Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

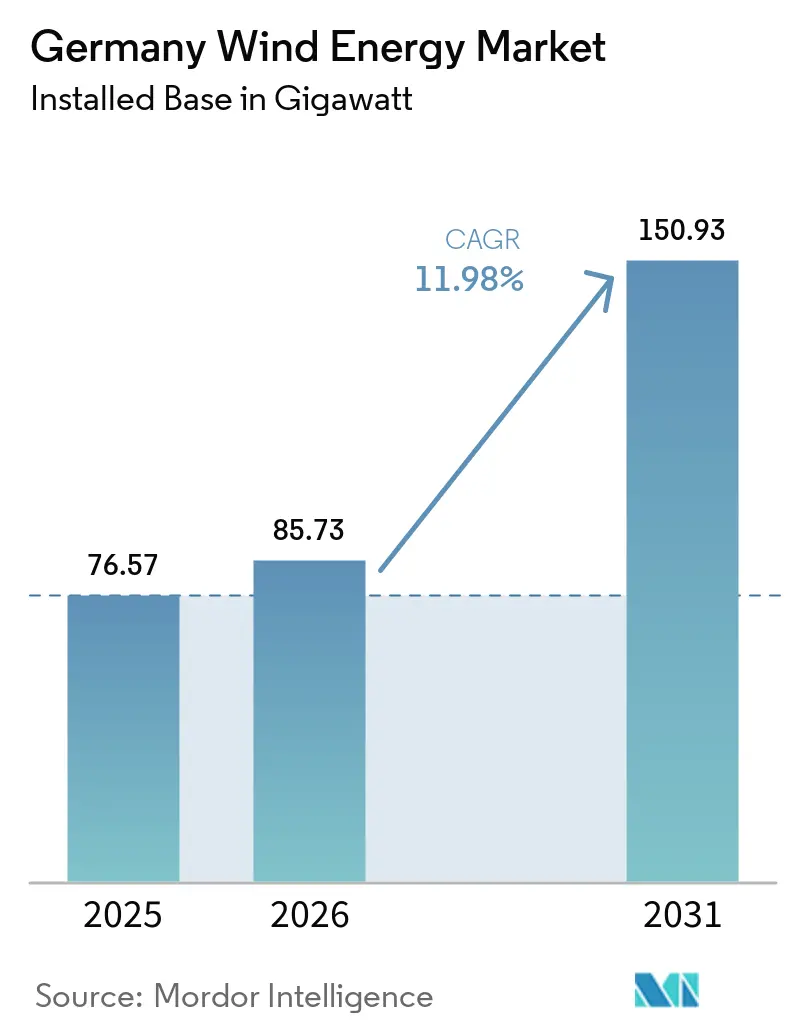

| Base Year Market Size (2025) | 76.57 gigawatt |

| Market Volume (2026) | 85.73 gigawatt |

| Market Volume (2031) | 150.93 gigawatt |

| Growth Rate (2026 - 2031) | 11.98% CAGR |

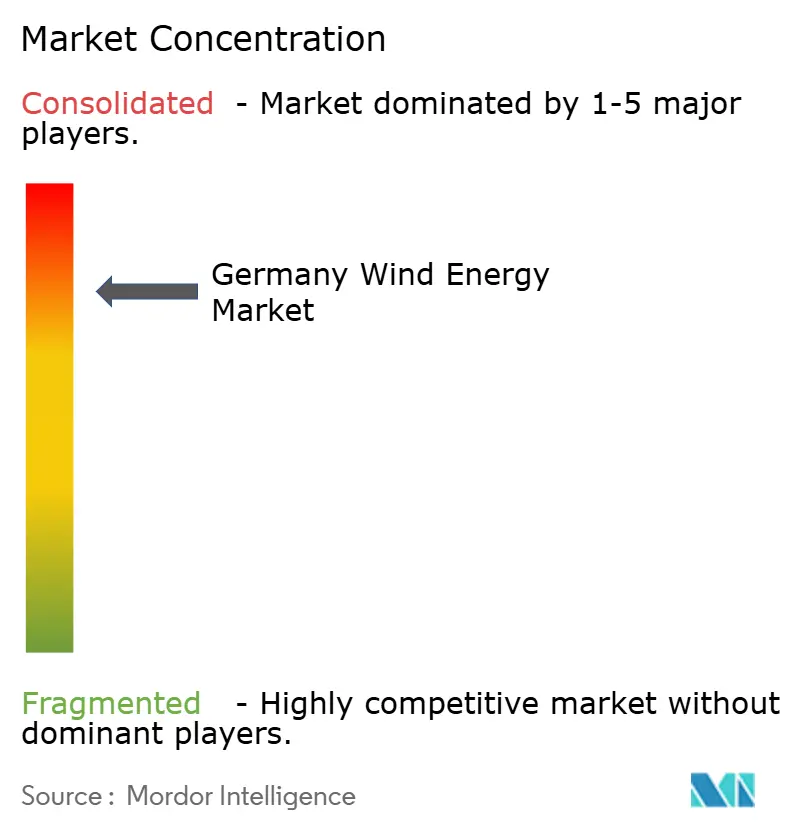

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Wind Energy Market Analysis by Mordor Intelligence

The Germany Wind Energy Market size is expected to grow from 76.57 gigawatt in 2025 to 85.73 gigawatt in 2026 and is forecast to reach 150.93 gigawatt by 2031 at 11.98% CAGR over 2026-2031.

Uptake is propelled by binding federal targets of 115 GW onshore and 30 GW offshore capacity, streamlined permitting, and a surge in corporate power-purchase agreements. Record approvals of 2,400 turbines totaling 14 GW in 2024 underscore how the policy mix shortens project pipelines while creating a two-year lag between licensing and grid connection. Offshore projects benefit from cost-curbing technology such as 15 MW turbines, while repowering raises site productivity by up to fivefold. Rising HVDC links curb curtailment risks, yet grid constraints and supply-chain exposure to Asia moderate near-term build-out.

Key Report Takeaways

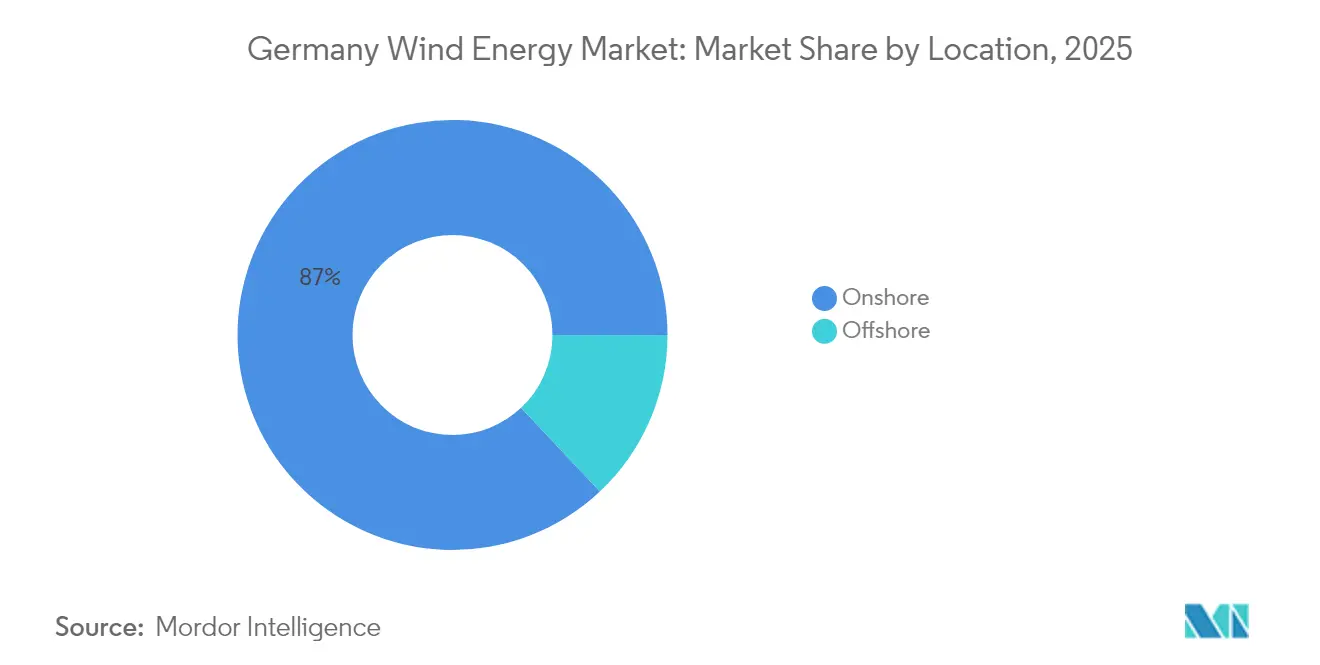

- By location, onshore installations led with 87.02% of Germany's wind energy market share in 2025; offshore capacity is forecast to expand at 20.7% CAGR through 2031.

- By turbine capacity, the above 6 MW class accounted for 64.05% share of the German wind energy market size in 2025, and the same is projected to grow at 13.05% CAGR between 2026-2031.

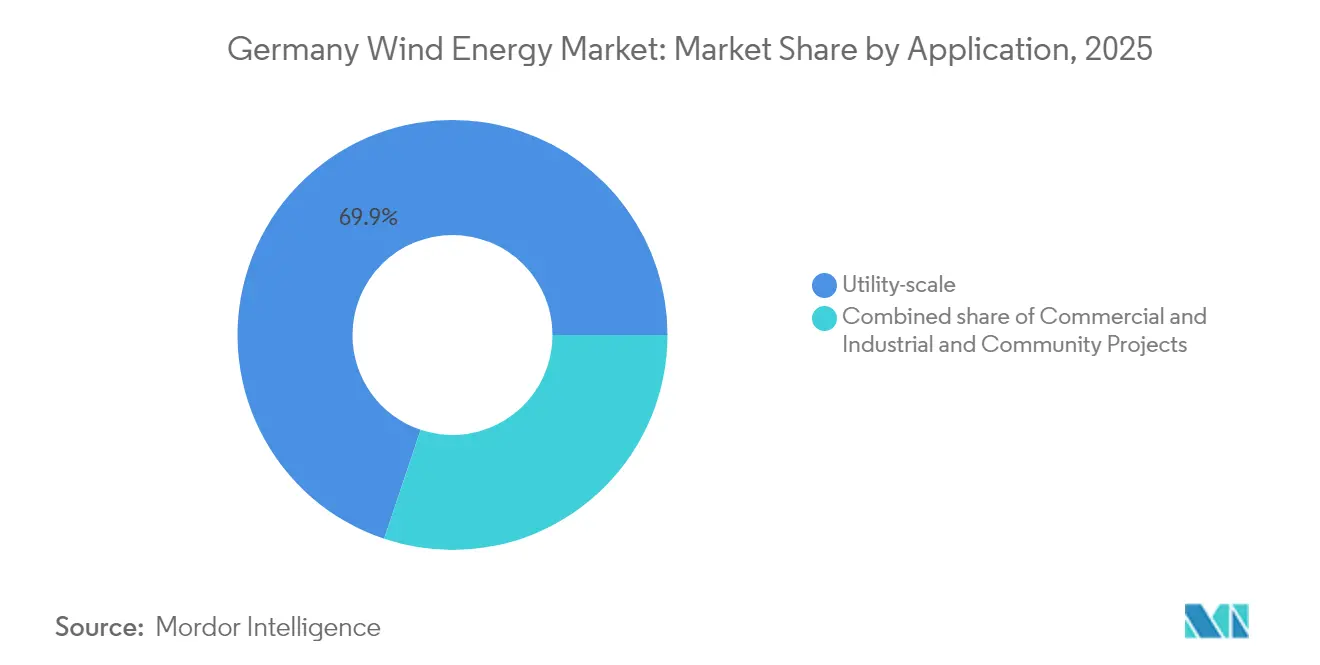

- By application, utility-scale projects commanded 69.85% of German's wind energy market share in 2025, while community projects are forecast to expand at a 15.95% CAGR to 2031.

- By manufacturer, Vestas, Nordex, and Enercon together captured 91.2% market share in European onshore additions in 2025, with Vestas alone installing 1,479.7 MW in Germany.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Wind Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal 115 GW onshore & 30 GW offshore targets (2030) | +2.5% | National, with concentration in Schleswig-Holstein, Lower Saxony, Mecklenburg-Vorpommern, North Sea, Baltic Sea | Long term (≥ 4 years) |

| Streamlined permitting & Wind-an-Land Act | +2.0% | National, priority zones in northern and eastern Länder | Medium term (2-4 years) |

| Corporate PPAs + green-hydrogen demand pull | +1.8% | National, industrial clusters in North Rhine-Westphalia, Hamburg, Bremen | Medium term (2-4 years) |

| Repowering of >15-yr turbines boosts MW additions | +1.5% | National, legacy sites in Lower Saxony, Brandenburg, Saxony-Anhalt | Short term (≤ 2 years) |

| HVDC offshore grid & North Sea interconnectors | +1.2% | Offshore zones, North Sea, Baltic Sea, grid corridors to Bavaria, Baden-Württemberg | Long term (≥ 4 years) |

| Citizen-energy revenue-sharing schemes | +0.8% | National, rural municipalities in onshore wind regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Federal 115 GW Onshore & 30 GW Offshore Targets Drive Market Acceleration

Binding 2030 capacity goals translate into annual additions of 7.7 GW onshore and 4 GW offshore, a step-change from 2024’s 2.5 GW net onshore increase. Developers with shovel-ready projects and secured interconnection spots gain a first-mover advantage. Offshore ambitions triple present capacity, forcing unprecedented coordination between grid operators and project sponsors. TenneT’s North Sea links already move 8.03 GW, yet expansion to 70 GW by 2045 requires 35 HVDC corridors that are now entering the tender phase.[1]TenneT, “North Sea Grid Expansion Milestones,” tennet.eu

Streamlined Permitting & Wind-an-Land Act Reduce Development Friction

Permitting reforms lifted 2024 approvals 85% year-on-year to 14 GW, cutting bureaucratic hurdles for small and mid-sized developers. Federal states must zone 2% of land for wind by 2027-2032, guaranteeing spatial certainty. North Rhine-Westphalia licensed 1.5 GW in Q1-2025 alone, illustrating rapid uptake. Yet average construction lead time still exceeds two years, meaning the bulk of new capacity flows into the 2026-2028 window.

Corporate PPAs & Green Hydrogen Create New Revenue Streams

Corporate PPAs rose 323% in 2023 as firms hedge power price volatility and pursue Scope 2 decarbonization. BASF’s long-term offtake from Vattenfall’s 1.6 GW Nordlicht project highlights how industrial loads anchor offshore finance. Demonstration projects such as a 10 MW offshore electrolyzer at Alpha Ventus point to integrated wind-to-hydrogen value chains that increase electricity offtake certainty for developers.

Repowering of >15-Year Turbines Amplifies Capacity Additions

Repowering contributed 37% of 2024 onshore growth as first-generation 2 MW turbines give way to 6 MW models on identical sites. Schleswig-Holstein alone has 3,190 permitted turbines totaling 8.9 GW awaiting upgrade, offering a rapid capacity lift without new land take. Streamlined repowering rules shorten timelines and improve community acceptance by replacing older, noisier models with fewer high-output units.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid bottlenecks & curtailment risk | -1.5% | Schleswig-Holstein, Lower Saxony, Mecklenburg-Vorpommern, offshore zones | Medium term (2-4 years) |

| Dependency on Asian turbine supply chains | -0.8% | National, affects all OEMs and developers | Short term (≤ 2 years) |

| Local opposition & litigation delays | -1.0% | Bavaria, Baden-Württemberg, Hesse, rural municipalities | Medium term (2-4 years) |

| Skilled-labour shortage for offshore O&M | -0.7% | Offshore zones, North Sea, Baltic Sea, coastal service hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid Bottlenecks & Curtailment Risk Constrain Output Optimization

Nineteen TWh of wind power were curtailed in 2023, equal to 13% of total generation, due to limited north-to-south transmission. Federal approval of five major AC corridors will ease congestion, but completion dates after 2027 leave near-term earnings exposed. Offshore generation compounds the issue as North Sea output surges ahead of onshore grid reinforcements.

Dependency on Asian Supply Chains Creates Strategic Vulnerabilities

Nordex’s closure of its Rostock blade plant and the growing reliance on Asian rare-earth and electronics suppliers expose the German wind energy industry to geopolitical shocks. Long lead times for nacelle bearings and power converters pose schedule risks for large offshore turbines, while cybersecurity scrutiny of imported control systems adds compliance complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location: Onshore Remains the Anchor, Offshore Is the Engine of Acceleration

Onshore assets supplied 87.02% of the German wind energy market size in 2025, yet offshore projects grow at a 20.7% CAGR through 2031. Schleswig-Holstein, Lower Saxony, and Mecklenburg-Vorpommern host two-thirds of installed capacity, benefiting from 7-8 m/s winds at 100 m hub height and early zoning. Fixed-bottom foundations in 30–50 m depths cost EUR 1.5-2 million per turbine, well below floating alternatives, giving the German wind energy market strong cost signals to push near-shore sites first.

Offshore capacity rises from 10.03 GW in 2025 to 33.58 GW in 2031 as the German Bight and Pomeranian Bay absorb 7 GW of 2024 auction awards. Capacity factors above 50% and zero-subsidy economics improve project finance leverage ratios. Onshore growth hinges on repowering in Lower Saxony and Brandenburg, where three 2 MW turbines give way to one 6 MW unit, freeing rotor-swept area while recycling foundations. This dual-track expansion keeps the German wind energy industry resilient to site scarcity.

By Turbine Capacity: Above-6 MW Class Dominates New Orders

Turbines above 6 MW held 64.05% of 2025 installations and expanded at a 13.05% CAGR to 2031, reflecting OEM roadmaps to 15 MW offshore and 7 MW onshore models. One V236-15 MW machine produces 80 GWh annually, allowing 400 MW farms to use fewer than thirty turbines and reducing foundation count by 40%, an efficiency prized across the German wind energy market.

The 3-6 MW band serves repowering sites where crane access and permitting cap turbine height. Sub-3 MW units represent less than 10% of orders and exit the market once FIT contracts expire. Modular nacelles, carbon-fiber blades, and predictive maintenance shift value from hardware to software, an evolution shaping the German wind energy industry as a technology platform.

By Application: Utility-Scale Leads, Community Projects Accelerate

Utility-scale parks above 100 MW held 69.85% of 2025 deployments and use EUR 200–300 per kW cost advantages to dominate tender rounds. Projects over 500 MW require dedicated HVDC links to bypass congested AC corridors, a bottleneck relieved once SuedLink starts service in 2028.

Community projects add 15.95% CAGR through 2031 as EEG 2023 revenue sharing pays municipalities directly. Cooperatives own up to 49% equity and distribute 4-5% annual dividends, halving permit appeals in pilot regions. C&I on-site parks remain below 5% share but grow as data centers and chemical hubs hedge volatile grid prices, diversifying the German wind energy market.

Geography Analysis

Northern Länder house 65% of installed capacity because of strong winds and early zoning. Schleswig-Holstein ran 9 GW onshore and 3 GW offshore in 2024, generating 22 TWh, 150% of local demand. Offshore expansion grows at 20.7% CAGR as 7 GW of 2024 seabed rights concentrate in the German Bight (4 GW) and Pomeranian Bay (3 GW). TenneT plans 12 GW of offshore grid capacity by 2032, each 2 GW link costing EUR 2.5-3.0 billion, reducing curtailment across the German wind energy market.

Southern states hold only 15% of capacity yet consume 40% of electricity, causing EUR 3.2 billion redispatch in 2024. Bavaria’s 10H rule freezes 2-3 GW of projects while federal overrides pushed 600 MW through in 2024. SuedLink and SuedOstLink HVDC add 4 GW north-south transfer by 2030, enabling 5 GW lignite retirement and balancing the German wind energy market.

Eastern Länder are repowering hubs, with 1.5 GW of legacy turbines scheduled for 5-6 MW replacements by 2027. Existing grid connections expedite upgrades, tripling output without new land. These patterns create a polarized yet complementary geography that underpins the German wind energy market size expansion.

Competitive Landscape

Germany Wind Energy Market is semi-consolidated. Siemens Gamesa’s integration into Siemens Energy transfers scale efficiencies but exposes the parent to warranty liabilities after gearbox defects triggered EUR 800 million provisions. Vestas leads the above-15 MW offshore class with the V236 platform, and Nordex capitalizes on 6 MW modular machines optimized for repowering forest sites.

Offshore development is more consolidated. RWE, Ørsted, and EnBW control 3.5 GW of operating capacity and 4 GW under construction, leveraging vertical integration from seabed leasing to 20-year service contracts. These players signed 1.2 GW of corporate PPAs in 2024 to hedge merchant volatility, an approach that shapes capital allocation within the German wind energy market.

OEMs extend reach by buying service specialists. Siemens Gamesa paid EUR 300 million for Deutsche Windtechnik’s offshore unit, adding a 1.5 GW backlog and fifteen-year annuity contracts. Emerging disruptors like ABO Energy and PNE target 10-50 MW brownfield projects, exploiting incumbent focus on gigawatt-scale assets and delivering 15-20% internal rates of return.[4]ABO Energy, “Company Presentation 2024,” aboenergy.de Technology edges narrow, shifting competition toward supply-chain resilience, lead-time reliability, and compliance with IEC 61400 type-certification, now mandatory for turbines above 3 MW.

Declining equity returns now at 7-9% for onshore push developers toward hybrid wind-solar-storage clusters and green-hydrogen offtake to supplement revenue. Market barriers include rare-earth supply risks and offshore labor gaps, yet scale integration keeps the German wind energy market attractive to global infrastructure funds seeking predictable yields.

Germany Wind Energy Industry Leaders

Enercon GmbH

Nordex SE

Siemens Gamesa Renewable Energy, S.A.

Vestas Wind Systems A/S

GE Vernova (GE Renewable Energy)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Germany's Federal Network Agency (BNetzA) launched its third onshore wind tender of the year, aiming to allocate support for a capacity of 3.44 GW. To qualify, projects must obtain permits under the Federal Immission Control Act (BImSchG). The cap for bids is set at EUR 0.0735 (USD 0.086) per kWh.

- June 2025: Vestas clinched its largest-ever order for V172-7.2 MW wind turbines from ENERTRAG, securing a total of 115 MW across two projects in Brandenburg, Germany.

- April 2025: Iberdrola has partnered with Kansai, Japan's second-largest electricity provider and a major player in Asia, to jointly invest in the 315 MW Windanker offshore wind farm in Germany's Baltic Sea.

- March 2025: Vattenfall's Nordlicht 1 offshore wind project placed a firm order with Vestas for 68 V236-15.0 MW wind turbines. The total order for Nordlicht 1 stands at 1,020 MW, featuring a grid connection capacity of 980 MW. Additionally, there's an extra 40 MW capacity, optimizing the use of the connection.

Germany Wind Energy Market Report Scope

Wind power is made by the force of the wind, mostly through the rotor, which turns kinetic energy into mechanical energy, and the generator, which turns this mechanical energy into electrical energy.

The German wind energy market is segmented by Location (Onshore, Offshore), by Turbine Capacity (Up to 3 MW, 3 to 6 MW, Above 6 MW), by Application (Utility-scale, Commercial and Industrial, Community Projects), by Component (Qualitative Analysis) (Nacelle/Turbine, Blade, Tower, Generator and Gearbox, Balance-of-System). For each segment, the market sizing and forecasts have been done based on installed capacity (GW).

By Location

| Onshore |

| Offshore |

By Turbine Capacity

| Up to 3 MW |

| 3 to 6 MW |

| Above 6 MW |

By Application

| Utility-scale |

| Commercial and Industrial |

| Community Projects |

By Component (Qualitative Analysis)

| Nacelle/Turbine |

| Blade |

| Tower |

| Generator and Gearbox |

| Balance-of-System |

| By Location | Onshore |

| Offshore | |

| By Turbine Capacity | Up to 3 MW |

| 3 to 6 MW | |

| Above 6 MW | |

| By Application | Utility-scale |

| Commercial and Industrial | |

| Community Projects | |

| By Component (Qualitative Analysis) | Nacelle/Turbine |

| Blade | |

| Tower | |

| Generator and Gearbox | |

| Balance-of-System |

Key Questions Answered in the Report

How large will German wind capacity be in 2031?

The Germany wind energy market is forecast to reach 150.93 GW of cumulative capacity by 2031.

Which segment grows fastest to 2031?

Offshore wind leads with a 20.7% CAGR through 2031, adding scale in the North Sea and Baltic Sea.

Why are above-6 MW turbines favored?

Larger turbines reduce foundations, cables, and crane lifts, cutting installed costs by EUR 200–300 per kW and boosting capacity factors.

How do community projects overcome local opposition?

EEG 2023 mandates pay municipalities EUR 0.002 per kWh and allow cooperatives up to 49% equity, aligning local financial interests with project success.

What role do HVDC links play?

2 GW SuedLink and SuedOstLink corridors transfer 15–20 TWh per year southward, reducing curtailment and balancing regional supply.

How concentrated is turbine supply?

Siemens Gamesa, Vestas, Enercon, and Nordex supplied 75% of 2024 turbines, indicating moderate concentration in the supplier base.

Page last updated on: