Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 10.94 Billion |

| Market Size (2026) | USD 11.5 Billion |

| Market Size (2031) | USD 14.82 Billion |

| Growth Rate (2026 - 2031) | 5.20% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Chocolate Market Analysis by Mordor Intelligence

The Germany chocolate market size was valued at USD 10.94 billion in 2025, stands at USD 11.50 billion in 2026, and is projected to reach USD 14.82 billion by 2031, expanding at a 5.20% CAGR during the forecast period. In 2024, cocoa-bean costs surged by 172% before moderating, significantly impacting gross margins for manufacturers. This cost pressure persists even as premium, health-oriented product lines drive higher average unit prices, as reported by. Germany, with exports reaching USD 6.26 billion in 2023, continues to reinforce its dual role as a major consumption hub and a manufacturing powerhouse in the global market. The market's primary growth drivers include premiumization, increasing e-commerce penetration, and regulatory initiatives aimed at reducing sugar content in products. Large-scale players are mitigating cost challenges through strategies like hedging and vertical integration, ensuring better control over their supply chains. Meanwhile, artisanal producers are leveraging traceability and sustainability narratives to justify higher price points, appealing to a growing segment of conscious consumers.

Key Report Takeaways

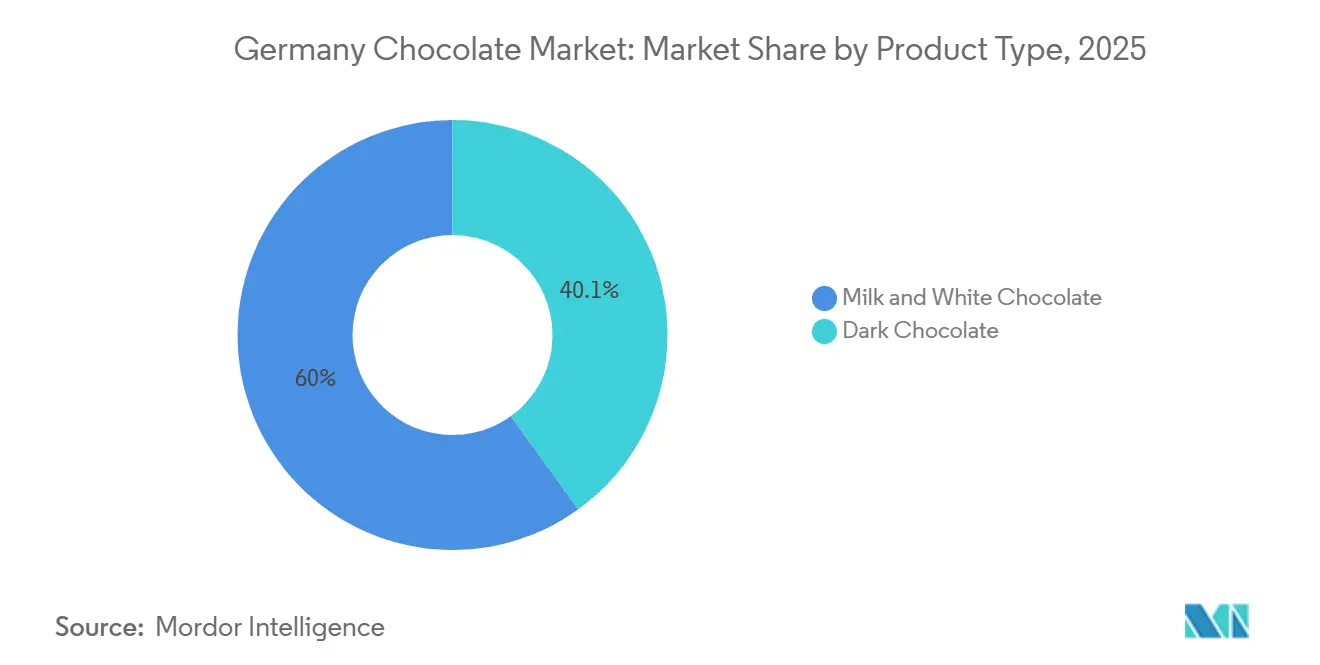

- By product type, milk and white chocolate led with a 59.95% share in 2025, while dark chocolate is forecast to grow at a 6.12% CAGR through 2031.

- By form, tablets and bars held 51.63% of 2025 sales, whereas pralines and truffles show the fastest expansion at a 5.54% CAGR through 2031.

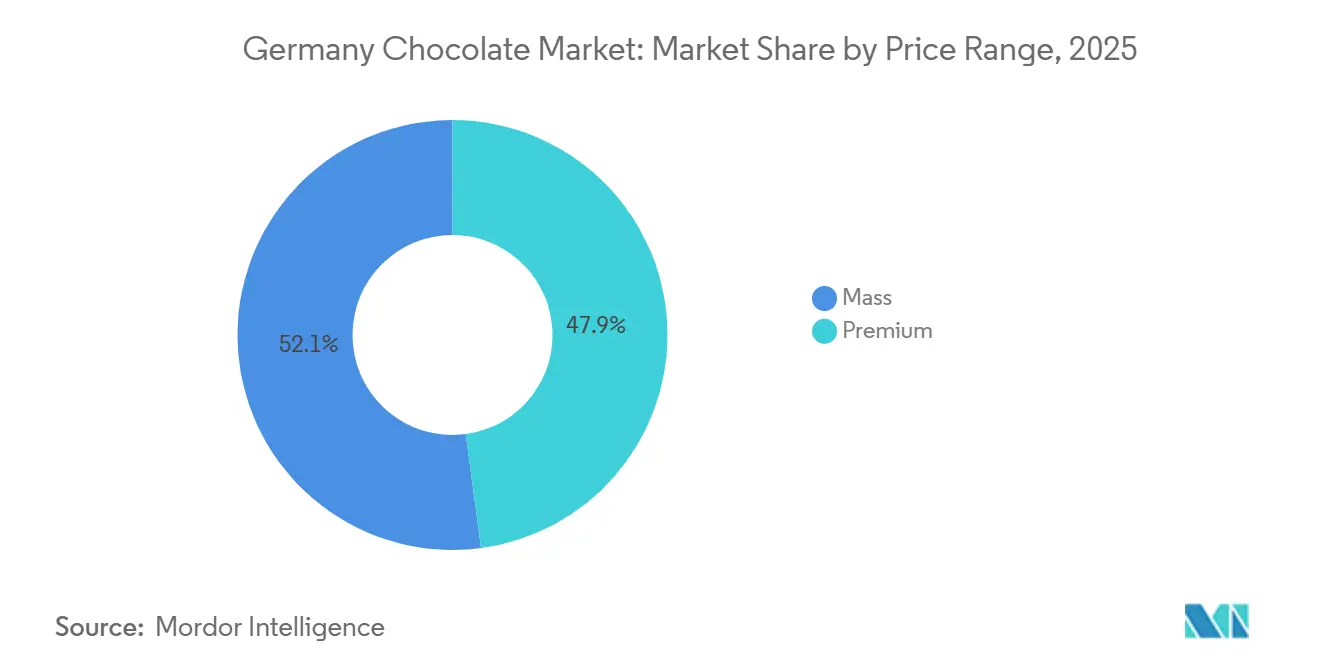

- By price range, the mass segment accounted for 52.12% of 2025 value, yet premium offerings are projected to climb at a 6.42% CAGR through 2031.

- By ingredient type, dairy-based formulations captured 67.18% in 2025, but single-origin chocolate is set to surge at a 10.15% CAGR through 2031.

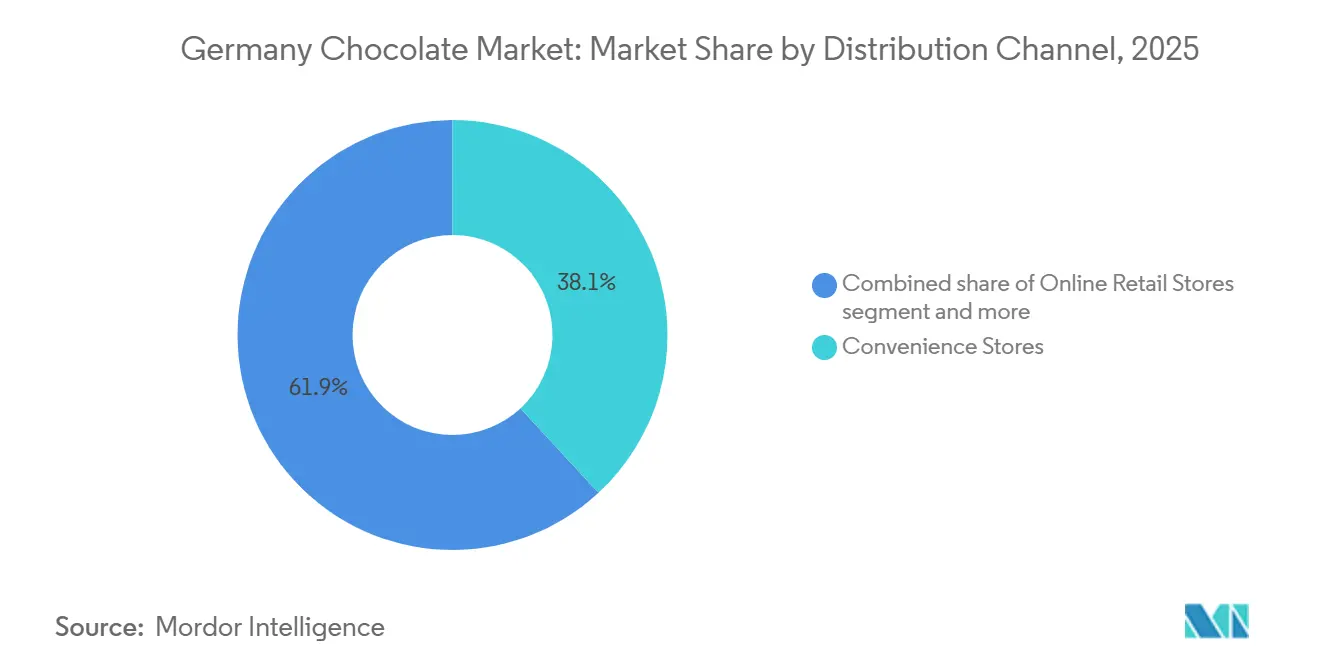

- By distribution channel, convenience stores retained 38.12% share in 2025, while online retail is growing at a 6.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumisation and gifting culture resurgence | +1.2% | Urban centers and tourist destinations nationwide | Medium term (2-4 years) |

| Health-centric demand for high-cocoa, low-sugar SKUs | +1.0% | Metro areas with higher disposable income | Medium term (2-4 years) |

| E-commerce and quick-commerce penetration | +0.8% | Major metropolitan areas | Short term (≤ 2 years) |

| Sustainability and traceable bean-to-bar micro-roasters | +0.6% | Craft clusters in Berlin, Munich, Hamburg | Long term (≥ 4 years) |

| Made-in-Germany tourist purchases rebound | +0.4% | Berlin, Munich, Hamburg, Heidelberg, Dresden | Short term (≤ 2 years) |

| Upcycling of cacaofruit into new SKUs | +0.3% | Premium and organic segments nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premiumization and gifting culture resurgence

German shoppers are increasingly viewing chocolate as an affordable luxury. A 2024 survey by Barry Callebaut revealed that 64% of consumers are on the lookout for premium variants, 65% desire multi-texture experiences, and 61% have a preference for limited editions. Seasonal collections, which saw an annual growth of 4.5% from 2019 to 2023, are projected to accelerate to 4.9% growth through 2028. According to the Allensbach Institute of Public Opinion Research, it is revealed that about 9.09 million consumers across Germany bought chocolates in the last 14 days in 2024[1]Source: Allensbach Institute for Public Opinion Research," AWA 2024", ifd-allensbach.de. This trend underscores the resilience of gifting, even in the face of food inflation, as consumers continue to prioritize high-quality and unique chocolate options for special occasions. Premium SKUs, with their higher margins, effectively counterbalance spikes in cocoa costs, making them a profitable choice for manufacturers and retailers alike. Retailers are dedicating more shelf space to single-origin bars and luxury boxed assortments, reflecting the growing demand for artisanal and exclusive products. Additionally, subscription services that offer curated monthly selections are solidifying chocolate's place in consumers' indulgence routines, providing a convenient and personalized way to enjoy premium offerings regularly.

Health-centric demand for high-cocoa, low-sugar SKUs

Dark chocolate's rise is driven by shifting nutritional standards.As diabetes and other lifestyle diseases become more prevalent, German consumers are increasingly turning to dark and low-sugar chocolate variants. For instance, the Robert Koch Institute reported in 2024 that approximately 10.3% of adults in Germany were diagnosed with diabetes[2]Source: Robert Koch Institute, "Diabetes mellitus: prevalence (from 18 years)", gbe.rki.de. Starting January 2024, the revised Nutri-Score algorithm will favor chocolates with higher cocoa percentages, benefiting bars with over 70% cocoa content. In a move towards healthier options, ETH Zurich, Koa, and Felchlin have introduced a whole-fruit chocolate that substitutes up to 10% of added sugar with cocoa-pulp gel. This innovation not only enhances fiber content by 20% but also reduces saturated fat by 30%. Such advancements align with health and sustainability objectives, as they make use of cocoa pulp that was previously discarded. In response to these evolving standards, brand portfolios are increasingly showcasing reduced-sugar or high-cocoa variants to sidestep potential downgrades on the Nutri-Score scale.

E-commerce and quick-commerce penetration

Between 2019 and 2023, online chocolate sales surged at a double-digit rate, significantly outpacing gains seen in traditional brick-and-mortar stores. This growth highlights the increasing consumer preference for the convenience and variety offered by digital channels. Brands are increasingly turning to direct-to-consumer webshops, allowing them to safeguard margins that would typically be eroded by retail mark-ups while also fostering direct relationships with their customers. In cities like Berlin, Munich, Hamburg, and Cologne, quick-commerce players such as Rohlik and REWE Online are ensuring deliveries in under 30 minutes, transforming sudden cravings into instant purchases and redefining consumer expectations for speed and convenience. Meanwhile, venture-backed newcomers are harnessing their digital platforms to swiftly test limited edition chocolates, gather real-time consumer feedback, and adapt their offerings based on market demand. In response, established players are adopting omnichannel approaches, seamlessly merging in-store experiences with home delivery services to remain competitive in this evolving landscape.

Sustainability and traceable German bean-to-bar micro-roasters

Transparency is driving up chocolate prices. Rausch, for instance, directly sources cocoa from farms in Costa Rica, Ecuador, and Peru, sidestepping intermediaries to ensure accurate origin data and maintain quality control throughout the supply chain. Similarly, Ritter Sport pours EUR 7 million annually into cocoa programs and runs its own farm in Nicaragua, achieving complete traceability while supporting sustainable farming practices. Fairafric and Amanase, by manufacturing in their home countries, not only add local value by creating jobs and fostering economic growth but also reduce their CO₂ emissions through shorter supply chains. These practices resonate with the EU Deforestation Regulation, which, starting December 2025, will require proof of geolocation to ensure compliance with sustainability standards. Notably, two-thirds of German consumers are now actively seeking sustainably produced chocolate, underscoring the growing importance of traceability as a key factor influencing purchasing decisions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile cocoa futures elevating input costs | -1.5% | Global, with direct effect on German plants | Short term (≤ 2 years) |

| Stringent sugar-reduction regulation | -0.8% | Nationwide | Medium term (2-4 years) |

| Share shift to savory protein snacks | -0.5% | Urban health-oriented demographics | Medium term (2-4 years) |

| NGO scrutiny on deforestation and child labor | -0.4% | Global supply chains feeding Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile cocoa futures elevating input costs

In April 2024, cocoa prices soared to a record high of USD 12,000 per tonne, only to drop to around USD 7,000 by May. The International Cocoa Organization reported a historic deficit of 500,000 tonnes for the 2023-24 season, the largest ever recorded, and cautioned of only a slight surplus in the future. Farms in West Africa, grappling with viral outbreaks, have seen significant disruptions in production, while low stocks-to-grindings ratios continue to exert upward pressure on raw material prices. These factors have created a challenging environment for manufacturers, particularly those lacking multi-year purchase contracts, as they either face shrinking profit margins or are compelled to increase retail prices to offset costs. Consequently, adopting robust hedging strategies and pursuing vertical integration into the source have become critical measures for maintaining competitiveness in the market.

Stringent sugar-reduction regulation and nutri-score labelling

Since January 2024, Germany's updated Nutri-Score, overseen by RAL gGmbH, has begun penalizing sugar-laden recipes, pushing brands towards reformulation to meet stricter nutritional standards. The Federal Ministry of Food and Agriculture's strategy to reduce sugar content extends through 2025, with public reporting increasingly influencing retailer decisions on product listings. Supermarkets are prioritizing healthier product portfolios, and brands hesitant to reduce sugar content face the risk of losing valuable shelf space. As manufacturers explore fiber-rich bulking agents and alternative sweeteners to replace sugar, the costs of reformulation continue to rise, adding financial pressure. Smaller firms, often with limited research and development budgets and resources, are particularly vulnerable to compliance fatigue, which hampers their ability to adapt to these regulatory changes effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dark Chocolate Extends Health-Led Momentum

In 2025, milk and white chocolates captured a dominant 59.95% share of Germany's chocolate market, becoming staples for gifting and impulse purchases, thanks to their widespread availability. These variants have maintained their popularity due to their versatility and appeal across various consumer demographics. As cocoa prices surged, brands felt the pinch on volume. In response, many turned to plant-based milks and fiber fillers, aiming to enhance Nutri-Scores while retaining their loyal customer base. This shift reflects a broader trend of aligning with health-conscious consumer preferences without compromising on taste. Looking ahead to 2031, brands are diversifying their portfolios, catering to both the mass market and premium segments with high-cocoa offerings. Meanwhile, cost-effective ingredients like milk ensure affordability, overshadowing the pricier dark chocolate options and sustaining their mass appeal.

Dark chocolate is projected to grow at a robust 6.12% CAGR through 2031, driven by Nutri-Score enhancements and a significant 77% reduction in consumer sugar intake. This growth is further supported by increasing consumer awareness of the health benefits associated with dark chocolate, such as its antioxidant properties. Craft brands, emphasizing single-origin sourcing and ethical practices, command premium prices, providing a buffer against market volatility. These brands also leverage storytelling around sustainability and quality to attract discerning consumers. Innovations like whole-fruit sweetening strike a harmonious balance between health and indulgence, appealing to a growing segment of health-conscious yet indulgent shoppers. In urban centers, a trend of premiumization is steering shoppers towards narratives centered on high-cocoa content, reflecting a shift in consumer preferences towards more sophisticated and ethically sourced products.

By Form: Pralines and Truffles Reinforce Seasonal Upselling

In the German chocolate market, tablets and bars accounted for 51.63% of the 2025 volume, thanks to their portability and prime placement at checkouts. These products are a staple for consumers due to their convenience and accessibility. Facing intense competition from private labels, brands are turning to single-origin editions and sustainable wrappers to enhance their value and differentiate themselves in the market. While there's a noticeable shift towards premium offerings, tablets and bars remain crucial to the market's volume, serving as a reliable choice for everyday consumption. Supermarkets, recognizing the trend, are prominently showcasing premium chocolates during the Christmas and Easter peaks, capitalizing on increased consumer spending during these festive seasons.

Pralines and truffles are set to grow at a 5.54% CAGR until 2031, fueled by their popularity in seasonal gifting and allure to tourists. These products are often associated with indulgence and luxury, making them a preferred choice for special occasions. Even as cocoa prices surge, luxury packaging, multi-texture fillings, and limited editions help maintain elevated price points, appealing to consumers willing to pay a premium for exclusivity. Craft assortments, featuring unique flavors like yuzu or pink peppercorn, cater to the adventurous palate, offering a novel experience. Additionally, niche formats such as drinking chocolate, nibs, and decorative figures are enriching the chocolate experience with a touch of storytelling, creating a deeper emotional connection with consumers and enhancing the overall appeal of the product offerings.

By Price Range: Premium Outpaces Mass on Provenance Storytelling

In 2025, the mass segment held a commanding 52.12% share of the German chocolate market, driven by scale brands and widespread distribution catering to price-sensitive consumers. This segment benefits from its ability to offer affordable options without compromising on availability, making it a preferred choice for a broad consumer base. To navigate fluctuations in cocoa prices and tightening margins, brands rely on promotional discounts to maintain volume. With a tiered approach, brands introduce entry-level, mid-range, and premium offerings, adeptly managing shifts in consumer spending. The widespread presence of these brands in everyday retail channels, such as supermarkets and convenience stores, solidifies their market dominance by ensuring accessibility and visibility.

Outpacing the overall market, the premium segment is set to grow at a robust 6.42% CAGR through 2031. This surge is attributed to the rising allure of single-origin cacao, organic certifications, and climate-neutral endorsements, all underscoring a commitment to quality. Consumers in this segment are increasingly drawn to products that emphasize sustainability and ethical sourcing, reflecting a shift in purchasing priorities. In affluent locales like Berlin and Munich, retailers are dedicating prime shelf space to craft bars and curated bundles, further enhancing the visibility and appeal of premium offerings. Furthermore, farm-owned and direct-trade networks bolster credibility by providing assurances of deforestation-free sourcing, which resonates strongly with environmentally conscious buyers. As brands leverage their pricing power, they not only shield themselves from input volatility but also drive a trend towards premiumization, capitalizing on the growing demand for high-quality, ethically produced chocolate.

By Ingredient Type: Single-Origin Surges While Dairy Dominates Base Volume

In 2025, dairy-based recipes dominated the German chocolate market, making up 67.18% of the output, thanks to their traditional roots and widespread appeal. These recipes have long been a staple in the market, appealing to a broad consumer base that values the rich, creamy texture and familiar taste associated with dairy. However, plant-based alternatives are making inroads: Ferrero's chickpea Nutella, Barry Callebaut's Plant Craft, and Hochdorf's VIOPLUS 1:1 milk substitute cater to the lactose-free and vegan segments. These products address the growing demand for healthier and more sustainable options, driven by shifting consumer preferences and dietary restrictions. As these alternatives carve out space in supermarkets, traditional recipes may see a gradual decline in market share. Yet, reformulations aim to maintain a sense of familiarity amidst these changes, ensuring that traditional consumers remain engaged while adapting to evolving trends.

Lines emphasizing single-origin ingredients are leading the pack, boasting a 10.15% CAGR, the fastest growth rate among all segments. This surge is driven by narratives of terroir, reminiscent of the trends seen in specialty coffee and craft beer. Single-origin chocolates highlight the unique flavors of specific regions, appealing to consumers seeking authenticity and exclusivity. Urban connoisseurs are increasingly valuing transparent sourcing, and with the EU's deforestation regulations, traceable suppliers are gaining structural advantages. These regulations not only ensure environmental sustainability but also enhance the credibility of brands that comply. This credibility, coupled with premium pricing, is attracting discerning shoppers who are willing to pay a premium for quality and ethical sourcing.

By Distribution Channel: Online Accelerates, Convenience Retains Impulse Core

In 2025, convenience stores captured a dominant 38.12% share of Germany's chocolate market, driven by impulse purchases and high foot traffic. These stores remain a preferred choice for consumers seeking immediate gratification, as their strategic locations and wide product availability cater to on-the-go buyers. Despite rising rents and labor costs, mass brands continue to thrive in physical retail channels due to their ability to attract a broad customer base. Meanwhile, discount retailers are expanding their offerings to include premium and organic chocolate bars, blurring the lines between market tiers and appealing to health-conscious and quality-focused consumers. Additionally, a hybrid click-and-collect model is emerging, allowing customers to make online reservations and swiftly pick up their purchases from nearby locations, combining the convenience of e-commerce with the immediacy of physical stores.

Online retail is set to grow at a projected CAGR of 6.12% through 2031, bolstered by rapid delivery services and brands' ability to harness direct consumer data for personalized marketing strategies. Quick-commerce platforms are pairing chocolates with grocery items, fueling spontaneous purchases by leveraging convenience and speed. Subscription clubs are carving out a niche, ensuring consistent revenue from artisanal chocolates by offering curated selections and exclusive flavors, which appeal to premium consumers. These models also enjoy higher profit margins by eliminating intermediaries, allowing brands to directly connect with their customers and build loyalty.

Geography Analysis

Germany stands as the world's leading chocolate exporter, a testament to its robust domestic capabilities and strategic proximity to major EU markets. Urban hubs like Berlin, Munich, Hamburg, Cologne, and Frankfurt showcase a heightened demand for premium, single-origin, and reduced-sugar chocolates, driven by affluent consumers and discerning retailers. These cities also serve as trendsetters for innovative product launches and marketing strategies, further solidifying Germany's position in the global chocolate market. Seasonal surges, particularly for "Made in Germany" boxed pralines, are bolstered by tourist hotspots such as Dresden and Heidelberg, where local traditions and cultural appeal enhance product desirability.

These metropolitan areas grapple with intricate regulations, yet they swiftly embrace front-of-pack Nutri-Score labels and emphasize certified sustainable cocoa. While 79-81% of chocolate products nationwide boast sustainability certifications[3]Source: Centre for the Promotion of Imports from Developing Countries, "The German market potential for cocoa", cbi.eu. This discrepancy is set to come under scrutiny with the EU Deforestation Regulation, which aims to tighten compliance and transparency across supply chains. Notably, producers like Ritter Sport, with their Nicaraguan farm and vertically integrated supply chains, are poised to reap competitive advantages by ensuring traceability and sustainability.

Despite Germany being home to Europe's largest organic grocery market, organic chocolate constitutes a mere 2.5% of the total category turnover, signaling a significant growth opportunity. Retail chains are responding by establishing dedicated "Bio" aisles, enhancing visibility for certified bars and catering to the growing consumer preference for organic products. Regional spending habits diverge, with southern states indulging more per capita due to higher disposable incomes and a preference for premium offerings, while northern rural areas remain steadfast to mainstream brands, driven by price sensitivity. While quick-commerce has predominantly thrived in major cities, projections indicate its expansion into second-tier markets by 2028, driven by advancements in logistics and increasing consumer demand for convenience.

Competitive Landscape

Germany's chocolate market indicates a moderate consolidation, leaving space for specialty disruptors. Dominating the volume are multinationals like Mars, Mondelez, Ferrero, Nestlé, Lindt & Sprüngli, and Barry Callebaut, all leveraging procurement scales to navigate cocoa's volatility. In a strategic pivot, Mars acquired Kellanova for USD 36 billion in August 2024, broadening its portfolio to include savory snacks. This acquisition highlights Mars's intent to diversify beyond confectionery and strengthen its position in the broader food market. Meanwhile, Mondelez's December 2024 exploration of a bid for Hershey underscores its ongoing merger and acquisition appetite, reflecting the competitive dynamics and growth ambitions within the global chocolate industry.

German craft champions are carving out profitable niches. In July 2024, Ritter Sport expanded its facility with a EUR 200 million investment, boosting capacity by 20% and committing to 100% certified sustainable cocoa by 2025. This move aligns with the growing consumer demand for ethical and sustainable products, positioning Ritter Sport as a leader in responsible chocolate production. Rausch, with its own plantation in Costa Rica and a flagship store in Berlin, ensures traceability from bean to bar and offers an experiential retail experience that appeals to premium and conscious consumers. Fairafric, manufacturing in Ghana, emphasizes the social impact of its products to German consumers, capturing more value at the origin while addressing the increasing preference for fair trade and locally sourced goods.

Innovation alliances are increasingly blurring the lines between established players and start-ups. In November 2025, Barry Callebaut teamed up with Planet A Foods, introducing the cocoa-free ingredient ChoViva to over 60,000 stores across eight European nations, Germany included. This partnership demonstrates the industry's shift toward sustainable and alternative ingredients to address environmental concerns and evolving consumer preferences. Lindt, recognizing the plant-based trend, incorporated ChoViva into its vegan bars, catering to the growing demand for plant-based and allergen-free options. These collaborations not only mitigate research and development risks for larger firms but also provide start-ups with immediate market scale, fostering innovation across the supply chain. Looking ahead, anticipate more partnerships focusing on upcycled ingredients and carbon-neutral supply chains through 2030, as companies strive to meet sustainability goals and consumer expectations.

Germany Chocolate Industry Leaders

-

August Storck KG

-

Chocoladefabriken Lindt & Sprüngli AG

-

Ferrero International SA

-

Mars Incorporated

-

Mondelēz International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Lindt stirred excitement in Germany with its launch of the Dubai Style Chocolate. The pistachio-filled bars, priced at a premium, were released in a limited run across 10 select shops. Drawing inspiration from viral trends in Dubai, the creamy white chocolate bars with nutty fillings led to long queues as chocolate enthusiasts rushed to grab them.

- November 2025: Läderach rolled out its FrischSchoggi Dark Mint in Germany. This limited-edition slab combined freshly poured dark chocolate with caramelized almonds and a hint of organic dried mint, delivering a crisp, cooling finish.

- October 2025: Ritter Sport unveiled its Travel Retail Editions in Germany, featuring 15 mini bars across five distinct flavors. This premium line, emphasizing the brand's signature square-shaped innovation, is tailored for travelers seeking high-quality chocolate on the go.

- January 2025: Adlon Schokolade's Dubai Style chocolate made waves in Berlin, selling out in just four days. Crafted by the hotel's skilled patissiers, this luxurious pistachio-filled bar capitalized on global trends favoring opulent, textured confections.

Germany Chocolate Market Report Scope

The chocolate market encompasses the global industry involved in the production, distribution, and sale of chocolate products derived from cocoa beans. The scope of the German chocolate market includes product type, form, price range, ingredient type, and distribution channel. Based on the product type, the market is segmented into Dark Chocolate, Milk and White Chocolate. On the basis of form, the market is segmented into tablets and bars, molded blocks, pralines and truffles, and other forms. Based on the price range, the market is segmented into mass and premium. Convenience Store, Online Retail Store, Supermarket/Hypermarket, and others are covered as segments by Distribution Channel. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments. Source: https://www.mordorintelligence.com/industry-reports/chocolate-market

By Product Type

| Dark Chocolate |

| Milk and White Chocolate |

By Form

| Tablets and Bars |

| Molded Blocks |

| Pralines and Truffles |

| Other Forms |

By Price Range

| Mass |

| Premium |

By Ingredient Type

| Dairy-based |

| Plant-based |

| Single-origin |

By Distribution Channel

| Supermarket/Hypermarket |

| Convenience Store |

| Online Retail |

| Other Distribution Channels |

| By Product Type | Dark Chocolate |

| Milk and White Chocolate | |

| By Form | Tablets and Bars |

| Molded Blocks | |

| Pralines and Truffles | |

| Other Forms | |

| By Price Range | Mass |

| Premium | |

| By Ingredient Type | Dairy-based |

| Plant-based | |

| Single-origin | |

| By Distribution Channel | Supermarket/Hypermarket |

| Convenience Store | |

| Online Retail | |

| Other Distribution Channels |

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms