Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

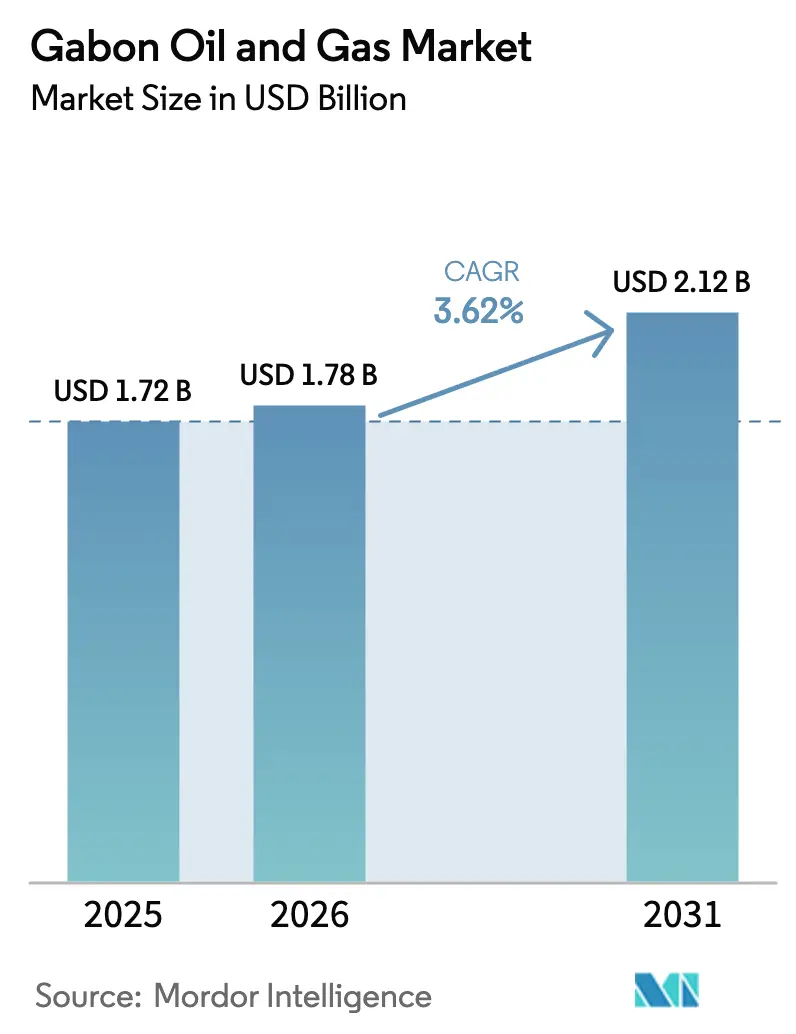

| Base Year Market Size (2025) | USD 1.72 Billion |

| Market Size (2026) | USD 1.78 Billion |

| Market Size (2031) | USD 2.12 Billion |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

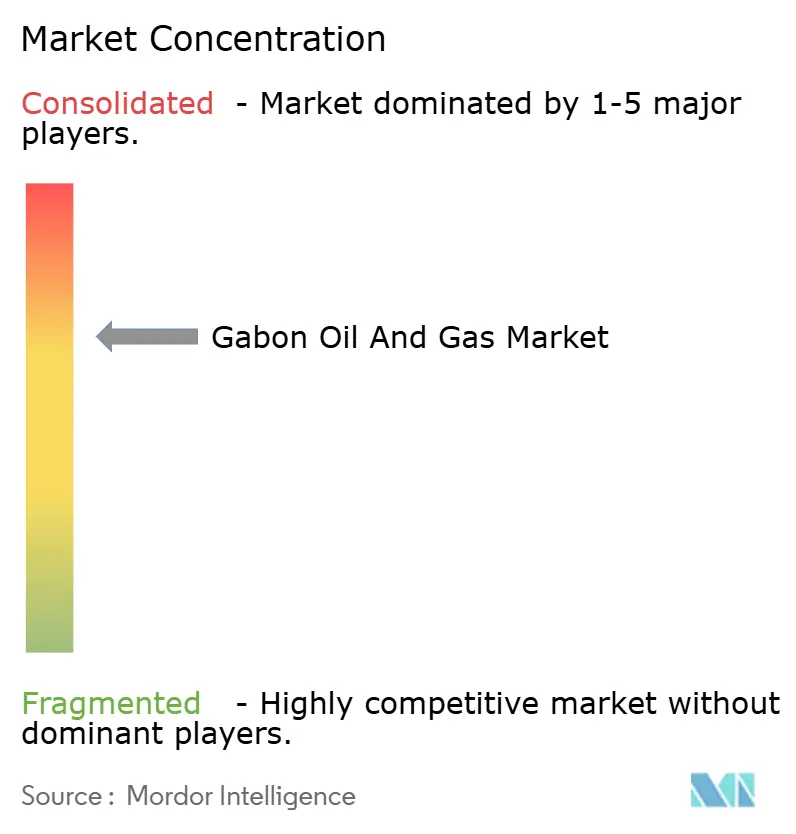

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gabon Oil And Gas Market Analysis by Mordor Intelligence

The Gabon Oil And Gas Market size was valued at USD 1.72 billion in 2025 and is estimated to grow from USD 1.78 billion in 2026 to reach USD 2.12 billion by 2031, at a CAGR of 3.62% during the forecast period (2026-2031).

Deep-water exploration successes, a streamlined dual-code fiscal regime, and steady Asian demand for low-sulfur crude underpin the outlook. At the same time, declining legacy onshore fields, skills gaps in subsea operations, and tighter safety oversight keep growth moderate. Upstream activity will remain the engine of the Gabon oil & gas market as international oil companies (IOCs) accelerate drilling around Dussafu and Hibiscus, while Perenco’s Cap Lopez floating LNG facility anchors midstream investment. Decommissioning spend is also rising, creating a parallel opportunity set for specialized contractors.

Key Report Takeaways

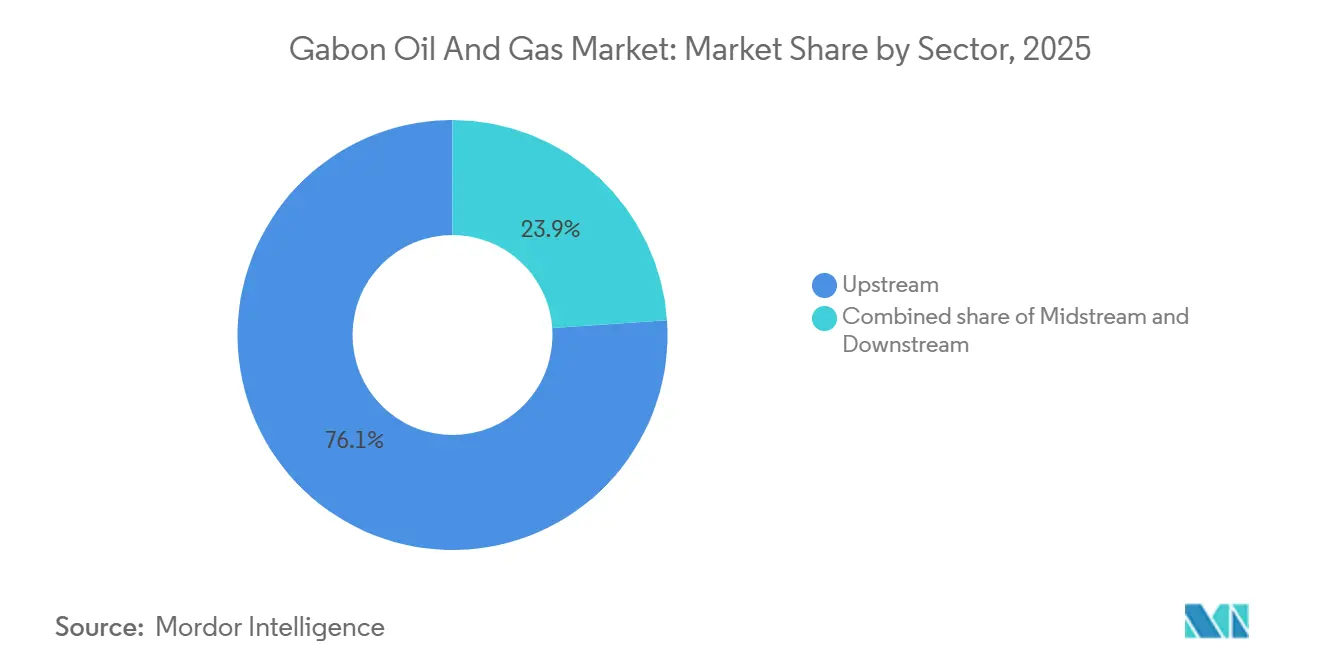

- By sector, the upstream segment held 76.1% of Gabon's oil & gas market share in 2025, and the same is forecast to post the fastest 3.8% CAGR through 2031.

- By location, onshore operations accounted for 70.5% of the Gabon oil & gas market in 2025, whereas offshore projects are expanding at a 6.5% CAGR through 2031.

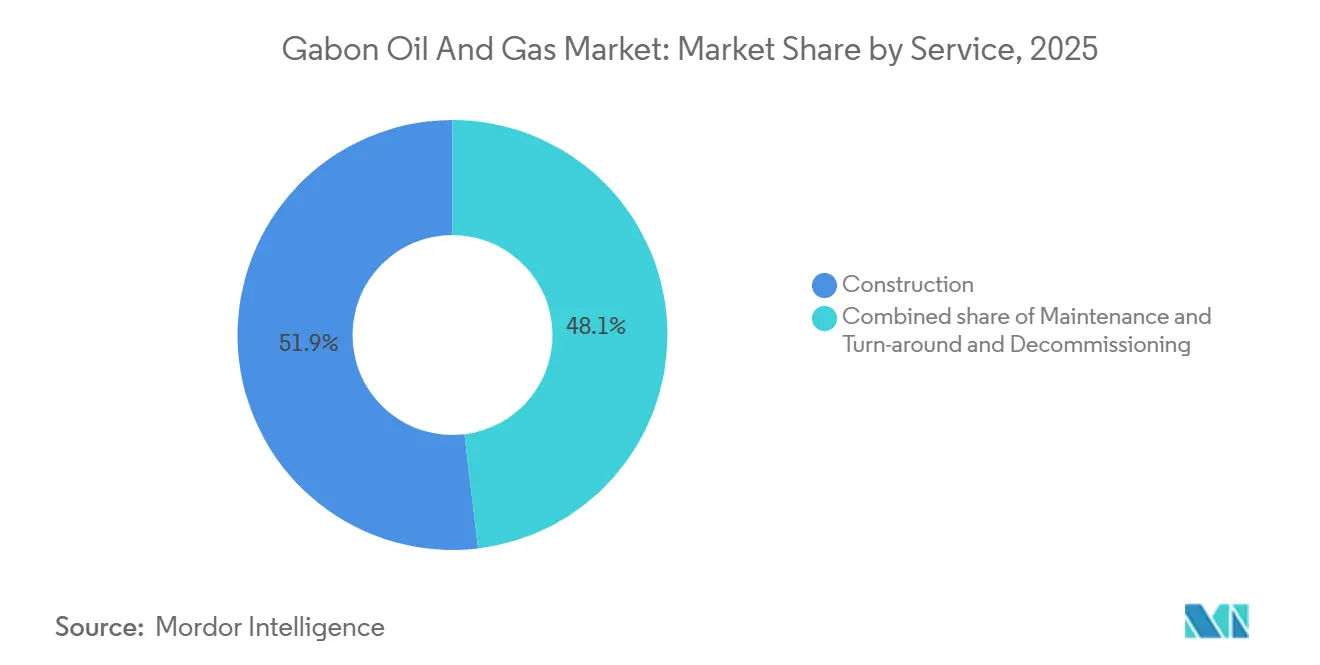

- By service, construction captured 51.9% revenue share in 2025, yet decommissioning is advancing at a 7.2% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Gabon Oil And Gas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Revised Hydrocarbons Code attracting IOCs | 0.8% | National, with offshore deepwater blocks | Medium term (2-4 years) |

| New deep-water discoveries (Dussafu, Hibiscus) | 1.2% | Offshore Gabon, primarily Dussafu basin | Long term (≥ 4 years) |

| Cap Lopez FLNG & gas monetisation build-out | 0.9% | National, export to regional LNG markets | Short term (≤ 2 years) |

| Global demand for low-sulphur crudes | 0.4% | Global, with primary demand from Asia-Pacific | Medium term (2-4 years) |

| Batanga LPG project cutting imports | 0.3% | National, Libreville and Port-Gentil markets | Short term (≤ 2 years) |

| AI-enabled EOR for mature fields | 0.5% | Onshore legacy fields, Gamba and Rabi-Kounga | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Revised Hydrocarbons Code Attracting IOCs

Gabon’s 2025 dual-code framework separates oil and gas terms, trims state participation to 10%, and grants import-duty exemptions for LNG equipment, making fiscal terms regionally competitive.[1]Africa Oil & Power, “Gabon Adopts Dual Hydrocarbons Code,” africaoilpower.com ExxonMobil and BP executed ultra-deepwater memoranda of understanding (MoUs) in 2025, ending a decade-long hiatus by supermajors. Perenco fast-tracked Cap Lopez FLNG once accelerated depreciation for gas projects became law. The code mandates 90-day approvals for production-sharing contracts, compressing bureaucratic timelines. Independents such as BW Energy and Panoro expanded Dussafu drilling on the back of the same incentives.

New Deep-Water Discoveries (Dussafu, Hibiscus)

BW Energy’s Bourdon find in March 2025 raised Dussafu recoverable reserves to over 150 million barrels and supports a third production hub. Reservoirs in Gamba sandstones show permeability above 500 mD, yielding 5,000-10,000 barrels per day (bpd) initial rates that justify USD 40-60 million well costs. PETRONAS confirmed frontier potential when Boudji-1 logged 90 m hydrocarbon sands in 2024. These successes offset a 60% onshore decline since the 1990s. Panoro’s 17.5% stake in Dussafu generated 4,760-6,502 bpd in 2025 and funded MaBoMo Phase 2 drilling.

Cap Lopez FLNG & Gas Monetization Build-Out

Perenco’s USD 2 billion Cap Lopez FLNG, slated for 2026 start-up, will liquefy 700,000 tpa LNG and 25,000 tpa LPG from associated gas currently flared. The modular barge converts environmental liabilities into export cash flow, targeting Asian buyers seeking smaller cargoes.[2]Offshore Technology, “Perenco Sanctions Cap Lopez FLNG,” offshore-technology.com Gabon holds 27 billion scm of proven gas yet lacks domestic pipelines, so floating LNG is the only bankable route. Replicable modules may unlock Tchibala and Torpille gas, broadening the monetization base. Compliance with ISO 14001 and IMO MARPOL Annex VI is baked into the export license.

Global Demand for Low-Sulfur Crudes

Rabi Light and Mandji contain <0.5% sulfur, meeting IMO 2020 rules and commanding USD 8-per-barrel premiums to sour grades in 2025. Exports averaged 204,000 bpd in 2024, with China taking 72,000 bpd and other Asian refiners 57,000 bpd. Low-sulfur demand helps sustain drilling even when Brent prices soften. However, fresh sweet supply from Guyana and Brazil is narrowing differentials, pressuring Gabonese netbacks. Producers must therefore pare costs or integrate carbon-intensity certification to stay competitive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Decline of legacy on-shore fields | -0.6% | Onshore Gamba, Rabi-Kounga, Tchatamba basins | Long term (≥ 4 years) |

| Post-coup political / fiscal uncertainty | -0.4% | National, affecting upstream investment decisions | Medium term (2-4 years) |

| Skilled-labour shortage for deep-water ops | -0.3% | Offshore deepwater blocks, subsea operations | Medium term (2-4 years) |

| Environmental & safety lapses (platform fires) | -0.2% | Offshore platforms, primarily Perenco operations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Decline of Legacy Onshore Fields

Onshore output fell from 370,000 bpd in 1997 to 224,000 bpd in 2024 and could slip to 100,000-200,000 bpd by 2030 without major EOR investment. Water cuts exceed 80%, and reservoir pressure is dropping, reducing waterflood efficiency. Polymer or CO₂ projects cost USD 15,000-25,000 per incremental barrel of reserves with 10-year paybacks, deterring capital. TotalEnergies quit its mature assets in 2021, transferring liabilities to Perenco. A 30% decline would cut fiscal receipts by USD 1.8 billion, squeezing infrastructure budgets.

Skilled-Labor Shortage for Deep-Water Ops

Subsea engineers, dynamic-positioning officers, and ROV pilots are scarce, forcing operators to import specialists at USD 800-1,200 per day.[3]OECD-AUC, “Skills Outlook for Resource-Rich Africa 2024,” oecd.org Gabonese vocational programs focus on onshore trades; few graduates have hands-on BOP or subsea tree exposure. Expat reliance triggers local-content penalties when national staffing falls under 70%. Industry/academic partnerships and CEMAC-wide certification could ease costs and improve mobility. TechnipFMC and Schlumberger have begun sponsoring simulation labs, but scale remains modest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Upstream Dominance Sustained by Deep-Water Momentum

The upstream portion of the Gabon oil & gas market size accounted for 76.1% revenue in 2025 and is advancing at a 3.8% CAGR through 2031. Annual spend is driven by USD 40-60 million wells and USD 500 million-plus floating production systems. Midstream outlays are smaller because new wells tie back to existing hubs, while downstream refining covers only 7% of domestic crude throughput.

Investment prioritizes projects with quick cash cycles, such as VAALCO’s USD 80 million infill program at Etame that pays back in under two years, contrasting with PETRONAS’s ultra-deepwater Boudji-1, where capital and risk rise sharply. Efficiency gains from integrated engineering contracts further cement upstream primacy. The Gabon oil & gas market will maintain this upstream tilt unless incentives emerge for local petrochemicals or gas-to-liquids complexes.

By Location: Offshore Acceleration Reshaping Production Geography

Onshore fields still dominate Gabon's oil & gas market share at 70.5% in 2025, yet offshore volumes are growing 6.5% per year and could overtake by 2028. Deep-water wells deliver 5,000-10,000 bpd rates at operating costs of USD 12-18 per barrel, outranking older onshore units that now average USD 20-28.

The trend accelerated after ExxonMobil's 2025 MoU to explore ultra-deepwater blocks analogous to Guyana's Stabroek play. Onshore players are piloting horizontal drilling and AI-enabled polymer floods, but each well adds just 200-500 bpd. Offshore growth, therefore, sets the pace for the Gabon oil & gas market, contingent on timely FPSO deployment and streamlined environmental reviews.

By Service: Decommissioning Surge Reflects Aging Infrastructure

Construction claimed 51.9% of service revenue in 2025, yet decommissioning is the fastest-growing slice at 7.2% CAGR, mirroring platform age profiles.[4]Delta Decom, “Asset Retirement in West Africa,” deltadecom.com More than 40 structures installed pre-2000 show corrosion and fatigue that demand removal under ISO 14001.

Tullow’s asset sale carried USD 31 million in decommissioning provisions, highlighting latent liabilities. Specialized contractors handle plug-and-abandonment, heavy-lift topside removal, and seabed remediation, all new revenue pools inside the Gabon oil & gas market. Operators must decide between life-extension capex or earlier retirement to redeploy capital offshore.

Geography Analysis

Offshore Dussafu, Cap Lopez, and Likuale blocks and onshore Gamba and Rabi-Kounga basins form the geographic spine of the Gabon oil & gas market. Onshore still represented 70.5% market weight in 2025, yet depletion has set total national production on course for 100,000-200,000 bpd by 2030 unless offshore replacement barrels arrive. Perenco leads onshore with marginal-field projects such as Wamba, but output gains are modest. BW Energy’s Bourdon find, and Panoro’s MaBoMo Phase 2 inject growth offshore, nudging the balance seaward.

Higher-quality reservoirs offshore achieve breakeven at USD 35-45 per barrel Brent, well under the USD 50-60 required for advanced EOR onshore. PETRONAS’s Likuale discovery and ExxonMobil’s ultra-deepwater initiative may unlock Guyana-scale Cretaceous plays, broadening the reserve base. Meanwhile, fiscal incentives in the 2025 code and the country’s compact geography - with many discoveries within 50 km of shore - lower tie-back costs and de-risk economics.

Cap Lopez FLNG monetizes associated gas, converting what was flared into export revenue while cutting carbon penalties. The onshore Batanga LPG plant reduces import dependence but cannot absorb all surplus gas, leaving reinjection prevalent. Future basin entries will likely cluster around existing hubs, reinforcing geographic path dependence inside the Gabon oil & gas market.

Competitive Landscape

Gabon's upstream remains moderately concentrated: Perenco, BW Energy, VAALCO, and Gabon Oil Company jointly hold roughly 70% of production, with no single entity above 30%. The state's USD 1.04 billion purchases of Assala and Tullow assets in 2025 lifted Gabon Oil Company to 50,700 bpd and 133 million barrels of 2P reserves. Independents exploit nimble models, BW Energy's fast-track FPSOs bring wells online within 18-24 months, beating deepwater norms.

Service majors TechnipFMC and Schlumberger deploy integrated EPC and digital reservoir solutions, securing sticky long-term contracts. White spaces include ultra-deepwater frontier acreage, modular FLNG for stranded gas, and AI-enhanced EOR onshore, each demanding USD 500 million-plus capex portfolios. ExxonMobil's 2025 re-entry suggests supermajor appetite is returning as fiscal risk abates.

Local-content rules mandating a 70% Gabonese workforce could skew competition if training pipelines lag. Digital analytics and decarbonization credentials are emerging as tender differentiators, potentially reshaping supplier hierarchies inside the Gabon oil & gas market.

Gabon Oil And Gas Industry Leaders

Perenco SA

BW Energy

TotalEnergies SE

VAALCO Energy Inc.

Maurel et Prom SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: VAALCO Energy, Inc. has kicked off its Phase Three Drilling Program offshore Gabon, marking the start with the spudding of the ET-15 infill well on the Etame platform.

- October 2025: Gabon inked Memorandums of Understanding (MoUs) with global oil giants BP and ExxonMobil (XOM). The move is part of Gabon's strategy to delve into deep and ultra-deep offshore blocks, with aspirations to tap into vast reserves, amplify production, and solidify its stature in Central Africa's oil arena, bolstered by favorable policies and regulatory changes.

- September 2025: ReconAfrica revealed its signing of a Production Sharing Contract (PSC) for the offshore Block C-7, now known as the Ngulu block, situated in shallow waters off the coast of Gabon. The PSC bestows ReconAfrica with a 55% working interest and the role of operator.

- July 2025: Gabon's Minister of Oil & Gas, Minister Nguema, has made his mark at the African Energy Week (AEW): Invest in African Energies conference. His presence underscores Gabon's commitment to collaborating with global partners, aiming to extract enhanced value from the nation's oil and gas sector, and paving the way for fresh avenues of collaboration and investment.

Gabon Oil And Gas Market Report Scope

Oil and gas refer to petroleum, natural gas, other related hydrocarbons or minerals, and all other substances produced or extracted in association.

The Gabon Oil & Gas Market is segmented by sector, location, service, and geography. By sector, the market is segmented into upstream, midstream, and downstream activities. By location, the market is categorized into onshore and offshore operations. By service, the market is segmented into construction, maintenance and turn-around, and decommissioning services. For each segment, market sizing and forecasts are provided on the basis of value (USD).

By Sector

| Upstream |

| Midstream |

| Downstream |

By Location

| Onshore |

| Offshore |

By Service

| Construction |

| Maintenance and Turn-around |

| Decommissioning |

| By Sector | Upstream |

| Midstream | |

| Downstream | |

| By Location | Onshore |

| Offshore | |

| By Service | Construction |

| Maintenance and Turn-around | |

| Decommissioning |

Key Questions Answered in the Report

What is the forecast value of the Gabon oil & gas market by 2031?

It is projected to reach USD 2.12 billion, growing at a 3.62% CAGR.

Which segment currently dominates spending in Gabon’s hydrocarbons sector?

Upstream operations hold 76.1% revenue share and continue to absorb most capital.

How will Cap Lopez FLNG influence Gabon’s gas strategy?

The 700,000 tpa facility monetizes previously flared gas, turning an environmental liability into LNG export revenue from 2026.

Why are offshore projects gaining momentum in Gabon?

Deep-water wells deliver higher initial rates at lower operating costs, leading offshore volumes to grow 6.5% annually.

What safety challenges have recently affected operations?

Incidents such as the 2024 Becuna platform fire prompted stricter audits and raised offshore insurance premiums by 20-30%.

Page last updated on: