Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

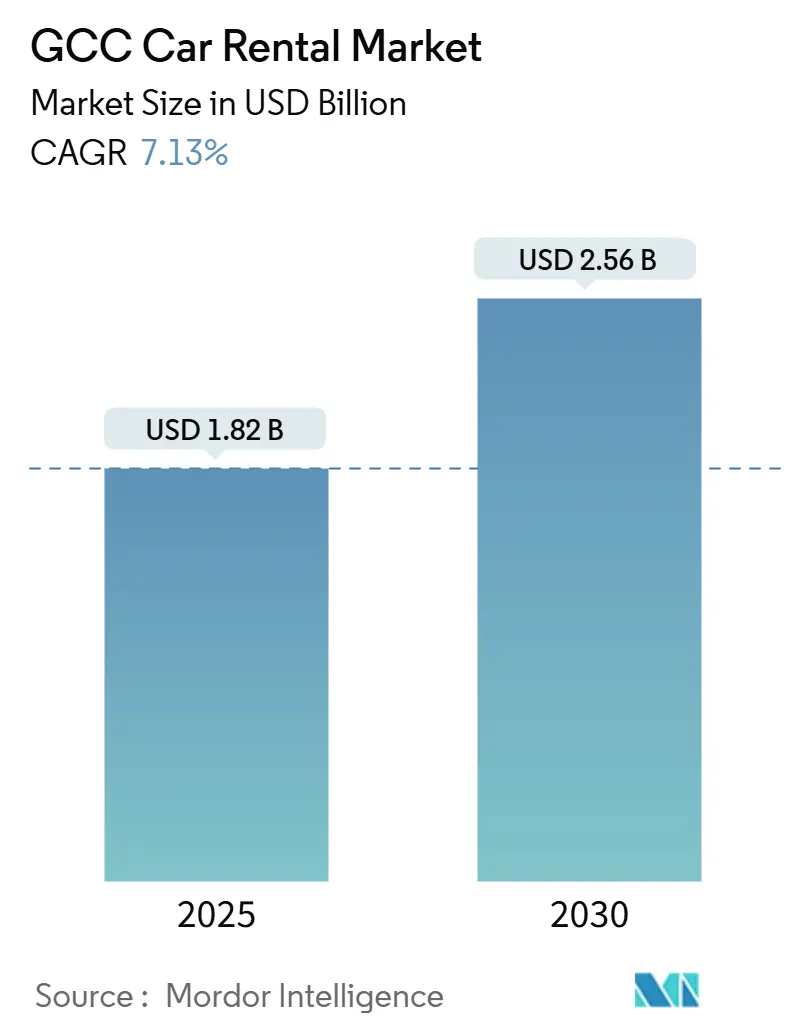

| Market Size (2025) | USD 1.82 Billion |

| Market Size (2030) | USD 2.56 Billion |

| Growth Rate (2025 - 2030) | 7.13% CAGR |

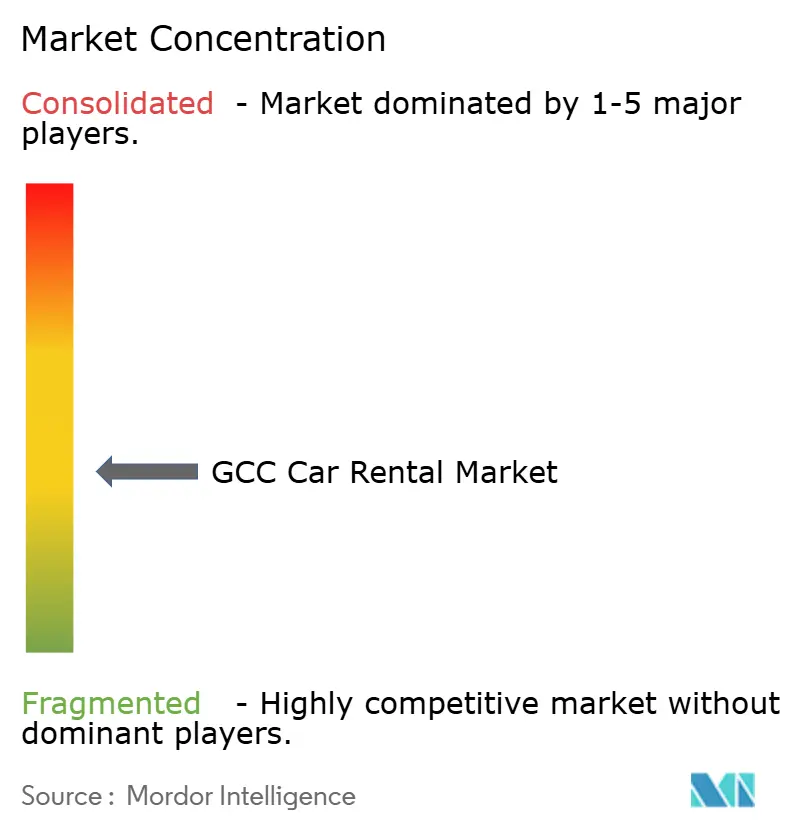

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

GCC Car Rental Market Analysis by Mordor Intelligence

The GCC car rental market is valued at USD 1.82 billion in 2025 and is forecast to expand at a 7.13% CAGR, lifting revenue to USD 2.56 billion by 2030. This growth mirrors the region’s commitment to tourism-led diversification, the rapid rise of super-apps, and an unmistakable preference for access rather than ownership. Greater airline seat capacity, cross-border weekend travel, and increasingly flexible corporate mobility budgets reinforce the sector’s resilience. At the same time, integrating rental services into digital ecosystems and subscription platforms is reshaping competitive moats, while rising electric-vehicle (EV) incentives promise new revenue streams for operators prepared to retool their fleets.

Key Report Takeaways

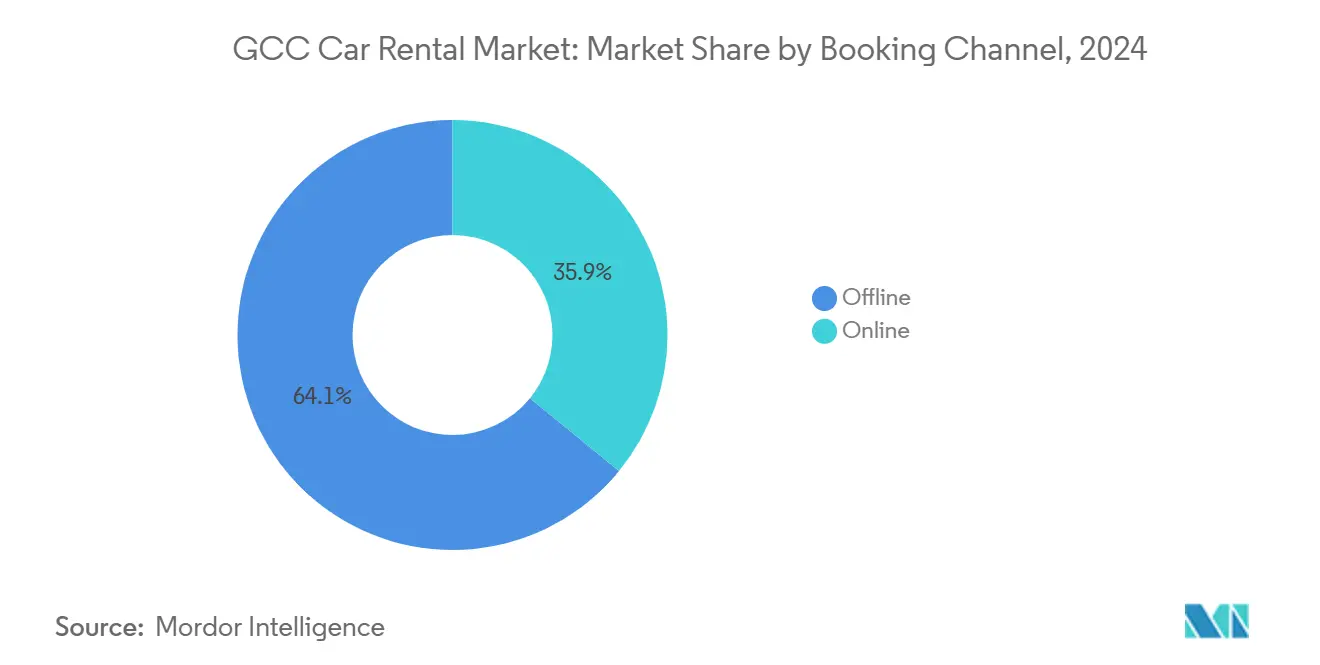

- By booking channel, offline counters retained 64.13% of the GCC car rental market share in 2024; online platforms are on track to rise at a 7.42% CAGR to 2030.

- By rental duration, short-term bookings captured 71.28% of the GCC car rental market size in 2024, while long-term and operating leases will advance at 7.75% CAGR between 2025-2030.

- By vehicle type, sedans dominated the GCC car rental market, with 38.65% of the share in 2024; SUVs and luxury models are poised for the quickest 7.21% CAGR to 2030.

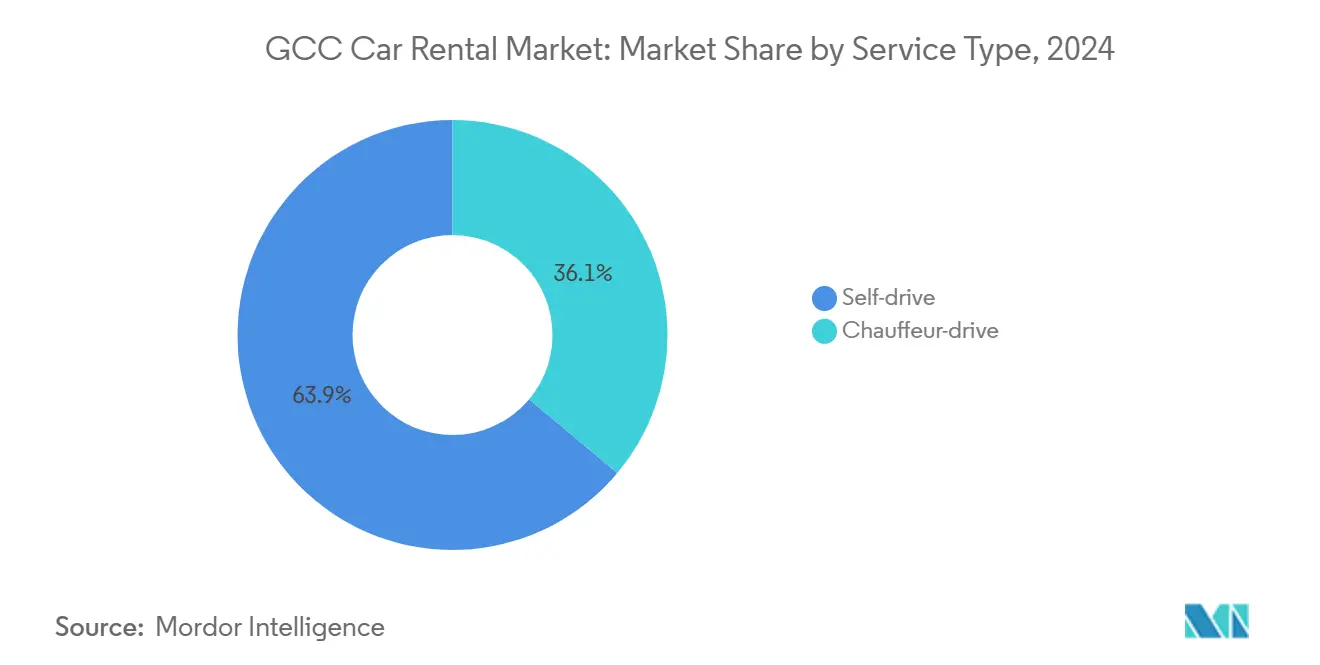

- By service type, self-drive rentals commanded 63.89% of the GCC car rental market share in 2024 and are expanding at 7.88% CAGR through 2030.

- By end-user, individuals held 48.76% of the GCC car rental market share in 2024, but the corporate segment will outpace at 7.47% CAGR to 2030.

- By country, the United Arab Emirates led with 39.94% of GCC car rental market share in 2024, whereas Saudi Arabia is projected to record the fastest 7.71% CAGR through 2030.

GCC Car Rental Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tourism rebound | 1.8% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Government Vision programs | 1.5% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Rising digital aggregation platforms | 1.2% | Global, with UAE and Saudi Arabia leading | Short term (≤ 2 years) |

| Gig-economy demand for flexible wheels | 0.9% | UAE, Saudi Arabia core, spill-over to Kuwait | Short term (≤ 2 years) |

| EV adoption incentives | 0.7% | UAE, Saudi Arabia | Long term (≥ 4 years) |

| Cross-border one-way rentals | 0.4% | UAE-Oman, Saudi-Bahrain corridors | Medium term (2-4 years) |

Source: Mordor Intelligence

Tourism rebound & mega-events pipeline

Gulf governments have synchronized a calendar of global spectacles ranging from Formula 1 races to World Cups, each generating predictable surges that rental companies meet through dynamic pricing and fleet redeployment. Saudi Arabia’s target of 150 million annual visits by 2030 and the UAE’s aim for 40 million overnight stays anchor long-range demand visibility. Dubai welcomed 9.3 million visitors in H1 2024, a 9% year-on-year lift, prompting Dubizzle to debut a dedicated aggregation service to capture the influx.[1]Dubai Department of Economy and Tourism, “Dubai Tourism Performance H1 2024,” det.gov.ae Qatar’s experience during the 2022 World Cup revealed both upside—Careem briefly scaled cross-border ride services—and downside risk once the event concluded. Continuous investments in airports and entertainment precincts entrench car rentals as indispensable infrastructure for the visitor economy.

Government Vision programs boosting inbound mobility

Policy frameworks embedded in Saudi Vision 2030 and the UAE Energy Strategy 2050 couple tourism and sustainability goals with regulatory clarity. Saudi Arabia’s Ministry of Transport has codified rules for leasing brokers, enabling scale while Qatar and Bahrain publish visitor targets of 7.1 million and 14.1 million respectively.[2]Ministry of Transport Saudi Arabia, “Regulations on Vehicle Leasing and Broker Activities 2025,” mot.gov.sa UAE authorities simplify cross-border mobility by recognizing GCC licenses, thereby enlarging the addressable tourist pool. Procurement guidelines that favor hybrid or electric fleets incentivize operators to green their inventories, a move that also appeals to corporate clients pursuing ESG metrics.

Rising digital aggregation platforms & super-apps

Super-apps such as Careem now bundle more than a dozen services, including car rental partnerships with Swapp, which compress acquisition costs and lift utilization by keeping users inside a single interface. Dubizzle’s October 2024 rollout leverages a combined 73% share of online automotive marketplaces with DubiCars, underscoring the power of platform economics. Subscription specialists like invygo, backed by USD 1.9 million in recent funding, signal consumer comfort with flexible access models. While small operators gain visibility without heavy marketing spend, established brands face margin pressure as platforms wedge themselves between renter and customer, turning brand equity into a commodity unless firms upgrade their own direct-to-consumer channels.

Gig-economy demand for flexible wheels

Udrive, which surpassed 2 million trips and attracted USD 5 million from Cultiv8 and Oman Holding International, is emblematic of the micro-rental wave reshaping urban transport. Young professionals in Riyadh and Jeddah lean on subscription models for delivery and ride-sharing work, treating vehicles as income-generating tools. Pay-per-minute schemes bridge the affordability gap between daily rentals and ride-hailing, optimizing costs for drivers who work in bursts rather than full shifts. The MENA ride-share sector is projected to grow exponentially through 2028, links directly to incremental rental demand as drivers rotate between owned cars, rentals, and on-demand leases.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High insurance premiums | -1.1% | UAE, Qatar, Kuwait | Short term (≤ 2 years) |

| Fragmented regulatory rules | -0.8% | Global GCC, with cross-border operations most affected | Medium term (2-4 years) |

| Limited secondary market | -0.5% | UAE, Saudi Arabia | Long term (≥ 4 years) |

| Shortage of Arabic UX in global OTAs | -0.3% | Global GCC, with Saudi Arabia and UAE most affected | Short term (≤ 2 years) |

Source: Mordor Intelligence

High insurance premiums on expatriate drivers

UAE motor premiums climbed 40% in 2024, with rental vehicle cover leaping from 2% to 8.5% of asset value. Expatriates pay additional surcharges due to limited local driving histories, compressing operator margins or inflating retail prices. The wider GCC insurance sector is propelled by IFRS 17 compliance costs and reinsurer hardening that flows through to end-customers. Extreme weather loss events amplify claims severity, and when combined with cross-border cover needs, insurers frequently attach bespoke riders that elevate premiums on multi-jurisdiction rentals.

Fragmented regulatory rules across emirates/kingdoms

A mosaic of licensing, vehicle specification, and insurance mandates forces operators to maintain separate compliance regimes for each jurisdiction. Differences extend to emirate level inside the UAE and persist across Saudi Arabia, Qatar, Oman, and Bahrain, complicating fleet allocation and administrative processes. For customers, uneven rules dilute one-way rental convenience because paperwork and coverage rarely align across borders. The absence of unified digital payment standards further obliges companies to duplicate back-office systems, raising operational cost and dampening cross-border growth.

Segment Analysis

By Booking Channel: Offline dominance endures, yet digital platforms accelerate

The GCC car rental market retains a 64.13% offline share in 2024, underscoring the appeal of face-to-face interaction for first-time visitors and corporate bookers who favor in-person verification of vehicle condition and insurance coverage. Nevertheless, online channels are on course for a 7.42% CAGR, bolstered by super-apps that promise frictionless reservations in under 60 seconds. Young leisure travelers value transparent pricing and the ability to sync car pick-up with flight itineraries inside the same app, while corporate mobility managers begin to adopt dashboards that consolidate reservation data for expense control.

Dubizzle’s entry in October 2024 immediately broadened digital supply, exploiting its marketplace traffic to funnel tourists—Dubai recorded 9.3 million arrivals in H1 2024—into rental bookings. Zero-commission innovators such as Drife illustrate how aggregator economics may compress commissions further, threatening traditional intermediaries. Still, offline counters continue to shine for premium bookings where renters demand bespoke packages, additional insurance clarifications, or luxury vehicle upgrades negotiated on the spot. The coexistence of channel models suggests that the GCC car rental market will evolve into a hybrid ecosystem rather than a pure-play digital environment.

Note: Segment shares of all individual segments available upon report purchase

By Rental Duration: Short-term leadership, but long-term leasing gathers pace

Short-term contracts generated 71.28% of the GCC car rental market size in 2024, buoyed by holidaymakers, business travelers, and weekend shoppers crossing borders within the bloc. Yet long-term and operating leases outstrip in growth, advancing at 7.75% CAGR because corporates embrace asset-light approaches that free balance sheets from depreciation expenses. Regional corporations and project contractors now bundle maintenance, insurance, and telematics in twelve-month contracts that can be upsized or downsized as head-count fluctuates.

This structural pivot is mirrored in the subscription boom led by IndyGo, which raised USD 1.9 million to extend all-inclusive packages across Saudi Arabia and the UAE. Long-term clients prioritize total cost of mobility rather than day rates, rewarding operators who offer predictive maintenance and downtime guarantees. For short-term renters, fleet breadth and airport counter efficiency remain decisive. The coexistence of both duration types underlines how the GCC car rental market accommodates tourist spontaneity while simultaneously embedding itself into corporate supply chains.

By Vehicle Type: Sport Utility Vehicle categories climb the ladder

Sedans accounted for 38.65% of the GCC car rental market share in 2024 due to their fuel efficiency and comfort profile desired by cost-conscious tourists and executives alike. Sport Utility Vehicle marques are forecast to post a 7.21% CAGR, encouraged by rising disposable incomes and corporate perception that upscale vehicles reinforce brand positioning during client visits. Chinese brands experienced a 150% demand spike in June 2024, signaling consumers are open to alternative premium propositions when pricing and features align.

Mohamed Yousuf Naghi Motors’ deal to supply BMW and MINI models to Budget adds credibility to the high-end shift. At the same time, EV adoption gathers momentum as Gulf authorities subsidize charging infrastructure. The UAE targets 25% EV sales by 2035, and Saudi Arabia is installing 50,000 public chargers by 2025, paving the way for greener rental fleets.[3]Public Investment Fund Saudi Arabia, “Charging Infrastructure Deployment Plan,” pif.gov.sa Customers on longer leases increasingly select SUVs for versatility—ample cargo for family excursions and superior ride height for desert terrain—whereas urban weekend renters still lean towards sedans for parking ease.

By Service Type: Self-drive prevails, chauffeur services find niches

Self-drive arrangements dominated with a 63.89% slice of the GCC car rental market in 2024, growing at 7.88% CAGR as visitors relish the freedom to design bespoke itineraries. The ascent is enabled by upgraded highways, English-Arabic signage, and smartphone navigation tools that lower apprehension for foreign drivers. Chauffeur-driven packages, although smaller, cater to VIP travelers, corporate roadshows, and high-net-worth individuals who value local knowledge and time efficiency.

Dubai Taxi Company’s 2025-2029 roadmap hints at expansion into chauffeur-grade rentals that straddle the boundary between taxi meters and multi-hour hires. Hybrid offerings now permit the same booking to toggle between self-drive and professional driver add-ons, matching service to evolving daily schedules. As a result, the GCC car rental market presents operators with an opportunity to graduate customers up the value chain from economy self-drive to executive chauffeur services during repeat visits.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Individuals dominate, but corporates build momentum

Individuals comprised 48.76% of the GCC car rental market share in 2024, reflecting tourism’s weight in Gulf economies. Corporate and SME users, however, register the sharper 7.47% CAGR, spurred by policies that let companies expense rental costs in lieu of owning depreciating fleets. Enterprise Mobility’s USD 38 billion global revenue underscores the appetite for outsourced vehicle management. Within the GCC car rental industry, large construction and energy projects embed rental clauses into contracts, ensuring dedicated fleets for site staff without the capital hurdle of outright purchases.

Gig-economy growth adds a further twist, with freelance drivers renting vehicles only for peak demand windows, thereby distorting the clear-cut individual-versus-corporate dichotomy. Government entities occasionally request specialty fleets, such as electric sedans for diplomatic events, creating niche orders that influence the overall fleet mix. The evidence points to a maturing market in which operators must master both retail volume and fewer, high-value corporate accounts.

Geography Analysis

The United Arab Emirates set the pace with 39.94% of revenue in 2024, leveraging Dubai’s “Destination 2030” tourism blueprint and Abu Dhabi’s status as an MICE powerhouse. Visitor inflows rose 9% year-on-year in the first half of 2024 and underpin high fleet utilization at airport locations, even as insurance premiums climbed by 40% and challenged pricing models. Authorities ease cross-border friction by recognizing GCC licenses, a policy that steers some Saudi and Kuwaiti tourists toward self-drive options upon arrival. Meanwhile, EV incentives, including reduced Salik tolls and free parking for electric cars, coax operators to pilot battery-electric sedans in select fleets.

Saudi Arabia posts the fastest 7.71% CAGR, powered by Vision 2030, which combines vast infrastructure spending with a formal regulatory architecture for leasing brokers. Premium taste evolution is evident in Budget’s procurement of BMW and MINI units supplied by Mohamed Yousuf Naghi Motors, highlighting the country’s appetite for luxury. EV momentum gains traction with 50,000 chargers slated for installation by 2025, and ride-subscription apps like invygo use Riyadh as a test bed for flexible access models.

Qatar, Kuwait, Oman, and Bahrain round out the landscape, each with a tourism and diversification agenda. Qatar Tourism wrapped up 2024 on a high note, underscoring its rising stature in global tourism. The year-end count was a notable 5,076,640 visitors, marking a robust 25% uptick from the 4,046,281 visitors recorded in 2023. Cross-border weekend rentals between Oman and the United Arab Emirates or Bahrain and the Eastern Province of Saudi Arabia create micro-spikes in demand. However, fragmented rules on insurance endorsements occasionally deter spontaneous bookings. Still, the smaller markets’ compact geographies enable high fleet turnover and keep operating costs in check for companies that master regulatory nuances.

Competitive Landscape

Competition is moderate and fragmented. Multinationals such as Hertz, Enterprise, and SIXT tussle with regional stalwarts Al-Futtaim Automall, Yelo, and Thrifty, while digital insurgents ekar and Udrive chip away at legacy market share through app-centric micro-rentals. Execution risk runs high for incumbents that misjudge fleet electrification; Hertz’s chalk-and-cheese experience—selling off 20,000 EVs and replacing its CEO—illustrates the danger of over-aggressive pivots.

Enterprise Mobility’s expansion into Thailand confirms the ambitions of leading groups to transplant know-how into growth markets. Super-app integration places platform operators like Careem in a gatekeeper role, controlling customer access yet offloading fleet risk onto partners.

White-space opportunities remain: Arabic-language UX remains under-served; cross-border one-way rentals need harmonized insurance; and specialized gig-worker packages could unlock latent demand. The winners will be firms that weld fleet-management discipline to data-driven pricing inside ecosystems customers already trust.

GCC Car Rental Industry Leaders

-

Hertz Corporation

-

Yelo

-

Sixt SE

-

Avis Budget Group

-

Enterprise Holdings

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: Smart Mobility International announced a state-of-the-art New Energy Vehicle service center in Dubai’s Al Quoz district, including E-Charging Stations to support the UAE’s 50% NEV target by 2050.

- December 2024: Dubai Taxi Company unveiled its 2025-2029 strategy aimed at entering untapped UAE and regional markets with an expanded chauffeur offering.

- October 2024: Dubizzle launched a rental-car aggregation service on its marketplace platform following robust 9% visitor growth in Dubai during H1 2024.

GCC Car Rental Market Report Scope

The GCC Car Rental Market is segmented by Vehicle Type (Economy/Budget and Premium/Luxury), by Vehicle Body Style (Hatchback, Sedan, and Sport Utility Vehicle), and by Booking Channel (Online and Offline) and by Country (United Arab Emirates (UAE), Saudi Arabia, Qatar, and Rest of GCC Countries). The report offers market size and forecasts for GCC Car Rental in terms of value (USD Million) for all the above segments.

| By Booking Channel | Online |

| Offline | |

| By Rental Duration | Short-term |

| Long-term / Operating Lease | |

| By Vehicle Type | Hatchback |

| Sedan | |

| Sport Utility Vehicle | |

| Multi-Purpose Vehicle | |

| By Service Type | Self-drive |

| Chauffeur-drive | |

| By End-User | Individual |

| Corporate & SME | |

| Government & NGO | |

| By Country | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

By Booking Channel

| Online |

| Offline |

By Rental Duration

| Short-term |

| Long-term / Operating Lease |

By Vehicle Type

| Hatchback |

| Sedan |

| Sport Utility Vehicle |

| Multi-Purpose Vehicle |

By Service Type

| Self-drive |

| Chauffeur-drive |

By End-User

| Individual |

| Corporate & SME |

| Government & NGO |

By Country

| United Arab Emirates |

| Saudi Arabia |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the GCC car rental market?

The GCC car rental market is valued at USD 1.82 billion in 2025.

How fast is the market expected to grow?

Revenue is projected to rise at a 7.13% CAGR, reaching USD 2.56 billion by 2030.

Which GCC country holds the largest market share?

The United Arab Emirates leads with 39.94% share in 2024.

Which booking channel is growing the quickest?

Online platforms are expanding at a 7.42% CAGR, outpacing the still-dominant offline counters.

What rental duration segment shows the strongest future momentum?

Long-term and operating leases are projected to grow at 7.75% CAGR as companies shift to asset-light fleet strategies.

How are electric vehicles influencing GCC rental fleets?

Government incentives and charging-station roll-outs are encouraging operators to integrate EVs, opening new revenue opportunities while lowering total cost of ownership.

Page last updated on: July 3, 2025