Europe Satellite Bus Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

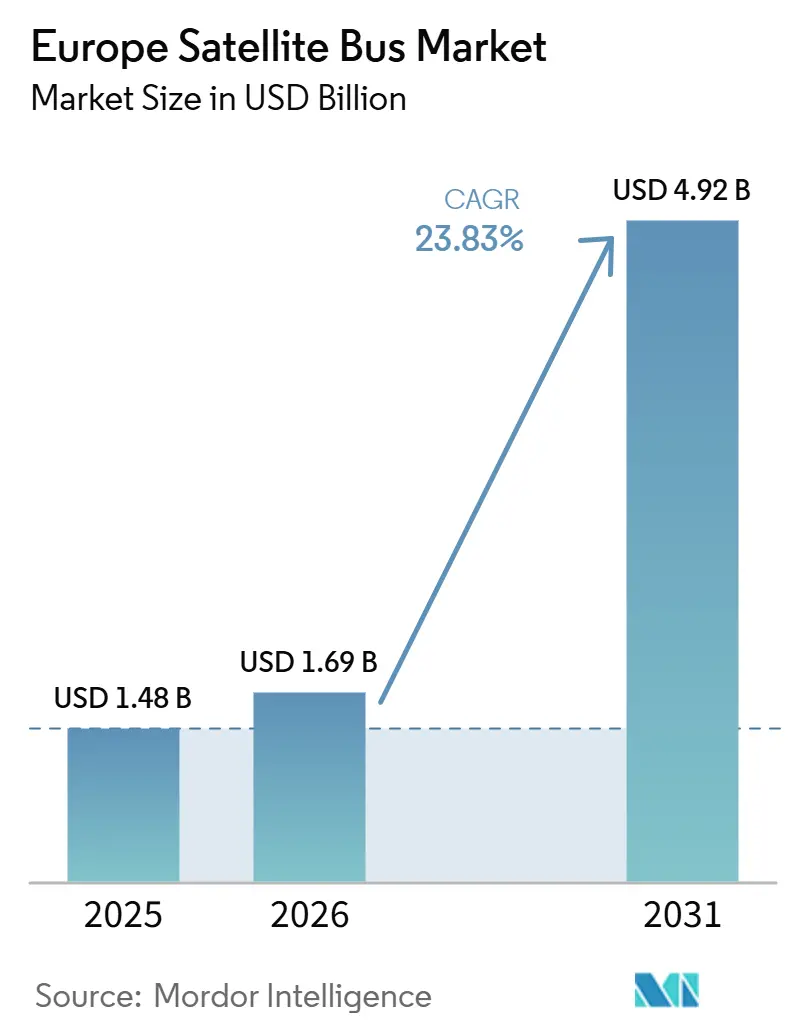

| Base Year Market Size (2025) | USD 1.48 Billion |

| Market Size (2026) | USD 1.69 Billion |

| Market Size (2031) | USD 4.92 Billion |

| Growth Rate (2026 - 2031) | 23.83% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Satellite Bus Market Analysis by Mordor Intelligence

The Europe satellite bus market size is projected to be USD 1.48 billion in 2025, USD 1.69 billion in 2026, and reach USD 4.92 billion by 2031, growing at a CAGR of 23.83% from 2026 to 2031. The market is entering a period of stronger demand as the IRIS² program has entered active procurement for a multi-orbit sovereign system comprising 272 LEO and 18 MEO satellites. It is also benefiting from factory-scale production capacity, as Thales Alenia Space has opened its Space Smart Factory in Rome and NanoAvionics has expanded its production capacity in Vilnius to serve large constellation orders. Secure connectivity requirements further support the Europe satellite bus market, as 6G NTN roadmaps and early 5G NTN demonstrations are driving demand for buses capable of handling multi-band payloads, software reconfiguration, and higher on-board power loads. Institutional procurement is adding another layer of support, as ESA, national governments, and defense agencies place greater emphasis on resilient Earth observation, secure SATCOM, and dual-use architectures. Competitive strategy is becoming more deliberate, with larger primes pursuing consolidation, while mid-tier suppliers are investing in specialized platforms, production lines, and institutional credibility, giving the current Europe satellite bus market a more operational character than earlier regional space buildouts.

Key Report Takeaways

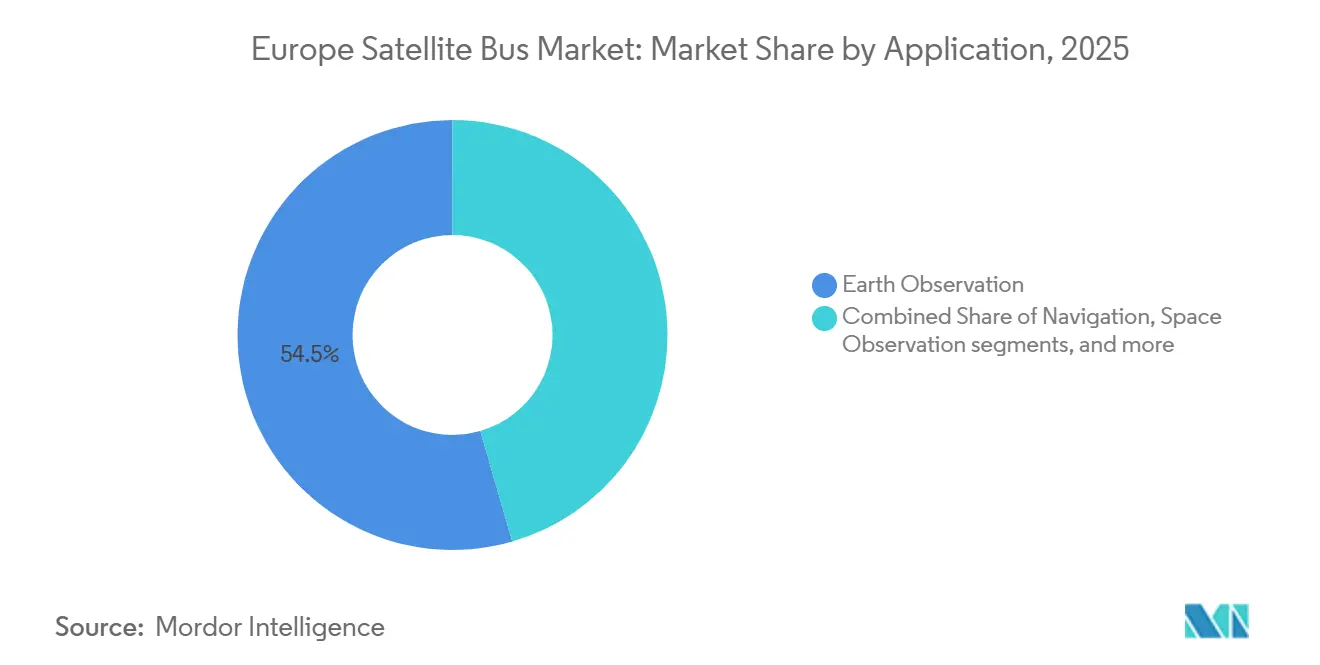

- By application, Earth observation accounted for 54.49% of revenue in 2025, while Space observation is projected to expand at a 24.65% CAGR through 2031.

- By satellite mass, the 100 to less than 500 kg class accounted for 49.51% of revenue in 2025, while the greater than 1,000 kg class is forecast to grow at a 25.36% CAGR through 2031.

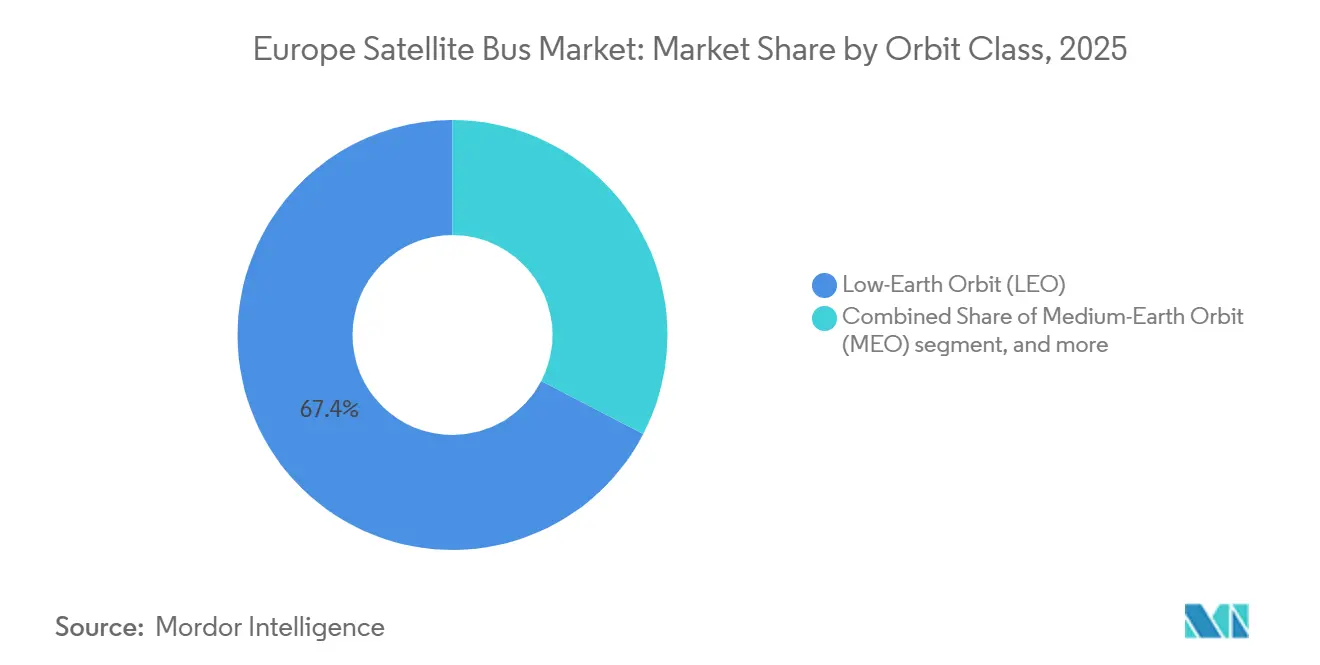

- By orbit class, LEO captured 67.38% share in 2025, while GEO is projected to grow at a 25.29% CAGR through 2031.

- By end user, commercial customers held 62.87% of the Europe satellite bus market share in 2025, while government and military are forecast to grow at a 26.56% CAGR through 2031.

- By geography, the United Kingdom accounted for 39.58% of the Europe satellite bus market in 2025, while Germany is projected to grow at a 25.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Satellite Bus Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU sovereign-backed LEO constellation demand | +6.50% | France, Germany, Italy, Belgium, Spain, Luxembourg | Medium term (2-4 years) |

| Increased ESA and defense procurement for resilient space assets | +4.00% | Europe wide, with spillover to the United Kingdom and Norway | Long term (≥ 4 years) |

| Surge in miniaturized high-throughput payloads for secure SATCOM and 6G NTN | +3.80% | United Kingdom, Germany, France | Medium term (2-4 years) |

| Standardization and mass-manufacturing of small-sat buses | +3.20% | Italy, Germany, Lithuania | Short term (≤ 2 years) |

| Demand for on-board processing and AI-enabled data handling | +2.20% | Belgium, Germany, United Kingdom | Short term (≤ 2 years) |

| Adoption of electric and air-breathing propulsion for long-life VLEO buses | +1.80% | Spain, France, Germany | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Sovereign-Backed LEO Constellation Demand (IRIS², OneWeb Extension)

The Europe satellite bus market is receiving a direct demand push from sovereign-backed LEO programs that now have defined procurement paths and clearer manufacturing schedules. ESA has framed IRIS² as a 12-year concession program for secure connectivity and resilience, and that program includes 272 LEO satellites and 18 MEO satellites that will require bus production across several European industrial sites.[1]European Space Agency, “ESA Programme Related to EU Secure Connectivity and IRIS²,” European Space Agency, resilience.esa.int This matters because a program of that size gives suppliers more confidence to qualify components, scale cleanroom capacity, and lock in supplier commitments before the first full production batches move through the line. The same pattern is evident in commercial LEO activity, where Airbus is already tied to large-scale OneWeb manufacturing demand and is aligning production around greater repeatability and shorter delivery cycles. Sovereign orders and commercial replenishment are therefore building capacity together instead of displacing one another, which is helping the Europe satellite bus market develop a broader production base. That mix lowers the risk of idle capacity and supports a more durable investment case for bus manufacturers, integrators, and qualified component suppliers.

Surge in Miniaturized High-Throughput Payloads for Secure SATCOM and 6G NTN

The Europe satellite bus market is also being shaped by payload changes, as payload miniaturization is now forcing platform redesign rather than simply improving payload efficiency. ESA's 6G NTN white paper set out a role for LEO satellites as native elements of future networks. That vision requires buses that can host software-reconfigurable payloads, optical links, and more advanced processing hardware within tighter mass and power envelopes. The commercial proof point came when Eutelsat, MediaTek, and Airbus completed a 5G NTN connection over OneWeb satellites in 2025, demonstrating that these architectures are no longer theoretical. Defense demand is reinforcing the same direction, as the CENTAURE agreement under the NEXUS framework confirms that governments are willing to pay for secure, low-latency LEO capacity when it meets military communication needs. For bus manufacturers, the result is not only higher payload sophistication but also pressure on thermal management, battery design, solar array performance, and on-board computing. That is why the Europe satellite bus market is seeing faster redesign cycles in the mid-weight classes, where secure SATCOM, EO, and network payloads now converge.

Standardization and Mass-Manufacturing of Small-Sat Buses (Assembly-Line)

The Europe satellite bus market is moving away from low-volume bespoke integration and toward repeatable assembly models that look more like industrial production. Thales Alenia Space has already opened a 5,000 m² Space Smart Factory in Rome, built around digital twins, robotics, and scalable constellation integration.[2]Thales Alenia Space, “Thales Alenia Space Awarded Contract as Prime Contractor for Two Copernicus Sentinel-1 NG Satellites,” Thales Alenia Space, thalesaleniaspace.com NanoAvionics has also expanded its Vilnius assembly and testing capacity after securing a EUR 122.5 million (USD 142 million) contract to build 280 satellites for the Meridian Space constellation, which shows that production readiness is now central to winning large orders. Airbus also used an assembly-line approach for the CO3D optical constellation, indicating that the production model is spreading beyond communications constellations into dual-use imaging programs. Once integration becomes more standardized, schedule risk shifts upstream toward processors, power systems, qualified materials, and other constrained inputs. That shift favors suppliers that can secure qualified inventories and stable component pipelines, and it gives the Europe satellite bus market a clearer path toward lower unit costs and shorter delivery times.

Increased ESA and Defense Procurement for Resilient Space Assets

The Europe satellite bus market is also benefiting from the way public procurement is changing, because resilience is now driving architecture decisions across civil and defense space programs. ESA has advanced programs that combine Earth observation, communications, and security objectives, while national governments are placing contracts for sovereign imaging, secure connectivity, and next-generation weather and radar assets. OHB Sweden's EPS-Sterna contract and Thales Alenia Space's Sentinel-1 Next Generation award demonstrate that European institutions continue to fund large, technically demanding missions that require reliable bus performance and manufacturing depth. This gives bus suppliers a more stable order environment than commercial cycles alone can provide, even if public programs move through longer review and qualification steps. It also helps the Europe satellite bus market build technical heritage that can later support commercial bids, because government missions often validate higher-specification designs under strict performance standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shrinking commercial GEO demand and video revenue erosion | -1.80% | GEO-heavy operators across Europe | Long term (≥ 4 years) |

| Limited European launch cadence and backlog of Ariane 6 | -1.30% | All European satellite programs | Short term (≤ 2 years) |

| Supply-chain exposure to critical materials and ITAR parts | -1.00% | Germany, France, Italy, and wider Europe | Long term (≥ 4 years) |

| Growing orbital-debris compliance costs in dense LEO | -0.80% | Global, with early policy relevance in the United Kingdom and France | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shrinking Commercial GEO Demand and Video Revenue Erosion

The Europe satellite bus market still faces a real constraint from the weakening commercial GEO business, because legacy video revenue no longer supports the same level of commercial platform replacement. Early 2026 operator results indicated weaker GEO revenue and stronger LEO connectivity revenue, suggesting that the center of operator spending is shifting away from traditional broadcast-focused systems. That change matters for bus manufacturers because commercial GEO programs once provided a dependable basis for large-platform design work, supply chain continuity, and engineering utilization. Governments are still ordering higher-capability GEO assets for secure communications and sovereign persistence, but public demand does not fully match the volume pattern that commercial broadcast platforms once generated. As a result, suppliers with deep heritage in large GEO buses have to redirect capacity toward defense, dual-use, and more software-defined architectures faster than in prior cycles. The Europe satellite bus market can still grow strongly under that shift, but the mix of future orders is becoming less forgiving for companies that remain tied to legacy commercial GEO demand.

Limited European Launch Cadence/Backlog of Ariane 6

The Europe satellite bus market also faces a timing constraint because launch availability is not scaling as quickly as satellite manufacturing plans. Ariane 6 completed 4 successful flights in 2025 and is targeting a higher cadence in 2026, yet the launch pipeline still has to absorb institutional missions, commercial commitments, and future IRIS² demand. This creates a practical issue for bus suppliers because spacecraft completed on time can still sit in storage while they wait for launch slots. Extended storage raises insurance, handling, and schedule management costs, and it can also complicate customer delivery milestones when buses are tied to fixed program windows. The problem is most visible during production ramp-up periods, when factories are being optimized for throughput, but launch manifests remain tighter than the new manufacturing rhythm. That mismatch does not alter long-term demand for the Europe satellite bus market, but it can pressure margins, working capital, and delivery confidence during the current scale-up phase.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Earth Observation Anchors, Space Science Missions Rise

Earth observation accounted for 54.49% of the market in 2025, making it the largest application segment within the Europe satellite bus market. This lead reflects the way surveillance, environmental monitoring, and sovereign intelligence requirements now overlap on a shared manufacturing base. Airbus strengthened that pattern in June 2026 when it signed an MoU with Rohde and Schwarz, Constellr, Orbint, and HPS for a sovereign German space intelligence solution that combines national demand into one architecture.[3]Airbus, “A Sovereign Space Intelligence Team, Airbus, Rohde and Schwarz, constellr, Orbint, HPS,” Airbus, airbus.com Airbus also demonstrated that Earth observation manufacturing can be repeated more efficiently by launching the CO3D constellation using an assembly-line model drawn from automotive and aeronautical methods. Within the Europe satellite bus industry, this application remains attractive because it combines recurring institutional demand with growing military urgency and clearer dual-use value. Communications and navigation still matter, but Earth observation has become the most visible anchor for near-term bus deployment, especially where security, revisit rate, and data sovereignty carry equal weight.

Space observation is projected to expand at a 24.65% CAGR through 2031, making it the fastest-growing application in the Europe satellite bus market. ESA's adoption of the ARRAKIHS mission in June 2026 added another science mission that will require precision pointing, stable structures, and low-vibration platform performance. OHB's role in the PLATO mission also shows that science programs remain an important route for European suppliers to build flight heritage on complex buses before pursuing broader institutional work. That matters because science missions validate core platform capabilities that later become useful in defense imaging, high-value observation, and specialized communications programs. The Europe satellite bus market size for Earth observation was the largest in 2025. Yet, the growth profile in science-led missions suggests that higher-specification niche platforms will gain more visibility during the forecast period. This pattern supports a two-track market where repeatable observation buses drive scale. At the same time, science programs lift technical credibility and help smaller or mid-tier suppliers move up the value chain.

By Satellite Mass: Mid-Weight Platforms Dominate, Heavyweight Missions Rise

The 100 to less than 500 kg class accounted for 49.51% of the market in 2025, making it the core mass segment in the Europe satellite bus market. That position comes from its ability to serve LEO Earth observation, secure SATCOM, IoT, and hosted-payload missions without the cost burden of heavier platforms. In practical terms, this class is where assembly-line economics and mission versatility meet most effectively, which is why it remains central to the Europe satellite bus market. NanoAvionics has used its MP42 bus in that broad weight range to support missions that combine defense-grade SAR, neutrino science, and quantum key exchange on a single launch campaign. That mix shows why the mid-weight category continues to attract both sovereign and commercial buyers, since it balances launch flexibility with enough payload headroom for demanding missions. The category also benefits from shorter design cycles than large platforms, which matters when customers want faster replenishment, newer processors, or updated propulsion options within a stable bus family.

Satellites weighing greater than 1,000 kg are forecast to record the fastest CAGR at 25.36% through 2031, indicating that heavy platforms are regaining strategic relevance in the Europe satellite bus market. The demand is being driven by large defense surveillance satellites, sovereign GEO communications systems, and complex science missions that still need higher power, larger structures, and longer design life. Luxembourg's approval of the GovSat-2 project in January 2026 is a clear signal that governments are still willing to support large, secure communications spacecraft when mission assurance is critical. This is important because headline commentary on GEO weakness can obscure the fact that public customers are replacing some legacy commercial demand with higher-value sovereign systems. Heavy platforms do not yet lead the Europe satellite bus market by market share. Still, their value per mission is rising, and their procurement logic is becoming more defense-led than operator-led. Qualification standards also remain tougher in this class, which raises timelines but protects incumbents and capable regional suppliers from easier outside competition in sensitive tenders.

By Orbit Class: LEO Leads, GEO Rebounds on Defense Demand

LEO held a 67.38% share in 2025, giving it the largest orbital position within the Europe satellite bus market. That lead reflects the accumulation of constellation programs across imaging, secure communications, hosted payloads, and technology demonstration. LEO platforms also support a procurement model that governments now favor because mission risk can be spread across multiple satellites rather than concentrated in a few large assets. NanoAvionics illustrated that logic with the N3X maritime surveillance constellation for the Norwegian Armed Forces, in which microsatellites provide repeated, mission-focused coverage rather than relying on a single platform. The Europe satellite bus industry is therefore treating LEO not only as a lower-cost orbit but also as a strategic architecture that fits resilience, refresh cycles, and mixed civil-defense demand. MEO remains narrower and is more closely tied to navigation and the MEO layer of IRIS². However, it still has a place in the regional bus roadmap because it carries distinct radiation and mission-design needs.

GEO is projected to witness the fastest growth at 25.29% CAGR through 2031, giving the European satellite bus market an unusual orbit mix in which the largest share and the fastest growth sit in different classes. This apparent contrast makes sense because bus procurement and operator revenue are moving in different directions, with public agencies ordering higher-value sovereign GEO systems even as commercial GEO video economics weaken. GovSat-2 supports that pattern by pointing to continued investment in secure and government-focused GEO communications capacity. The trend also aligns with software-defined payloads, greater power-conditioning needs, and the push for more capable thermal management on fewer, more strategic spacecraft. In that setting, a single GEO order can carry far more value than a smaller LEO platform, even if total unit volume remains lower. The Europe satellite bus market size linked to LEO remains dominant today. Still, the forecast path shows that Europe will continue to fund a more balanced orbital portfolio, with sovereign GEO retaining a strategic role.

By End User: Commercial Leadership Meets Government Acceleration

Commercial customers held a 62.87% share in 2025, keeping them the largest end-user base in the Europe satellite bus market. That base is still anchored by constellation replenishment, new commercial buildouts, and the need to refresh satellites according to design life rather than quarterly revenue shifts. Airbus's manufacturing work for the next wave of OneWeb satellites reflects how strong replenishment logic can persist even as customer priorities evolve toward secure, low-latency services. Commercial manufacturers are also seeking to improve their access to sovereign demand, as long-term growth now depends on demonstrating local production, security alignment, and platform flexibility rather than on scale alone. That is why bus suppliers are pairing constellation volume with institutional credibility rather than treating commercial and public markets as separate tracks. The Europe satellite bus market still needs commercial demand to sustain factory utilization and cost learning, even as government procurement increasingly shapes the direction of product design.

Government and military end users are projected to grow at a 26.56% CAGR through 2031, making it the fastest-growing end-user group in the Europe satellite bus market. France's DESIR award, Germany's stronger sovereign ISR posture, and the broader shift toward secure communications and resilient observation platforms all point in the same direction. Military buyers are also demanding stronger control over data, mission assurance, and industrial access, which creates room for European bus suppliers that can satisfy national security review processes. The downside is that classified procurement takes longer because those orders pass through more technical, legal, and security gates than commercial deals do. Even so, once these programs enter execution, they often support greater mission value, tighter customer relationships, and follow-on work for upgrades or replenishment. That is why the Europe satellite bus market is likely to keep a commercial volume base while government and military demand increasingly determines the slope of future growth.

Geography Analysis

The United Kingdom held a 39.58% share of the Europe satellite bus market in 2025, keeping it the largest national market in the region. That position rests on a concentrated industrial base around Stevenage, Portsmouth, Guildford, Surrey, and Oxford, where prime contractors and specialist suppliers are already established. The UK Space Agency reported that the wider space sector generated GBP 18.90 billion (USD 25.40 billion) in revenue and employed 55,000 people directly in 2025-2026, which supports the depth of the domestic ecosystem. Government procurement is also active, as the Oberon satellite contract awarded to Airbus ties defense capability to local jobs and domestic subsystem participation. In the Europe satellite bus market, that combination of industrial concentration and official demand keeps the UK ahead in current value, even as continental Europe accelerates.

France remains a major market because it integrates CNES, DGA, Airbus, Thales Alenia Space, and broader sovereign program activity into a single national system. The DESIR program and the CO3D constellation show how France continues to back dual-use radar and optical capabilities through domestic industrial partners. Germany is projected to expand at a 24.81% CAGR through 2031, making it the fastest-growing geography in the Europe satellite bus market. Germany's rise is supported by a mix of military SAR activity, stronger sovereign communications interest, OHB's institutional programs, and the Airbus-led ISR consortium signed in Berlin. The country is also benefiting from new-space manufacturing around Munich and Berlin, which broadens the supply base beyond traditional prime contractors.

The Rest of Europe adds important specialist capabilities, even when it does not match the scale of the largest national markets. Italy contributes through the Rome Space Smart Factory and platform development activities; Lithuania contributes through NanoAvionics' satellite production base; Spain contributes through science and optical mission roles; Belgium contributes through space-based AI computing; and Luxembourg contributes through secure government communications programs. Russia's role in the regional supply picture has weakened under export controls and sanctions, reducing its engagement with European bus programs and shifting greater emphasis toward internal European sourcing. That change has created both a supply gap and an incentive for European component and subsystem suppliers to deepen local capability. As a result, the Europe satellite bus market is not only led by the largest national clusters, but also reinforced by a wider network of specialized suppliers across the region.

Competitive Landscape

The Europe satellite bus market remains moderately consolidated at the prime level, because a small group of major suppliers still captures much of the value in institutional and sovereign programs. Airbus, Leonardo, and Thales signed a MoU in October 2025 to combine satellite and space systems activities into a new joint venture with annual revenue of EUR 6.50 billion (USD 7.44 billion) and a workforce of around 25,000, demonstrating how the largest players are responding to scale, cost, and strategic pressures. That planned consolidation could further tighten the prime tier, especially in large institutional contracts where heritage, qualification depth, and political confidence matter as much as price. At the same time, the Europe satellite bus market still leaves room for mid-tier firms that can deliver faster, more modular, or more cost-effective buses for constellation and dual-use missions. OHB maintains an important place in that group through institutional work such as EPS-Sterna and science heritage, which continue to support its credibility with public customers.

NanoAvionics occupies a valuable middle position in the Europe satellite bus market because it serves commercial, institutional, and defense missions without competing only on the same basis as large primes. Its Meridian Space order, ESA IOD and IOV selection, Kepler partnership, and Eycore-linked SAR mission show a company using repeatable buses to expand from smallsat manufacturing into more demanding sovereign and hosted-payload work. Thales Alenia Space is strengthening its competitive position through both capacity and program wins, with the Rome Space Smart Factory on one side and major institutional contracts such as Sentinel-1 Next Generation on the other. Airbus is using a similar dual strategy through industrial partnerships, Earth observation programs, and secure communications manufacturing tied to large constellation needs.

Technology is becoming a stronger differentiator inside the Europe satellite bus market, especially in on-board processing, AI-enabled computing, and more efficient data handling. ESA-backed in-orbit work with EDGX's STERNA platform showed that compact satellites can now run stronger AI processing in orbit, which can reduce downlink demand and improve mission responsiveness. NVIDIA's 2026 space computing launch aligns with this trend by raising the performance ceiling that bus makers will now try to integrate into future designs. This gives incumbents an edge when they can combine heritage with upgraded computing architecture, but it also opens room for smaller suppliers with more modular platforms. The result is a Europe satellite bus market where concentration is real at the top. Yet, competitive dynamics remain active because mid-tier firms are still finding ways to win on specialization, responsiveness, and platform flexibility.

Europe Satellite Bus Industry Leaders

Airbus SE

Lockheed Martin Corporation

Northrop Grumman Corporation

Thales Alenia Space (Thales Group)

Honeywell Aerospace Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Thales Alenia Space secured the first tranche of a EUR 700 million (USD 800.78 million) European Space Agency (ESA) contract to develop two Sentinel-1 Next Generation (Sentinel-1NG) Earth observation satellites under the Copernicus program. As the prime contractor, Thales Alenia Space will lead the mission, with Airbus Defence and Space serving as the main partner responsible for the C-band Synthetic Aperture Radar (SAR) instrument.

- October 2024: Eutelsat and Airbus signed a EUR 100 million (USD 109.04 million) OneWeb Gen-2 production contract for 100 satellites, Europe’s largest LEO constellation agreement to date.

- July 2024: Germany’s MoD awarded a EUR 2.10 billion (USD 2.44 billion) military SATCOM contract to an Airbus–OHB consortium, strengthening sovereign communications capability.

Europe Satellite Bus Market Report Scope

A satellite bus is the primary spacecraft platform that houses and integrates the non-payload subsystems required to operate a satellite in orbit. It provides mechanical structure, electrical power generation and distribution, propulsion, thermal regulation, attitude determination and control, command and data handling, and telemetry, tracking, and communication interfaces. The bus maintains spacecraft stability, manages onboard resources, supports payload pointing, controls orbital maneuvers, routes mission data, and enables continuous health monitoring, fault management, and command execution throughout the satellite's operational life.

The Europe satellite bus market is segmented by application, satellite mass, orbit class, end-user, and geography. By application, the market is segmented into communications, Earth observation, navigation, space observation, and others. By satellite mass, the market is segmented into less than 10 kg, 10 to less than 100 kg, 100 to less than 500 kg, 500 to less than 1,000 kg, and greater than 1,000 kg. By orbit class, the market is segmented into low Earth orbit (LEO), medium Earth orbit (MEO), and geosynchronous Earth orbit (GEO). By end-user, the market is segmented into commercial, government and military, and others. The report also covers the market sizes and forecasts for the Europe satellite bus market in four countries across the region. For each segment, the market size is provided in terms of value (USD).

| Communication |

| Earth Observation |

| Navigation |

| Space Observation |

| Others |

| Less than 10 kg |

| 10 to Less than 100 kg |

| 100 to Less than 500 kg |

| 500 to Less than 1,000 kg |

| Greater than 1,000 kg |

| Low-Earth Orbit (LEO) |

| Medium-Earth Orbit (MEO) |

| Geosynchronous Orbit (GEO) |

| Commercial |

| Government and Military |

| Others |

| United Kingdom |

| France |

| Germany |

| Russia |

| Rest of Europe |

| By Application | Communication |

| Earth Observation | |

| Navigation | |

| Space Observation | |

| Others | |

| By Satellite Mass | Less than 10 kg |

| 10 to Less than 100 kg | |

| 100 to Less than 500 kg | |

| 500 to Less than 1,000 kg | |

| Greater than 1,000 kg | |

| By Orbit Class | Low-Earth Orbit (LEO) |

| Medium-Earth Orbit (MEO) | |

| Geosynchronous Orbit (GEO) | |

| By End User | Commercial |

| Government and Military | |

| Others | |

| By Geography | United Kingdom |

| France | |

| Germany | |

| Russia | |

| Rest of Europe |

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.