Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

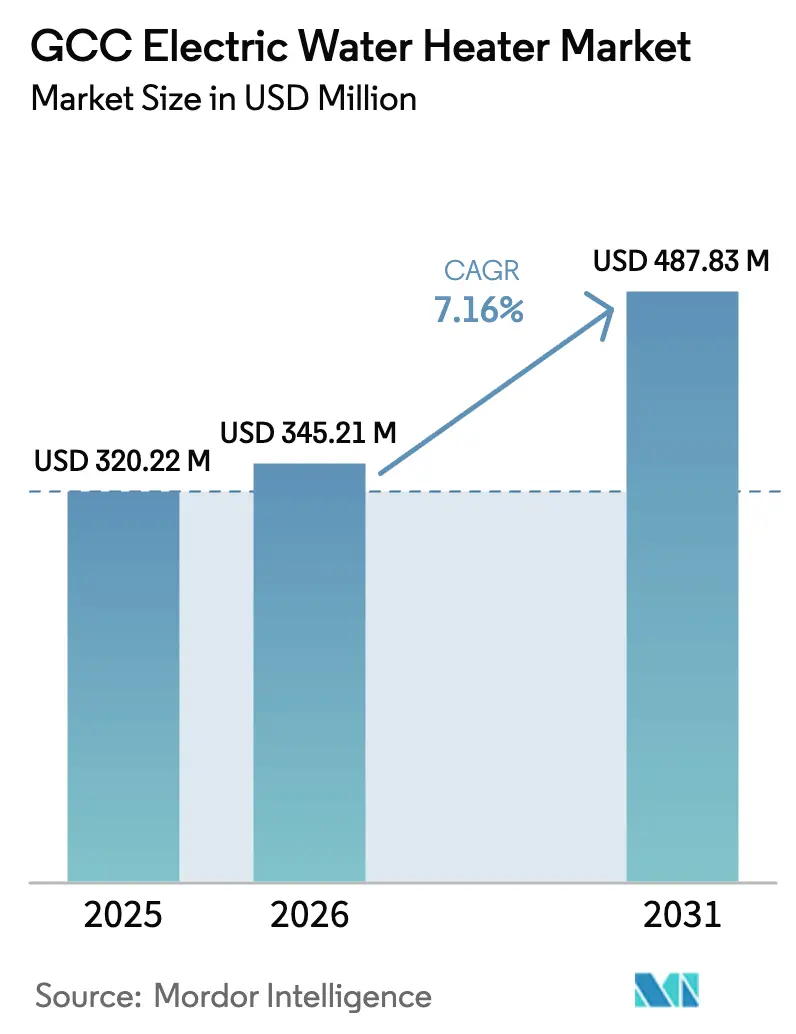

| Base Year Market Size (2025) | USD 320.22 Million |

| Market Size (2026) | USD 345.21 Million |

| Market Size (2031) | USD 487.83 Million |

| Growth Rate (2026 - 2031) | 7.16% CAGR |

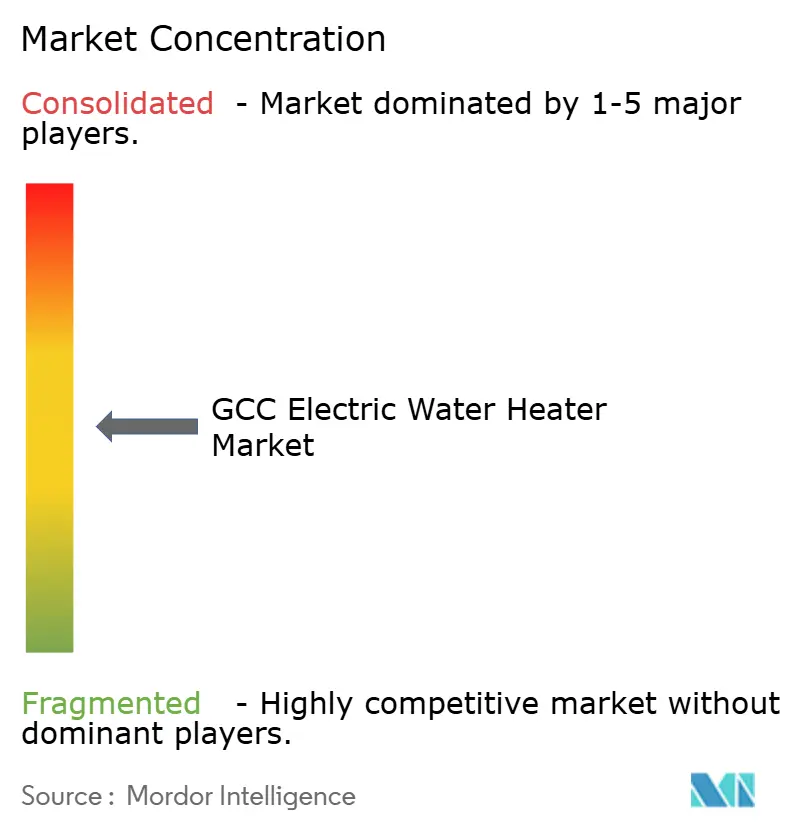

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Electric Water Heater Market Analysis by Mordor Intelligence

The GCC electric water heater market size is expected to increase from USD 320.22 million in 2025 to USD 345.21 million in 2026 and reach USD 487.83 million by 2031, growing at a CAGR of 7.16% over 2026-2031. The GCC electric water heater market benefits from sustained residential construction supported by Saudi Arabia’s Sakani program and Dubai’s population growth agenda, and it gains further momentum from mandatory efficiency labeling and minimum performance standards that shape product portfolios across storage, tankless, and heat pump categories[1]GSO Secretariat, “GSO 2770:2024 Minimum Energy Performance Standards for Water Heaters,” GCC Standardization Organization, gso.org.sa . As mixed-use, hospitality, and healthcare projects expand, buyers emphasize faster recovery, lower operating costs, and compliance readiness, which lift demand for tankless and heat pump systems, especially in high-rise and retrofit settings. The GCC electric water heater market is also shaped by water-quality constraints in desalination-heavy geographies, which intensify corrosion risks and steer buyers toward anode-free or titanium-anode solutions with longer service intervals. Competitive intensity remains moderate, with global brands scaling local compliance and manufacturing and regional players competing on speed, service, and cost alignment with GCC standards.

Key Report Takeaways

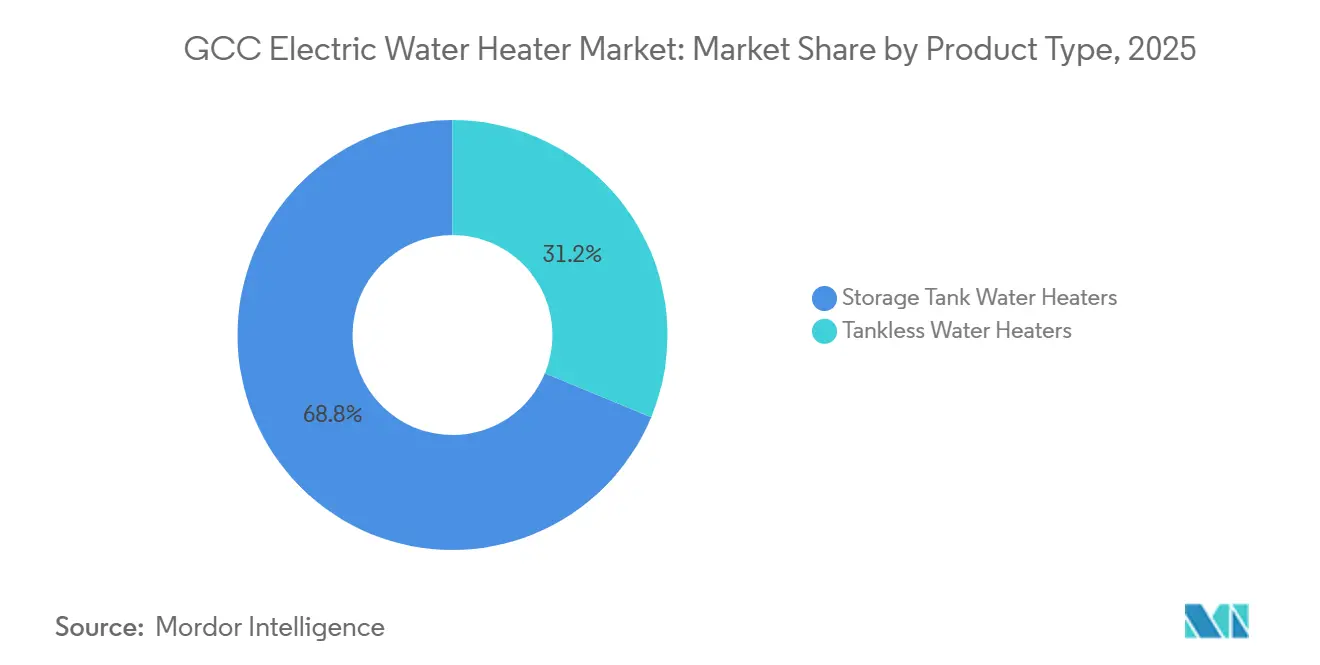

- By product type, storage tank systems led with 68.76% of the GCC electric water heater market share in 2025, while tankless variants are projected to expand at an 8.18% CAGR through 2031.

- By capacity, medium-sized units held 47.73% of the GCC electric water heater market share in 2025, whereas small units are forecast to grow at a 7.26% CAGR through 2031.

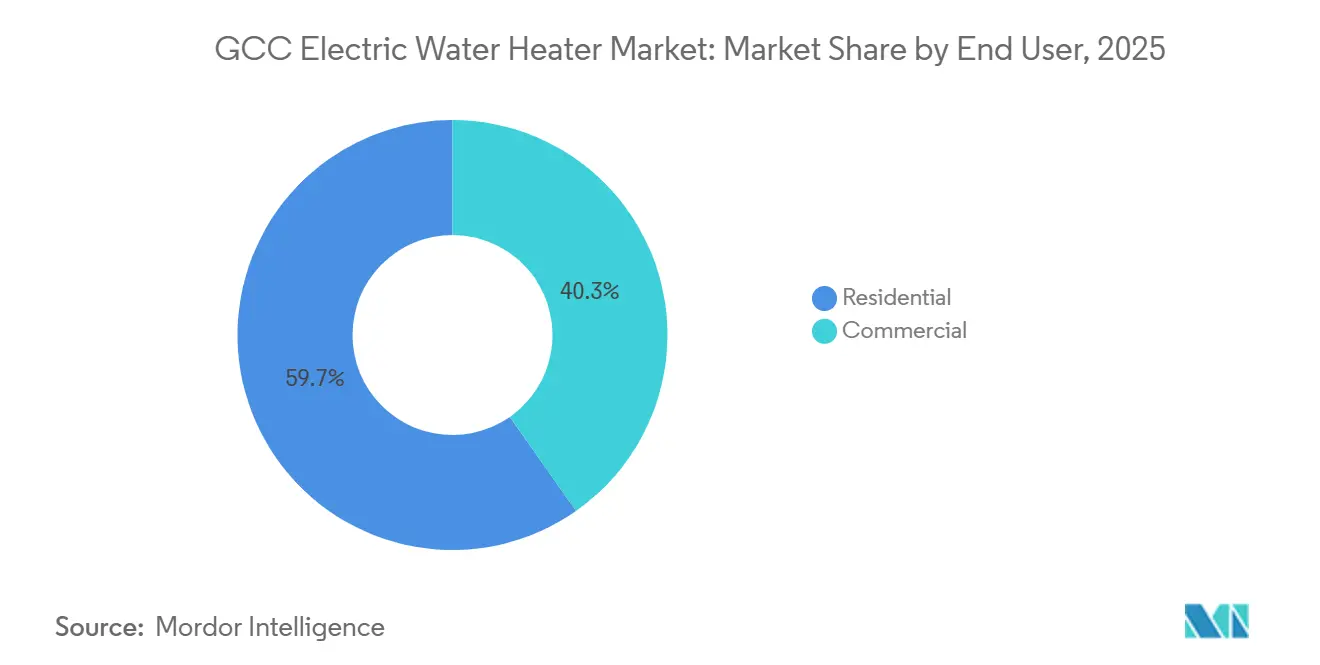

- By end user, residential accounted for 59.73% of the GCC electric water heater market share in 2025, while commercial is projected to expand at a 6.27% CAGR through 2031.

- By distribution channel, offline captured 65.84% of the GCC electric water heater market share in 2025, whereas online platforms are expected to grow at a 9.43% CAGR through 2031.

- By geography, Saudi Arabia held 51.27% of the GCC electric water heater market share in 2025, while the United Arab Emirates is projected to expand at a 7.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC Electric Water Heater Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Housing program-fueled residential construction | +1.8% | Saudi Arabia and the UAE | Medium term (2–4 years) |

| Mandatory energy-efficiency labeling and standards | +1.3% | GCC-wide | Short term (≤ 2 years) |

| Rapid hotel and healthcare pipeline boosting commercial demand | +1.2% | UAE core, Saudi spillover | Medium term (2–4 years) |

| Replacement demand from the aging installed base | +0.9% | GCC-wide | Long term (≥ 4 years) |

| Heat pumps and smart controls are reducing operating costs | +1.0% | UAE and Saudi Arabia | Medium term (2–4 years) |

| Electrification of DHW in light industry and mixed-use projects | +0.8% | GCC-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Housing Program-Fueled Residential Construction

Saudi Arabia’s Sakani program has provided support to more than one million families since the launch of Vision 2030, lifting national homeownership above 60% by 2022 and targeting 70% by 2030. These policy outcomes sustain demand for mid-range electric storage water heaters in 30–80-liter brackets as financing translates into steady handovers and fit-outs in major cities[2]Vision 2030 Office, “Saudi Vision 2030 Housing Programs,” Vision 2030, vision2030.gov.sa. In the UAE, contracts awarded between 2020 and August 2025 totaled USD 328.7 billion, with residential real estate accounting for 28% of the construction pipeline, supporting recurring demand in apartments and villas. Mixed-use developments that represent a significant share of future projects are shifting specifications toward compact tankless and heat pump units that align with Estidama, Al Sa’fat, and Barjeel frameworks in local markets. A UAE high-rise case study using Ariston heat pump water heaters lowered connected electrical load from 508.8 kW to 178.4 kW, reducing connection fees by AED 660,800 (USD 179,932) and annual running costs by AED 193,000 (USD 52,553).

Mandatory Energy-Efficiency Labeling and Standards

Mandatory energy-efficiency labeling and standards across GCC countries are driving demand for advanced electric water heaters. Regulatory frameworks encourage manufacturers to develop energy-efficient models, while consumers increasingly prefer labeled products to reduce electricity costs. These policies support sustainability goals and accelerate the replacement of older, inefficient systems with compliant, high-performance alternatives. SASO 2884:2017/AMD4:2021 mandates energy labels for electric storage and instantaneous water heaters, including declared load profiles and consistent testing parameters for compliance and market entry. GSO 2770:2024, approved at the GCC level, establishes Minimum Energy Performance Standards for electric storage, instantaneous, heat pump, and solar heaters up to 70 kW and 2,000 liters, harmonizing thresholds across member states while allowing national variations where applicable. The unified GCC Conformity Mark framework requires the GSO Conformity Tracking Symbol and digital traceability through the Hazm platform, ensuring that higher-risk electrical products complete type examination and factory audits before placement on the market. These requirements accelerate the phaseout of sub-MEPS inventory and reward brands that invest in accredited testing and in-region compliance workflows. Third-party testing scope expansions, such as Oman's DGSM accreditation with UL Solutions Demko A/S in late 2025, reinforce enforcement and shorten approval cycles as suppliers update portfolios. In practice, these rules shift purchasing toward higher-efficiency storage models, tankless systems with improved controls, and heat pumps in retrofit and new-build contexts[3]Dubai Electricity and Water Authority, “Regulations for Solar Water Heaters in Villas,” DEWA, dewa.gov.ae .

Rapid Hotel and Healthcare Pipeline Boosting Commercial Demand

Dubai is building 8.2 million square feet of office space for delivery by 2028, while Abu Dhabi indicates a surge of new office stock in 2027, which underpins steady commercial demand for systems that deliver continuous hot water with minimal downtime. Hospitality anchors such as signature mixed-use resorts prioritize uptime and rapid recovery, making tankless electric and modular heat pump systems a default choice in detailed specifications. Healthcare investments aligned with Vision 2030 require redundant DHW loops and hygienic temperature controls that favor premium product lines with sterilization support. Ariston’s regional heat pump line with COP 3+ and smart Wi-Fi controls targets this need set in new builds and retrofits, enabling remote scheduling and optimization. Commercial procurement teams increasingly bundle equipment, documentation, and service into a single process that includes BIM models and compliance certificates accessible before tender. As these workflows standardize across mega-projects and mixed-use towers, the commercial share gains momentum within the GCC electric water heater market.

Replacement Demand from the Aging Installed Base of Storage Heaters

The average lifespan of conventional electric storage heaters in the GCC is compressed by high-TDS desalinated water, which accelerates anode depletion and internal corrosion that leads to tank failure. Water-quality conditions, particularly in coastal Saudi Arabia, increase maintenance frequency and replacement rates, which support steady aftermarket demand for residential and commercial units. To counter corrosion, brands offer proprietary solutions such as titanium-anode systems and anode-free designs that extend service intervals and reduce unplanned downtime. Local manufacturing upgrades to Industry 4.0 production with anti-corrosion coatings have increased output capacity and diversified models tailored for high-TDS environments. Replacement cycles from earlier construction waves are now entering end-of-life support heat pump retrofits in villas and premium apartments, where energy savings offset the higher first cost. This dynamic supports a sustained base of recurring revenue for distributors and service partners in the GCC electric water heater market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from gas and solar thermal in select projects | -0.6% | Saudi Arabia and the UAE | Short term (≤ 2 years) |

| Higher upfront cost for heat pumps and tankless units | -0.5% | GCC-wide | Medium term (2–4 years) |

| Water-quality scale and corrosion increase maintenance costs | -0.3% | GCC-wide, high-TDS zones | Medium term (2–4 years) |

| Installer availability varies across micro-markets | -0.2% | Smaller emirates and secondary Saudi cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from Gas and Solar Thermal Alternatives in Select Projects

Pipeline networks and legacy project designs can favor gas-fired hot water in compounds and facilities where local tariffs, existing infrastructure, or engineered standards already tilt the balance against fully electric systems. Rooftop solar thermal systems mandated for Dubai villas reinforce this restraint in low-rise detached housing, where collectors fit well on available roof space. Developers targeting net-zero or near-zero operating profiles sometimes specify hybrid architectures that rely on thermal collection as a primary source with an electric boost for reliability[4]Saudi Water Authority, “Water Quality Standards and Monitoring,” Saudi Water Authority, swa.gov.sa. Under certain design and tariff assumptions, the lifecycle economics of solar thermal can be competitive in villas with favorable orientation and minimal shading. Electric systems retain an edge in high-rise and multi-family buildings due to roof area constraints per dwelling and in retrofits where structural conditions limit collector installation.

Higher Upfront Cost for HPWH and Tankless vs. Basic Storage Units

Premium systems such as heat pumps and tankless heaters command higher purchase prices than standard storage designs, which slows adoption in mass housing that prioritizes initial capital budgets. Specifiers in value-engineered projects often revert to compliant storage heaters to protect margins unless green-building points or operational budgets are weighted in the decision. Commercial buyers with larger daily hot water loads are more likely to evaluate the total cost of ownership and payback, which favors premium systems in hotels and healthcare. Some tankless installations require higher-capacity electrical circuits than legacy storage replacements, which introduces panel upgrade and wiring costs that can deter retrofits. Embedded retail financing options spread the initial outlay for homeowners acquired through e-commerce channels, which helps premium models gain traction despite higher starting prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: On-Demand Recovery Drives Tankless Surge in High-Density Urban Cores

Storage tank systems accounted for 68.76% of revenue in 2025 within the GCC electric water heater market, while tankless models are forecast to post an 8.18% CAGR through 2031 from a smaller base. Storage remains prevalent due to lower first cost, installer familiarity, and compatibility with existing infrastructure across new-build and retrofit contexts. Tankless models grow faster where space is tight, recovery speed is important, and standby losses need reduction in luxury apartments and hospitality suites. Modular tankless architectures enable cascaded installations to meet peak loads with better utilization, which supports uptake in commercial kitchens and spas that need swift temperature stabilization. Leading portfolios adapt to Gulf water chemistry with anti-scale features and corrosion control that preserve efficiency and extend service intervals in hard-water conditions.

Heat pump water heaters create a premium subcategory within storage, where COP 3+ performance and smart controls help reduce operating costs in villas and high-end retrofits. Brands are also aligning product testing with SASO Energy Efficiency Labeling and the GCC G-Mark system to streamline approvals under unified compliance workflows. In-region manufacturing investments and regional service networks shorten lead times and enable faster product updates that reflect evolving standards. This execution focus supports broader choice across storage, tankless, and heat pump systems in the GCC electric water heater industry, encouraging channel partners to match product features to project requirements.

By Capacity: Compact Units Gain as Studio and One-Bedroom Inventory Expands

Medium-sized units around 50–100 liters held a 47.73% share in 2025, reflecting the capacity range favored in villas and two-to-three-bedroom apartments across major GCC cities. Small-capacity units under 50 liters are projected to grow at a 7.26% CAGR as densification adds studios and one-bedroom apartments near transit and employment centers. Large-capacity formats above 100 liters serve multi-bathroom villas, hospitality, and healthcare use cases that demand redundancy or extended draw profiles. Tankless products disrupt traditional capacity definitions by shifting sizing from stored volume to flow rate, which allows designers to right-size systems based on peak fixtures and diversity factors.

Water chemistry is a factor in effective capacity over time, as scale can reduce flow and heat transfer in high-TDS zones unless mitigated by product design. Anode-free and titanium-anode designs aim to preserve performance throughout service life, which sustains rated output in homes and small commercial sites. As unit mixes evolve with housing formats, contractors emphasize serviceability and total lifecycle cost to recommend capacity categories that balance draw patterns and energy savings within the GCC electric water heater industry.

By End User: Commercial Retrofit Pipelines Narrow the Residential Lead

Residential applications represented 59.73% of demand in 2025, supported by household formation and handovers in flagship housing programs as well as continuing demand in apartments and villas. Commercial demand is accelerating at a 6.27% CAGR through 2031 as hospitality, healthcare, and mixed-use projects require uptime, control integration, and documented compliance for tender processes. Hotels, clinics, and office towers value tankless and heat pump systems that reduce recovery time and energy use, especially where operating schedules can leverage off-peak tariffs. This shifts commercial procurement toward premium models and service contracts in the GCC electric water heater market.

Residential retrofits, particularly in villa communities, lean toward heat pump replacements to capture material energy savings without reworking plumbing or electrical systems substantially. Commercial buyers centralize procurement and maintenance, which pushes platforms and distributors to deliver documentation packs that include BIM files and certificates. Product differentiation that addresses high-TDS risks is a shared theme across both segments because water quality influences maintenance cycles and operating costs. These patterns together shape how the GCC electric water heater market serves end users with distinct usage and budget profiles.

By Distribution Channel: E-Commerce Platforms Capture Millennial Home Improvement Spend

Offline channels accounted for 65.84% of revenue in 2025, anchored by consultant specifications, contractor networks, and the need for coordinated delivery, installation, and warranty service. Online platforms are projected to grow at a 9.43% CAGR, aided by transparent product data, energy labels, and same-day delivery in metro zones that serve replacement demand and elective upgrades. Embedded payment options and customer reviews increase confidence in higher-priced products, which supports premium adoption for tankless and heat pump models purchased online. B2B portals deepen reach into contractor and facilities segments by offering compliance documents and digital procurement workflows that align with project timelines.

Offline partners retain advantages in commercial new-builds where logistics, site coordination, and after-sales service are bundled into a single award. In remote micro-markets, distributor networks reduce last-mile complexity and preserve service levels during warranty periods. The mix of offline and online channels reflects buyer preferences by segment, with digital transparency and financing supporting premium upgrades, while project-based work remains relationship-driven in the GCC electric water heater market.

Geography Analysis

Saudi Arabia accounted for 51.27% of the GCC electric water heater market in 2025, supported by Vision 2030 housing policies that raised homeownership and delivered sustained residential fit-out demand. Energy-efficiency rules require visible labels and defined load profiles, steering portfolios toward compliant models suited to national testing conditions. Manufacturing upgrades in the Kingdom, including high-volume Industry 4.0 lines with anti-corrosion enhancements, increase supply resilience and reduce lead times for local channels. Grid reliability improvements contribute to confidence in electric systems for domestic hot water in large projects and mixed-use developments. Water quality remains a design and maintenance factor, which pushes more buyers to consider anode-free or titanium-anode systems.

The United Arab Emirates is the fastest-growing geographic segment with a 7.42% forecast CAGR through 2031, underpinned by urban planning and a pipeline that includes significant residential and mixed-use projects. Office, hospitality, and healthcare investments increase demand for systems that maintain hot water continuity with intelligent controls and lower operating costs. Solar water heater requirements in villas shape product choices in low-rise housing, while electric systems expand in high-rise and retrofits where roof space and structural constraints apply. The G-Mark system and its digital tracking requirements streamline cross-border product compliance, which accelerates updates to higher-efficiency models in the local channel mix.

Kuwait, Oman, Qatar, and Bahrain comprise the remainder of the GCC, with growth shaped by population bases, project intensity, and the pace of standards adoption under the regional framework. Regional bodies have advanced the digitalization of conformity processes, which supports coordinated enforcement and lowers the risk of non-compliant products in smaller markets. Oman’s testing scope expansion with UL Solutions tightened market access and improved product quality controls, which affects importers and in-region assemblers. Local suppliers in these markets compete on quick delivery and robust documentation to address replacement and project-driven demand. These dynamics ensure that the GCC electric water heater market remains responsive to national codes and procurement styles while moving toward higher efficiency tiers.

Competitive Landscape

The GCC electric water heater market shows moderate concentration, with the top five suppliers holding about half of the combined share in 2025 across aggregated regional datasets. Global brands strengthen capabilities through acquisitions that expand integrated HVAC and DHW offerings, which improve their ability to bid for complex mixed-use and industrial packages. Local manufacturers invest in production technologies that enable high output and corrosion-resistant designs tailored to desalination-heavy markets. These moves raise baseline product quality and expand choices for consultants and contractors across storage, tankless, and heat pump categories.

Strategic initiatives highlight heat pump and smart-control portfolios, with Wi-Fi features and COP 3+ ratings aimed at villas, hotels, and clinics seeking energy savings and uptime. Vendors with in-region testing and documentation readiness move faster through compliance gates, which shortens time to market under SASO and G-Mark rules. Suppliers differentiate on water-quality resilience with titanium-anode and anode-free tanks designed for high-TDS conditions that extend service life and stabilize maintenance cycles. New manufacturing bases in nearby countries improve logistics for GCC demand and help align portfolio refresh cycles with regulatory updates.

Emerging players scale through channel breadth and localized offerings, while established brands emphasize digital procurement and after-sales service for commercial accounts. As product compliance tightens and procurement digitizes, the competitive field remains open to both premium and value-based strategies that meet distinct buyer needs in the GCC electric water heater market. Portfolio diversity supports consultants who match features to building codes and project goals, which keeps specifications dynamic across residential and commercial work. Developers continue to pursue combinations of efficiency, corrosion resistance, and service support, which guide vendor selections in bids and frameworks.

GCC Electric Water Heater Industry Leaders

Ariston Group

A. O. Smith MEA

Rheem Middle East & Africa

Saudi Ceramics Company

Orbital Horizon

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Ariston Group launched local production of water heaters at its new facility in Egypt's 6th of October City, manufacturing storage and instant models for African and Middle Eastern markets with proprietary anti-corrosion technology, reducing regional lead times and ensuring SASO and GSO compliance within North African and GCC logistics networks.

- August 2025: Haier Smart Home reported that overseas water heater sales doubled year-on-year following an acquisition and the rollout of magnesium-rod-free electric models featuring 56°C sterilization, AI cleaning systems to prevent scale, and IoT modules enabling remote diagnostics and predictive maintenance.

- July 2025: Bosch acquired Johnson Controls' global residential and light commercial HVAC business for USD 8 billion, expanding its Thermotechnology portfolio to include integrated DHW, heat recovery ventilation, and solar pre-heat packages, positioning the combined entity to bundle electric tankless heaters with HVAC systems in GCC mixed-use and light industrial projects.

- December 2024: Oman's Directorate General for Standardization and Metrology expanded its accredited testing scope to include water heaters, partnering with UL Solutions Demko A/S for third-party verification of GSO and local energy-efficiency requirements, tightening enforcement of Minimum Energy Performance Standards, and accelerating the removal of non-compliant imports from Omani retail channels.

GCC Electric Water Heater Market Report Scope

Electric water heaters rely on electricity rather than gas to heat water for residential and commercial use. The GCC Electric Water Heater Market is segmented by product type, capacity, end-user, distribution channel, and geography. By product type, the market is divided into storage tank water heaters and tankless water heaters. By capacity, the market is categorized into small, medium, and large water heaters. By end-user, the market is segmented into commercial and residential segments. By distribution channel, the market is divided into online and offline channels. Geographically, the market analysis covers Saudi Arabia, the United Arab Emirates, Kuwait, Oman, Qatar, and Bahrain. The report provides market size and forecasts for the GCC electric water heater market in value (USD) across all the above segments.

By Product Type

| Storage Tank Water Heaters |

| Tankless Water Heaters |

By Capacity

| Small |

| Medium |

| Large |

By End Users

| Commercial |

| Residential |

By Distribution Channels

| Online |

| Offline |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Kuwait |

| Oman |

| Qatar |

| Bahrain |

| By Product Type | Storage Tank Water Heaters |

| Tankless Water Heaters | |

| By Capacity | Small |

| Medium | |

| Large | |

| By End Users | Commercial |

| Residential | |

| By Distribution Channels | Online |

| Offline | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Kuwait | |

| Oman | |

| Qatar | |

| Bahrain |

Key Questions Answered in the Report

What is the current size and near-term growth outlook for the GCC electric water heater market?

The GCC electric water heater market size is expected to increase from USD 320.22 million in 2025 to USD 345.21 million in 2026 and reach USD 487.83 million by 2031 at a 7.16% CAGR over 2026-2031.

Which product types are leading and which are growing the fastest in the GCC electric water heater market?

Storage tank systems led with 68.76% revenue share in 2025, while tankless models are projected to post the fastest growth at an 8.18% CAGR through 2031.

Which end users and channels are shaping demand in the GCC electric water heater market?

Residential held 59.73% in 2025, while commercial is growing at 6.27% CAGR, and offline channels captured 65.84% with online platforms expanding at 9.43% CAGR.

How do GCC efficiency regulations and labeling impact product selection?

SASO and GSO requirements enforce visible labels and MEPS compliance, which shift portfolios toward higher-efficiency storage, tankless, and heat pump models and accelerate the retirement of sub-MEPS inventory.

Which GCC geography leads, and where is growth strongest?

Saudi Arabia held 51.27% of the GCC electric water heater market in 2025, while the United Arab Emirates is forecast to grow the fastest at a 7.42% CAGR through 2031.

What features are most in demand for premium upgrades in the GCC electric water heater market?

Heat pump systems with COP 3+ and smart Wi-Fi controls, along with corrosion-resistant tanks and service-ready documentation, are most sought after for hotels, clinics, and villas.

Page last updated on: