Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 9.10 Billion |

| Market Size (2026) | USD 10.11 Billion |

| Market Size (2031) | USD 17.09 Billion |

| Growth Rate (2026 - 2031) | 11.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Cybersecurity Market Analysis by Mordor Intelligence

The France cybersecurity market size was valued at USD 9.10 billion in 2025 and estimated to grow from USD 10.11 billion in 2026 to reach USD 17.09 billion by 2031, at a CAGR of 11.08% during the forecast period (2026-2031). Rapid regulatory expansion under NIS2, heavier public-sector funding, and a sharp rise in cloud migration are synchronizing to widen the addressable opportunity for vendors. Enterprises continue to consolidate security stacks, channeling spending toward integrated platforms that ease compliance and talent pressures. Managed security services are surging as buyers offset a persistent shortage of skilled practitioners, while AI-driven analytics are becoming standard in French security operations centers. Heightened Olympic-period cyber activity has permanently recalibrated domestic threat awareness, prompting long-term investment in threat-monitoring infrastructure across critical sectors such as healthcare, energy, and transportation.

Key Report Takeaways

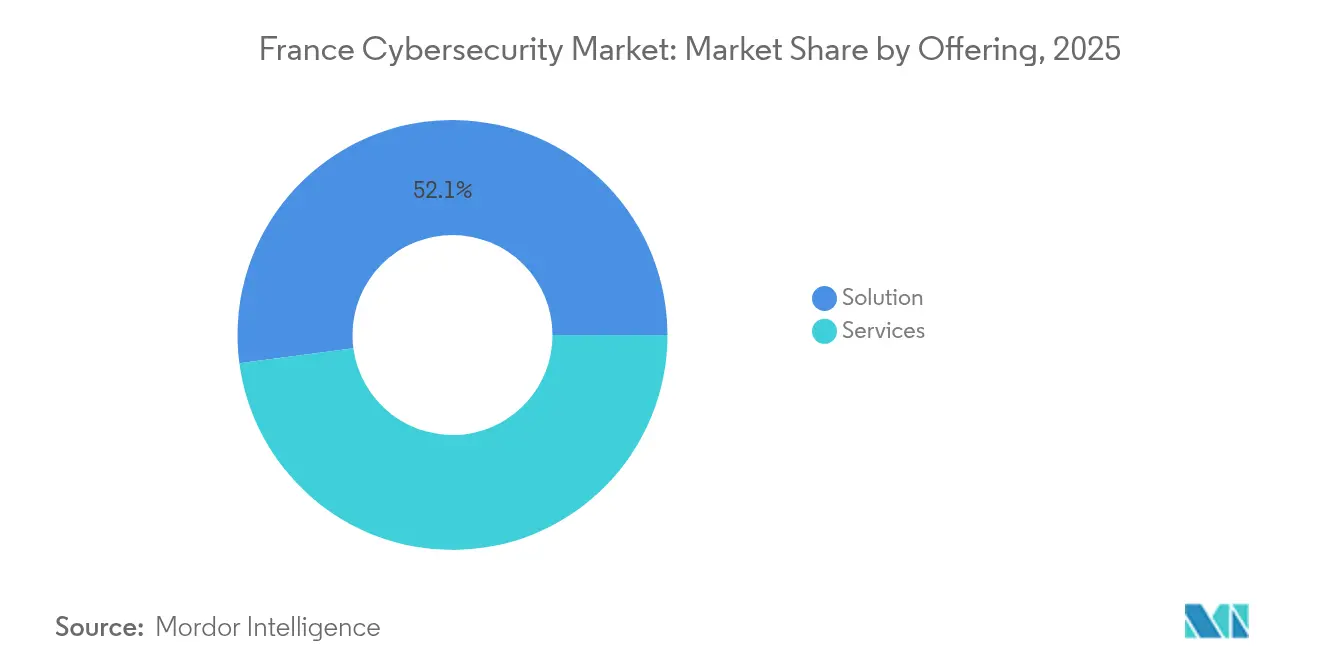

- By offering, solutions held 52.10% of the France cybersecurity market share in 2025, whereas services are projected to expand at a 12.85% CAGR through 2031.

- By deployment mode, cloud platforms captured 59.78% revenue share of the France cybersecurity market in 2025 and are tracking a 14.25% CAGR to 2031.

- By enterprise size, large organizations controlled 64.05% of the France cybersecurity market in 2025; SMEs represent the fastest trajectory at a 12.15% CAGR through 2031.

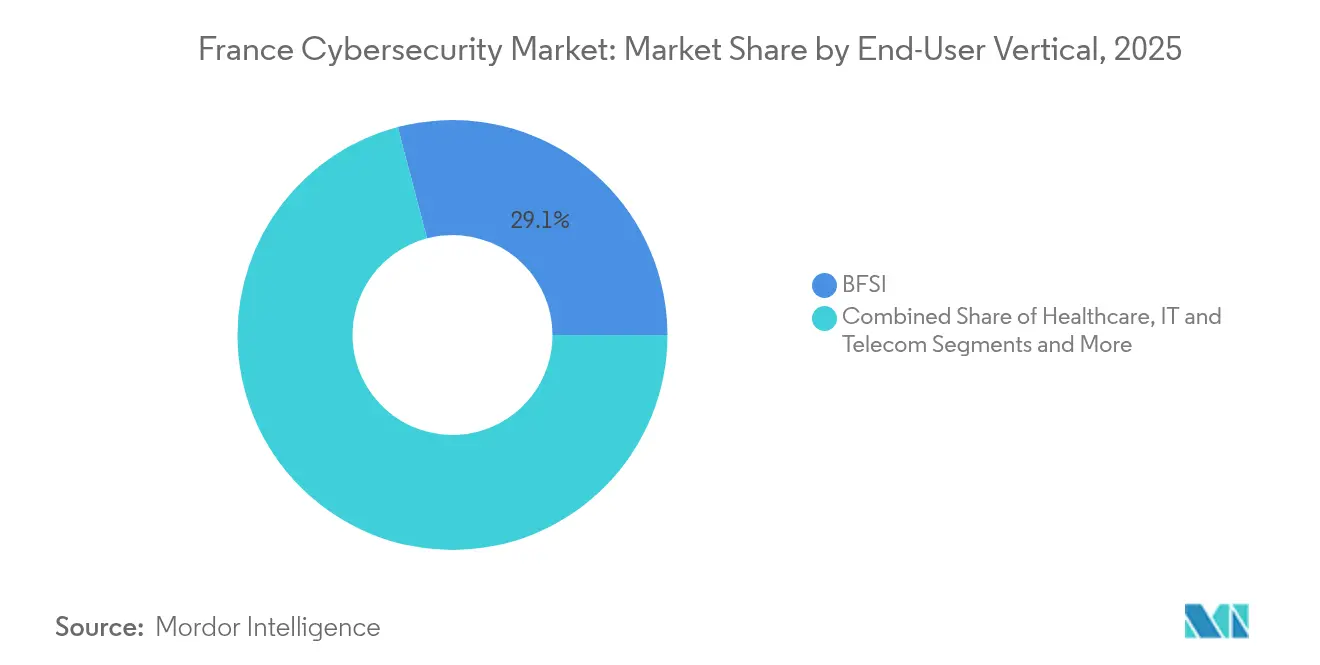

- By vertical, BFSI contributed 29.10% to the France cybersecurity market size in 2025, while healthcare is on course for a 12.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated NIS2 adoption & Increasing French Government Cyber Plan funding | +2.8% | National, with spillover to EU compliance frameworks | Medium term (2-4 years) |

| Ransomware surge on French critical infrastructure & healthcare | +2.1% | National, concentrated in metropolitan areas | Short term (≤ 2 years) |

| Paris 2024 Olympics-driven threat-monitoring investments | +1.4% | National, with Paris region epicenter | Short term (≤ 2 years) |

| SME cloud-migration boom under "France Num" digital vouchers | +1.7% | National, with regional variations | Medium term (2-4 years) |

| Campus Cyber ecosystem catalysing local solution innovation | +1.2% | National, centered in Paris Region | Long term (≥ 4 years) |

| Remote-work shift demanding Zero-Trust & IAM upgrades | +1.6% | National, with urban concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated NIS2 adoption and French Government cyber funding

NIS2 widens the compliance net from 500 to roughly 15,000 French entities, tripling the number of regulated sectors and intensifying demand for governance, risk, and compliance tooling. France 2030 earmarked EUR 39 million (USD 42 million) for 17 cybersecurity projects, anchoring sovereign capability development[1]info.gouv.fr, “France 2030: 17 nouveaux projets pour la cybersécurité,” info.gouv.fr. ANSSI’s phased roll-out stresses enablement over sanction, spurring advisory services as firms race to close gaps. Government interest in acquiring Atos’ cybersecurity assets for EUR 700 million (USD 748 million) further underlines the strategic value of domestic IP. Together these moves inject capital, enlarge the client base, and reinforce the France cybersecurity market as a continental compliance hub.

Ransomware surge on French critical infrastructure and healthcare

ANSSI logged 4,386 security incidents in 2024, up 15% year on year, with healthcare representing 10% of ransomware filings. Hospitals at Armentières and Corbeil-Essonnes endured emergency shutdowns, driving urgency around endpoint detection and incident-response retainer services. Cultural landmarks such as the Louvre and Grand Palais also faced disruptions, proving no sector is immune. Spending is pivoting toward XDR platforms and crisis-management consulting, reinforcing the France cybersecurity market as a responsive services arena.

Paris 2024 Olympics-driven threat-monitoring investments

ANSSI coordinated a two-year security program that neutralized more than 140 attempted attacks during the Games, validating large-scale, multi-stakeholder defense models. Eviden deployed real-time analytics across 500 venues, embedding automated playbooks now repurposed for critical infrastructure. Cisco and Palo Alto Networks formed intelligence alliances that persist beyond the event, extending the France cybersecurity industry’s ecosystem appeal.

SME cloud-migration boom under “France Num” digital vouchers

France Num subsidizes up to EUR 1,500 (USD 1,605) per SME for security expenses, with regional grants reaching EUR 50,000 (USD 53,500). As 53% of SMEs now host workloads in the cloud, demand spikes for SaaS-based identity management and managed detection services suited to lean IT teams. This subsidy-driven adoption enlarges the cloud portion of the France cybersecurity market and feeds a robust MSP channel.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute cyber-talent shortage inflating SOC service costs | -1.8% | National, with Paris region concentration | Medium term (2-4 years) |

| Budget aversion among French SMEs viewing cyber as OPEX | -1.4% | National, with rural/regional emphasis | Short term (≤ 2 years) |

| Regulatory overlap (GDPR, NIS2, ANSSI sector rules) delaying buys | -1.2% | National, with cross-border compliance implications | Medium term (2-4 years) |

| Tool-sprawl and integration complexity across fragmented stack | -1.0% | National, concentrated in large enterprises | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Acute cyber-talent shortage inflating SOC costs

Roughly 15,000 cybersecurity vacancies persist nationwide, despite an 89% workforce expansion since 2020. Salary inflation reaches EUR 90,000 (USD 96,300) for senior analysts, squeezing provider margins and stimulating automation. Thales responded with GenAI4SOC to improve case triage efficiency by 40%. Such initiatives temper, but do not erase, the talent gap that restrains the France cybersecurity market’s ability to scale fully.

Budget aversion among SMEs viewing cyber as OPEX

Forty percent of SMEs cite cost as the main hurdle to stronger defenses while 18% run no formal controls at all. Limited awareness of state subsidies compounds the hesitancy, leaving small firms prone to fines under GDPR and imminent NIS2 rules. Vendors targeting this segment must emphasize outcome-based pricing and turnkey managed offerings to unlock untapped layers of the France cybersecurity market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Balanced platform demand amid services acceleration

Solutions generated 52.10% of 2025 revenue, with unified threat-management suites and XDR gaining traction as enterprises rationalize tool sprawl. The managed-services slice is growing at 12.85% CAGR as clients contract out 24/7 monitoring to compensate for staffing gaps. Identity-and-access tools, especially privileged-access management, underpin Zero-Trust rollouts. Wallix, for example, leverages its ANSSI qualification to court regulated clients. Professional services complement software spend, delivering assessment and remediation projects tied to NIS2 milestones. Hardware appliances remain foundational but are increasingly bundled with AI-driven analytics, illustrating the convergence that defines the France cybersecurity market.

The integration trend is fostering hybrid consumption models in which buyers license core platforms and overlay retained services for incident response. This approach expands lifetime value for vendors while providing flexibility in tight budget cycles. As ransomware campaigns intensify, incident-response retainers are now a baseline requirement across BFSI and healthcare, pushing the France cybersecurity market size for services steadily upward.

By Deployment Mode: Cloud predominance strengthens

Cloud deployments accounted for 59.78% of 2025 spending, reflecting widespread SaaS preference and rapid SME onboarding. The France cybersecurity market size attached to cloud solutions is forecast to rise at a 14.25% CAGR, outpacing the on-premise base as more critical workloads move to hybrid environments. SecNumCloud certification accelerates trust in domestic hosting, benefiting players such as OVHcloud and Outscale.

On-premise models persist in defense and heavily regulated utilities where data residency and latency demands outweigh elasticity. Yet even these sectors adopt cloud-based analytics to augment legacy controls. Multi-cloud orchestration platforms that normalize policy across providers are gaining lift, mitigating vendor lock-in risks for enterprises expanding beyond a single hyperscaler. As a result, the France cybersecurity market continues to blur traditional deployment lines, pivoting toward control-plane-centric architectures.

By End-User Vertical: BFSI lead with healthcare surge

BFSI led 2025 revenue with a 29.10% contribution to the France cybersecurity market size, compelled by stringent supervisory directives and high attacker return ratios. Healthcare, however, is advancing fastest at a 12.74% CAGR after a wave of hospital breaches spotlighted vulnerabilities in outdated medical networks. Industrial and defense operators are layering IT and OT defenses to protect mission-critical systems, aided by ANSSI-certified vendors such as Stormshield.

Retail and e-commerce entities focus on payment security and fraud analytics, while energy firms shore up SCADA environments against supply-chain exploits. Cross-sector convergence creates demand for platforms able to ingest telemetry from both corporate and industrial domains. Vendors that demonstrate competence across IT-OT boundaries capture increasing mindshare within the France cybersecurity market.

By Enterprise Size: Large-enterprise dominance with SME momentum

Large organizations held 64.05% of 2025 spend, leveraging broad budgets to build in-house security operations and bespoke compliance workflows. SMEs, buoyed by subsidy schemes, are forecast to grow at 12.15% CAGR, injecting fresh volume into the France cybersecurity market. Managed security providers tailor subscription packages that align to cash-flow realities of small firms.

Cloud-native secure web gateways, micro-segmentation tools, and turnkey MDR services resonate with mid-market buyers needing immediate coverage without capital outlay. Vendors that couple automation with advisory touchpoints lower entry friction, expanding addressable demand and nurturing the long-tail of the France cybersecurity market.

Geography Analysis

The Paris Region anchors 60% of domestic cybersecurity startups and produced EUR 14.6 billion (USD 15.6 billion) in segment revenue during 2021, reinforcing the city as the gravitational center of the France cybersecurity market. Campus Cyber facilitates cluster effects by co-locating enterprises, regulators, and academia. The region also hosts ANSSI headquarters, ensuring policy proximity and rapid certification cycles.

Beyond Paris, metropolitan areas such as Lyon, Lille, and Toulouse have expanded incident-response hubs to conform with NIS2 requirements, spreading demand geographically. Nouvelle-Aquitaine offers grants up to EUR 50,000 (USD 53,500) for digital security projects, catalyzing local partner ecosystems that feed into the national channel. Cross-border initiatives under the EU Cybersecurity Act encourage French vendors to scale within the single market, enlarging export potential for the France cybersecurity industry.

Regional threat profiles vary. Coastal energy infrastructure in Brittany faces state-linked reconnaissance, whereas Alsace manufacturers report heightened industrial-espionage attempts. Such diversity reinforces a multi-layered defense imperative and positions the France cybersecurity market as a patchwork of localized needs under a unifying regulatory umbrella.

Competitive Landscape

France hosts a moderately concentrated supplier base. Thales, Orange Cyberdefense, and Atos together hold 28% of 2024 revenue, while a vibrant startup tier fills niche requirement. Domestic champions emphasize sovereign cloud, ANSSI accreditation, and AI differentiators to counter global hyperscalers. Thales’ GenAI4SOC illustrates generative-AI infusion into incident workflows, promising 40% analyst time savings[3]Thales Group, “GenAI4SOC launch,” thalesgroup.com. Eviden capitalized on its Olympics contract to showcase large-event security orchestration.

Specialists target vertical pain points: Stormshield safeguards industrial control systems; HarfangLab advances endpoint detection with EUR 25 million (USD 27 million) in new funding. International entrants such as Palo Alto Networks and Cisco deepen local footprints through threat-intelligence alliances and Paris RandD labs. MandA activity is intensifying, evidenced by Integrity360 acquiring Holiseum to secure industrial expertise. These moves hint at an impending consolidation wave that could raise entry barriers across the France cybersecurity market.

Channel ecosystems evolve in tandem. Telecommunication operators bundle managed security with connectivity, expanding reach into SMB segments. Systems integrators curate compliance-as-a-service packages aimed at NIS2 newcomers. Startups leverage Campus Cyber to co-develop solutions with anchor corporates, accelerating commercialization cycles. The competitive chessboard remains dynamic yet tilts toward players boasting sovereign hosting, scalable AI, and clear regulatory alignment.

France Cybersecurity Industry Leaders

IBM Corporation

Cisco Systems Inc

Dell Technologies Inc.

Fortinet Inc.

Intel Security (Intel Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Integrity360 purchased Holiseum to broaden industrial cybersecurity capacity and establish a Paris security operations center.

- January 2025: Eviden became the official cybersecurity services supporter for the Paris 2024 Olympic and Paralympic Games, delivering automated monitoring across 500 venues.

- November 2024: Thales introduced GenAI4SOC, embedding generative AI into SOC workflows for French enterprises.

- August 2024: HarfangLab secured EUR 25 million (USD 27 million) to scale its endpoint platform across Europe.

France Cybersecurity Market Report Scope

IT advancement, communication technologies, and smart energy grids are changing the landscapes of almost every country’s critical infrastructure and business networks. However, with rapidly changing technology comes rapidly advancing threats. Cybersecurity solutions help an organization to monitor, detect, report, and counter cyber threats, which are internet-based attempts to damage or disrupt information systems and hack critical information using spyware and malware and by phishing in order to maintain data confidentiality.

The France cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security Equipment | |

| Endpoint Security | |

| Other Services | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premise |

| Cloud |

By End-User Vertical

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Others |

By End-User Enterprise Size

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security Equipment | ||

| Endpoint Security | ||

| Other Services | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By End-User Vertical | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

Key Questions Answered in the Report

What is the current value of the France cybersecurity market?

The France cybersecurity market size stands at USD 10.11 billion in 2026.

How fast is the France cybersecurity market expected to grow?

Revenue is projected to rise at an 11.08% CAGR, reaching USD 17.09 billion by 2031.

Which deployment model leads spending in France?

Cloud-based security dominates with a 59.78% share of 2025 revenue and a 14.25% CAGR outlook.

Why is healthcare the fastest-growing vertical?

Repeated ransomware attacks on French hospitals have accelerated investments, sending healthcare on a 12.74% CAGR trajectory.

How is the talent shortage influencing market dynamics?

Around 15,000 open cybersecurity roles inflate service costs and spur automation, prompting providers to launch AI tools such as Thales GenAI4SOC.

Page last updated on: