Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

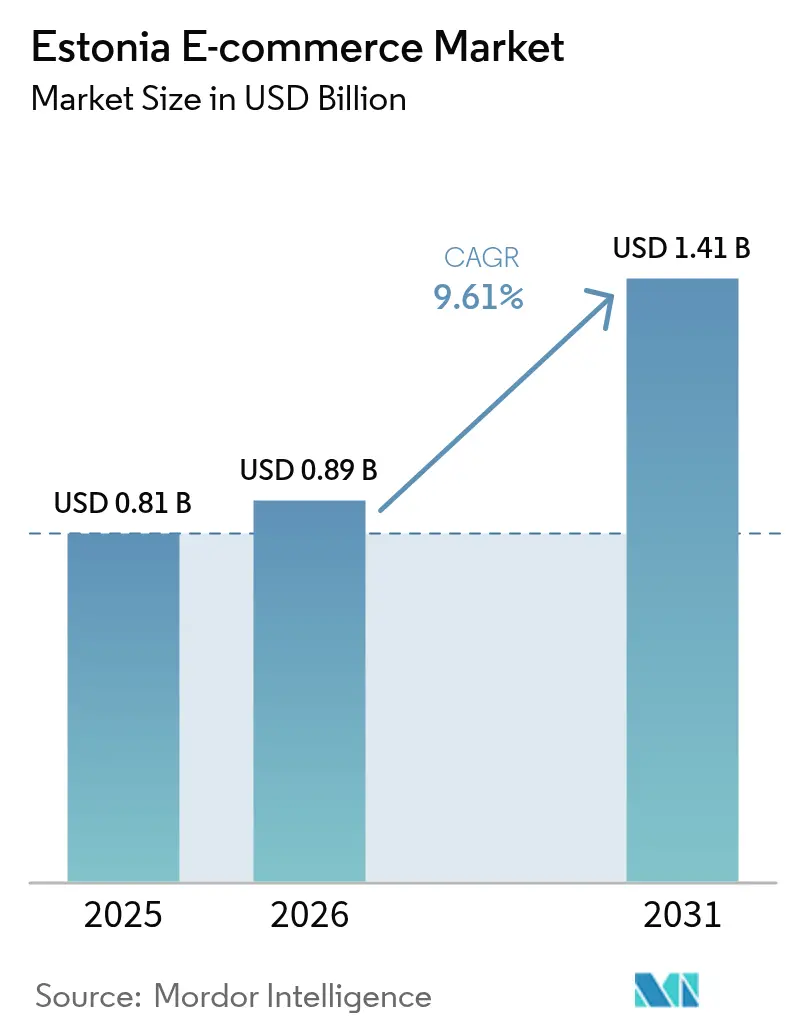

| Base Year Market Size (2025) | USD 0.81 Billion |

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 1.41 Billion |

| Growth Rate (2026 - 2031) | 9.61% CAGR |

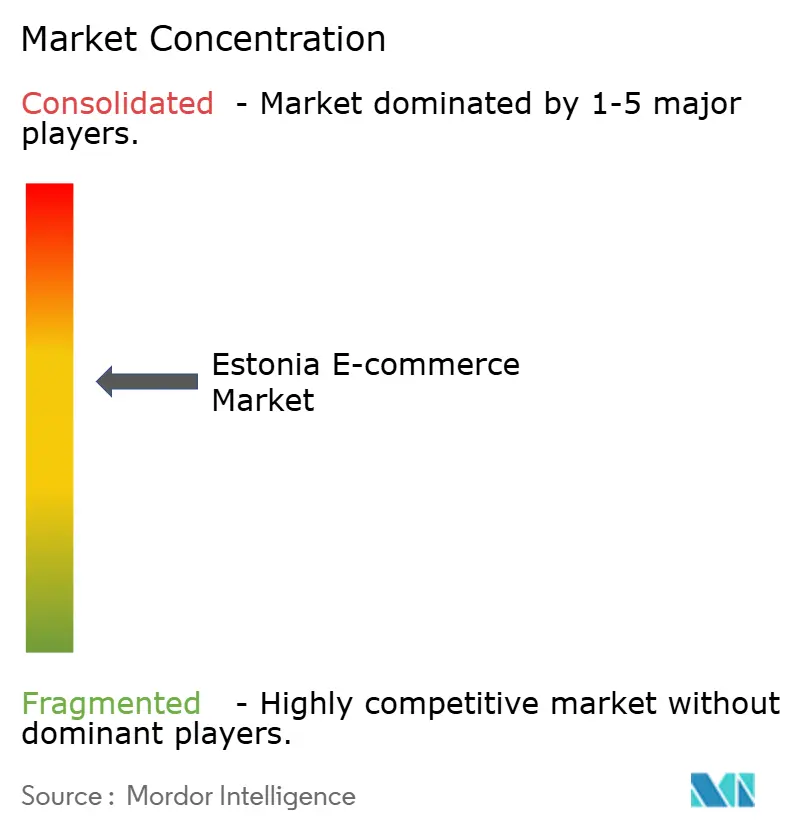

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Estonia E-commerce Market Analysis by Mordor Intelligence

Estonia e-commerce market size in 2026 is estimated at USD 887.84 million, growing from 2025 value of USD 0.81 billion with 2031 projections showing USD 1.41 billion, growing at 9.61% CAGR over 2026-2031. The Estonia e-commerce market has been shaped by a combination of advanced digital ID penetration, an export-oriented tech sector, and proximity to Nordic trade routes, allowing domestic and cross-border sellers to scale without heavy fixed-asset commitments. Local retailers have adopted parcel-locker logistics to cut last-mile costs, while international platforms leverage the e-Residency framework to open EU storefronts with minimal red tape. Fintech partnerships are enabling new payment flows that balance Estonia’s traditional bank-link habit with rising demand for Buy Now Pay Later services. On the supply side, warehouse capacity remains the main bottleneck, yet investments in automation and AI-driven demand planning are steadily easing the constraint.

Key Report Takeaways

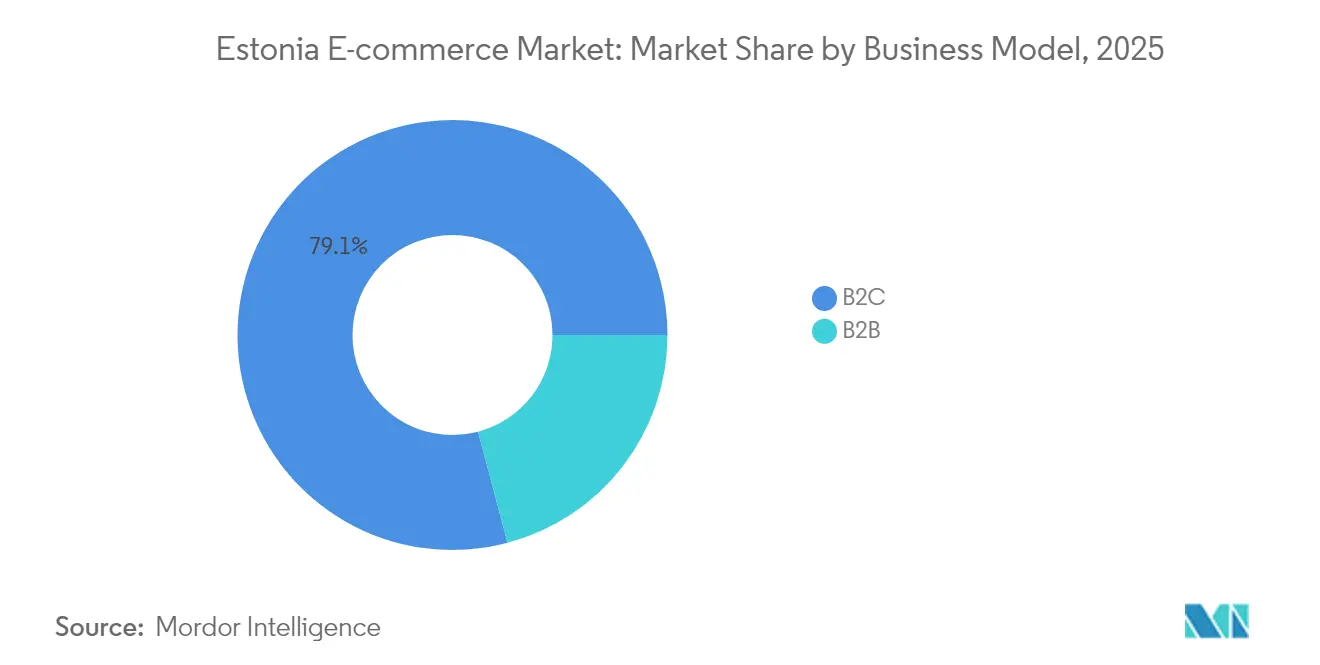

- By business model, B2C led with 79.12% revenue share in 2025; B2B is forecast to expand at an 11.63% CAGR through 2031.

- By device, smartphone/mobile captured 63.60% of the Estonia e-commerce market share in 2025 and is advancing at a 12.08% CAGR through 2031.

- By payment method, credit/debit cards accounted for 39.08% share of the Estonia e-commerce market size in 2025 while BNPL is projected to grow at 14.59% CAGR to 2031.

- By B2C product category, fashion & apparel held 24.62% revenue share in 2025; food & beverages is forecast to expand at a 14.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Estonia E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Parcel-Locker Culture Reducing Last-Mile Costs in Tallinn & Tartu | +2.1% | National, concentrated in Tallinn & Tartu | Medium term (2-4 years) |

| Government-Led e-Residency Programme Attracting Cross-Border Sellers | +1.8% | National, with spillover to EU market | Long term (≥ 4 years) |

| High Digital ID Penetration Enabling One-Click Checkout | +1.4% | National | Short term (≤ 2 years) |

| Widespread Bank-Link Payment Habit Boosting Trust in Online Purchases | +1.2% | National | Medium term (2-4 years) |

| EU Digital Services Act Forcing Marketplace Compliance – Favouring Local Niche Stores | +0.9% | EU-wide, early impact in Estonia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Parcel-Locker Culture Reducing Last-Mile Costs in Tallinn & Tartu

Extensive parcel-locker roll-outs have lowered delivery overheads by as much as 40% compared with door-to-door models, enabling retailers to protect margins during peak sales windows.[1]“Annual Report 2024,” Omniva Group, omniva.ee Omniva’s 2025 addition of 135 machines raises the Baltic locker count above 1,240, creating unprecedented pick-up convenience. Monthly locker usage exceeds 50% of Baltic consumers, a figure that surges around Black Friday and Singles’ Day events. Estonian logistics software firms now embed AI route optimisation to shorten driver kilometres and shrink carbon footprints, cementing the locker network as a durable differentiator within the Estonia e-commerce market. Export of this expertise, exemplified by Cleveron’s grocery-locker contracts in the United States, underscores the flywheel effect of local innovation.Government-Led e-Residency Programme Attracting Cross-Border Sellers

Government-Led e-Residency Programme Attracting Cross-Border Sellers

Nearly 100,000 global entrepreneurs have become e-residents, founding more than 15,000 Estonian-registered companies that trade throughout the EU.[2]e-Residency Team, “Statistics Dashboard,” e-Residency, e-residency.gov.ee The 0% corporate income tax on retained earnings lets digital merchants reinvest cash in inventory and customer acquisition more aggressively than in neighbouring jurisdictions. High-profile incorporations, such as Eric Schmidt’s drone venture, bolster Estonia’s brand equity as a frictionless launchpad for EU commerce. The influx of diverse sellers widens product assortments for local shoppers while intensifying price competition, reinforcing the Estonia e-commerce market’s reputation for agility.

High Digital ID Penetration Enabling One-Click Checkout

Digital ID covers 95.8% of citizens, and its integration with local banks enables one-click authentication that trims checkout steps and lowers abandonment by up to 30%.[3]“Digital Decade Policy Programme Progress Report 2024,” European Commission, ec.europa.eu Fewer security fears translate into a smaller share of shoppers who exit the funnel due to payment concerns than the EU average. The same ID rails facilitate automated VAT filing and smoother KYC for merchants, eliminating routine paperwork. This infrastructure, unique within Europe, directly boosts conversion rates and shortens working-capital cycles in the Estonia e-commerce market.

Widespread Bank-Link Payment Habit Boosting Trust in Online Purchases

A 22.6% capital-adequacy ratio underpins the banking sector, maintaining customer confidence in direct transfers that settle within seconds on the SEPA network. Merchants that optimise their interfaces for bank-link flows gain lower fraud exposure and better fee economics than card-centric rivals. BNPL products—championed by Inbank and ESTO—layer new flexibility on top of trusted rails rather than replacing them, letting consumers split payments without abandoning habitual payment environments. The synthesis of old and new payment logic differentiates the Estonia e-commerce market from card-dominated neighbours.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Warehouse Stock-Keeping Capacity for Flash-Sale Peaks | -1.6% | National, acute in Tallinn metropolitan area | Short term (≤ 2 years) |

| Ageing Rural Population Slowing Digital Adoption Outside Tallinn | -1.1% | Rural Estonia, excluding Tallinn-Tartu corridor | Long term (≥ 4 years) |

| Rising Cross-Border Return Costs to Germany & Finland | -0.8% | National, affecting cross-border e-commerce | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Warehouse Stock-Keeping Capacity for Flash-Sale Peaks Hinders the Market

Current stock-holding space cannot absorb high-velocity campaigns such as 11.11 or Black Friday, leading to rushed cross-docking and out-of-stock situations that erode shopper loyalty. Logistics overheads average 16% of GDP for manufacturing and trade firms, indicating suboptimal utilisation of freight and warehousing assets. Robotics pilots and AI demand-forecasting have improved picking accuracy, but physical expansion is still needed to stabilise fulfilment during spikes.

Ageing Rural Population Slowing Digital Adoption Outside Tallinn

Gigabit roll-outs backed by EUR 289 million (USD 314 million) in public and state funds promise full coverage, yet behavioural hurdles remain in sparsely populated counties. Older residents favour brick-and-mortar outlets and show limited interest in BNPL or app-based shopping, capping penetration ceilings. Multi-channel models that pair local pickup points with online interfaces offer a transitional path, but the demographic skew drags on the long-tail CAGR of the Estonia e-commerce market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2B Acceleration Outpaces B2C Maturation

B2C accounted for 79.12% revenue in 2025, anchoring the Estonia e-commerce market’s early trajectory. However, B2B orders are set to outstrip overall growth at 11.63% CAGR through 2031, driven by e-Resident technology consultancies that adopt digital procurement suites. Estonia’s 0% tax on retained profits encourages SMEs to reinvest surpluses in inventory and SaaS tools, reinforcing platform stickiness. The Estonia e-commerce market size allocated to B2B operations is projected to expand steadily as international clients exploit Estonian supply-chain gateways into the wider EU. Sophisticated buyers demand API-driven catalogues, encouraging local marketplaces to integrate AI-guided RFQ engines and embedded financing.B2C remains powerful due to deep mobile reach and fast fashion cycles. Yet customer-acquisition costs inflate as global marketplaces add localized Estonian pages. Consequently, leading grocers and fashion retailers build loyalty ecosystems that offer next-day locker delivery and in-app payment rewards. These defensive plays slow share erosion and preserve domestic gross margins.

By Device Type: Mobile Commerce Dominance Reshapes User Experience

Smartphone and tablet screens generated 63.60% of transactions in 2025 and will widen their lead with a 12.08% CAGR. The Estonia e-commerce market share commanded by mobile derives from 77% national 5G footprint and near-universal smartphone ownership. Augmented-reality try-ons for apparel as well as one-tap ID authentication compress purchase journeys into seconds. The Estonia e-commerce market size for mobile-centric transactions is set to reach USD 0.99 billion by 2031, reflecting seamless wallet integrations.Desktop remains relevant in B2B contexts where buyers evaluate bulk SKUs and negotiate payment terms. Dual-screen setups also support long research phases for high-value electronics, preserving average basket sizes. Connected TVs and IoT devices open new touchpoints for contextual commerce such as recipe-to-cart grocery top-ups, although adoption is nascent.

By Payment Method: BNPL Innovation Disrupts Traditional Banking Preferences

Cards capture 39.08% of payment volume, yet BNPL is scaling fastest at 14.59% CAGR. The Estonia e-commerce market size routed through BNPL could exceed USD 0.23 billion by 2031 if current momentum holds. Local banks co-create white-label instalment plans, ensuring regulatory alignment on consumer credit disclosures. As a result, default rates remain below regional averages, preserving lender risk appetite.Bank-link transfers, underpinned by instant SEPA, dominate repeat purchases in grocery and utilities. They exhibit the lowest direct cost per transaction, which reinforces merchant preference. Digital wallets ride mobile ubiquity yet stay niche in absolute terms, primarily serving younger segments that favour super-app experiences.

By B2C Product Category: Food & Beverages Surge Challenges Fashion Leadership

Fashion retained 24.62% revenue share in 2025 through rapid assortment refreshes and influencer-driven campaigns. Nevertheless, online grocery will post a 14.21% CAGR, narrowing the gap by 2031. Expanded cold-chain parcel lockers and same-day courier fleets allow fresh produce to arrive within two-hour windows, elevating shopper trust. The Estonia e-commerce market size allocated to food & beverages will correspondingly rise, supported by consolidation moves such as Barbora’s integration into Maxima’s Baltic network.Electronics leverages Estonia’s high export orientation; reverse-logistics loops enable refurbishment channels that feed secondary-market demand. Furniture and DIY categories see steadier growth as consumers migrate to click-and-collect models that circumvent high delivery surcharges.

Geography Analysis

Urban corridors dominate digital spending, with Tallinn and Tartu generating more than 70% of online GMV. These hubs benefit from dense parcel-locker grids, fibre connectivity, and youthful demographics. In Tallinn alone, daily locker pickups surpassed 65,000 in 2024, illustrating ingrained convenience culture. Suburban areas within a 30-minute drive of these cities enjoy spill-over effects as commuters adopt online subscriptions for repeat household needs.

Coastal regions that interface with Finland leverage ferry freight routes for same-day cross-border returns, making them attractive for fashion marketplaces handling Nordic shoppers. The Estonia e-commerce market experiences heightened weekend sales peaks when tourists supplement domestic demand.

Rural counties lag on both high-speed coverage and digital literacy. Government broadband subsidies coupled with mobile-enabled payment awareness campaigns aim to narrow this divide by 2028. Retailers pilot hybrid locker-van models, parking mobile pickup stations at village squares on market days to stimulate first-time digital orders. Over the long term, these initiatives widen the total addressable base for the Estonia e-commerce market without cannibalising urban volumes.

Regulatory Landscape

Estonia e-commerce operators operate under a combined national and EU rule-set, with the Consumer Protection and Technical Regulatory Authority (TTJA) overseeing consumer protection, market surveillance, and distance-selling compliance. Core obligations trace back to the Law of Obligations Act provisions on contracts concluded via communication means, including clear pre-contractual information, transparent final pricing, and a statutory 14-day withdrawal right. Marketplaces also work within EU requirements such as the Platform-to-Business (P2B) Regulation and broader EU platform compliance duties that interact with the Digital Services Act requirements referenced in market drivers.

For tax and cross-border trade, the Estonian Tax and Customs Board (EMTA) administers VAT and EU e-commerce special schemes including the One Stop Shop (OSS), which supports merchants selling cross-border to EU consumers from an Estonian base. A specific 2026 compliance and cost anchor is EMTA implementing EU-wide low-value import changes from July 1, 2026, including a fixed customs duty for consignments below EUR 150, which affects non-EU small-parcel flows and the economics of low-ticket cross-border orders.

Value Chain Analysis

The Estonia e-commerce value chain begins with merchants and brands, including domestic omnichannel retailers and cross-border sellers using Estonia as an EU storefront base. The storefront and enablement layers cover checkout and fraud tooling, bank-link/open-banking payment flows, and BNPL providers. Because demand capture is increasingly mobile-first, conversion depends heavily on digital identity based authentication and fast bank-link settlement, while platform compliance tooling and customer-service automation sit alongside the storefront layer to support dispute-handling and disclosure obligations under TTJA oversight.

Order fulfillment and distribution center on warehousing, pick-pack operations, and last-mile networks built around parcel machines, where Omniva leads the parcel machine market (followed by Smartpost and DPD). The logistics layer increasingly mixes local fulfillment providers with digitally enabled freight forwarding for cross-border flows; for example, MyDello raised EUR 3.1 million in December 2025 to expand its digital freight forwarding platform, reflecting continued investment in integrating Estonian sellers into broader carrier networks. A persistent constraint remains warehousing capacity and peak management, which pushes merchants toward automation pilots, tighter inventory planning, and greater reliance on standardized digital freight data initiatives such as eFTI-related work to reduce cross-border paperwork.

Competitive Landscape

Market structure is moderately concentrated: the top five operators account for close to 45% of GMV, led by Selver, Barbora, Zalando, Amazon, and Pigu Group. Local chains lean on omnichannel synergies, integrating loyalty programmes across online and 73 physical stores. Regional fashion specialists exploit algorithmic sizing tools to keep return rates under 20%, protecting operating margins.

International entrants adopt asset-light playbooks, using third-party fulfilment centres in Tallinn’s free zone to minimise duty exposure. Their primary strategic lever is assortment depth, while local firms differentiate through 24-hour locker delivery and Estonian-language customer support. AI chatbots, such as those built on Klaus technology, cut ticket resolution times by 35%, sharpening service competitiveness. Sustainability emerges as a soft differentiator; players publicise carbon-neutral shipping lanes and recycled packaging pilots to court eco-conscious consumers.

Tech suppliers form a critical layer of the Estonia e-commerce market. Parcel-locker manufacturers, AI-based fraud-detection vendors, and compliance SaaS providers export know-how to neighbouring markets, reinforcing Estonia’s stature as a commerce tech laboratory.

Estonia E-commerce Industry Leaders

Barbora

DenimDream

Cellbes

Euronics Estonia

Selver AS

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Administrative automation is a practical whitespace for merchants handling high SKU velocity or operating across borders, supported by Estonia's Real-Time Economy agenda and the Ministry of Economic Affairs and Communications digital transformation frameworks (Digital Agenda 2030 under renewal and linked national roadmaps). The most tangible opportunity areas include automating invoicing, inventory data exchange, and reporting workflows to reduce manual handling across e-commerce operators and their logistics partners, especially for B2B transactions where API-based catalogs and structured procurement data already influence buying behavior.

Cross-border small-parcel flows also create a second opportunity cluster focused on compliance-first, cost-efficient import and returns management, particularly as a material share of international orders originates from Asia and tends to be low value. With EMTA implementing EU-wide low-value import changes from July 1, 2026 and Estonia relying on parcel-machine last-mile networks, operators that build tooling for customs and VAT handling, duty-inclusive pricing transparency, and returns routing can differentiate on total landed cost clarity and post-purchase experience. On the customer-facing side, the June 28, 2025 applicability of European Accessibility Act requirements for non-micro e-shops increases demand for accessibility audits and UI remediation services, creating service revenue potential for local commerce tech vendors and agencies that can standardize compliant checkout and content patterns across multiple storefronts.

Recent Industry Developments

- July 2026: The Estonian Tax and Customs Board (EMTA) implemented EU-wide low-value consignment changes from July 1, 2026, including a fixed customs duty for imports below EUR 150. This directly alters the landed-cost structure for non-EU small-parcel shipments, an important channel for low-ticket cross-border orders. Merchants and marketplaces face added pressure to improve duty and tax transparency at checkout and to tighten parcel data handoffs with logistics partners.

- October 2025: Cellbes migrated its IT infrastructure to Microsoft Azure, aiming to strengthen security, improve cost control, and support operations across multiple European markets. For Estonia-facing e-commerce operations, the migration supports faster scaling of digital storefront performance and standardized security controls across regions. It also raises the bar for smaller retailers competing on uptime, personalization, and secure payments.

- December 2024: Zalando moved to acquire ABOUT YOU, targeting consolidation in European fashion e-commerce and logistics synergies. The transaction strengthens platform leverage in assortment and fulfillment across Europe, which matters for Estonia because international fashion platforms are among the leading GMV players serving local shoppers. Local and regional fashion specialists face a tougher competitive set where delivery speed, returns handling, and pricing consistency become more platform-driven.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Estonia e-commerce market is defined as the value of online transactions for physical goods and digitally delivered services that are initiated, paid for, and fulfilled through online channels for shoppers in Estonia, including cross-border purchases booked to domestic buyers.

Scope exclusions: Lottery and gambling tickets are excluded from the market value.

Segmentation Overview

- By Business Model

- B2C

- B2B

- By Device Type

- Smartphone / Mobile

- Desktop and Laptop

- Other Device Types

- By Payment Method

- Credit / Debit Cards

- Digital Wallets

- BNPL

- Other Payment Method

- By B2C Product Category

- Beauty and Personal Care

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Furniture and Home

- Toys, DIY and Media

- Other Product Categories

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the factual boundaries of the market, then to anchor the model to real demand signals found in public data. We mainly relied on official and non-paywalled sources, including Statistics Estonia for retail and ICT indicators, Eurostat for household internet access and online purchasing rates, and Bank of Estonia or similar central bank publications for payment behavior and macro context.

To keep the market grounded in how commerce is executed, we also reviewed sources such as the US International Trade Administration country commercial guide, the Estonian E-commerce Association statistics pages, and national press that reports annual turnover and parcel trends. Company filings, investor presentations, and retailer disclosures were used to understand mix shifts, including higher share of marketplaces, omnichannel pickup behavior, and the role of cross-border orders. In addition, our analysts referenced paid subscriptions for company financials and news, and a patent database to track checkout, logistics, and fraud-related activity that can affect conversion and cost assumptions. The desk research sources listed above are illustrative, and many other public sources were also consulted for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what the desk sources could not fully explain, such as the online share of sales by category, typical order values, and how cross-border buying is counted in reported turnover. We spoke with executives and operating leaders across online retailers, marketplaces, payment and delivery ecosystem participants, and industry bodies, then used follow-ups to pressure test key assumptions before finalizing the market model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 15% | APAC: 46% |

| Mid tier: 47% | Functional/Unit leaders: 26% | EMEA: 36% |

| Smaller Players: 17% | Managers: 59% | Americas: 18% |

Market-Sizing & Forecasting

The core sizing logic uses a top-down build that starts from Estonia's online commerce turnover signals, then reconstructs a clean e-commerce value pool by applying scope rules and consistency checks. In practice, we mapped public turnover and retail indicators to online penetration, then calibrated the result using inputs that interviewees could confirm with day-to-day operating experience.

To keep the model realistic, we treated a few market fingerprints as key inputs, including the share of retail turnover conducted online, household online purchasing rates, cross-border purchase intensity, parcel volume growth and delivery mode shifts, and the average order value direction in major categories. Where a public data series was broad or reported in euros, we standardized it into USD using annual average exchange rates to avoid artificial spikes linked to one-time currency timing.

Forecasting used scenario analysis supported by a light multivariate regression check. The main drivers were private consumption, online shopper penetration, parcel volume growth, and the expected normalization of category-level growth after promotional peaks. Bottom-up approximations were also used as a reasonableness check. For example, we sampled typical basket sizes and purchase frequency by category, then rolled them up to the online buyer base. Where gaps remained, we used conservative ranges and later narrowed them with interview feedback.

Data Validation & Update Cycle

Before sign-off, our team triangulated the market total against independent signals such as reported national e-commerce turnover, retail trade benchmarks, and logistics activity indicators, then checked whether growth rates stayed consistent with macro demand. Outliers were flagged and reworked, and assumptions were revisited when a single metric drove an unusual jump, such as a sudden AOV shift or a one-year spike in cross-border purchases.

Each model version went through stepwise internal review, and respondents were re-contacted when gaps remained around inclusion rules, currency timing, or treatment of digital services. Reports are refreshed annually, with interim updates made when material events occur, including regulation changes affecting online payments or major fulfillment disruptions. Before delivery, analysts perform a final review pass so clients receive the latest updated view.

Mordor Intelligence's Estonia Ecommerce Market Size Compared With Other Published Estimates

Published e-commerce market values for Estonia can differ substantially, even for the same year, because underlying definitions are not always consistent. The biggest differences usually come from whether the estimate is measuring online retail revenue, a broader "e-commerce turnover" concept, or a GMV style measure that can include services and cross-border flows.

Payment turnover signals, association-reported e-commerce turnover, and parcel volume direction are the checks that keep Mordor Intelligence's estimate tied to online transactions that are initiated, paid for, and fulfilled through digital channels for shoppers in Estonia, with lottery and gambling tickets excluded. Once those boundaries are applied, remaining gaps to other figures usually relate to whether digitally delivered services are fully included, whether B2B online sales are counted, and how currency conversion timing is handled in a small euro-based economy.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.81 B (2025) | |

| Industry Association A | USD 6.34 B (2025) | Uses national e-commerce turnover reported in euros for goods and services and then converted, which can reflect a broader turnover concept than GMV scoped to online initiated, paid, and fulfilled transactions, and it may include wider payment-based activity depending on the indicator applied. |

| Government Trade Brief B | USD 5.77 B (2024) | Reports e-commerce revenue as a share of overall trade turnover in Estonia and does not clearly state inclusion rules for B2B online sales, cross-border flows, and digital services, which can inflate comparability versus a strictly scoped e-commerce transaction model. |

Overall, the table shows that the spread is mainly explained by scope boundaries and the definition of the value pool, not by small math differences. By tying the model to observable turnover and activity signals, then applying clear inclusions and exclusions, our estimate stays easier to audit and repeat year after year.

Key Questions Answered in the Report

What is the current value of the Estonia e-commerce market?

The Estonia e-commerce market is worth USD 887.84 million in 2026 and is projected to reach USD 1.41 billion by 2031.

Which segment is growing fastest within the Estonia e-commerce market?

B2B transactions show the highest momentum at an 11.63% CAGR, outpacing the overall market trajectory.

How significant is mobile commerce in Estonia?

Smartphones account for 63.60% of online purchases and are forecast to grow at a 12.08% CAGR through 2031, underscoring Estonia’s mobile-first profile.

What payment methods dominate online spending?

Credit and debit cards hold the largest share at 39.08%, but BNPL is the fastest-growing option, expanding at 14.59% CAGR.

How does Estonia’s e-Residency programme affect e-commerce?

E-Residency lowers administrative friction for foreign entrepreneurs, enabling over 15,000 companies to sell across the EU from an Estonian legal base, thereby intensifying market competition.

Which product category will drive future growth?

Food & beverages is forecast to grow at 14.21% CAGR, benefiting from expanded cold-chain locker networks and rapid delivery services.

Page last updated on: