Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 680.85 Billion |

| Market Size (2031) | USD 830.62 Billion |

| Growth Rate (2026 - 2031) | 4.06% CAGR |

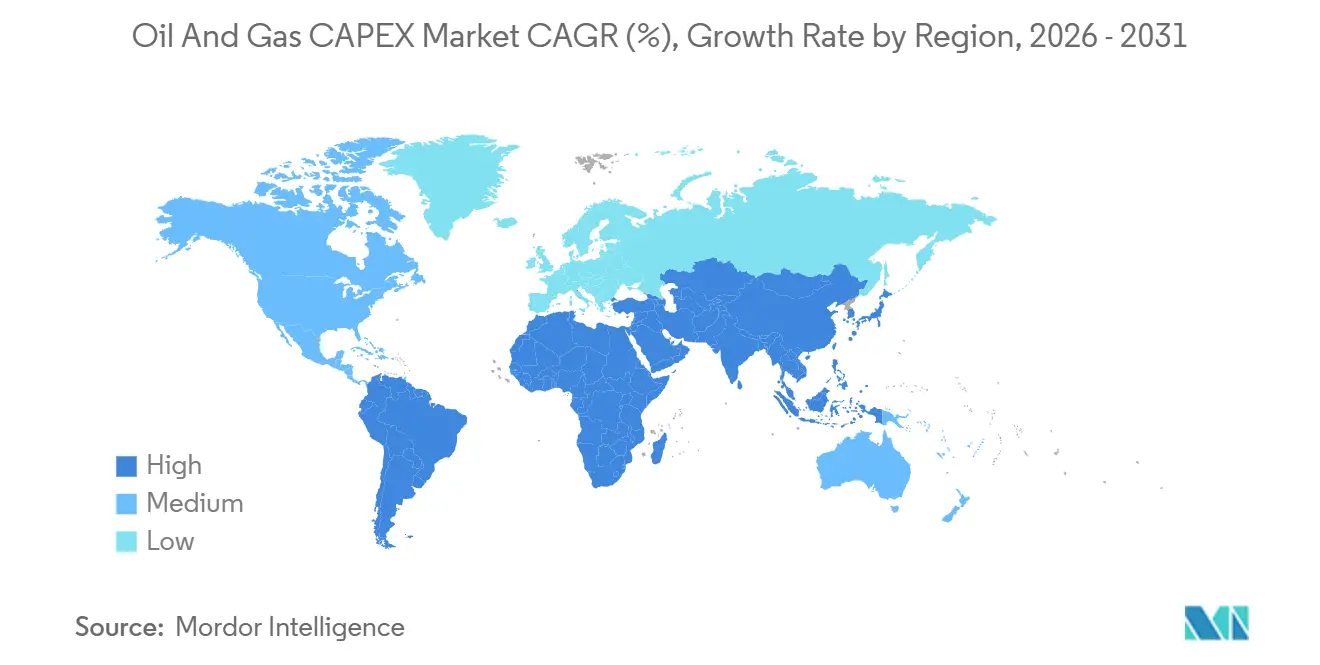

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oil And Gas CAPEX Market Analysis by Mordor Intelligence

The Oil And Gas CAPEX Market size is estimated at USD 680.85 billion in 2026, and is expected to reach USD 830.62 billion by 2031, at a CAGR of 4.06% during the forecast period (2026-2031).

State-backed operators in the Middle East and Asia are accelerating long-cycle investments even as OECD-based majors curb upstream budgets under tightening ESG covenants, creating a two-speed capital landscape. Deepwater final investment decisions (FIDs) that sanctioned 15 billion barrels of oil-equivalent reserves in 2024, together with modular floating LNG units, are compressing breakeven costs to USD 35-40 per barrel and sustaining offshore momentum. Onshore projects still command most spending, but standardized FPSO hulls, subsea tiebacks, and digital-twin workflows are redirecting incremental capital to offshore developments. Maintenance budgets for methane capture, electrification, and carbon-capture retrofits rival greenfield allocations, signaling a pivot from reserve replacement toward emissions-intensity mitigation.

Key Report Takeaways

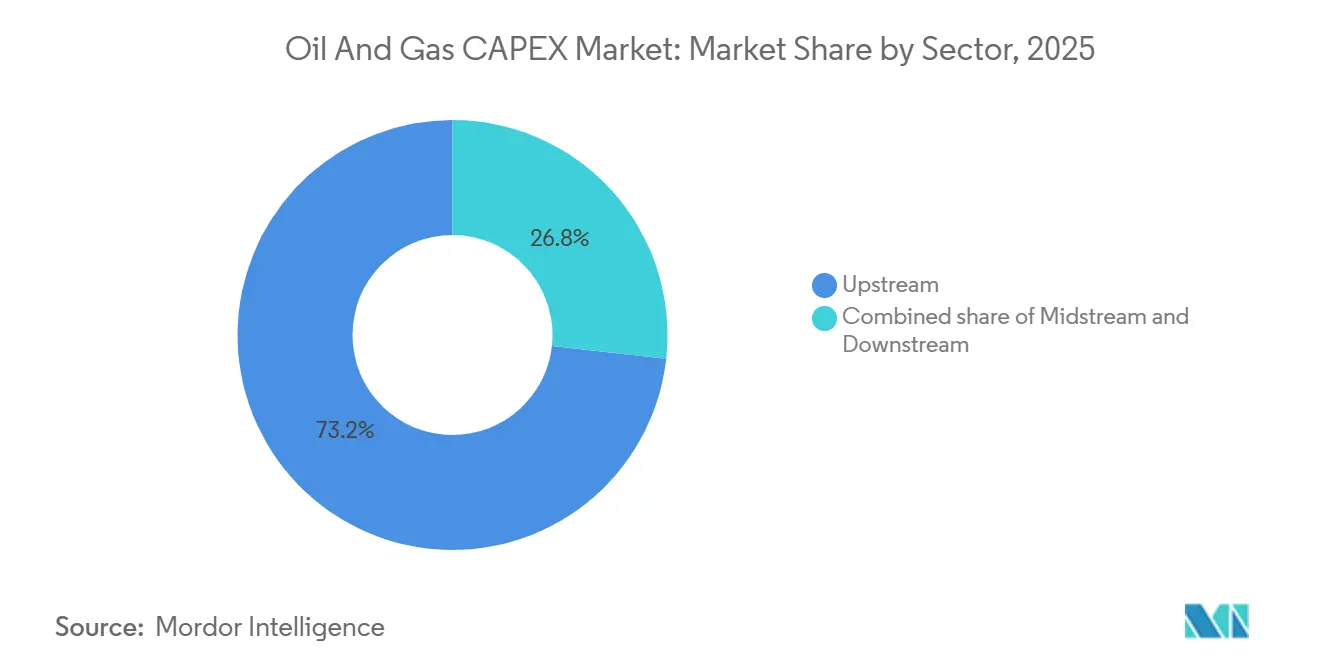

- By sector, upstream captured a 73.24% CAPEX oil & gas market share in 2025 and is forecast to expand at a 4.12% CAGR through 2031.

- By location, onshore projects held 79.43% of spending in 2025, while offshore is projected to grow at a 7.21% CAGR through 2031.

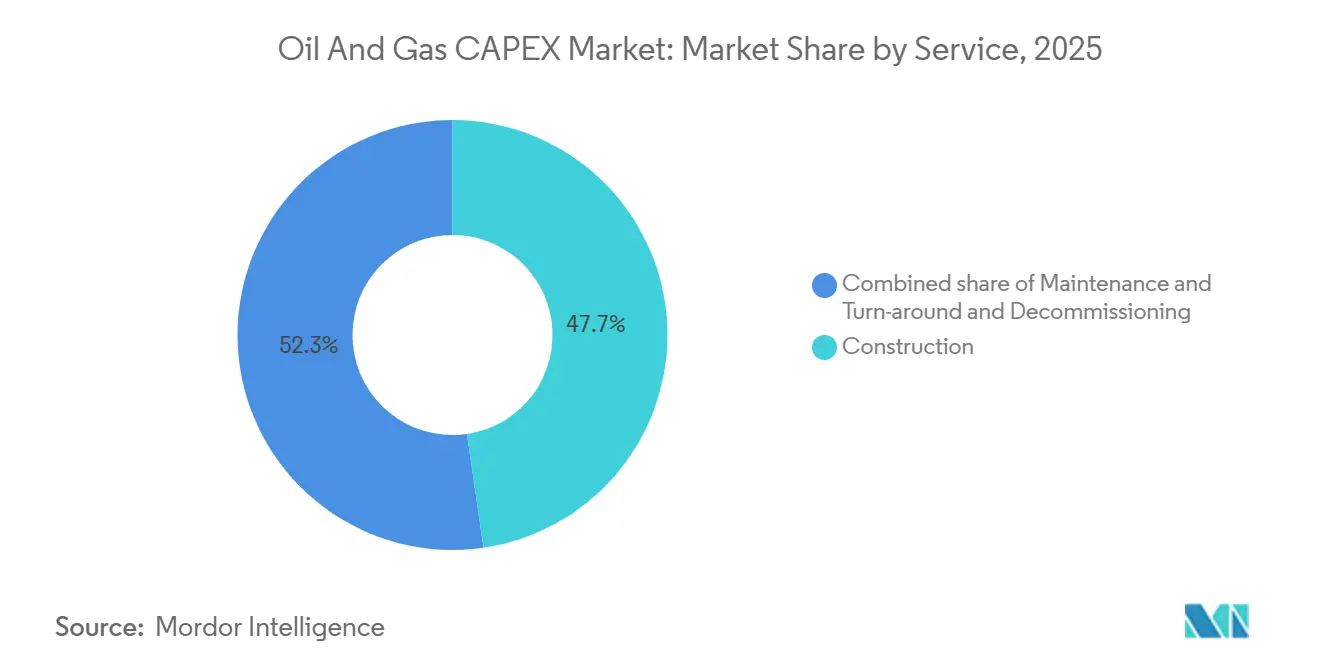

- By service, construction accounted for 47.70% of 2025 expenditure, whereas decommissioning is expected to register the fastest 6.55% CAGR to 2031.

- By geography, Asia-Pacific led with 29.36% of CAPEX in 2025; the region is set to advance at a 4.83% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Oil And Gas CAPEX Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing LNG-ready gas infrastructure build-out | +1.2% | Global, with concentration in US Gulf Coast, Qatar, Australia, Mozambique | Medium term (2-4 years) |

| Rising deepwater discoveries driving FIDs | +0.9% | South America (Brazil, Guyana, Suriname), West Africa (Angola, Nigeria), Asia-Pacific (Australia) | Long term (≥4 years) |

| NOC upstream spending rebound in Middle East & Asia | +1.1% | Middle East (Saudi Arabia, UAE, Qatar), Asia-Pacific (China, India, Malaysia) | Medium term (2-4 years) |

| Surge in maintenance CAPEX to decarbonise brownfields | +0.7% | North America, Europe (North Sea), Middle East mature fields | Short term (≤2 years) |

| Digital twin roll-outs cutting project overruns | +0.5% | Global, with early adoption in North America, Europe, Middle East NOCs | Short term (≤2 years) |

| Sub-1 MW modular FLNG attracting small-field sanctioning | +0.4% | Asia-Pacific (Southeast Asia, Papua New Guinea), West Africa, South America niche basins | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing LNG-Ready Gas Infrastructure Build-Out

IEA tracks 290 billion cubic meters per year of new liquefaction capacity slated for 2025-2030, underpinning a wave of midstream investment.[1]International Energy Agency, “Methane Tracker 2025,” iea.org ExxonMobil recommitted USD 30 billion to restart Mozambique LNG in 2026, while Woodside approved a USD 17.5 billion Louisiana export facility expected online in 2029.[2]Woodside Energy, “ASX Filing March 2025,” woodside.com Asian buyers continue to sign 15-20-year offtake agreements, de-risking project finance and enabling debt-to-equity ratios above 70:30. Lake Charles LNG reached mechanical completion in late 2025, adding 16.5 million tonnes per annum (mtpa) of nameplate capacity. Similar milestones at Plaquemines LNG tighten global supply-demand balances and sustain construction backlogs through decade-end.

Rising Deep-Water Discoveries Driving FIDs

Projects in water depths beyond 1,500 meters received FIDs covering 15 billion barrels of recoverable reserves during 2024-2025. Petrobras sanctioned Búzios 11 and Atapu 3 FPSOs, each rated for 180,000 barrels per day, leveraging standardized hulls that cut fabrication time by 18 months. Shell advanced Sparta in the US Gulf of Mexico at a USD 35 per barrel breakeven, and BP approved Kaskida using subsea boosting to extend plateau production by five years. TotalEnergies’ Kaminho project in Angola integrates subsea-to-shore power, eliminating platform-generator emissions. Guyana’s Whiptail and Hammerhead FPSOs will lift national capacity beyond 1.2 million barrels per day by 2027.

NOC Upstream Spending Rebound in Middle East & Asia

Saudi Aramco’s USD 50 billion 2024 budget prioritized Jafurah unconventional gas and offshore expansions aimed at displacing liquids in domestic power generation. Middle East upstream spend reached USD 130 billion in 2025 as the United Arab Emirates and Qatar scaled offshore capacity. PetroChina exceeded USD 60 billion in 2024 capital outlay, targeting tight-gas and South China Sea exploration, while CNOOC allocated USD 13-14 billion to offshore condensate and gas projects. India’s ONGC earmarked USD 8.6 billion across 2024-2025 for Krishna-Godavari developments and mature-field enhanced recovery.

Surge in Maintenance CAPEX to Decarbonize Brownfields

IEA estimates USD 600 billion will be spent through 2030 retrofitting methane-capture, electrification, and carbon-capture solutions on existing assets. NETL studies show post-combustion amine systems can be integrated at USD 80-100 per tonne of CO₂ when pipelines are nearby. Siemens Energy reports 15-20% emissions reductions after replacing diesel generators with shore-power or hybrid systems. Subsea compression in the North Sea is extending asset life by up to 15 years, deferring abandonment costs under stricter emissions benchmarks. The capital shift reduces reserve-replacement ratios but lengthens economic lives of mature basins under evolving disclosure frameworks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Dated Brent discouraging long-cycle projects | -0.8% | Global, with acute impact on frontier deepwater basins in West Africa, East Mediterranean | Medium term (2-4 years) |

| ESG-linked debt covenants capping fossil CAPEX ceilings | -0.6% | OECD markets (North America, Europe), with spillover to international project finance | Long term (≥4 years) |

| Policy pivots toward renewables in OECD | -0.5% | North America (selective), Europe (EU Green Deal jurisdictions), with spillover to international project finance | Long term (≥4 years) |

| Scarcity-pricing of Tier-1 EPC labour elevating costs | -0.6% | Global, with acute pressure in North America (Gulf Coast), Middle East (Qatar, UAE), Asia-Pacific fabrication hubs | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Volatility in Dated Brent Discouraging Long-Cycle Projects

Brent traded between USD 70 and USD 95 per barrel across 2024-2025, below breakevens for many frontier deepwater prospects, leading operators to defer 8-10 billion barrels of potential resources. Drilling costs above USD 150 million per well and 6-8-year timelines deter FIDs when forward curves flatten.[3]International Energy Agency, “World Energy Outlook 2025,” iea.org Independent E&P companies saw borrowing costs rise by up to 200 basis points, pushing hurdle rates to 15-18% IRR.[4]Financial Times, “Energy Finance Coverage 2025,” ft.com Capital is shifting to short-cycle shale and brownfield upgrades, potentially constraining global supply in the early 2030s if sanctioning does not rebound.

ESG-Linked Debt Covenants Capping Fossil CAPEX Ceilings

North American and European lenders embedded emissions-intensity tests into reserve-based lending structures, limiting the share of proceeds eligible for oil and gas spending. OECD fossil-fuel exploration subsidies fell 22% between 2023 and 2025, and private project finance dropped 18%. Shell, BP, and TotalEnergies cut collective oil and gas CAPEX by 12% in 2025 versus 2023 to meet net-zero pathways, redirecting funds to offshore wind and storage. Sustainability-linked loans now ratchet interest margins upward by 25-50 basis points when methane-intensity targets are missed, further steering capital to lower-carbon LNG projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Upstream Holds Dominance

Upstream captured a 73.24% share in 2025, and the CAPEX oil & gas market size for this segment is forecast to grow at a 4.12% CAGR through 2031. Deepwater FIDs totaling 15 billion barrels in 2024 across Brazil, the US Gulf of Mexico, Angola, and Guyana capitalize on standardized FPSO and subsea systems that reduce per-barrel costs. National oil companies are sustaining high spend levels, with Saudi Aramco, PetroChina, and CNOOC together exceeding USD 130 billion in combined upstream budgets during 2024.

Digital-twin platforms deliver 30-40% reductions in cost overruns, freeing capital for parallel projects and shortening schedules by up to 18 months. Midstream investment remains steady as hydrogen-ready pipelines and carbon-capture hubs secure US Department of Energy support. Downstream complexes in Asia and the Middle East integrate refining and petrochemicals to improve margins by 15-20% in response to declining OECD gasoline demand.

By Location: Offshore Momentum Builds

Onshore projects commanded 79.43% of 2025 expenditure, yet offshore CAPEX is set for a 7.21% CAGR to 2031 as the CAPEX oil & gas market size for deepwater projects grows faster than onshore equivalents. Shell’s Sparta and BP’s Kaskida use subsea boosting and tiebacks to existing infrastructure, cutting development costs 25-30%. New Fortress Energy’s small-scale FLNG fleet monetizes stranded reserves below 1 trillion cubic feet, supporting offshore gas monetization without new pipelines.

Onshore unconventional activity remains intense, with 12,000 wells drilled in the Permian during 2024 to sustain 6 million barrels per day of output. Canada invested USD 12 billion in oil sands expansions, while China’s Sichuan tight-gas program commands USD 15 billion annually. Decommissioning liabilities, £24 billion in the UK North Sea and 14,000 idle Gulf of Mexico structures, create a parallel offshore spend stream focused on safe retirement.

By Service: Decommissioning Leads Growth

Construction held 47.70% of 2025 expenditure, but decommissioning is projected to log a 6.55% CAGR, the highest among services within the CAPEX oil & gas market. Plug-and-abandonment costs ranging from USD 1.5-2.5 million per well in the Gulf of Mexico and escalating UK North Sea mandates underpin demand. Robotics-enabled abandonment rigs are reducing intervention time by 40%, attracting specialized contractors and fragmenting a space long dominated by integrated service providers.

Maintenance CAPEX for emissions retrofits totals USD 600 billion through 2030, compelling service firms to scale electrification, methane-capture, and CO₂-sequestration offerings. Simultaneously, liquefaction megaprojects in Qatar, the US Gulf Coast, and Mozambique account for individual construction packages exceeding USD 20 billion, preserving a robust backlog for civil, mechanical, and module-assembly contractors.

Geography Analysis

Asia-Pacific captured 29.36% of 2025 spending, and the CAPEX oil & gas market size in the region is forecast to grow at a 4.83% CAGR to 2031. PetroChina’s USD 60 billion annual budget and CNOOC’s USD 13-14 billion offshore program underpin tight-gas and condensate growth targets. India’s ONGC invests USD 8.6 billion in Krishna-Godavari assets and plans 10 mtpa of new regasification capacity by 2030. Woodside’s Scarborough and Browse LNG projects add 13 mtpa of capacity, while Papua New Guinea and Vietnam develop integrated gas-to-power schemes.

North America and Europe together accounted for roughly 35% of 2025 CAPEX but recorded slower growth as institutional capital pivots toward renewables. The United States maintains leadership through 12,000 Permian wells and 27.5 mtpa of new LNG capacity at Woodside, Louisiana, and Lake Charles. Canada’s USD 12 billion oil-sands expansions prioritize 30-year SAGD projects. European majors trimmed oil and gas CAPEX 12% in 2025 to fund offshore wind and batteries, yet Equinor sanctioned Johan Castberg, showing selective approval for high-return Norwegian Barents projects.

The Middle East and Africa hold near-25% of global spending. Saudi Aramco’s USD 50 billion program boosts unconventional and offshore capacity, while QatarEnergy’s North Field expansion adds 48 mtpa of LNG by 2027. Angola’s Kaminho and Brazil’s Búzios 11 demonstrate deepwater momentum, complemented by Guyana’s additional FPSOs raising capacity above 1.2 million barrels per day.

Competitive Landscape

Integrated majors and large NOCs account for about 40% of global upstream CAPEX, evidencing moderate concentration in core segments. Saudi Aramco, ExxonMobil, Shell, BP, TotalEnergies, and Chevron leverage balance-sheet strength and engineering scale to secure fabrication slots and negotiate favorable equipment terms. Middle Eastern and Asian NOCs expand upstream budgets by double digits to meet domestic energy-security mandates, offsetting Western capital retreat. Service giants SLB, Halliburton, and Baker Hughes pivot toward digital and emissions-reduction solutions, deploying digital-twin platforms that cut overruns up to 40%.

OECD majors trimmed oil and gas spending by 12% in 2025, reallocating to renewables, while Aramco, PetroChina, and CNOOC raised upstream budgets by 18%, endorsing long-cycle assets with 20-year paybacks. Technology adoption, digital twins, subsea boosting, and modular FLNG reduce per-barrel costs by 15-25%, becoming a key differentiator. Decommissioning invites new entrants with robotics and autonomous inspection, fragmenting a niche historically dominated by integrated service providers.

Oil And Gas CAPEX Industry Leaders

Saudi Aramco

PetroChina (CNPC)

Exxon Mobil Corporation

Shell plc

Chevron Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Tourmaline Oil Corp. announced two acquisitions in the NEBC Montney area, which are expected to add approximately 20,000 boepd of production and 369.4 million barrels of oil equivalent (mmboe) of reserves.

- April 2025: Oil States International reported its strongest backlog since 2015 at USD 357 million, driven by a USD 25 million contract for a deepwater production facility in Brazil. The company generated USD 9 million in cash flow from operations, reversing a previous trend of negative cash flow.

- April 2025: Chevron commenced oil and natural gas production from the Ballymore subsea tieback in the Gulf of America, targeting 300,000 net barrels per day by 2026 with estimated recoverable resources of 150 million barrels of oil equivalent.

- November 2024: EQT Corp. announced a USD 1.8 billion acquisition of Olympus Energy Holdings, adding 500 MMscf/D production capacity and 90,000 net acres in Pennsylvania's Marcellus and Utica shale plays.

Global Oil And Gas CAPEX Market Report Scope

Capital expenditure (CAPEX) is the funds used by a company/organization to acquire, upgrade, and maintain physical assets, such as property, plants, buildings, technology, or equipment. CAPEX is often used to undertake new projects or investments by a company. The global oil and gas CAPEX market considers the total capital expenditure of oil and gas operators worldwide annually. The CAPEX/investments in the upstream, midstream, and downstream oil and gas projects across different regions are taken into consideration while estimating the market size.

The CAPEX oil & gas market is segmented by sector, location, service, and geography. By sector, the market is segmented into upstream, midstream, and downstream. By location, the market is segmented into onshore and offshore. By service, the market is segmented into construction, maintenance and turn-around, and decommissioning. The report also covers the market sizes and forecasts for the CAPEX oil & gas market across major countries within each region. For each segment, market sizing and forecasts are provided on the basis of value (USD).

By Sector

| Upstream |

| Midstream |

| Downstream |

By Location

| Onshore |

| Offshore |

By Asset Type

| Construction |

| Maintenance and Turn-around |

| Decommissioning |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Norway |

| United Kingdom | |

| Russia | |

| Netherlands | |

| Germany | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Nigeria | |

| South Africa | |

| Rest of Middle East and Africa |

| By Sector | Upstream | |

| Midstream | ||

| Downstream | ||

| By Location | Onshore | |

| Offshore | ||

| By Asset Type | Construction | |

| Maintenance and Turn-around | ||

| Decommissioning | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Norway | |

| United Kingdom | ||

| Russia | ||

| Netherlands | ||

| Germany | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the CAPEX oil & gas market in 2026?

The CAPEX oil & gas market size is USD 680.85 billion in 2026 and is set to reach USD 830.62 billion by 2031 at a 4.06% CAGR.

Which segment holds the highest spend share?

Upstream operations account for 73.24% of 2025 spending and are projected to grow at 4.12% through 2031.

Where is CAPEX growing fastest geographically?

Asia-Pacific leads growth with a 4.83% CAGR to 2031, driven by elevated NOC budgets and LNG infrastructure build-outs.

Why is decommissioning attracting attention?

Regulatory mandates in the Gulf of Mexico and UK North Sea, plus 14,000 idle structures, are pushing decommissioning to a 6.55% CAGR by 2031.

How are digital twins impacting project economics?

Operators report 30-40% fewer cost overruns and the ability to redeploy freed capital, shortening schedules by up to 18 months.

Page last updated on: