Market Overview

| Study Period | 2019 - 2030 |

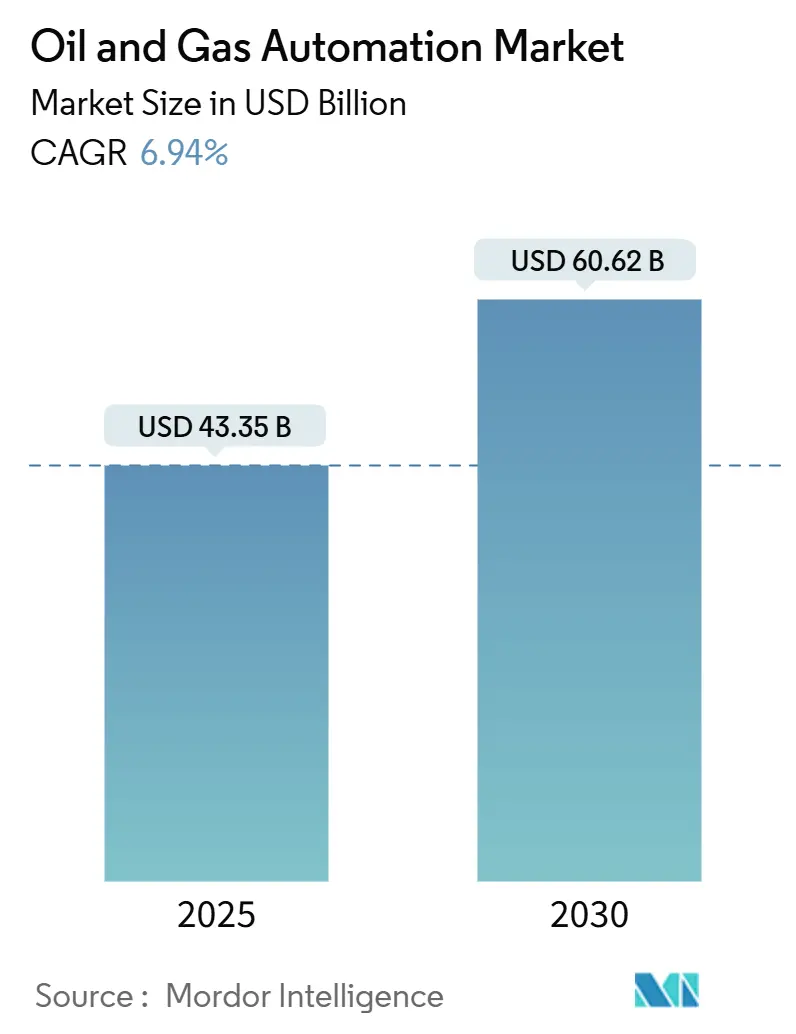

| Market Size (2025) | USD 43.35 Billion |

| Market Size (2030) | USD 60.62 Billion |

| Growth Rate (2025 - 2030) | 6.94% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Oil & Gas Automation Market Analysis by Mordor Intelligence

The oil & gas automation market size reached a value of USD 43.35 billion in 2025 and is set to climb to USD 60.62 billion by 2030, registering a 6.9% CAGR during the forecast period. Operators are embracing intelligent field platforms, edge-AI analytics, and autonomous inspection tools to curb downtime and lift productivity as supply chains tighten and energy transition goals intensify. Mandatory safety regulations, especially those aligned with IEC 61511 and ISA-84, are accelerating uptake of Safety Instrumented Systems that respond to hazards in milliseconds. LNG infrastructure expansion across Asia-Pacific and Africa is unlocking new demand for cryogenic-grade control systems that handle high-pressure, −160 °C environments. Finally, growing cybersecurity budgets—now 15-20% of total automation spend—are reshaping project economics as operators harden operational technology (OT) environments against ransomware and state-sponsored attacks.

Key Report Takeaways

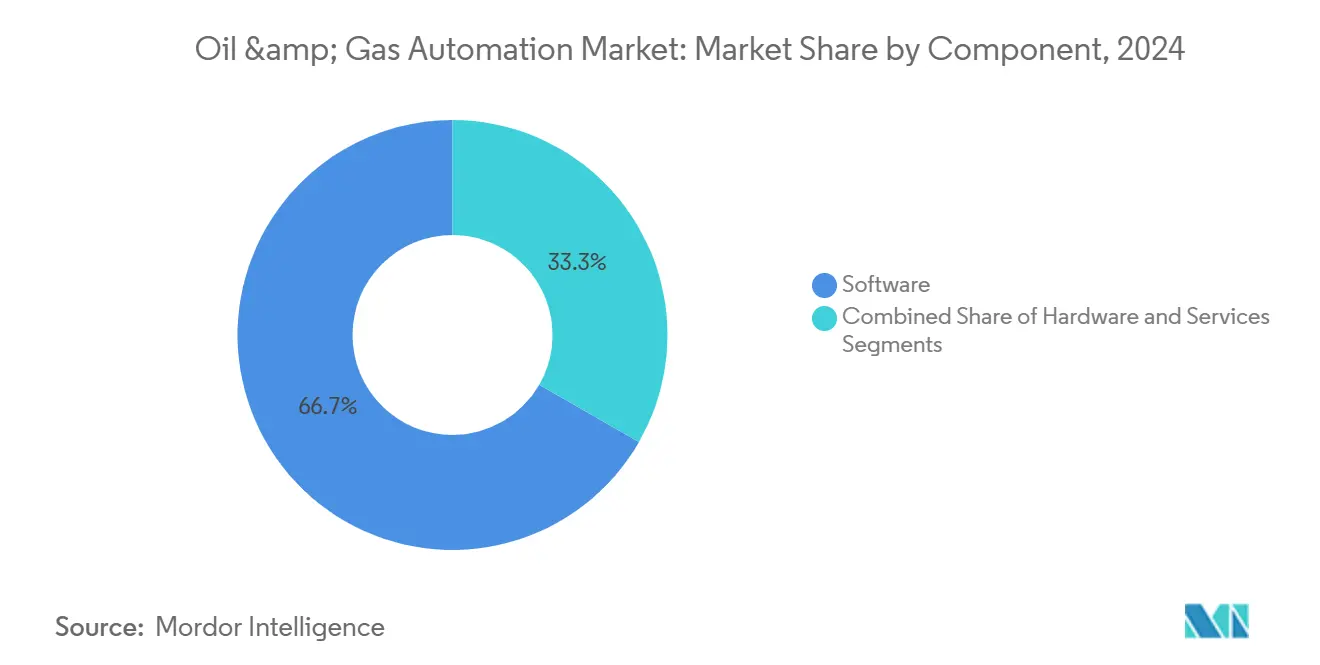

- By component, software held 66.7% of the oil & gas automation market share in 2024, while services are forecast to grow at an 8.5% CAGR through 2030.

- By process, upstream operations accounted for 59.1% of revenue in 2024; midstream activities are projected to expand at an 8.3% CAGR as LNG terminals proliferate.

- By technology, Distributed Control Systems retained 30.1% share of the oil & gas automation market size in 2024, whereas SCADA platforms are rising at a 7.0% CAGR.

- By application, production and well optimisation captured 38.2% share in 2024; LNG terminals and storage facilities are advancing at a 7.9% CAGR to 2030.

- By geography, North America led with 37.1% of market revenue in 2024; Asia-Pacific is set to grow the fastest at 7.5% CAGR on the back of refinery modernisation and upstream digitisation.

Global Oil & Gas Automation Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of digital-oilfield platforms | +1.2% | Global, with early gains in North America, Middle East | Medium term (2-4 years) |

| Modernization CAPEX for remote monitoring and predictive maintenance | +1.8% | North America and EU, APAC core | Long term (≥ 4 years) |

| Mandatory safety-system regulations | +1.0% | Global, with stringent enforcement in North America, Europe | Short term (≤ 2 years) |

| LNG and mid-stream build-out in APAC and Africa | +1.5% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Edge-AI deployment for real-time analytics at hazardous sites | +0.9% | Global, with concentration in offshore operations | Long term (≥ 4 years) |

| Autonomous inspection drones and robotics for offshore assets | +0.8% | Global offshore regions, North Sea, Gulf of Mexico, APAC | Medium term (2-4 years) |

Source: Mordor Intelligence

Rising Adoption of Digital-Oilfield Platforms

Real-time digital platforms fuse IoT sensors, machine-learning models, and cloud analytics into unified dashboards that shorten decision cycles from minutes to seconds. Devon Energy lifted well longevity by 25% after deploying AI-guided drilling adjustments. Virtual twins synchronised with live operating data let engineers test scenarios without risking physical assets, an approach that is especially potent in unconventional reservoirs where downhole conditions vary by the hour.

Modernisation CAPEX for Remote Monitoring and Predictive Maintenance

Operators are redirecting capital toward remote surveillance tools that cut site visits and shrink safety exposure. Enbridge’s Azure-based pipeline analytics improved threat detection by 30%[1]Enbridge, “AI ROW Threat Identification System,” enbridge.com. Predictive algorithms study vibration and thermal trends to spot failures weeks in advance, trimming routine inspection costs up to 50% while boosting reliability.

Mandatory Safety-System Regulations

IEC 61511 compliance is driving rapid deployment of automated shutdown layers that outperform human reaction times. The PHMSA control-room rules, paired with Europe’s NIS 2.0 cybersecurity directive, oblige operators to document risk reduction and install redundant logic solvers that isolate faults without process disruption.

LNG and Mid-Stream Build-Out in Asia-Pacific and Africa

Projected 40% growth in Asia-Pacific LNG import capacity is pushing demand for automation that can handle extreme cryogenic conditions. Emerson’s DeltaV platform underpins several 10 Mtpa projects, balancing −160 °C temperature swings while optimising energy consumption by up to 5% through AI-driven tuning.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-oil price volatility impacting OPEX and CAPEX cycles | -1.5% | Global, with acute impact in North America | Short term (≤ 2 years) |

| Escalating cyber-risk and OT-security compliance costs | -0.8% | Global, with stringent requirements in North America, Europe | Medium term (2-4 years) |

| High upfront automation expenditure and ROI uncertainty | -1.2% | Global, particularly affecting smaller operators | Long term (≥ 4 years) |

| Legacy-system interoperability | -0.6% | Global, with concentration in mature oil regions | Medium term (2-4 years) |

Source: Mordor Intelligence

Crude-Oil Price Volatility Impacting OPEX and CAPEX Cycles

Six-month lags between crude swings and spending shifts force smaller producers to delay automation upgrades when cash flows tighten. Subscription-based automation services that align fees with production volumes are gaining favour because they lower upfront risk and preserve liquidity during downturns.

Escalating Cyber-Risk and OT-Security Compliance Costs

Following the Colonial Pipeline incident, security spending now consumes up to one-fifth of automation budgets. Air-gapped architectures, zero-trust networks, and 24-hour threat monitoring inflate life-cycle costs and prolong project timelines in regions under strict critical-infrastructure rules.

Segment Analysis

By Component: Software Leadership Drives Service Innovation

Software captured 66.7% of 2024 revenue, anchoring the oil & gas automation market through analytics engines that power predictive maintenance and autonomous operations. In value terms, the component accounted for USD 28.9 billion of the oil & gas automation market size in 2024. Services, although smaller, are projected for an 8.5% CAGR as operators outsource AI configuration and cybersecurity hardening.

Software growth is reinforced by edge-AI packages that lift drilling rates of penetration by 35-45%. Meanwhile, service contracts that bundle 24-hour monitoring and outcome-based guarantees move providers from product suppliers to performance partners. Hardware remains essential for sensor grids and ruggedised edge devices; however, its share is expected to decline gradually as virtualised control logic migrates to software layers.

Note: Segment shares of all individual segments available upon report purchase

By Process: Upstream Dominance Meets Midstream Acceleration

Upstream activities generated 59.1% of 2024 process revenue as autonomous drilling and production optimisation platforms calibrated thousands of downhole parameters at shale wells. This translated to roughly USD 25.6 billion of the oil & gas automation market size. Midstream operations, while holding a smaller base, are growing at 8.3% CAGR due to global LNG terminal build-outs and pipeline digitisation.

Upstream players like SLB demonstrated 25 automatic geosteering corrections on a single lateral, signalling a shift toward fully autonomous rigs. For midstream firms, cloud-linked SCADA systems enable real-time leak detection and remote valve actuation across thousands of kilometres, reducing incident response time from hours to minutes. Downstream sites are piloting AI-directed distillation columns that cut energy use and trim emissions.

By Technology: DCS Stability Anchors SCADA Innovation

Distributed Control Systems remained the backbone of complex refining and LNG trains, controlling 30.1% of technology-based revenue in 2024. SCADA, however, is the fastest climber at 7.0% CAGR as pipeline operators adopt satellite-enabled remote monitoring for widely dispersed assets.

Honeywell’s Experion PKS exemplifies convergence by embedding AI decision support inside a classic DCS framework. PLCs continue to govern high-speed, deterministic tasks such as blowout preventer actuation, while Safety Instrumented Systems provide independent protective layers meeting SIL-3 mandates. Intelligent sensors now integrate edge compute boards, turning field devices into micro-decision nodes that pre-filter data before dispatch to a central historian.

Note: Segment shares of all individual segments available upon report purchase

By Application: Production Optimisation Leads LNG Terminal Surge

Production and well optimisation retained 38.2% share in 2024, representing USD 16.5 billion of the oil & gas automation market size. AI-driven artificial-lift management raised ExxonMobil’s output by 2.2% across 1,300 wells. LNG terminals and storage facilities, although smaller today, are on track for 7.9% CAGR as governments lock in flexible gas supply and mandate cryogenic-grade automation.

Drilling applications benefit from real-time downhole analytics that steer bits through productive zones, while pipeline operators deploy fibre-optic sensing for predictive leak detection. Refining assets are testing closed-loop AI controllers that adjust 13 valves simultaneously, a milestone achieved during continuous autonomous distillation at Eneos Kawasaki refinery.

Geography Analysis

North America led the oil & gas automation market with 37.1% revenue share in 2024, buoyed by shale developers that pioneered AI-steered drilling and pad optimisation. Persistent learn-and-apply cycles keep regional productivity high even when rig counts fluctuate. The region’s cybersecurity posture is also mature, with operators adopting zero-trust OT frameworks mandated by federal guidelines.

Asia-Pacific is poised for a 7.5% CAGR through 2030. China is modernising refineries to produce cleaner fuels, while India accelerates upstream digitisation across deep-water blocks. Massive LNG import projects in Southeast Asia rely on AI-enabled cryogenic controls to secure supply and balance power grids with intermittent renewables. Governments support digital twins to curb emissions and enhance safety, propelling technology adoption.

Europe maintains steady spending under stringent safety and environmental regulations. New LNG regasification units in Germany and Finland integrate DCS platforms that meet SIL-3 safety layers and NIS 2.0 cybersecurity mandates. Middle Eastern national oil companies, supported by sovereign funds, scale AI-driven well monitoring across mature carbonate reservoirs, exemplified by ADNOC’s USD 920 million ENERGYai program[2]ADNOC, “ENERGYai Digital Well Programme,” adnoc.ae. Africa and South America remain emerging adopters, often leveraging joint-venture partners for technology transfer and financing.

Competitive Landscape

Market concentration is moderate as four global automation majors—ABB, Honeywell, Siemens, and Emerson—provide end-to-end portfolios covering sensors, control systems, and lifecycle services[3]Honeywell, “Experion PKS with AI-Driven Decision Support,” honeywell.com. Their installed bases and worldwide service networks create high switching costs for brownfield upgrades.

Disruption comes from AI-native firms such as Corva, Agora, and Sensia, which specialise in edge-based analytics, autonomous drilling, and real-time production optimisation. These players often partner with incumbents; Honeywell and Chevron co-developed AI advisory tools for refineries, while Enbridge teamed with Microsoft to launch AI-powered threat detection for pipelines.

Oilfield service giants—SLB, Baker Hughes, and Halliburton—are folding proprietary automation suites into drilling and completions offerings. SLB’s Neuro geosteering technology autonomously executed 25 trajectory changes in Ecuador, signalling that algorithms can now assume complex directional decisions. White-space opportunities persist in autonomous robotics, OT cybersecurity, and outcome-based contracting, allowing niche specialists to carve out defensible positions even as consolidation accelerates.

Oil & Gas Automation Industry Leaders

-

ABB Ltd

-

Honeywell International Inc

-

Rockwell Automation Inc

-

Mitsubishi Corporation

-

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Chevron started production at the Ballymore subsea tie-back, targeting 300,000 bpd using advanced automation.

- March 2025: TotalEnergies prepared remotely controlled robots for offshore inspection trials.

- February 2025: ADNOC and AIQ completed ENERGYai proof-of-concept with 70% seismic interpretation accuracy gain.

- May 2024: Eneos and Preferred Networks achieved the first continuous autonomous distillation run at Kawasaki refinery.

Global Oil & Gas Automation Market Report Scope

Oil & Gas is a dynamic global industry that faces challenges in cost management, extraction of high value from current assets, and maximization of the up-time. Technological advancement has led to the establishment of connected enterprises that are helping the oil and gas industry move closer to operational excellence. Hence, the industry has been deploying various automation solutions to optimize operations.

The Oil & Gas Automation Market is segmented by Process (Upstream, Midstream, Downstream), by Technology (Sensors & Transmitters, Distributed Control Systems (DCS), Programmable Logic Controllers (PLC), Supervisory Control and Data Acquisition System (SCADA), Safety Instrumented Systems (SIS), Variable Frequency Drive (VFD), Manufacturing Execution System, Industrial Asset Management) and by Geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| By Component | Hardware | |||

| Software | ||||

| Services | ||||

| By Process | Upstream | |||

| Midstream | ||||

| Downstream | ||||

| By Technology | Sensors and Transmitters | |||

| Distributed Control Systems (DCS) | ||||

| Programmable Logic Controllers (PLC) | ||||

| Supervisory Control and Data Acquisition (SCADA) | ||||

| Safety Instrumented Systems (SIS) | ||||

| Other Technologies | ||||

| By Application | Drilling and Completion | |||

| Production and Well Optimization | ||||

| Pipeline and Transportation | ||||

| Refining and Petrochemicals | ||||

| LNG Terminals and Storage | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| Japan | ||||

| India | ||||

| South Korea | ||||

| Australia | ||||

| Rest of Asia-Pacific | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Middle East and Africa | Middle East | Saudi Arabia | ||

| United Arab Emirates | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Egypt | ||||

| Nigeria | ||||

| Rest of Africa | ||||

By Component

| Hardware |

| Software |

| Services |

By Process

| Upstream |

| Midstream |

| Downstream |

By Technology

| Sensors and Transmitters |

| Distributed Control Systems (DCS) |

| Programmable Logic Controllers (PLC) |

| Supervisory Control and Data Acquisition (SCADA) |

| Safety Instrumented Systems (SIS) |

| Other Technologies |

By Application

| Drilling and Completion |

| Production and Well Optimization |

| Pipeline and Transportation |

| Refining and Petrochemicals |

| LNG Terminals and Storage |

By Geography

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the oil & gas automation market?

The oil & gas automation market size reached USD 43.35 billion in 2025 and is forecast to hit USD 60.62 billion by 2030 at a 6.9% CAGR.

Which component leads the oil & gas automation market?

Software leads with 66.7% market share, driven by AI analytics and real-time optimisation platforms.

Why are services growing faster than hardware?

Services are expanding at 8.5% CAGR because operators need specialised integration, cybersecurity, and continuous optimisation support for complex AI deployments.

Which region is growing the fastest?

Asia-Pacific is projected to grow at 7.5% CAGR owing to aggressive LNG infrastructure expansion and refinery modernisation initiatives.

What are the main restraints on market growth?

Crude-price volatility that delays CAPEX cycles and escalating cybersecurity compliance costs are the two strongest headwinds, together cutting 2.3 percentage points from the forecast CAGR.

How are autonomous robots used in oil & gas operations?

Operators like TotalEnergies are trialling remotely controlled robots for offshore inspections to cut human exposure and increase inspection frequency, signalling a wider move toward fully autonomous asset management.

Page last updated on: July 3, 2025