Acrylonitrile Butadiene Styrene (ABS) Resin Market Size and Share

Market Overview

| Study Period | 2024 - 2030 |

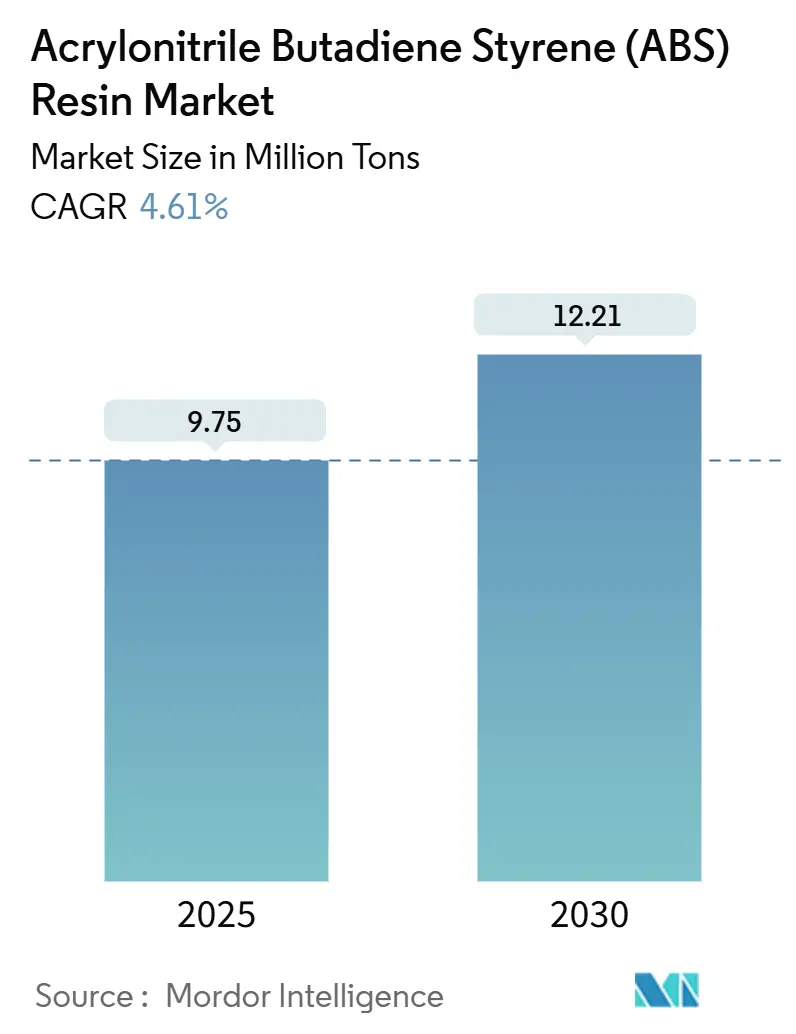

| Market Volume (2025) | 9.75 Million tons |

| Market Volume (2030) | 12.21 Million tons |

| Growth Rate (2025 - 2030) | 4.61% CAGR |

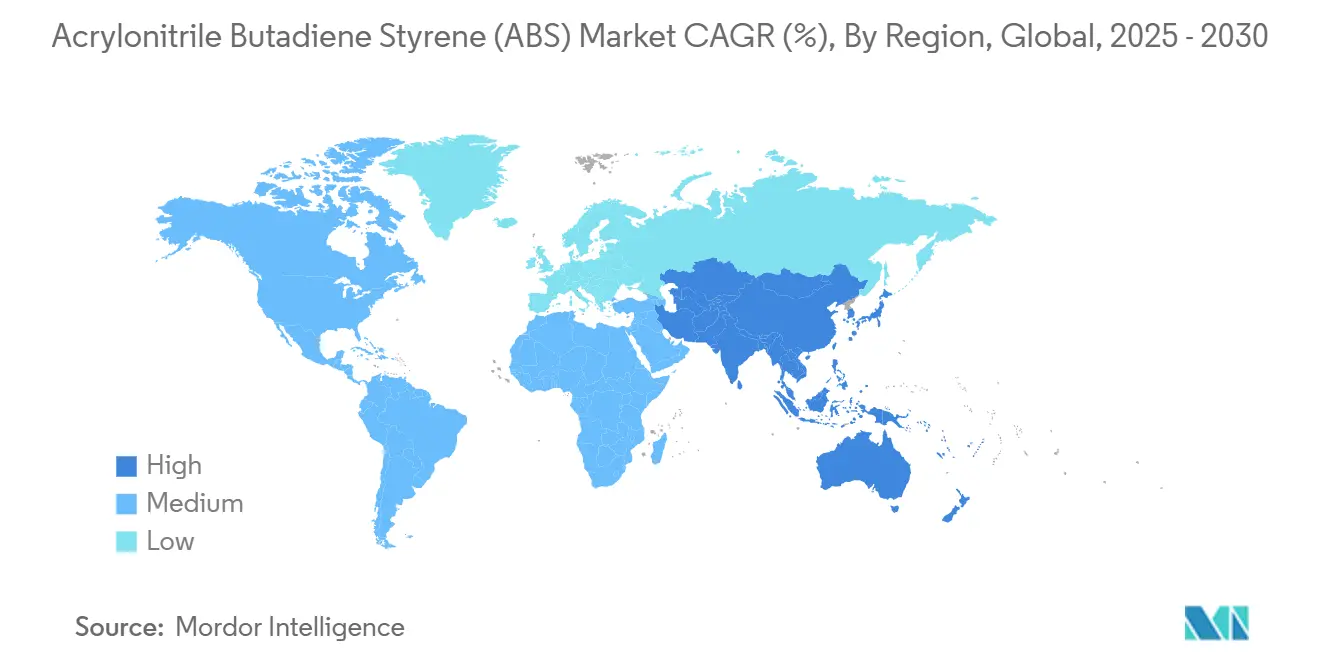

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Acrylonitrile Butadiene Styrene (ABS) Resin Market Analysis by Mordor Intelligence

The acrylonitrile butadiene styrene market stood at 9.75 million tons in 2025 and is forecast to reach 12.21 million tons by 2030, advancing at a 4.61% CAGR. Consistent demand stems from the resin’s strength-to-weight ratio, chemical resistance, and ease of processing, qualities that continue to attract high-volume users in automotive, electronics, and construction. Electric-vehicle platforms now specify reinforced ABS grades to replace aluminum brackets and housings, saving up to 40% in weight and 20% in cost while preserving structural integrity. Tight coupling between 5 G infrastructure build-outs and electroplatable ABS grades for antenna housings further widens the resin’s opportunity set.

Key Report Takeaways

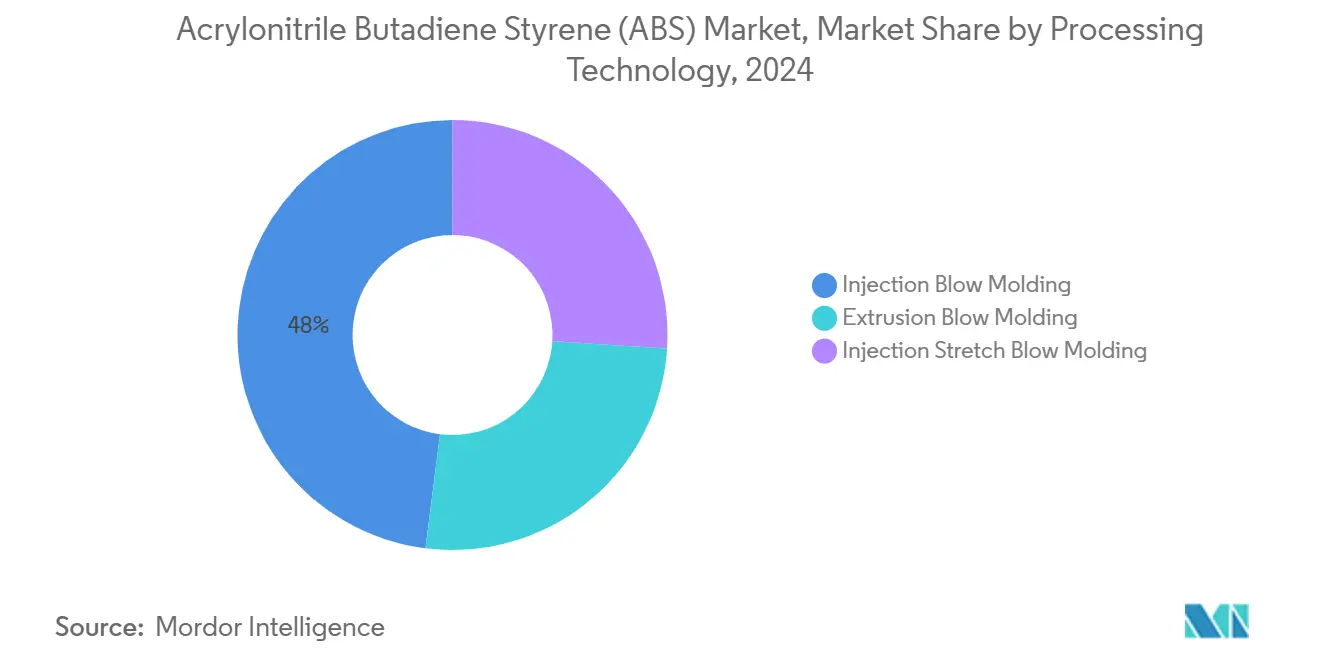

- By processing technology, Injection Blow Molding held 48% of the acrylonitrile butadiene styrene market share in 2024; it is projected to grow at a 5.15% CAGR to 2030.

- By ABS grade, General-Purpose formulations accounted for 37% of the acrylonitrile butadiene styrene market size in 2024, while Flame-Retardant grades are forecast to expand at a 6.56% CAGR.

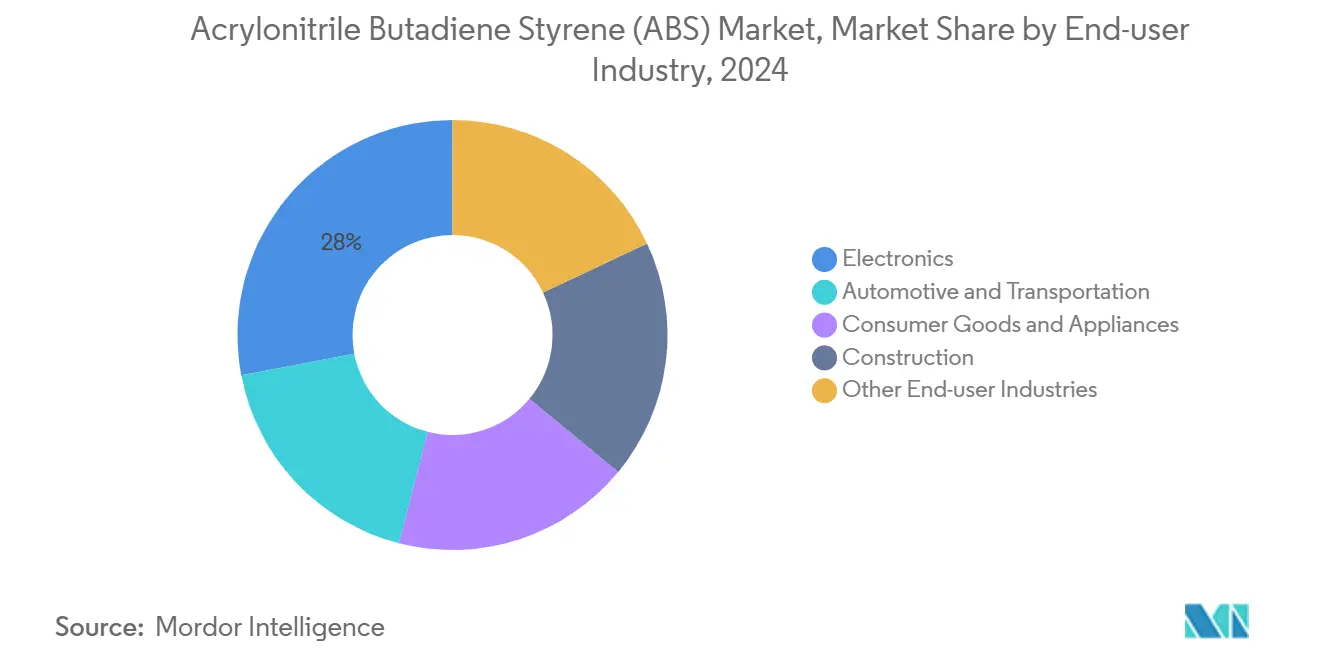

- By end-user industry, Electronics and Appliances commanded 28% of the acrylonitrile butadiene styrene market size in 2024, while the consumer goods and appliances is advancing at 6.2% CAGR through 2030.

- By geography, Asia-Pacific captured 75% of the acrylonitrile butadiene styrene market share in 2024; the region leads growth at 5.17% CAGR to 2030.

Global Acrylonitrile Butadiene Styrene (ABS) Resin Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweighting and Metal Replacement in E-Mobility Platforms | +1.2% | Global, with concentration in Europe, North America, and China | Medium term (2-4 years) |

| Smart-Home Appliances Requiring High-Gloss Heat-Resistant Grades | +0.9% | North America, Europe, and Asia-Pacific urban centers | Short term (≤ 2 years) |

| Rapid Adoption of Desktop 3-D Printers in Education | +0.7% | North America and Europe, with emerging adoption in Asia-Pacific | Medium term (2-4 years) |

| Mandatory Flame-Retardant Cockpit Components | +0.8% | Global, with emphasis on regions with stringent automotive safety regulations | Medium term (2-4 years) |

| 5G Infrastructure Driving Electroplatable ABS Demand | +0.6% | Global, with concentration in Asia-Pacific and North America | Short term (≤ 2 years) |

Source: Mordor Intelligence

Lightweighting and Metal Replacement in E-Mobility Platforms

- Electric-vehicle designers target mass reduction to extend driving range, and reinforced ABS grades are replacing metal brackets, ducts, and enclosures at scale. Glass-fiber-modified grades achieve tensile strengths above 75 MPa yet weigh 40% less than aluminum, aligning with the U.S. Department of Energy's goal of trimming 25% off light-duty vehicle curb weight by 2030. Automakers also cite lower tooling costs and faster cycle times, which compress program launch schedules. The acrylonitrile butadiene styrene market benefits directly as battery-pack makers specify resin housings that integrate fasteners and cooling channels.

Smart-Home Appliances Requiring High-Gloss Heat-Resistant Grades

- Connected home devices pack advanced processors into sleek casings that must withstand sustained temperatures near 100 °C. Appliance OEMs validate glossy, heat-stabilized ABS formulations that retain dimensional accuracy and resist discoloration over multi-year duty cycles. Brand owners also cite the polymer’s compatibility with laser-etch debossing, enabling seamless back-lit logos without secondary operations. Short product-refresh cycles maintain high baseline demand and encourage formulators to accelerate color-match services.

Rapid Adoption of Desktop 3-D Printers in Education

- K-12 and tertiary institutions now deploy desktop additive-manufacturing systems in STEM labs, modelling the engineering workflow from digital design to finished part. Classroom operators prefer resin filament with predictable extrusion behavior, low warp, and moderate emission profiles, making ABS the default material next to PLA. Annual hardware installations rise as state curricula embed additive-manufacturing competencies, expanding per-capita filament consumption. The acrylonitrile butadiene styrene market, therefore, captures steady growth through public-sector budgets rather than cyclical consumer spending.

Mandatory Flame-Retardant Cockpit Components

- Global safety standards push automakers toward UL-94 V-0 ratings for dashboards, consoles, and infotainment bezels. Flame-retardant ABS meets mechanical and aesthetic targets without compromising recyclability when producers remove halogenated additives. Regulations in Europe and North America already restrict PFAS, prompting OEMs to seek drop-in replacements that maintain gloss and color depth. Medium-term demand growth is therefore anchored in compliance schedules.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Acrylonitrile Feedstock Prices | -0.7% | Global, with higher impact in regions without integrated production | Short term (≤ 2 years) |

| Substitution by Bio-based Polymers in Electronics | -0.5% | Europe and North America, with gradual expansion to Asia-Pacific | Medium term (2-4 years) |

| Stringent Nordic VOC Limits on Processing Plants | -0.3% | Nordic countries, with potential expansion to broader EU | Medium term (2-4 years) |

Source: Mordor Intelligence

Substitution by Bio-Based Polymers in Electronics

- Consumer-electronics brands increasingly trial halogen-free biopolymer blends with carbon footprints seven times lower than ABS while still achieving UL-94 V-0 ratings. Europe’s Chemicals Strategy for Sustainability tightens scrutiny on petrochemical-derived materials, nudging procurement guidelines toward renewable content. American brands pursue ESG scorecard improvements that raise evaluation hurdles for traditional ABS unless accompanied by recycled content. The acrylonitrile butadiene styrene market retains incumbency where cost, processability, and supply reliability still dominate, yet faces gradual displacement in premium segments.

Stringent Nordic VOC Limits on Processing Plants

- Regulators in Sweden, Finland, and Denmark sharpen occupational exposure limits for styrene and ultrafine particles emitted during compounding. Compliance forces processors to retrofit ventilation systems and adopt closed-loop extrusion lines, increasing capital expenditures and operational outlays. Smaller moulders may relocate or exit, reducing local ABS throughput. If the broader EU adopts similar thresholds, investment deferrals could slow capacity upgrades in legacy plants, trimming medium-term acrylonitrile butadiene styrene market growth. Equipment makers respond with low-shear screw designs that dampen volatiles, but payback periods create financial friction.

Segment Analysis

By Processing Technology: Injection Blow Molding Maintains Production Edge

- Injection Blow Molding secured 48% of 2024 production volume and is growing 5.15% annually, reflecting its efficiency in turning pellets into complex parts with minimal post-processing. Thin-wall capability enables brand owners to cut resin usage without performance loss, supporting sustainability scorecards. Real-time cavity-pressure feedback and conformal-cooling inserts shave cycle times by up to 18%, translating into higher line uptime.

Note: Segment shares of all individual segments available upon report purchase

By ABS Grade: Flame-Retardant Formulations Accelerate

- General-Purpose ABS retained a 37% share in 2024, but Flame-Retardant grades expand at a 6.56% CAGR as safety regulations stiffen across electronics and mobility. Chemical suppliers shift away from brominated systems toward phosphorous and nitrogen synergists that comply with global RoHS and PFAS restrictions. High-Impact variants continue to dominate toys and power-tool housings, where drop performance matters, while electroplating grades climb on the back of 5 G radio hardware. Heat-Resistant types find a stable niche in under-hood automotive parts, capable of continuous service at 110 °C.

By End-User Industry: Electronics Convergence Leads Consumption

- Electronics and Appliances absorbed 28% of global volume in 2024, and Consumer Goods and Appliances will grow 6.2% yearly through 2030. Smart-home ecosystems combine sensors, processors, and wireless modules into design-rich housings that must resist scratches and provide EMI shielding. Multi-shot moulding of ABS with transparent PC lenses simplifies assembly, cuts the bill-of-materials cost, and accelerates product cycles.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific dominated the acrylonitrile butadiene styrene market with 75% volume in 2024 and will grow 5.17% annually through 2030. China anchors supply and demand by combining world-scale crackers, extensive compounding expertise, and proximity to high-growth consumer-electronics hubs.

North American demand is stable yet shifts toward premium grades. The average car built in 2025 contains 426 lb of plastics, with ABS supplying interior trims, bezels, and taillight modules. In Europe, policy-driven sustainability triggers higher recycled-content targets for automotive polymers, nudging OEMs toward circular ABS streams[1]Publications Office of the European Union, “Recycled Plastic Content Targets in New Passenger Cars,” europa.eu. Simultaneously, stricter emission controls in Nordic processing plants raise compliance.

Brazil’s appliance and automotive sectors underpin regional consumption, while Argentina and Colombia explore near-shoring of electronics assembly. Gulf Cooperation Council states leverage feedstock advantage and a 93% capacity-utilization rate to pivot from export-grade feedstock to local sheet and compound production[2]Gulf Petrochemicals and Chemicals Association, “GPCA Annual Report 2024,” gpca.org.ae

Competitive Landscape

- The top five suppliers account for about 55% of installed capacity worldwide, suggesting moderate concentration. INEOS, LG Chem, and SABIC leverage integrated feedstock chains to navigate acrylonitrile volatility, while regionally entrenched firms fine-tune grade portfolios for local specifications. Asia-Pacific hosts aggressive pricing dynamics as new entrants commission reactors with state-backed integration.

Acrylonitrile Butadiene Styrene (ABS) Resin Industry Leaders

-

LG Chem

-

INEOS

-

CHIMEI

-

SABIC

-

Trinseo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Trinseo launched MAGNUM ECO+, MAGNUM CR, and TYRIL CR recycled-content ABS and SAN resins for mobility and consumer goods, offering up to 18% lower carbon footprints while matching incumbent performance

- January 2024: BEPL (Bhansali Engineering Polymers) announced plans to expand ABS capacity in Rajasthan, India, to 145,000 tons per year within two years, supporting the domestic appliance and automotive sectors

Global Acrylonitrile Butadiene Styrene (ABS) Resin Market Report Scope

Acrylonitrile butadiene styrene (ABS) resin is a thermoplastic polymer, and products manufactured from ABS resin offer properties such as colorability, dimensional stability, toughness, and resistance to high temperature and scratch.

The market is segmented based on process type, end-user industry, and geography. By process type, the market is segmented into injection blow molding, extrusion blow molding, and injection stretch blow molding. By end-user industry, the market is segmented into automotive and transportation, construction, electronics, consumer goods and appliances, and other end-user industries (medical tools). The report also covers the market size and forecasts for the acrylonitrile butadiene styrene (ABS) resin market in 27 countries across major regions. For each segment, the market sizing and forecasts are done based on volume (tons).

| By Processing Technology | Injection Blow Molding | ||

| Extrusion Blow Molding | |||

| Injection Stretch Blow Molding | |||

| By ABS Grade | General-Purpose | ||

| High-Impact | |||

| Electro-plating | |||

| Flame-Retardant | |||

| Heat-Resistant | |||

| By End-user Industry | Automotive and Transportation | ||

| Electronics | |||

| Consumer Goods and Appliances | |||

| Construction | |||

| Other End-user Industries | |||

| By Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Thailand | |||

| Vietnam | |||

| Malaysia | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Turkey | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| Qatar | |||

| Egypt | |||

| South Africa | |||

| Nigeria | |||

| Rest of Middle East and Africa | |||

| Injection Blow Molding |

| Extrusion Blow Molding |

| Injection Stretch Blow Molding |

| General-Purpose |

| High-Impact |

| Electro-plating |

| Flame-Retardant |

| Heat-Resistant |

| Automotive and Transportation |

| Electronics |

| Consumer Goods and Appliances |

| Construction |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Thailand | |

| Vietnam | |

| Malaysia | |

| Indonesia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Turkey | |

| Nordics | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What growth rate is expected for the acrylonitrile butadiene styrene market through 2030?

The market is forecast to expand at a 4.61% CAGR, reaching 12.21 million tons by 2030.

How does lightweighting in electric vehicles influence acrylonitrile butadiene styrene usage?

Reinforced ABS grades replace aluminum brackets and housings, cutting weight by up to 40% and cost by 20%, which boosts resin uptake in battery packs and interior parts.

Which region accounts for most acrylonitrile butadiene styrene consumption?

Asia-Pacific leads with 75% of global volume and shows the fastest regional growth at 5.17% CAGR.

Which end-use sector consumes the most acrylonitrile butadiene styrene today?

Electronics and Appliances hold 28% of worldwide demand and post the highest segment growth at 6.2% CAGR.

Page last updated on: June 16, 2025