Home and Property Improvement

9th JuneA Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

The GCC Furniture Market Report is Segmented by Application (Home Furniture, Office Furniture, Hospitality Furniture, and More), Material (Wood, Metal, Plastic & Polymer, Other Materials), Price Range (Economy, Mid-Range, Premium), Distribution Channel (B2C/Retail, B2B/Project), and Geography (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman, Bahrain). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

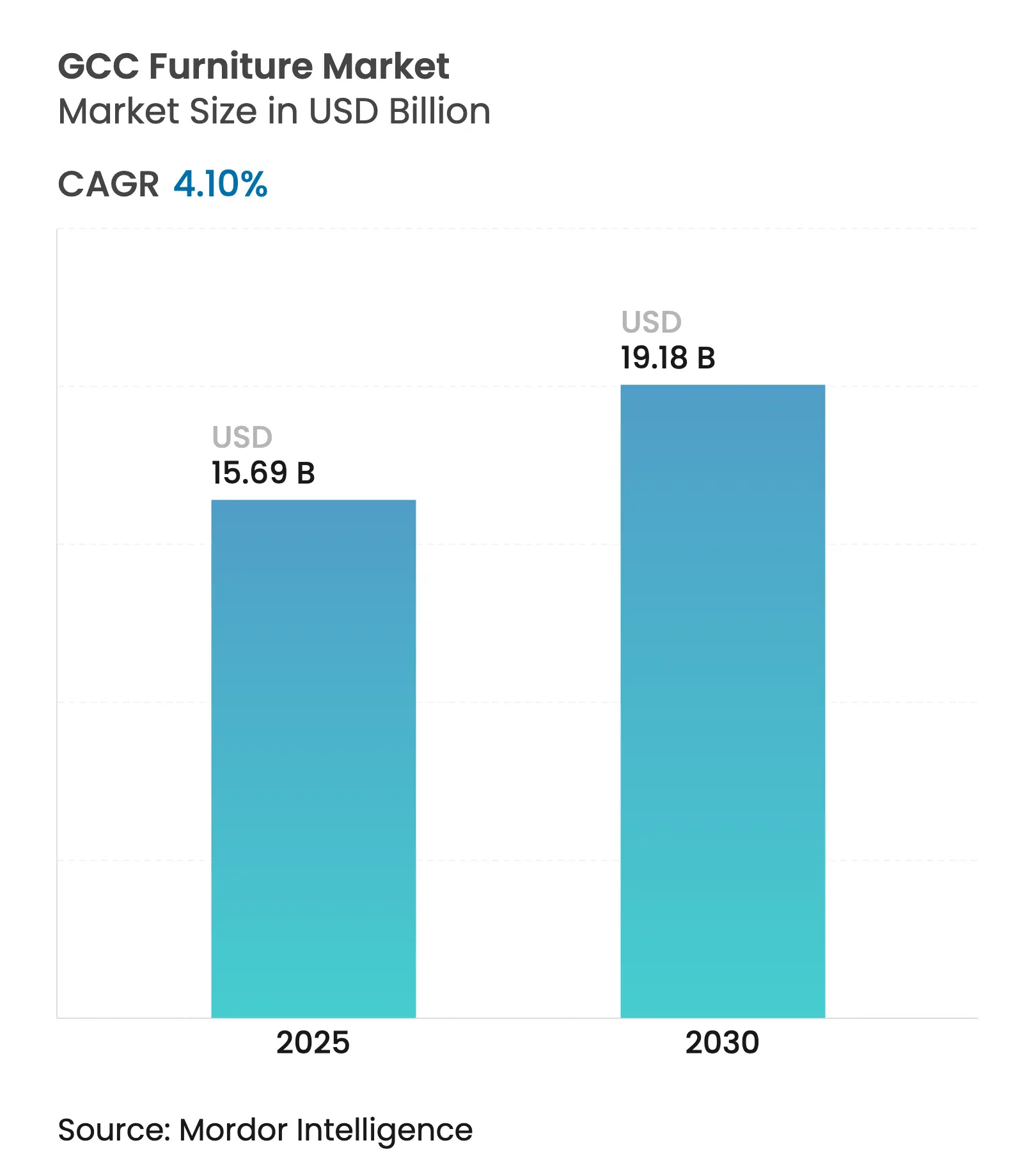

| Market Size (2025) | USD 15.69 Billion |

| Market Size (2030) | USD 19.18 Billion |

| Growth Rate (2025 - 2030) | 4.10 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The GCC furniture market size stood at USD 15.69 billion in 2025 and is on track to reach USD 19.18 billion by 2030, reflecting a 4.10% CAGR over the forecast period. Construction outlays tied to giga-projects, sovereign wealth–funded smart-city programs, and the region’s emergence as a tourism and business hub form a demand backbone that is less cyclical than traditional building cycles[1]Consultancy-me Staff, “Saudi Arabia’s Construction Spending to Hit $150 Billion in 2025,” Consultancy-me.com. Saudi Arabia’s USD 150 billion 2025 construction spend and USD 850 billion pipeline through 2030 translate into sustained contract-furniture orders for hospitality, residential, and commercial fitouts. Online migration, local wood-panel manufacturing scale-ups, and cross-border B2B digital procurement add structural depth to growth, while expatriate inflows maintain a high furniture replacement velocity. Competitive pressure escalates as global retailers deploy price cuts and omnichannel models, and local producers expand capacity to capture import substitution and near-shoring benefits.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Online migration of furniture retail

Online migration of furniture retail

| +0.8% | GCC-wide, led by UAE and Saudi Arabia | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+0.8%

|

Geographic Relevance

:

GCC-wide, led by UAE and Saudi Arabia

|

Impact Timeline

:

Medium term (2-4 years)

|

Hospitality boom linked to giga-projects

Hospitality boom linked to giga-projects

| +1.2% | Saudi Arabia, Qatar, UAE | Long term (≥ 4 years) | |||

Rapid expatriate inflow & rental turnover

Rapid expatriate inflow & rental turnover

| +0.6% | UAE, Qatar, Kuwait | Short term (≤ 2 years) | |||

Local wood-panel production scaling

Local wood-panel production scaling

| +0.4% | Saudi Arabia, UAE | Long term (≥ 4 years) | |||

Sovereign wealth–backed smart-city spending

Sovereign wealth–backed smart-city spending

| +0.9% | Saudi Arabia, UAE | Long term (≥ 4 years) | |||

Cross-border B2B digital marketplaces for fit-out

Cross-border B2B digital marketplaces for fit-out

| +0.3% | GCC-wide | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Online Migration of Furniture Retail

Digital commerce is reshaping the GCC furniture market as platform penetration rises. The UAE’s online home-office and workplace furniture segment reached USD 17.7 million in 2025, and penetration is set to climb to 51.9% by 2029[2]ECDB Analytics Team, “Home Office & Workplace Furniture eCommerce Market in UAE,” Ecommercedb.com. Egyptian marketplace Kemmitt entered Saudi Arabia with 25,000 SKUs, underscoring cross-border e-commerce scale. Traditional retailers respond by deploying augmented-reality tools and last-mile services; IKEA generated 26% of global revenue online in 2024, a benchmark that raises customer expectations region-wide[3]Inter IKEA Group Press Office, “A Year of Investment to Build a Stronger IKEA for the Future,” Inter.ikea.com. Buy-now-pay-later integration by Majid Al Futtaim lifted average order values 25–50% in 2024, proving that flexible payments accelerate premium uptake. As omnichannel formats mature, data-driven assortment planning and inventory pooling lower stock-out risk and improve lead times, reinforcing consumer migration to digital journeys.

Hospitality Boom Linked to Giga-Projects

Mega-projects in Saudi Arabia, Qatar, and the UAE are fuelling contract-furniture demand. Qatar’s room inventory climbed to 40,405 keys by end-2024 with 69% occupancy and 29% RevPAR growth, while Saudi giga-projects such as NEOM, the Red Sea, and Qiddiya push bespoke FF&E specifications into the procurement mix. NEOM’s hotel division mandates stringent sustainability criteria, opening routes for suppliers with certified materials[4]Source: NEOM Media Team, “NEOM Hotel Division,” Neom.com. The Middle East luxury fit-out market is projected to double from USD 16.3 billion in 2023 to USD 32.7 billion by 2030, an outlook that aligns with elevated furniture spend on craftsmanship and experiential design. Suppliers able to meet international brand standards, integrate smart features, and ensure rapid logistics gain preferred-vendor status across pipelines lasting well into the next decade.

Rapid Expatriate Inflow & Rental Turnover

Economic diversification accelerates demographic churn, triggering frequent furniture renewals. Saudi residential real-estate transactions reached USD 71.8 billion in 2024, while government programs target 70% homeownership, bolstering both sale-and-rent segments. UAE corporate housing and short-term rentals rely on flexible furnishings, spurring growth in leasing and subscription services that cater to relocations. Qatar welcomed 5.08 million tourists in 2024, 41% from GCC countries, adding new occupants to furnished apartments and serviced residences. Retailers monetize turnover through trade-in schemes and modular ranges designed for easy transport. Subscription models also serve facilities management firms, embedding annuity streams into what was traditionally a one-time sale.

Local Wood-Panel Production Scaling

Import substitution strategies are strengthening supply security while aligning with circular-economy goals. Although plywood imports tripled in Saudi Arabia and the UAE in 2024, investments are shifting toward in-country engineered-wood capacity to meet future demand. Saudi regulations now target 95% recycling of metals and 75% of plastics by 2040, encouraging composite-panel innovations using recycled content. Roshn Group embeds local manufacturing clauses in procurement, standardizing specifications across its multiyear housing pipeline. Domestic producers gain pricing leverage against currency swings and freight costs, and certified local panels satisfy international hotel requirements for chain-of-custody documentation.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Price volatility of imported hardwood & metals

Price volatility of imported hardwood & metals

| -0.7% | GCC-wide | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-0.7%

|

Geographic Relevance

:

GCC-wide

|

Impact Timeline

:

Short term (≤ 2 years)

|

Fragmented after-sales & logistics in GCC

Fragmented after-sales & logistics in GCC

| -0.5% | GCC-wide, acute in smaller markets | Medium term (2-4 years) | |||

Low adoption of circular-economy furniture take-back

Low adoption of circular-economy furniture take-back

| –0.3% | GCC-wide, especially in urban expatriate hubs | Medium term (2–4 years) | |||

Skilled upholstery & carpentry labour shortages Skilled upholstery & carpentry labour shortages | -0.2% | GCC-wide, severe in Qatar and UAE | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Price Volatility of Imported Hardwood & Metals

Raw material cost fluctuations create margin pressure across GCC furniture supply chains as the region maintains high import dependency for premium materials and metal components. Global supply chain improvements normalized freight costs toward 2019 levels by early 2023, yet persistent input-cost inflation from labour, energy, and supplier price increases offset transportation savings, while elevated inventory levels across retail sectors compress gross margins and limit procurement flexibility. China's reopening in January 2023 improved component availability and reduced lead times, though geopolitical trade measures continue to raise input costs for furniture supply chains globally, creating pricing volatility that affects both local manufacturers and importers. The concentration of supplier geographies creates systemic risks similar to semiconductor supply chains, where disruptions in key timber or metal-producing regions can rapidly impact GCC furniture costs and availability.

Fragmented After-Sales & Logistics in GCC

Service delivery inconsistencies across diverse GCC markets limit customer satisfaction and repeat purchase rates as logistics infrastructure varies significantly between major urban centers and secondary markets. The region's geographic spread across six countries with different regulatory frameworks, customs procedures, and last-mile delivery capabilities creates operational complexity for furniture retailers attempting to standardize service levels, while smaller markets like Bahrain and Oman lack the scale to support dedicated distribution networks. Cross-border logistics remain challenging despite GCC integration efforts, with furniture shipments requiring country-specific certifications and compliance procedures that increase delivery times and costs, particularly for custom or made-to-order products that cannot leverage consolidated shipping models. The lack of standardized installation and after-sales service networks across the region forces retailers to rely on local partnerships that may not maintain consistent quality standards or technical capabilities.

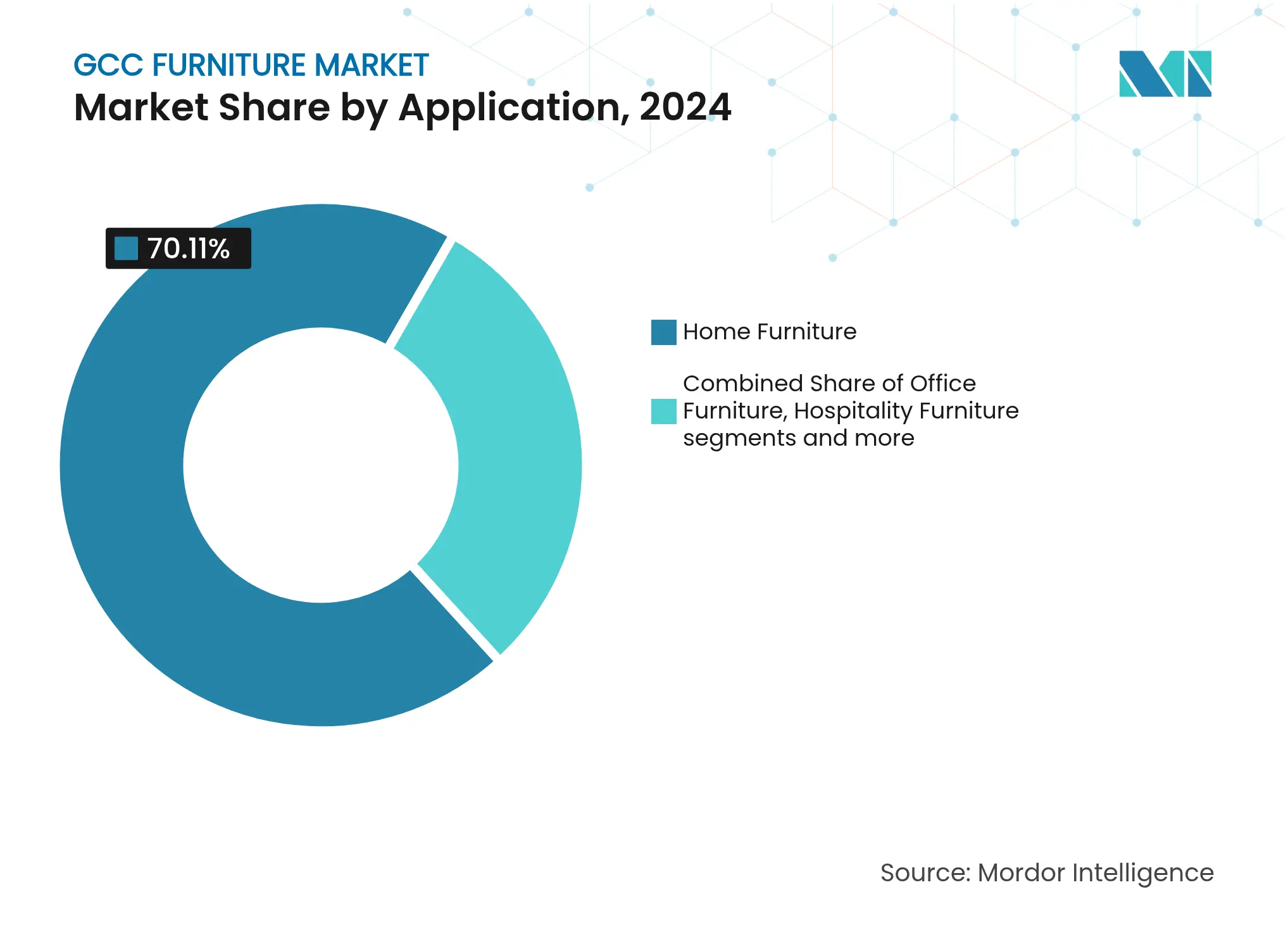

By Application: Home Furniture Anchors Demand, Hospitality Accelerates

Home furniture commanded 70.11% of the GCC furniture market share in 2024 as public-sector housing programs and sustained residential construction generated large order volumes. Built-in wardrobes, modular kitchens, and multi-use living-room sets form the bulk of sales in the GCC furniture market. Hospitality furniture, although smaller in base, is set to grow at a 4.71% CAGR, tapping the pipeline of hotel keys in Qatar and Saudi Arabia. Institutional segments such as office, educational, and healthcare furniture contribute to steady procurement linked to public budgeting cycles.

A lifestyle tilt toward space optimization, driven by expatriate rental churn, pushes demand for modular, easy-to-assemble items. Flat-pack propositions from global brands resonate with these needs, while luxury villas favor bespoke artisanal pieces. The integration of smart-home features, USB-enabled nightstands, and IoT-ready desks is becoming common across mid-range and premium tiers. Hospitality buyers increasingly specify eco-certified materials, aligning with global brand standards and net-zero pledges.

Note: Segment shares of all individual segments available upon report purchase

By Material: Wood Dominates, Polymers Gain Traction

Wood products retained a 60.01% share of the GCC furniture market size in 2024, reflecting cultural preference and perceived value. Mahogany and oak remain staples in premium ranges, while engineered wood gains share in mid-range offerings. Polymers, including recycled plastics and composite resins, will compound at a 5.56% CAGR on the back of outdoor-furniture demand and lightweight modular office solutions. Metal framing enjoys consistent uptake in hospitality and healthcare settings for durability.

Sustainability targets embedded in the UAE Circular Economy Policy and Saudi net-zero commitments amplify interest in FSC-certified lumber and recycled-content polymers. Local panel factories shorten lead times and provide price stability, while advances in texture-printing give polymer furniture a wood-like finish at lower cost and weight. Heat resistance and low maintenance appeal to outdoor dining venues and beachfront resorts, two segments expanding in line with tourism strategies.

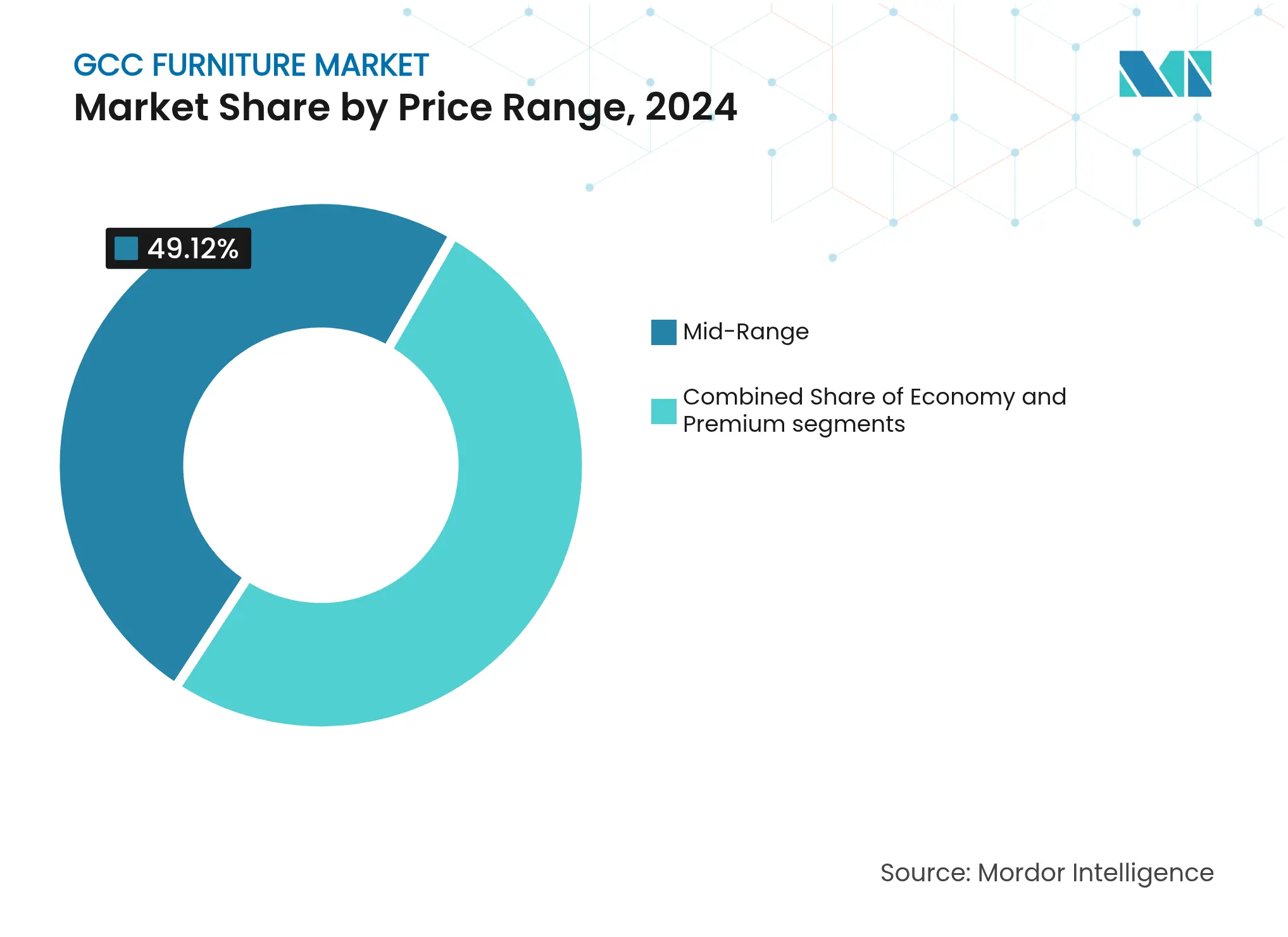

By Price Range: Mid-Range Forms the Core

Mid-range offerings held 49.12% of the GCC furniture market size in 2024 by balancing affordability and quality. Global retailers compete here through volume production and supply-chain optimization. Premium furniture, forecast at a 5.21% CAGR, captures disposable-income growth among affluent households and luxury hotel specifications. Economy ranges satisfy budget-constrained renters and large public projects, whereas ultra-luxury niches rely on Italian or bespoke Gulf artisans.

Price-sensitive consumers welcome the 10% global reductions introduced by IKEA in 2024, prompting regional peers to review cost structures. Buy-now-pay-later and subscription models democratize premium access, lifting average ticket sizes without upfront cash strain. Customized finishes, such as in-store upholstery selection, blur price-bracket boundaries, letting retailers upsell ancillary services like on-site assembly.

By Distribution Channel: Retail Dominates as Digital Curates Choice

B2C outlets held a 75.53% share and will grow at a 5.44% CAGR as the primary gateway to the GCC furniture market. Large showrooms retain an advantage in tactile product evaluation, complementing online catalogues enriched with 360-degree imaging. B2B project channels cater to bulk orders for schools, hospitals, and hotels, leveraging volume discounts and specification compliance.

Digital channels accelerate discovery and reduce geographic barriers. Serial renovators use AR apps to visualize pieces in existing decor, pushing conversion uplifts. Logistics partners improve reverse logistics for returns, a crucial pain point in furniture e-commerce. Marketplace data analytics inform assortment curation, reducing slow-moving SKUs and freeing warehouse space for high-velocity items.

Saudi Arabia dominated with a 52.74% share of the GCC furniture market in 2024, underpinned by Vision 2030’s SAR 4.9 trillion infrastructure pipeline and a 4.4% construction growth rate in 2025. Riyadh issued contracts worth USD 54 billion, securing substantial demand across public-sector ministries, hospitals, and universities. Giga-projects such as NEOM and the Red Sea mandate high-specification FF&E packages, fostering long-term supplier frameworks. The Kingdom’s young, urbanizing population drives residential demand, while large expatriate communities sustain rental turnover.

The UAE registers the fastest projected expansion at a 4.24% CAGR, anchored by Dubai’s retail ambitions and Abu Dhabi’s Tourism Strategy 2030. Sobha Group’s 71,000 m² production facilities will deepen manufacturing competencies and introduce luxury craftsmanship to regional project pipelines. The Emirates’ logistics infrastructure enables re-export to Bahrain and Oman, smoothing supply for smaller markets and bolstering the country’s role as a distribution hub.

Qatar’s post-World-Cup environment preserves momentum: 40,405 hotel keys, 69% occupancy, and 29% RevPAR improvement translate into robust hospitality orders. Kuwait, Oman, and Bahrain maintain steady growth through residential modernization and commercial refurbishments. Franchise arrangements allow international brands to enter these markets cost-effectively, leveraging centralized GCC inventory hubs to overcome scale limitations.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

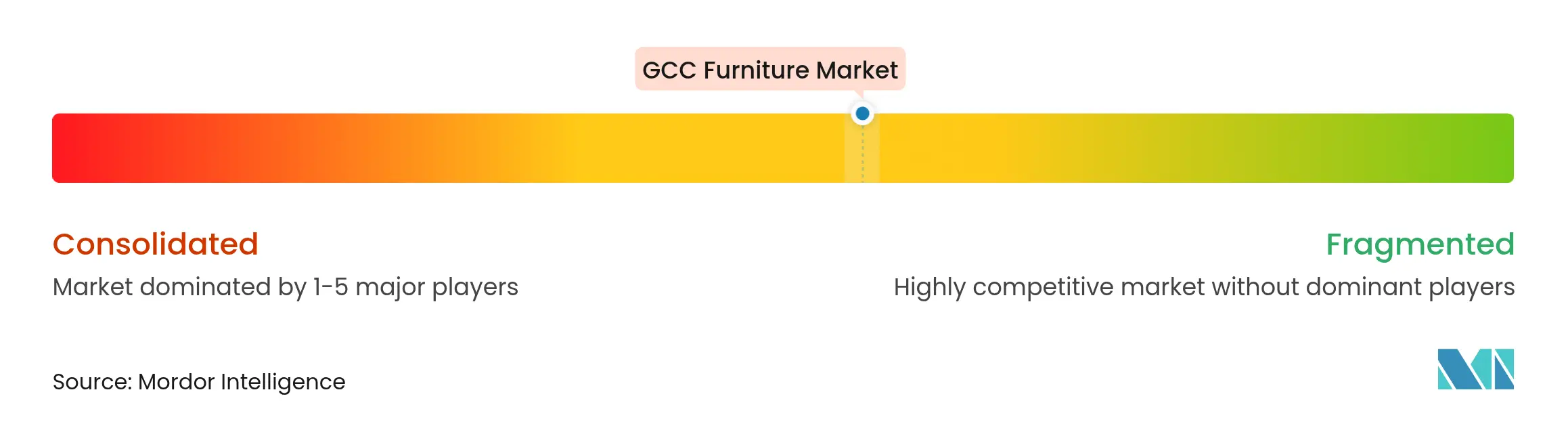

Market Concentration

The competitive landscape is moderately fragmented, with the leading five players holding a notable but not dominant portion of the market, creating ample space for niche and specialist brands. IKEA maintains a strong lead, backed by Al-Futtaim’s extensive distribution network and value-driven pricing strategy. Home Centre leverages its broad regional store presence and mid-market appeal to maintain a solid position, while Danube Home benefits from synergies with its project fit-out operations. Royal Furniture leverages in-house production to serve hospitality tenders, and Pan Emirates deploys fast-turn collections targeting fashion-driven consumers.

Global entrants heighten rivalry, particularly as omnichannel models reduce entry barriers. Digital tools ranging from AR showrooms to AI design engines emerge as differentiators, enabling personalized recommendations and shortened design-to-delivery cycles. Sustainability credentials influence tender outcomes, especially in hospitality, where brand standards demand eco-certifications. Leasing and subscription services are gaining traction, led by Dubai-based startups addressing expatriate mobility. Local factories expand output to capture regional content mandates, and foreign joint-ventures such as the TK Elevator–Alat partnership illustrate manufacturing localization trends.

Third-party marketplaces intensify price transparency, requiring retailers to streamline cost bases or emphasize experiential value. Partnerships with fintech providers expand consumer credit options while securing higher conversion rates. As price wars escalate, service quality, delivery punctuality, installation expertise, and after-sales support become an increasingly critical tiebreaker in brand selection.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts (Value in USD)

6. Competitive Landscape

7. Market Opportunities & Future Outlook

Moving objects that support a variety of human activities, including sleeping, eating, and sleeping and/or using an item, are referred to as furniture. The purpose of the report is to offer a thorough analysis of the GCC furniture market. It concentrates on market dynamics, new market tendencies in specialized markets and geographical regions, and insights into a broad range of product and application categories. It also looks at the leading businesses and market trends in the GCC for furniture.

The GCC furniture market is segmented by Application (Home Furniture, Office Furniture, Hospitality Furniture, and Other Furniture), by Material (Wood, Metal Plastic, and Others), by Distribution Channel (Home Centres, Flagship Stores, Specialty Stores, Online, and Other Distribution Channels), and by Country (United Arab Emirates, Saudi Arabia, Qatar, Kuwait, Oman, and Bahrain). The report offers Market size and forecasts for GCC Furniture Market in value (USD million) for all the above segments.

A Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

Strategic Expansion in the Russia Laundry Appliances Market

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.