External Pacemakers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

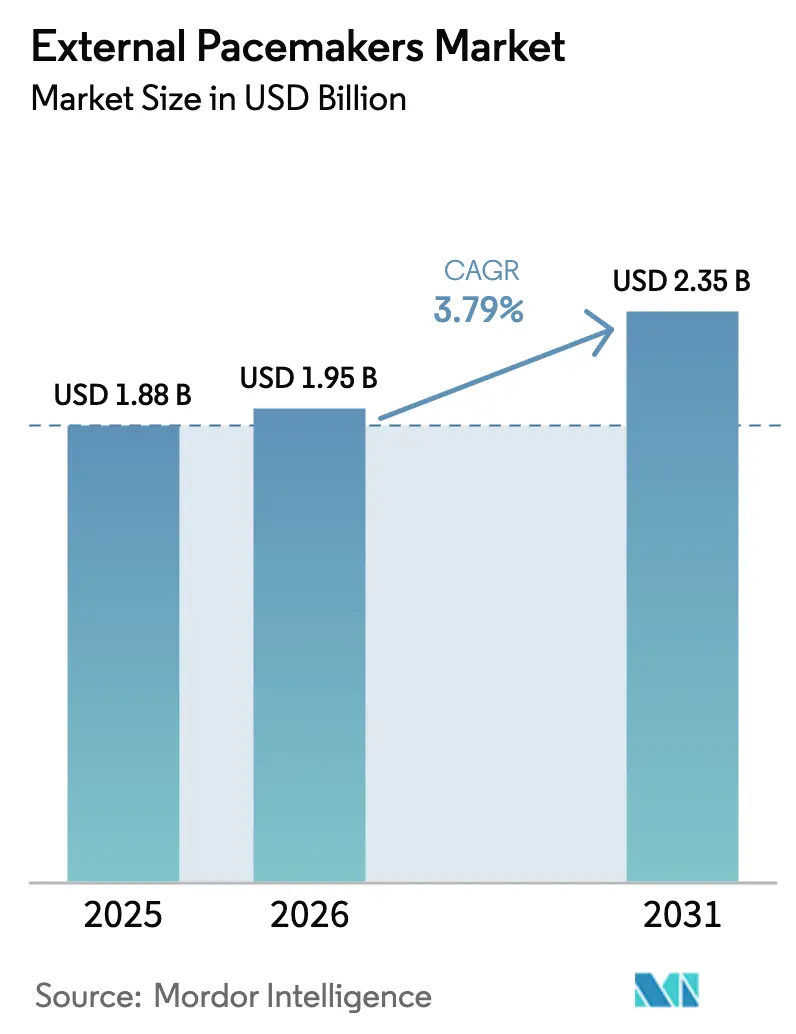

| Market Size (2026) | USD 1.95 Billion |

| Market Size (2031) | USD 2.35 Billion |

| Growth Rate (2026 - 2031) | 3.79% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

External Pacemakers Market Analysis by Mordor Intelligence

The external cardiac pacemaker market size is expected to grow from USD 1.88 billion in 2025 to USD 1.95 billion in 2026 and is forecast to reach USD 2.35 billion by 2031 at 3.79% CAGR over 2026-2031. Consistent procedure growth, breakthrough leadless technologies that shorten hospital stays, and broader adoption in emergency medical services keep the demand curve stable while moderating price volatility. Technological differentiation in dual-chamber systems and AI-driven remote re-programming allows leading vendors to protect margins even as smaller firms push lower-priced alternatives[1]Source: Richard Stevenson, “Forward-Deployable Cardiac Pacing in Military Settings,” tccc.org.ua. Military field-medicine protocols, along with aging populations that face rising rates of atrioventricular block, further widen the external cardiac pacemaker market’s clinical footprint[2]Source: U.S. Food and Drug Administration, “Accolade Pacemaker Devices: FDA Safety Communication,” fda.gov . Reimbursement complexity and uneven infrastructure outside Tier-1 hospitals remain headwinds, yet continuing investments in cath-lab capacity across Asia-Pacific underpin the market’s long-term trajectory.

Report Key Takeaways

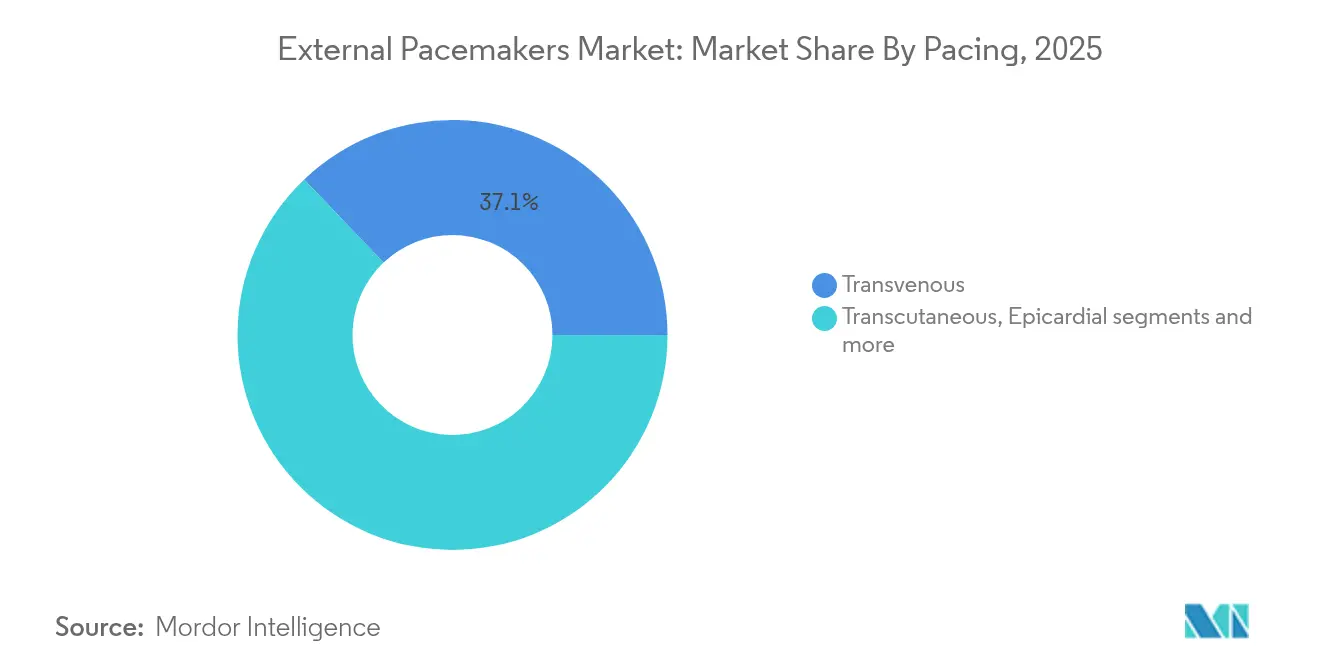

- By pacing type, transvenous systems led with 37.12% of the external cardiac pacemaker market share in 2025.

- By modality, single-chamber devices accounted for 43.65% of revenue in 2025, while dual-chamber units are poised for a 5.08% CAGR through 2031.

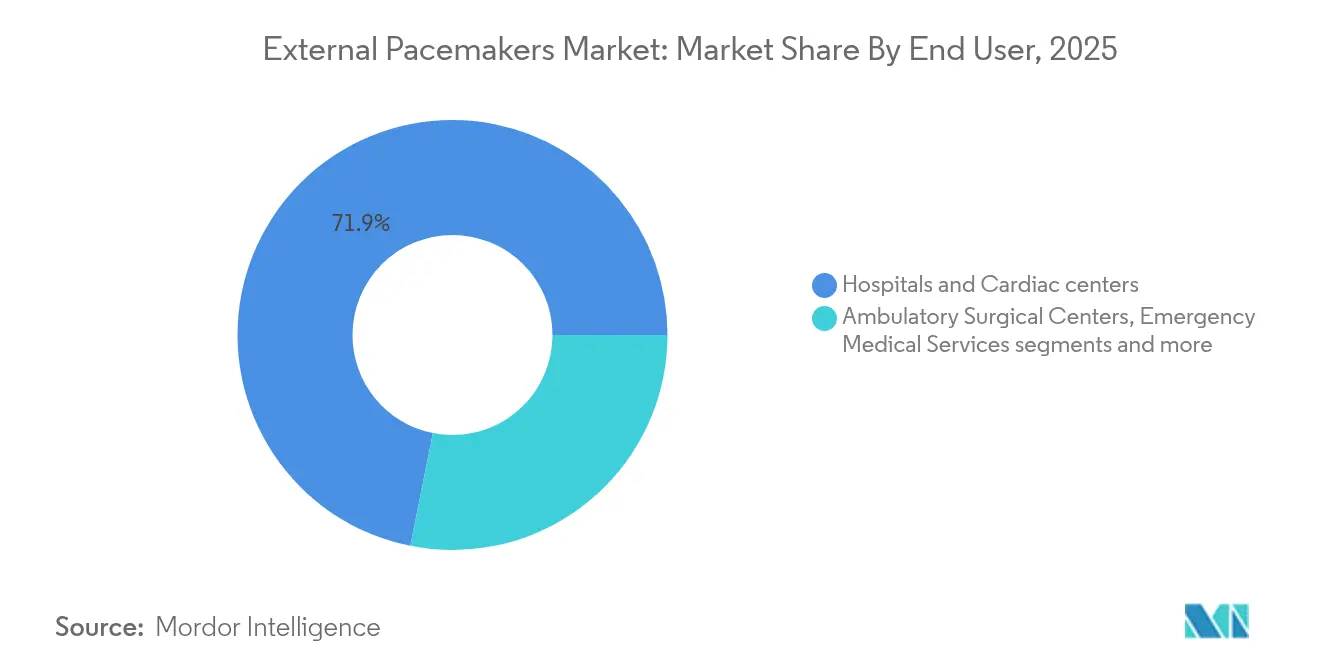

- By end user, hospitals and cardiac centers captured 71.86% of the external cardiac pacemaker market size in 2025; emergency medical services are growing fastest at 5.92% CAGR to 2031.

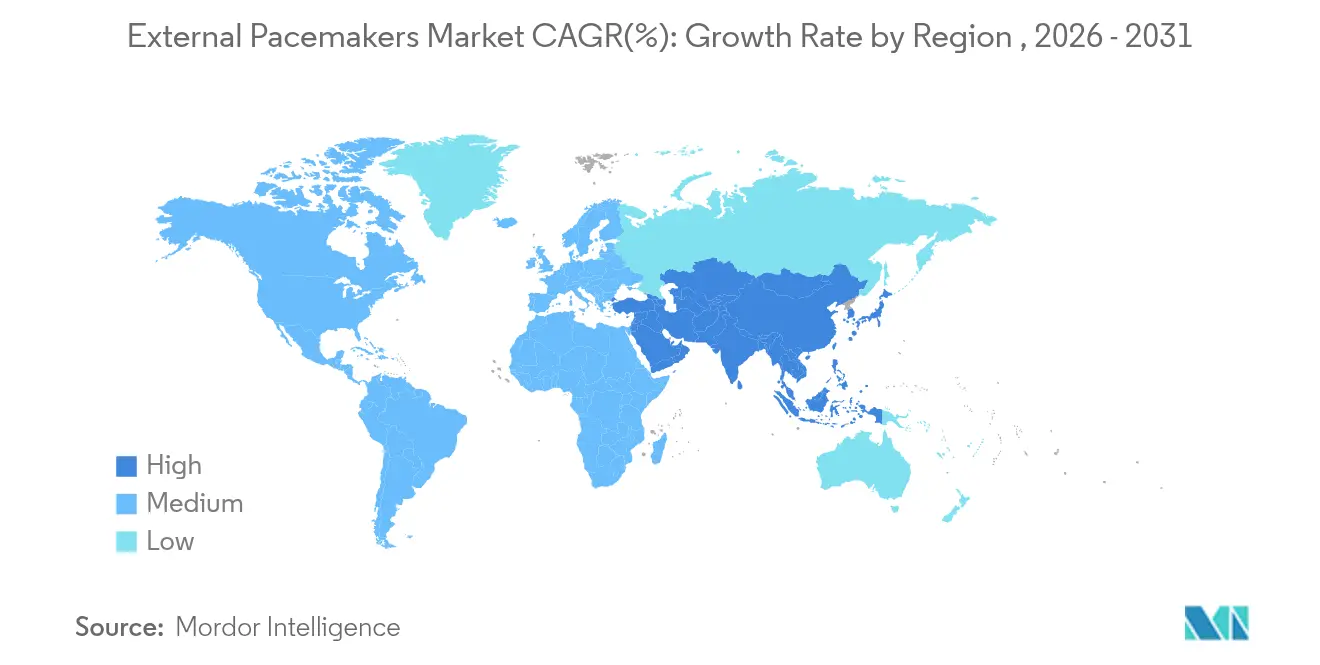

- By geography, North America commanded 38.12% of the external cardiac pacemaker market share in 2025, whereas Asia-Pacific is projected to expand at a 4.59% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global External Pacemakers Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of transient bradyarrhythmias & CVD | +1.2% | North America & Europe core, global spread | Medium term (2-4 years) |

| Growing volume of cardiac & structural-heart surgeries | +0.9% | Global, led by North America, Asia-Pacific accelerating | Short term (≤ 2 years) |

| Technological upgrades in dual-chamber & connected external pacemakers | +0.8% | North America & EU first adopters, Asia-Pacific emerging | Long term (≥ 4 years) |

| Expansion of emergency-medical & ambulance fleets | +0.5% | Rapid growth in emerging markets | Medium term (2-4 years) |

| AI-enabled remote monitoring platforms | +0.3% | North America & EU core | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Transient Bradyarrhythmias & CVD

High-grade AV block cases are expected to increase from 378,816 in 2020 to 535,076 by 2060, heavily concentrated in older adults, sustaining baseline demand for bridge pacing. Post-operative conduction disturbances follow a similar upward trend: 8.2% of cardiac surgery patients eventually need permanent implants, underscoring the external cardiac pacemaker market’s role during peri-operative stabilization.

Growing Volume of Cardiac & Structural-Heart Surgeries Requiring Temporary Pacing

Seventy-six percent of TAVR patients supported with a temporary generator avoid permanent devices one month later, cutting the permanent implant rate to 2.4% and saving USD 23,588 per case. This economic benefit strengthens the external cardiac pacemaker market’s value proposition, particularly in cost-sensitive health systems.

Technological Upgrades in Dual-Chamber & Connected External Pacemakers

Abbott’s AVEIR DR leadless platform delivers 98.3% implant success and >97% AV synchrony, showing that miniaturization no longer sacrifices physiologic pacing. Northwestern University’s rice-grain–sized dissolvable pacemaker offers a breakthrough for pediatric and post-surgical care by eliminating retrieval surgery. AI telemetry that lowers false alerts from 75% to 18% enables earlier discharge while preserving safety margins.

Expansion of Emergency-Medical & Ambulance Fleets Equipped with Pacing Capability

Modern ambulance protocols now require transcutaneous pacing capacity for hemodynamically significant bradycardia, widening first-hour survival windows and enlarging the external cardiac pacemaker market outside hospital walls. British Army advanced practitioners can place transvenous leads in austere environments, spotlighting defense procurement potential

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device cost & patchy reimbursement | -0.70% | Emerging markets & rural areas | Medium term (2-4 years) |

| Infection & lead-related complication risk | -0.40% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pacing Type: Transvenous Systems Drive Market Leadership

Transvenous platforms secured 37.12% of the external cardiac pacemaker market share in 2025 thanks to >95% capture reliability and well-established clinical familiarity. Corresponding revenue equaled roughly USD 697.9 million of the 2025 external cardiac pacemaker market size. Transcutaneous devices dominate early emergency usage but discomfort restricts dwell time to hours. Epicardial wires remain a surgical niche yet offer definitive capture post-sternotomy. Newly branded “temporary-permanent” leads show 2.5% infection and 1.7% dislodgement rates, improving confidence for multiday support.

Demand is shifting toward systems with integrated hemodynamic sensors that report real-time capture thresholds, helping intensivists fine-tune output without fluoroscopy. Major suppliers leverage these incremental upgrades to safeguard share against cost-focused entrants, underscoring the external cardiac pacemaker market’s reliance on feature innovation.

By Modality: Single-Chamber Dominance Faces Dual-Chamber Innovation

Single-chamber devices represented 43.65% of 2025 revenue, translating to about USD 820.6 million of the external cardiac pacemaker market size. Rapid deployment and adequate ventricular support keep the modality attractive during acute bradyarrhythmias. Dual-chamber solutions, however, are on a 5.08% CAGR path as data show AV synchrony lifts cardiac output by up to 20% sciencedirect.com. Abbott’s wireless AVEIR system sustains >90% synchrony during varied activities.

Ultra-high-frequency ECG mapping tools allow bedside optimization in under two minutes, encouraging broader uptake, especially where patients may need support for weeks. As pricing narrows, dual-chamber offerings are expected to erode the single-chamber lead, reshaping competitive hierarchies within the external cardiac pacemaker market.

By End User: Hospital Concentration Amid EMS Expansion

Hospitals and cardiac centers held 71.86% of 2025 revenues, equivalent to USD 1.35 billion of the external cardiac pacemaker market size, reflecting availability of fluoroscopy, telemetry and 24-hour staffing needed for safe temporary pacing. Emergency medical services show the fastest trajectory at 5.92% CAGR, riding investments in mobile critical-care units that integrate compact generators weighing under 300 g. Ambulatory surgical centers and specialty outpatient clinics contribute incremental gains as same-day electrophysiology interventions rise, supported by cloud-based rhythm dashboards that push monitoring out of the ICU.

Geography Analysis

North America captured 38.12% of 2025 revenue, driven by favorable reimbursement policies, large cardiac surgery volumes and rapid adoption of leadless platforms. AI-driven predictive analytics help U.S. centers shorten ICU dwell times, reinforcing the external cardiac pacemaker market’s health-economic case. Canada advances through provincial funding adjustments that now bundle external pacing into DRG payments, while Mexico’s IMSS system funds mobile coronary units equipped with transcutaneous kits.

Europe accounts for the second-largest share. France and Germany pursue sustainability by piloting device re-processing schemes that lower environmental impact without compromising sterility. The United Kingdom’s NHS trials cloud dashboards for step-down unit transfer within 24 hours of lead insertion, aiming to free ICU beds. Italian and Spanish hospitals recorded a 48.2% fall in permanent implants during COVID-19 lockdowns, yet emergency pacing volumes stayed comparatively resilient..

Asia-Pacific boasts the fastest growth at 4.59% CAGR. Japan pioneered reimbursements for leadless temporary generators, and China’s cath-lab count keeps multiplying in tier-2 cities. India’s national ambulance upgrade program equips every vehicle with external pacing pads, broadening rural access. South Korea, Australia and Singapore contribute with ageing demographics and medical-tourism flows that rely on quick-turnaround cardiac procedures to fuel the external cardiac pacemaker market.

Latin America and the Middle East & Africa remain nascent yet promising. Brazil’s SUS is piloting unit-price caps to stimulate local assembly, while Saudi Arabia funds advanced cardiac centers under Vision 2030. These programs could accelerate adoption once staff training and supply-chain barriers ease.

Competitive Landscape

The external cardiac pacemaker market is moderately Consolidated. Medtronic, Abbott and Boston Scientific collectively control about majority of global turnover and rely on proprietary algorithms, longer battery lifetimes and broad service networks. Medtronic’s Micra AV2 and VR2 promise 40% longer battery life—up to 17 years—which, while designed for permanent placement, resets clinician expectations for temporary replacements. Abbott pursues conduction-system pacing that may migrate into retrievable formats, while Boston Scientific fuses leadless pacemakers with subcutaneous ICD links to simplify escalation paths.

Tier-2 firms—BIOTRONIK, Osypka, MicroPort—compete on cost-effectiveness and regional customization, particularly across Europe and China. Teleflex’s planned EUR 760 million acquisition of BIOTRONIK’s vascular unit underscores portfolio bundling aimed at cath-lab procurement teams. University-backed start-ups target biodegradable materials and wireless energy harvesting to leapfrog legacy designs, reflecting how innovation pipelines keep the external cardiac pacemaker market dynamic.

Regulatory landscapes evolve in tandem. The FDA’s harmonization with ISO 13485, effective 2026, compels manufacturers to tighten cyber-security controls and traceability. Early movers may gain a negotiating edge with hospital groups that prioritize audit-ready supply chains.

External Pacemakers Industry Leaders

Medtronic

BIOTRONIK

MicroPort Scientific Corporation

Boston Scientific Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Teleflex agreed to acquire BIOTRONIK’s Vascular Intervention business for EUR 760 million.

- June 2024: Abbott earned CE Mark for AVEIR DR, the first dual-chamber leadless pacemaker.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the external pacemakers market consists of non-implantable, battery-powered devices that deliver short-term electrical stimulation through transcutaneous or transvenous leads to stabilize heart rhythm in emergency, peri-operative, or intensive-care settings. These units are counted at factory gate value, inclusive of single- and dual-chamber models supplied to hospitals, ambulatory surgical centers, emergency medical services, and military field hospitals worldwide.

Scope Exclusion: Permanent implantable, leadless, or biventricular pacemakers lie outside this study's boundary.

Segmentation Overview

- By Pacing Type

- Transcutaneous

- Transvenous (Temporary)

- Epicardial

- Esophageal

- By Modality

- Single-Chamber

- Dual-Chamber

- By End User

- Hospitals & Cardiac Centers

- Ambulatory Surgical Centers

- Emergency Medical Services

- Military Field Hospitals

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Cardiac electrophysiologists, perfusionists, biomedical engineers, and procurement heads across North America, Europe, Asia-Pacific, and Latin America were interviewed. Their insights on typical usage days, replacement cycles, and post-operative adoption helped validate secondary patterns and refine price corridors before the model was finalized by Mordor analysts.

Desk Research

Our analysts began with authoritative cardiovascular data sets such as the World Health Organization mortality database, American Heart Association procedure statistics, and Eurostat hospital discharge files, which anchor prevalence and treatment volumes. Regulatory clearance archives from the US FDA 510(k) portal, the European CE marking database, and Japan's PMDA informed product counts and launch timing. Trade-flow intelligence from Volza clarified cross-border shipments, while D&B Hoovers and Dow Jones Factiva supported company revenue splits. Peer-reviewed articles in journals like Circulation and patents queried through Questel mapped technology diffusion. This list is illustrative, not exhaustive, as many other open and subscription sources were reviewed to corroborate every datapoint.

Market-Sizing & Forecasting

A top-down construct translates procedure volumes for cardiac surgery, myocardial infarction admissions, and ICU bradycardia incidents into device demand, which is then multiplied by weighted average selling price to reach the base year value. Results are sense-checked with a selective bottom-up roll-up of manufacturer shipment disclosures and sampled hospital purchase orders. Key variables tracked include annual open-heart surgery count, incidence of post-operative conduction block, average days on pacing support, ASP progression, and regulatory approvals per geography. Forecasts to 2030 rely on multivariate regression blended with ARIMA smoothing, with scenario ranges aligned to expert consensus on aging demographics and technology upgrades. Data gaps from smaller economies are bridged using regional prevalence multipliers benchmarked against matched healthcare-spend cohorts.

Data Validation & Update Cycle

Every interim output passes a two-level analyst review where anomalies against historic ratios or sudden currency shifts trigger re-checks with interviewees. We refresh the model yearly, and we issue off-cycle updates if recalls, major reimbursement decisions, or disruptive product launches occur.

Why Our External Pacemakers Baseline Commands Reliability

Published figures often diverge because firms pick different device mixes, geographic spreads, and price anchors before projecting growth. Recognizing this, we isolate only acute-use external generators, convert revenues at constant 2024 dollars, and refresh input series annually, which keeps our baseline contemporary and comparable.

Key gap drivers include other publishers merging temporary devices with implantable units, using list prices rather than blended transaction prices, or extrapolating global totals from one region's usage pattern.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.88 B (2025) | Mordor Intelligence | |

| USD 1.83 B (2025) | Global Consultancy A | Includes select cardiac rhythm devices beyond external pacemakers and applies uniform ASP uplift across regions |

| USD 1.61 B (2025) | Trade Journal B | Limits geography to 25 countries and relies on five-year-old import data without adjustment for procedure growth |

| USD 1.89 B (2025) | Regional Consultancy C | Uses manufacturer list prices and excludes EMS procurements, inflating value but missing a key customer cohort |

Taken together, the comparison shows that Mordor Intelligence delivers a balanced, transparent figure rooted in clearly defined scope, current price realities, and a repeatable update cadence, giving decision-makers a dependable starting point for strategy and investment planning.

Key Questions Answered in the Report

What is the current size of the external cardiac pacemaker market?

The external cardiac pacemaker market generated USD 1.95 billion in 2026 and is projected to reach USD 2.35 billion by 2031.

Which segment holds the largest external cardiac pacemaker market share?

Transvenous systems led with 37.12% share in 2025, reflecting widespread clinical familiarity and reliable capture rates.

What is propelling growth in the Asia-Pacific external cardiac pacemaker market?

Rapid cath-lab expansion, ageing populations and national ambulance upgrades that carry pacing capability underpin a 4.59% CAGR outlook.

Why are dual-chamber external pacemakers gaining popularity?

Data show AV synchrony can boost cardiac output by up to 20%, and new leadless systems achieve high synchrony without traditional leads, driving a 5.08% CAGR for this modality.

How are reimbursement challenges affecting external cardiac pacemaker adoption?

High unit costs and complex Coverage-with-Evidence requirements limit uptake in smaller or resource-constrained facilities, creating geographical adoption gaps.

Page last updated on: