Germany Data Center Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

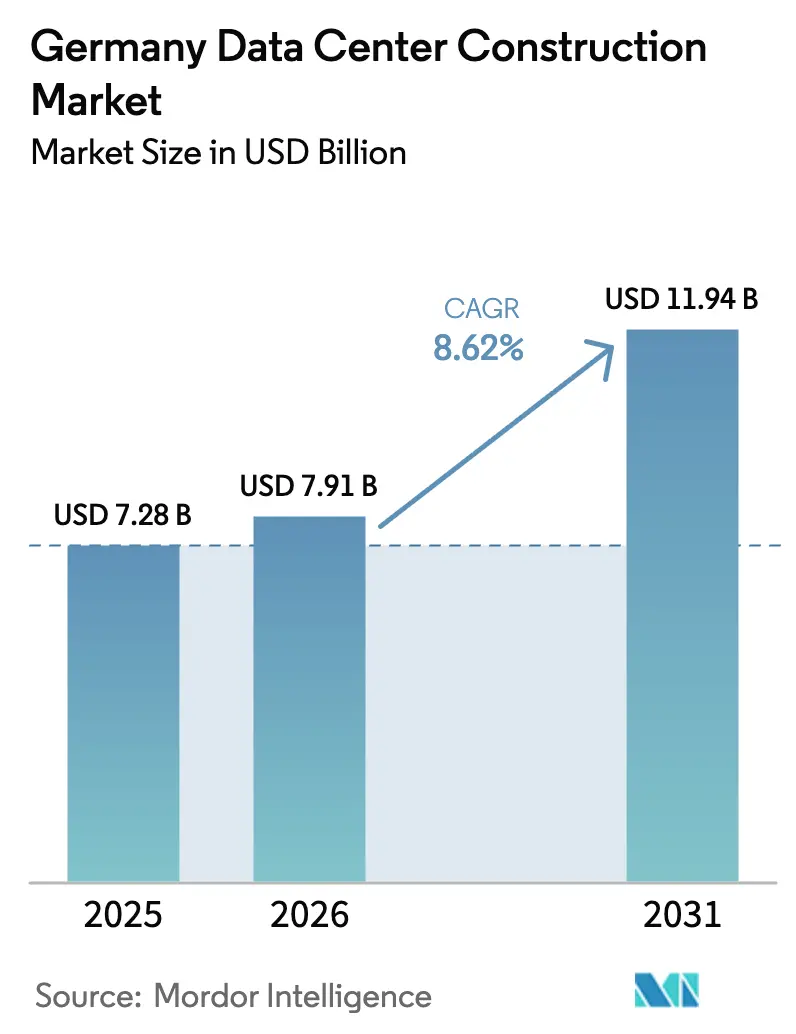

| Base Year Market Size (2025) | USD 7.28 Billion |

| Market Size (2026) | USD 7.91 Billion |

| Market Size (2031) | USD 11.94 Billion |

| Growth Rate (2026 - 2031) | 8.62% CAGR |

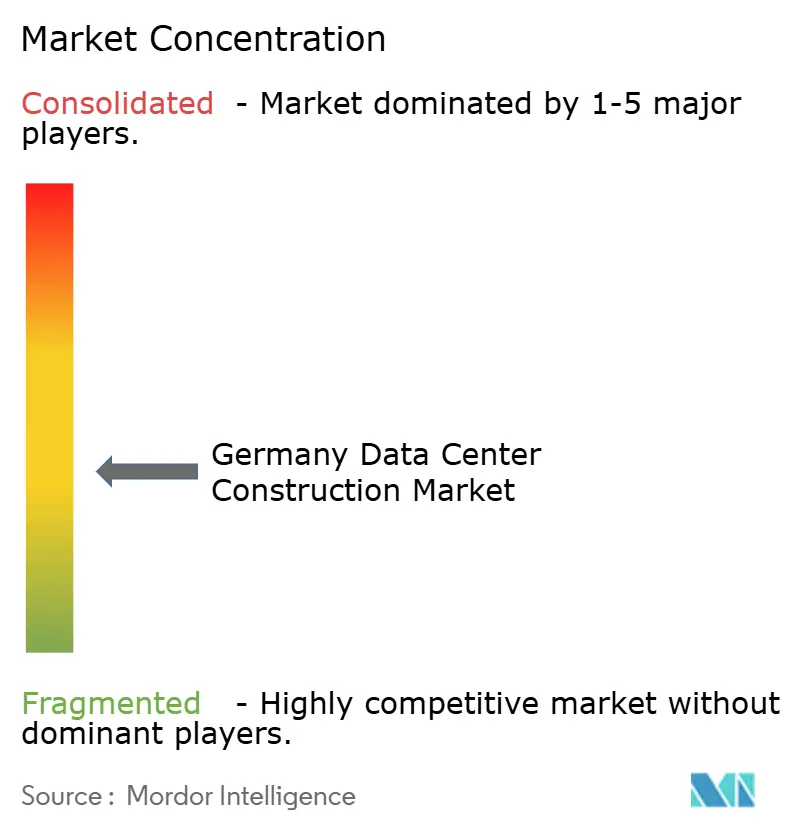

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Data Center Construction Market Analysis by Mordor Intelligence

The Germany data center construction market size was valued at USD 7.28 billion in 2025 and estimated to grow from USD 7.91 billion in 2026 to reach USD 11.94 billion by 2031, at a CAGR of 8.62% during the forecast period (2026-2031). Frankfurt anchors most hyperscale projects, yet regulatory pressure to improve energy efficiency and adopt ≥50% renewable power is driving advanced design and retrofit spending. Rising AI rack densities and liquid-cooling adoption are reshaping electrical and mechanical specifications, favoring builders that can standardize high-density modules. Material cost inflation—steel up 40.4% and glass up 49.3% since 2022—adds to project risk but has not slowed multi-billion-euro commitments from AWS, Microsoft, and other hyperscalers. Grid-capacity reallocation policies are opening Berlin, Munich, and Hamburg to large-scale builds as Frankfurt’s 110 kV network reaches saturation

Key Report Takeaways

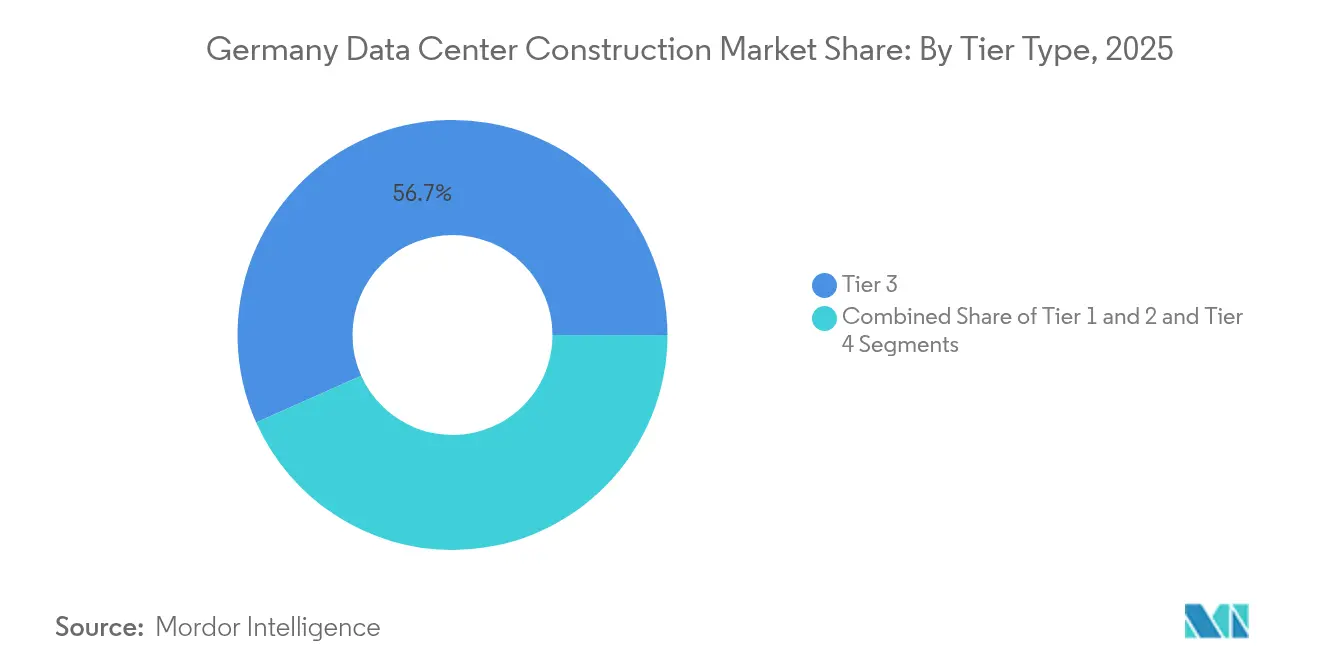

- By tier type, Tier 3 facilities accounted for 56.68% of the Germany data center construction market share in 2025, while Tier 4 projects are advancing at an 10.74% CAGR through 2031 U.S. Department of Commerce.

- By data-center type, colocation sites held 48.65% revenue in 2025; self-build hyperscale campuses are growing fastest at 11.87% CAGR to 2031 Data Center Dynamics.

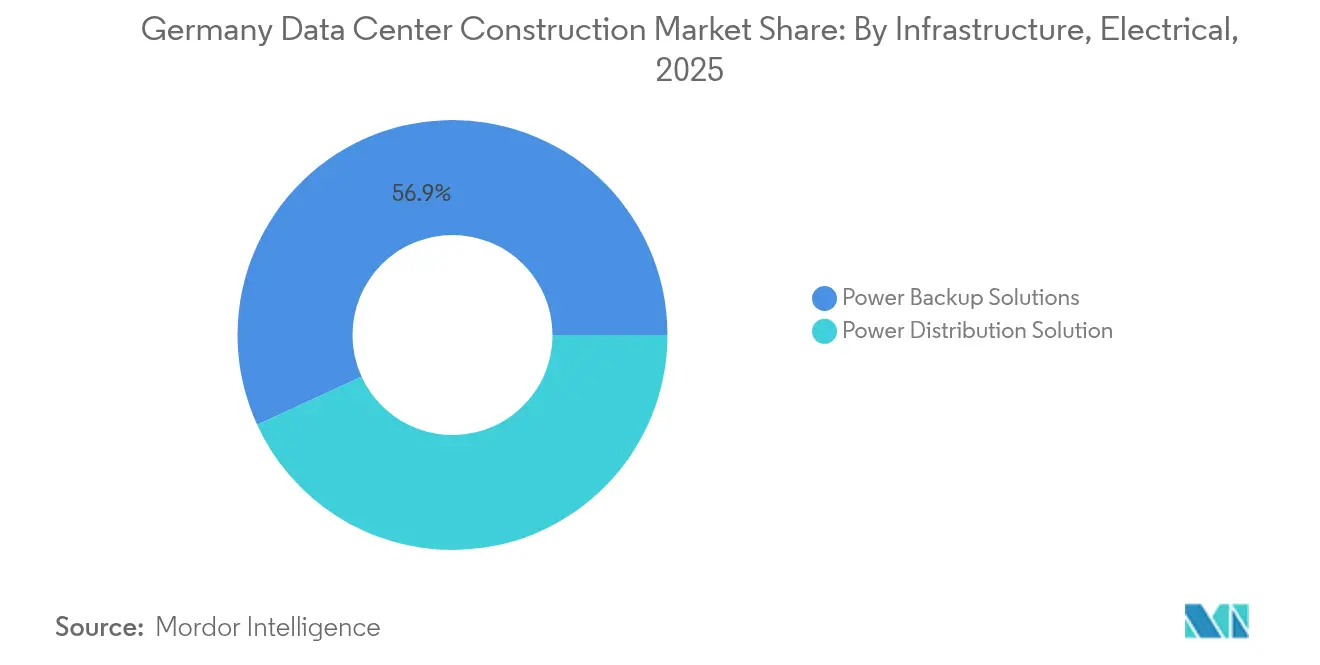

- By electrical infrastructure, power-backup systems commanded 56.85% share in 2025, while power-distribution solutions are forecast to lead growth at 12.71% CAGR Siemens.

- By mechanical infrastructure, cooling systems held 46.92% of the Germany data center construction market size in 2025, yet servers and storage integration is expanding at 12.22% CAGR Supermicro.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Data Center Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale cloud capex boom fuels multi-GW build-outs | 2.8% | Frankfurt, Berlin, Munich | Medium term (2-4 years) |

| AI/ML rack-density shift (>80 kW/rack) accelerates liquid-cooling projects | 2.1% | National, concentrated in Frankfurt | Short term (≤ 2 years) |

| Mandatory 50% renewable-power requirement under EnEfG drives retrofit spending | 1.4% | National | Medium term (2-4 years) |

| Grid-capacity re-allocation scheme opens secondary metros | 1.2% | Berlin, Munich, Hamburg, Düsseldorf | Long term (≥ 4 years) |

| Waste-heat purchase incentives (up to EUR 180/MWh) spur heat-re-use infrastructure | 0.8% | Frankfurt, Berlin, Munich | Long term (≥ 4 years) |

| On-site H₂ fuel-cell pilots cut diesel-backup OPEX in Tier 3/4 builds | 0.4% | National, early adoption in Frankfurt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyperscale Cloud Capex Boom Fuels Multi-GW Build-outs

Hyperscale operators are redefining the Germany data center construction market through record capital deployment. AWS committed USD 9.44 billion to multiple Frankfurt-area campuses designed for gigawatt-scale loads and 18-24 month delivery timetables,[1]AWS Press Office — "AWS to Invest USD 9.44 Billion in Frankfurt Cloud Region," DataCenterDynamicscatalyzing demand for prefabricated modules and concurrent permitting. Microsoft followed with a EUR 3.2 billion (USD 3.6 billion) expansion that doubles national AI capacity and specifies racks above 40 kW. Multi-building scheduling favors firms that can coordinate parallel crews and logistics across dispersed plots, while smaller regional contractors risk displacement. Accelerated timelines intensify competition for skilled labor and specialized switchgear, deepening reliance on global supply chains. The Germany data center construction market therefore rewards builders that scale quickly without compromising PUE performance.

AI/ML Rack-Density Shift Accelerates Liquid-Cooling Projects

AI inference and training clusters now exceed 80 kW per rack, making air cooling impractical and triggering a wave of liquid-cooling retrofits and green-field deployments. Google’s open 1 MW CDU blueprint illustrates a standardized high-voltage, liquid-ready architecture adopted by hyperscalers. Early movers such as GlobalConnect report 90% cuts in cooling energy after submersion projects, setting new efficiency baselines. Supermicro shipped more than 2,000 liquid-cooled racks between 2024 and 2025,[2]Supermicro — "Supermicro shipped more than 2,000 liquid-cooled racks between 2024 and 2025," supermicro.com proving fast hardware uptake and locking in new construction norms. Construction firms now integrate coolant distribution units and heat-recovery loops at slab stage, compressing later trades and altering contractual scopes within the Germany data center construction market.

Mandatory 50% Renewable-Power Requirement Under EnEfG Drives Retrofit Spending

Germany’s 2024 Energy Efficiency Act mandates 50% renewable electricity for data centers immediately and 100% by 2027,[3]Markus Schneider — "Germany Energy Efficiency Act Explained," White & Case LLP sparking a parallel retrofit segment Dentons. Maincubes signed its first solar PPA for Frankfurt operations, coupling data halls with dedicated photovoltaic arrays. Waste-heat reuse targets of 10% by 2026 and 20% by 2028 prompt district-heating tie-ins like TU Dresden’s EUR 1.6 million energy-reuse plant supplying 3,700 homes. Contractors versed in renewable interconnection and heat-export piping win higher-margin scopes. Financing terms increasingly link interest spreads to on-site green generation, embedding sustainability metrics into construction lending. As a result, the Germany data center construction market is seeing ESG compliance transform from a differentiator to entry requirement.

Grid-Capacity Re-allocation Scheme Opens Secondary Metros

The Federal Network Agency shifted from a first-come queue to merit-based allocation, redirecting 110 kV transmission slots toward under-utilized metros. Berlin’s Urban Tech Republic, redeveloping the former Tegel Airport, offers land and grid access for up to 1,000 tech firms, attracting new data center builds. Maincubes already secured a Nauen parcel for its second Berlin campus as operators hedge against Frankfurt constraints. Munich and Hamburg also market available capacity paired with district-heat reuse incentives, diversifying geographic risk. Developers targeting latency to Bavaria’s industrial base and Hamburg’s logistics corridor broaden the Germany data center construction market beyond its traditional Rhine-Main core.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarce 110 kV grid connections around Frankfurt delays >200 MW pipeline | -1.8% | Frankfurt metropolitan region | Short term (≤ 2 years) |

| Cap-ex inflation on switchgear and generators (+32% since 2022) | -1.2% | National | Short term (≤ 2 years) |

| Tightened PUE ≤1.2 (new DCs) under EnEfG raises design costs | -0.9% | National | Medium term (2-4 years) |

| Berlin land-use moratorium near TXL airport restricts hyperscale plots | -0.6% | Berlin metropolitan region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarce 110 kV Grid Connections Around Frankfurt Delay Pipeline Projects

Frankfurt’s 110 kV backbone operates near maximum load, extending new interconnection lead times to as long as eight years, well beyond typical hyperscale planning cycles. Digital Realty’s cluster of more than 20 local facilities underlines the demand legacy and the resulting saturation. In response, developers fragment projects below 100 MW or pivot to Brandenburg, Berlin, and North Rhine-Westphalia. Construction scheduling becomes contingent on utility-approved reinforcement works, complicating EPC contracts. The Germany data center construction market therefore prices grid-access scarcity into land valuations and PPA premiums.

Cap-ex Inflation on Switchgear and Generators Raises Construction Costs

Producer-price indices show switchgear and diesel-generator packages rising 32% above general building inflation since 2022, eroding project contingencies. Medium-voltage switchgear demand is projected to climb at 16% CAGR due to hyperscale growth, signaling sustained cost pressure. Siemens notes that a single hyperscale campus can require 1 GW annually, equivalent to the power draw of 750,000 homes, magnifying exposure to price swings. Builders increasingly adopt modular electrics to lock in prices early, but long lead items still extend procurement windows. Rising electrical budgets push clients toward design-build contracts that re-allocate risk inside the Germany data center construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tier Type: Tier 4 Drives Premium Construction

Tier 3 captured 56.68% of the Germany data center construction market share in 2025, confirming its balance of reliability and cost efficiency. Tier 4, however, is expanding at 10.74% CAGR, the swiftest pace within the Germany data center construction market size during 2026-2031. Hyperscale and financial-services buyers justify premium redundancy to achieve 99.995% uptime. Construction mandates include dual active power paths, concurrently maintainable cooling, and fault-tolerant fiber routes. Builders specializing in Tier 4 designs can command higher margins but must manage longer testing cycles and regulatory audits.

Tier 1 and Tier 2 builds now attract limited demand as enterprises shift to cloud and require higher availability. Consolidation around Tier 3 and Tier 4 accelerates a move from enterprise hosting to AI-ready hyperscale estates. Microsoft’s EUR 3.2 billion expansion specifies Tier 4 halls designed for continuous machine-learning workloads. Firms with deep experience in concurrent-maintenance architectures will see sustained pipelines, while contractors focused on lower tiers may need to reskill. The Germany data center construction industry therefore rotates toward premium tiers as table-stake reliability rises.

By Data Center Type: Hyperscalers Reshape Construction

Colocation accounted for 48.65% of 2025 revenue, yet self-build hyperscale projects are forecast to rise 11.87% annually, adding momentum to the Germany data center construction market size trajectory. Sovereign-cloud strategies drive hyperscalers to own facilities outright, bypassing neutral hosts. This ownership model scales multi-gigawatt campuses and demands fast-track permitting, high-voltage substations, and campus-wide liquid cooling.

Edge and enterprise builds remain smaller but strategic, supporting latency-sensitive workloads and regulatory data residency. Amazon’s EUR 7.8 billion Brandenburg sovereign-cloud program underscores how hyperscalers combine national compliance with self-managed infrastructure. For contractors, hyperscale self-builds concentrate scope into fewer, larger clients with stringent vendor audits. Colocation providers counter with district-heat reuse and energy-as-a-service models to stay competitive inside the Germany data center construction market.

By Electrical Infrastructure: Power Distribution Innovation

Power-backup solutions led 2025 electrical spend at 56.85%, reflecting UPS and generator dominance. Yet power-distribution systems will see 12.71% CAGR through 2031, the quickest ascent within the Germany data center construction market. AI clusters drive a shift to higher-voltage busways and direct-current architectures that reduce conversion loss and cable bulk. Builders must integrate bus-ducts capable of 1 MW per rack while meeting EnEfG PUE targets.

Hydrogen fuel-cell pilots by Microsoft (3 MW) and NorthC introduce diesel-free backup paths and new mechanical-electrical interfaces. Prefabricated medium-voltage skids now ship factory-tested, cutting on-site work by weeks. Electrical rooms become smaller yet denser, shifting fire-suppression strategies and access-clearance rules. These innovations raise the technical entry bar for newcomers in the Germany data center construction market.

By Mechanical Infrastructure: Cooling System Evolution

Cooling captured 46.92% of 2025 mechanical budgets, but servers and storage assemblies will post 12.22% CAGR as AI hardware proliferates. The Germany data center construction market faces a rapid pivot from air to direct-to-chip and immersion techniques. Builders must rough-in coolant supply and return manifolds early, coordinate floor loading for tanks, and route waste-heat pipelines to district networks.

Racks and cabinets standardize around 600 mm width but increase depth for rear-door heat exchangers. Fire suppression moves to water-mist and inert-gas blends compatible with liquid setups. Prefabricated white-space modules shorten fit-out schedules, yet require precise factory data to avoid rework. Contractors able to certify new liquid mediums gain a competitive advantage as 80 kW-plus racks become mainstream within the Germany data center construction market.

Geography Analysis

Frankfurt remains the primary hub, hosting more than 20 Digital Realty sites and the DE-CIX exchange, but grid constraints limit single-site expansions above 200 MW. AWS, NTT, and Vantage now distribute builds across multiple parcels to secure utility access, keeping the Germany data center construction market resilient despite bottlenecks.

Berlin is emerging as the leading secondary node. The Urban Tech Republic conversion of Tegel Airport offers sizeable plots with district-heating networks that align with EnEfG reuse targets. Maincubes’ forthcoming Nauen campus and Amazon’s Brandenburg sovereign-cloud zone confirm investor appetite. These projects raise the Germany data center construction market size in the capital region and diversify hyperscale footprints away from the Rhine-Main area.

Munich and Hamburg round out the growth corridor. Equinix’s USD 90 million MU4 site near Munich pairs aquifer thermal energy storage with Tier 3 redundancy. Hamburg leverages port-city renewables to market carbon-neutral edge halls. Together, these metros address regional latency, support automotive and logistics verticals, and absorb demand that Frankfurt’s grid cannot meet, extending the geography reach of the Germany data center construction market.

Competitive Landscape

International specialists such as DPR Construction, Exyte, and STRABAG combine global data-center know-how with German code compliance, positioning for hyperscale contracts. Domestic players like GOLDBECK and Data Center Group leverage utility relationships and local labor pools to compete on schedule certainty.

Strategic differentiation centers on liquid-cooling integration, waste-heat export, and on-site renewables that match EnEfG thresholds. Siemens moved beyond equipment supply by signing a multi-year modular electrics deal with Compass Datacenters, underlining a trend toward vertical integration.

Private equity interest remains strong. Vantage securitized EUR 720 million of German assets in 2025, the first such issuance in Europe, lowering its cost of capital. Bain Capital and Aquila formed a pan-European platform aimed at secondary metros, signaling confidence that the Germany data center construction market will maintain double-digit demand even outside Frankfurt.

Germany Data Center Construction Industry Leaders

-

Mercury Engineering

-

Michel Bau GmbH & Co. KG

-

Collen Construction Limited

-

DPR Construction

-

Royal HaskoningDHV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Vantage Data Centers completed an EUR 720 million (USD 821.4 million) asset-backed securitization involving four German facilities with 64 MW capacity, CNBC.

- May 2025: Siemens, SAP, and partners began evaluating domestic AI data-center builds Reuters.

- May 2025: Amazon announced EUR 7.8 billion (USD 8.8 billion) investment in an AWS European Sovereign Cloud in Brandenburg Heise.

- March 2025: Digital Realty expanded its Frankfurt footprint with a sustainable AI-optimized facility Digital Realty.

- February 2025: Vantage Data Centers earmarked EUR 1.4 billion for EMEA expansion, including German projects Vantage.

- February 2025: Green Mountain and KMW topped out a new site outside Frankfurt Data Center Dynamics.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Germany data center construction market as all capital spending tied to green-field or major brown-field facilities whose primary function is housing IT equipment, including the civil shell, electrical and mechanical systems, and integration services that bring the site to commissioning readiness. This covers Tier I-IV builds serving colocation, hyperscale, enterprise, and edge use cases across the country.

Scope exclusion: minor renovation or fit-out projects under EUR5 million are outside our baseline.

Segmentation Overview

-

By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

-

By Data Center Type

- Colocation

- Self-build Hyperscalers (CSPs)

- Enterprise and Edge

-

By Infrastructure

-

By Electrical Infrastructure

- Power Distribution Solution

- Power Backup Solutions

-

By Mechanical Infrastructure

- Cooling Systems

- Racks and Cabinets

- Servers and Storage

- Other Mechanical Infrastructure

- General Construction

- Service - Design and Consulting, Integration, Support and Maintenance

-

By Electrical Infrastructure

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed electrical engineers, EPC contractors, colocation operators, and grid planners in Frankfurt, Berlin, Munich, and Rhineland. Dialog centered on live cost per megawatt, permitting delays, liquid-cooling adoption, and EnEfG compliance, allowing us to validate desk findings and fine-tune escalation factors.

Desk Research

We began with structured desk work that drew on national statistics (Destatis construction permits, BMWK renewable-power data), trade bodies such as the German Datacenter Association, customs shipments for switchgear and chillers, and peer-reviewed energy-efficiency papers. Company filings, tender portals, and reputable press offered cost benchmarks, while D&B Hoovers and Dow Jones Factiva supported contractor revenue checks. Marklines was tapped for specialized generator imports tied to Tier IV sites. These sources are illustrative; many others informed data validation.

Market-Sizing & Forecasting

A top-down build was first created from national data on IT-load additions and EUR per-MW construction norms, which are then cross-checked through selective bottom-up supplier roll-ups and median ASP × volume samples from quoted projects. Key model drivers include (1) annual IT-load additions in MW, (2) average floor-space per rack, (3) EUR per-kW electrical infrastructure cost, (4) liquid-cooling penetration, and (5) renewable-power share mandated by EnEfG. Forecasts use multivariate regression that relates spending to GDP, cloud capex indices, and rack-density trends, with scenario analysis for power-grid constraints. Gaps in bottom-up data are bridged by contractor cost curves gathered during interviews.

Data Validation & Update Cycle

Outputs pass a three-layer review, starting with variance checks versus historic spend and JLL capacity pipelines, followed by peer review inside Mordor, and ending with a senior analyst sign-off. We refresh the model annually and issue interim updates when material investments or regulatory changes emerge; a last-mile check is run before every client delivery.

Why Our Germany Data Center Construction Baseline Commands Reliability

Published values often diverge because firms vary project scope, cost inflation treatment, and update cadence.

Key gap drivers include whether IT hardware is bundled with civil works, if retrofit spending is mixed with new builds, the exchange-rate month chosen, and how soon EnEfG-driven design premiums flow into forecasts. Our model strips out IT equipment, counts only project-level construction outlays, applies quarter-average EUR-USD rates, and is refreshed every twelve months, which is where Mordor Intelligence differentiates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.28 B (2025) | Mordor Intelligence | - |

| USD 10.53 B (2024) | Global Consultancy A | Includes IT racks and cooling retrofits; uses headline contract values without currency normalization |

| USD 7.71 B (2024) | Industry Publisher B | Blends electrical, mechanical, and IT investment; forecast rolled forward from 2022 costs, limited primary validation |

These contrasts show that our scoped, annually updated approach gives decision-makers a balanced figure anchored to clear cost elements and repeatable steps, making it the dependable baseline for strategic planning.

Key Questions Answered in the Report

What is the projected value of the Germany data center construction market by 2031?

The market is expected to reach USD 11.94 billion by 2031, growing at an 8.62% CAGR.

Which German city leads new data center construction?

Frankfurt remains the largest hub, but Berlin, Munich, and Hamburg are gaining share due to grid-capacity reallocation.

How are AI workloads affecting facility design?

AI clusters push rack densities above 80 kW, driving widespread adoption of liquid-cooling infrastructure and higher-voltage power distribution.

What does the Energy Efficiency Act require from new data centers?

The law mandates a PUE of ≤1.2 for new builds and at least 50% renewable electricity immediately, rising to 100% by 2027, plus progressive waste-heat reuse.

Why are Tier 4 facilities growing faster than Tier 3?

Hyperscale and financial-service operators demand 99.995% uptime, justifying the redundancy and higher capital outlay of Tier 4 designs, which are expanding at 10.74% CAGR.

How is construction cost inflation impacting projects?

Switchgear and generator prices have risen 32% since 2022, adding budget pressure and lengthening procurement timelines for large builds.

Page last updated on: