label standards. The 2024 Food and Health Survey by the International Food Information Council (IFIC) found 5% of Americans follow a flexitarian diet, with many seeking plant-based alternatives [1]Source: International Food Information Council (IFIC), "IFIC Food and Health Survey in 2024", ific.org. Beyond protein isolates, the market requires emulsifiers, texturizers, and flavor enhancers to mimic animal products' sensory attributes. Companies like Paleo use precision fermentation to produce GMO-free animal heme proteins, enabling plant-based meat producers to achieve authentic flavors and maintain premium pricing. Hydrocolloid and protein ingredient suppliers benefit as their products provide essential mouthfeel and binding properties. Supply chain issues with locust bean gum and carrageenan have led to alternatives like xanthan and gellan gums, offering similar functionality and better availability. Developing new ingredients involves rigorous testing, regulatory compliance, and optimization, requiring long-term R&D partnerships between ingredient suppliers and food manufacturers.

Rise in Demand for Processed/Packaged Food

Urbanization and changing lifestyles drive consistent demand for processed food ingredients focused on preservation, texturization, and nutrition. In 2024, the European Commission updated regulations on additives like sorbic acid and potassium sorbate, ensuring safety while supporting increased usage [2]Source: European Commission, “Commission Regulation (EU) 2024/… on Food Additives”, ec.europa.eu. These updates help manufacturers improve shelf life and quality, vital for exports. Enzyme manufacturers benefit as food processors adopt biotechnology for texture and nutrient enhancements. Ingredion's USD 100 million Indianapolis facility expansion in March 2025 highlights the industry's growth potential, supported by strong performance in its Texture and Healthful Solutions division despite inflation. The processed food sector's diverse ingredient needs create significant revenue opportunities for specialty ingredient manufacturers.

Premiumization of Food Products

Consumers' willingness to pay a premium for quality and health benefits is driving growth in the functional foods market, with demand for digestive health, immunity, and cognitive performance. This benefits suppliers of bioactive compounds, specialty proteins, and novel sweeteners, enabling manufacturers to differentiate products with validated health claims and superior sensory attributes. In August 2024, Rousselot launched Nextida GC collagen peptides for glucose management, showcasing targeted health solutions. Sustainability is also key, as seen in McCormick's "Grown for Good" initiative in China, which emphasizes ingredient origin and traceability. Premium formulations with higher-cost ingredients offer margin expansion opportunities for specialty suppliers demonstrating value through clinical studies and certifications.

Shift Toward Low-Glycemic and Diabetic-Friendly Products

Rising diabetes rates and growing metabolic health awareness have increased demand for low-glycemic ingredients that maintain taste. Bestzyme's FDA GRAS-approved Mellia Brazzein sweetener enables significant sugar reduction in chocolates and confections without compromising flavor. Enzyme technologies that convert sugar to fiber support healthier formulations, creating opportunities for enzyme suppliers and alternative sweetener producers. Precision-fermented sweeteners like reb-M and brazzein reduce sugar by 60-75% while preserving sensory properties, helping manufacturers meet regulations and consumer demands. The diabetic-friendly products market is expanding, driven by regulatory support and health-conscious consumers, fueling demand for specialized ingredient solutions.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost associated with speciality ingredients | -0.9% | Global | Short term (≤ 2 years) |

| Supply chain challenges for niche ingredients | -0.7% | Global, particularly Asia-Pacific supply chains | Medium term (2-4 years) |

| Significant investment required for certification and testing | -0.5% | North America and Europe regulatory markets | Long term (≥ 4 years) |

| Consumer resistance to novel ingredients | -0.4% | North America and Europe | Medium term (2-4 years) |

Source: Mordor Intelligence

High Cost Associated with Specialty Ingredients

Rising raw material costs and complex manufacturing processes are intensifying pricing pressures in the specialty ingredients market, particularly for small-scale producers lacking economies of scale. These producers face challenges in maintaining profit margins while managing higher costs and meeting quality standards. Companies like The Flava People are addressing ingredient cost inflation by renegotiating supplier contracts, adopting collective purchasing, and exploring alternative sourcing. In the hydrocolloids segment, supply constraints for locust bean gum and carrageenan are driving price increases, prompting manufacturers to shift to alternatives like xanthan gum and modified starches. The market is segmented between premium applications that can absorb higher costs and mass-market products requiring cost-effective substitutes, creating opportunities but challenging manufacturers to balance quality and cost.

Supply Chain Challenges for Niche Ingredients

Global supply chain vulnerabilities significantly affect specialty ingredient markets, with a particularly severe impact on niche products that rely on limited sourcing options. The hydrocolloids market faces persistent supply constraints stemming from multiple factors: critical raw material scarcity, widespread workforce limitations, substantially elevated energy costs, and intensifying geopolitical events, including the prolonged Ukraine conflict. These extensive supply disruptions clearly demonstrate the heightened susceptibility of niche ingredients to external market shocks and global disturbances. While DSM-Firmenich's vitamin operations benefited from the prevailing supply limitations, this situation emphasized the critical importance of implementing comprehensive diversified sourcing strategies and robust inventory management systems across specialty food ingredient manufacturers to ensure operational resilience.

Segment Analysis

By Product Type: Functional Ingredients Anchor Value Creation

Functional food ingredients accounted for 17.15% of the specialty food ingredients market share in 2024. This segment's growth is driven by rising consumer demand for health-promoting components such as vitamins, minerals, amino acids, omega-3s, and probiotics. The ability to make scientifically substantiated health claims enables manufacturers to position products at premium price points. Specialty fats and oils emerge as one of the fastest-growing segments, projected to register a 7.38% CAGR, propelled by demand for customized lipid profiles, plant-based alternatives, and tailored nutritional formulations. Meanwhile, segments such as natural sweeteners and specialty starches continue to gain ground due to sugar-reduction mandates and clean-label preferences.

Biotechnology continues to reshape the specialty food ingredients market, enabling enhanced functionality and greater sustainability. Onego Bio's Bioalbumen, a precision-fermented egg-white protein, exemplifies this trend by offering equivalent foaming and binding properties to conventional egg whites while eliminating exposure to avian flu-related supply chain risks. Enzymatic processing methods for flavor extraction and the shift toward cellulose-based natural colorants are further driven by regulatory shifts away from synthetic additives. These innovations ensure regulatory compliance while improving product performance, contributing to the overall expansion of the specialty ingredients space

Note: Segment shares of all individual segments available upon report purchase

By Application: Beverages Dominate, Plant-Based Foods Accelerate

Beverages accounted for 21.06% of the specialty food ingredients market size in 2024, driven by functional hydration products, nootropic drinks, and sports nutrition beverages. Companies like Quest Nutrition and Pioneer Pastures utilize ultra-filtered milk technology to produce high-protein products with lower sugar content, demonstrating the integration of membrane filtration with clean-label ingredient solutions. The plant-based food and beverage segment is expected to grow at a 6.68% CAGR, primarily through dairy alternatives and meat substitutes that require specialty proteins, emulsifiers, and natural flavors to replicate traditional products.

The bakery segment utilizes enzymes to enhance product softness and shelf life while reducing chemical additives. Confectionery manufacturers are reformulating products using low-glycemic sweeteners. The market expansion includes functional snacks targeting emotional wellness, as demonstrated by Singapore-based Hue's product line featuring Asian botanicals. The successful adaptation of formulations across different product categories creates diverse revenue opportunities for ingredient manufacturers.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America held 31.38% of global sales in 2024, driven by supportive regulations, established R&D infrastructure, and consumers' willingness to pay more for functional benefits. The FDA's GRAS pathway facilitates market entry for novel bioengineered ingredients despite ongoing regulatory review. The region's production capabilities benefit from precision-fermentation facilities and co-manufacturing centers, while consumers prefer "100% natural" labels, driving clean-label ingredient demand.

Europe influences global standards through the European Food Safety Authority's (EFSA) 2025 novel-food guidance, which implements stricter data requirements while introducing pre-submission reviews to reduce approval times [3]Source: European Food Safety Authority, “Novel Food Catalogue”, efsa.europa.eu. Industry initiatives, including Cargill's target to decrease supply-chain greenhouse gas emissions by 30% by 2030, reflect a growing interest in circular-economy ingredients from upcycled materials. Recent approvals of glucosyl hesperidin and tiger-nuts oil demonstrate regulatory support for scientifically validated innovations.

Asia-Pacific projects a 6.04% CAGR through 2030, driven by increasing disposable incomes, urbanization, and growing demand for functional products. China's expanded "Three New Foods" catalogue includes 98 new ingredients and 215 additives, providing clear guidelines for international suppliers. Regional biotechnology investments, such as VTT's CellularFood platform, support domestic production of alternative proteins and specialty bioactives. Traditional acceptance of botanical ingredients enables broader adoption of adaptogens and functional mushrooms in mainstream food products, expanding the specialty ingredients market.

Competitive Landscape

The specialty food ingredients market remains fragmented, with no single supplier holding more than a low-double-digit market share. The market anticipates increased consolidation in 2025, exemplified by Tate & Lyle's USD 1.8 billion acquisition of CP Kelco, which aims to establish a global texture and stabilization platform with projected annual synergies of USD 50 million. DSM-Firmenich demonstrates industry innovation through its single-cell protein development for net-zero-carbon applications, utilizing proprietary fermentation to maintain margins amid commodity price fluctuations.

Companies are pursuing vertical integration to mitigate supply chain risks by acquiring fermentation facilities, proprietary strains, and downstream formulation expertise. Regulatory approvals create competitive advantages, as demonstrated by FDA GRAS Notice 1143 for Bacillus subtilis NRRL 68053, which provides market exclusivity through validated safety documentation. The market sees increased activity from innovative start-ups, supported by venture capital and corporate investors, developing precision-fermented products such as heme proteins, egg alternatives, and sweet proteins that meet sustainability and clean-label requirements.

Application centers have become essential competitive differentiators, where ingredient suppliers collaborate with food manufacturers to test new solutions. This collaborative approach reduces product launch timelines while ensuring regulatory compliance. The service-oriented model strengthens customer relationships and increases switching costs, reinforcing market positions as functional requirements and labeling regulations become more complex across different regions.

Specialty Food Ingredients Industry Leaders

-

Cargill, Incorporated

-

Kerry Group PLC

-

International Flavors & Fragrances

-

Archer Daniels Midland Company

-

Tate & Lyle plc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Xampla developed a plant-based microencapsulation technology for Vitamin D fortification in food and beverages. The technology utilizes pea protein to create microscopic capsules that protect Vitamin D from degradation during processing, storage, and digestion, maintaining its stability and bioavailability.

- July 2024: NutraEx Food, Inc. introduced Bi-Sugar, a natural sweetener product developed using dry-embedding technology. The process bonds L-arabinose with regular sugar and an additional natural sweetener. Bi-Sugar is suitable for beverages, bakery items, confectionery, and dairy products and provides caramel notes. The product offers four key benefits: sweetness, reduced calories, sugar blocking properties, and lower costs.

- January 2024: Elo Life Systems, based in North Carolina, secured USD 20.5 million in Series A2 funding to advance its development of natural high-intensity sweeteners and disease-resistant Cavendish bananas that can withstand Fusarium wilt fungal disease (TR4).

- January 2024: Evonik Industries introduced VITAPUR, a new range of water-soluble vitamins for food and beverage fortification in the Asia-Pacific region. The product aims to enhance the nutritional value of various food products, addressing the increasing demand for fortified foods.

Global Specialty Food Ingredients Market Report Scope

Specialty food ingredients offer technological and functional benefits and provide consumers with a wide range of tasty, safe, healthy, affordable, qualitative, and sustainably produced food options.

The Specialty Food Ingredients Market is Segmented by Product Type (Functional Food Ingredient, Specialty Starch and Texturants, Sweeteners, Food Flavors and Enhancers, Acidulants, Preservatives, Emulsifiers, Colorants, Enzymes, Proteins, Specialty Fats and Oils, Food Hydrocolloids and Polysaccharides, Anti-Caking Agents, Yeast, and Food-Grade Glycerin), Application (Bakery Products, Beverages, Meat, Poultry and Seafood, Dairy Products, Confectionery, Fats and Oils, Dressings/Condiments/Sauces/Marinade, Pasta, Soup and Noodles, Prepared Food, Plant-based Food and Beverage, and Other Applications), and Geography (North America, Europe, Asia-Pacific, South America, and Middle-East and Africa). The report offers market size and forecasts in terms of value in USD million for all the above segments.

| By Product Type | Functional Food Ingredient | Vitamins | |

| Minerals | |||

| Amino Acids | |||

| Omega-3 Ingredients | |||

| Probiotic Cultures | |||

| Other Functional Food Ingredients | |||

| Speciality Starch and Texturants | |||

| Sweetener | |||

| Food Flavors and Enhancers | |||

| Acidulants | |||

| Preservatives | |||

| Emulsifiers | |||

| Colorants | |||

| Enzymes | |||

| Proteins | |||

| Speciality Fats and Oils | |||

| Food Hydrocolloids and Polysaccharides | |||

| Anti-Caking Agents | |||

| Other Product Types | |||

| By Application | Bakery Products | ||

| Beverages | |||

| Meat, Poultry, and Seafood | |||

| Dairy Products | |||

| Confectionery | |||

| Fats and Oils | |||

| Dressings/Condiments/Sauces/Marinade | |||

| Pasta, Soup and Noodles | |||

| Prepared Food | |||

| Plant-based Food and Beverage | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Netherlands | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Indonesia | |||

| South Korea | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

By Product Type

| Functional Food Ingredient | Vitamins |

| Minerals | |

| Amino Acids | |

| Omega-3 Ingredients | |

| Probiotic Cultures | |

| Other Functional Food Ingredients | |

| Speciality Starch and Texturants | |

| Sweetener | |

| Food Flavors and Enhancers | |

| Acidulants | |

| Preservatives | |

| Emulsifiers | |

| Colorants | |

| Enzymes | |

| Proteins | |

| Speciality Fats and Oils | |

| Food Hydrocolloids and Polysaccharides | |

| Anti-Caking Agents | |

| Other Product Types |

By Application

| Bakery Products |

| Beverages |

| Meat, Poultry, and Seafood |

| Dairy Products |

| Confectionery |

| Fats and Oils |

| Dressings/Condiments/Sauces/Marinade |

| Pasta, Soup and Noodles |

| Prepared Food |

| Plant-based Food and Beverage |

| Other Applications |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the specialty food ingredients market?

The specialty food ingredients market is valued at USD 166.17 billion in 2025 and is projected to reach USD 210.88 billion by 2030, growing at a 4.88% CAGR.

Which product category holds the largest share?

Functional Food Ingredients led with 17.15% of 2024 revenue, driven by demand for vitamins, minerals, and probiotics that support specific health claims.

Which application segment is growing fastest?

Plant-based food and beverage applications are forecast to grow at a 6.68% CAGR through 2030 as consumers seek sustainable protein alternatives.

Why is Asia–Pacific considered the fastest-growing region?

Rising disposable incomes, urbanization, and regulatory support for novel foods are propelling Asia–Pacific at a 6.04% CAGR.

Page last updated on: July 5, 2025