Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

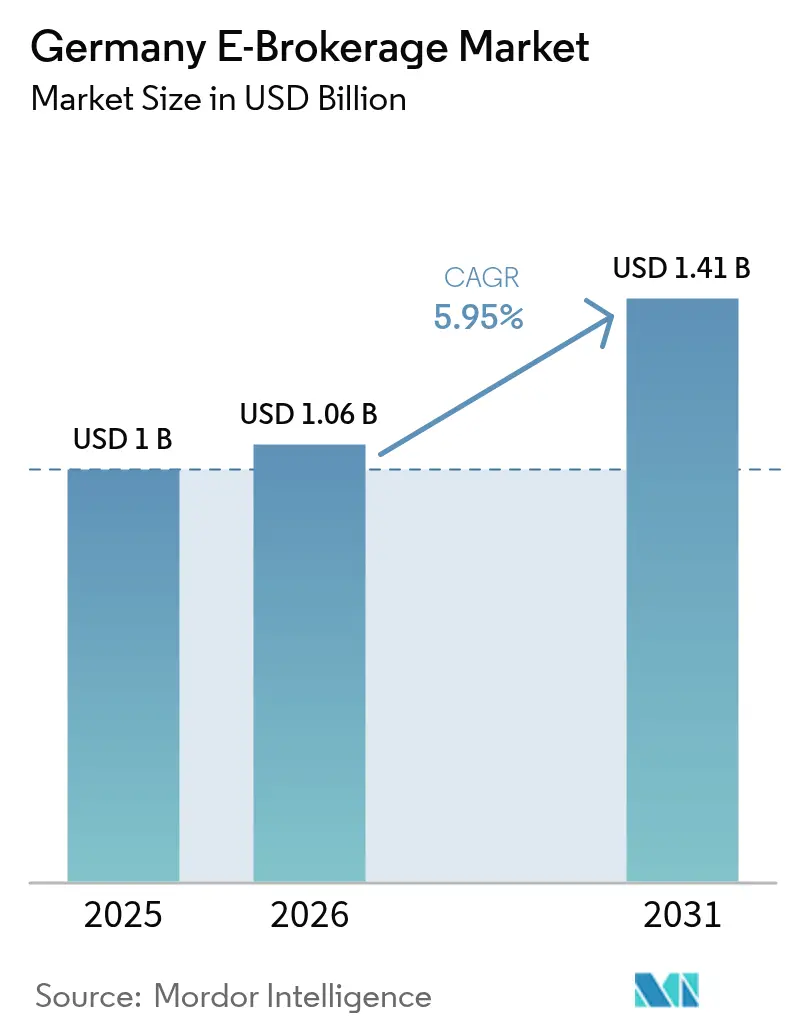

| Base Year Market Size (2025) | USD 1.00 Billion |

| Market Size (2026) | USD 1.06 Billion |

| Market Size (2031) | USD 1.41 Billion |

| Growth Rate (2026 - 2031) | 5.95% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany E-Brokerage Market Analysis by Mordor Intelligence

The Germany e-brokerage market size was valued at USD 1.00 billion in 2025 and estimated to grow from USD 1.06 billion in 2026 to reach USD 1.41 billion by 2031, at a CAGR of 5.95% during the forecast period (2026-2031). A surge of mobile-first platforms, an accelerating shift toward zero-commission trading, and supportive regulatory initiatives are driving sustained uptake among retail investors. Competitive intensity is rising as traditional banks digitalize their offerings while fintech entrants introduce fractional investing and high-yield cash accounts that attract deposits away from legacy institutions. The market’s resilience is being tested by the impending European Union ban on payment-for-order-flow (PFOF) revenue, yet leading brokers are diversifying into subscription models, proprietary trading venues, and embedded brokerage APIs to offset the lost income. Platform reliability, cybersecurity, and talent availability remain critical success factors as BaFin tightens oversight under the Digital Operational Resilience Act. Regional growth differentials persist, with West Germany contributing the largest volumes, while East Germany records the strongest momentum thanks to rapid digital adoption and lower traditional-bank penetration.

Key Report Takeaways

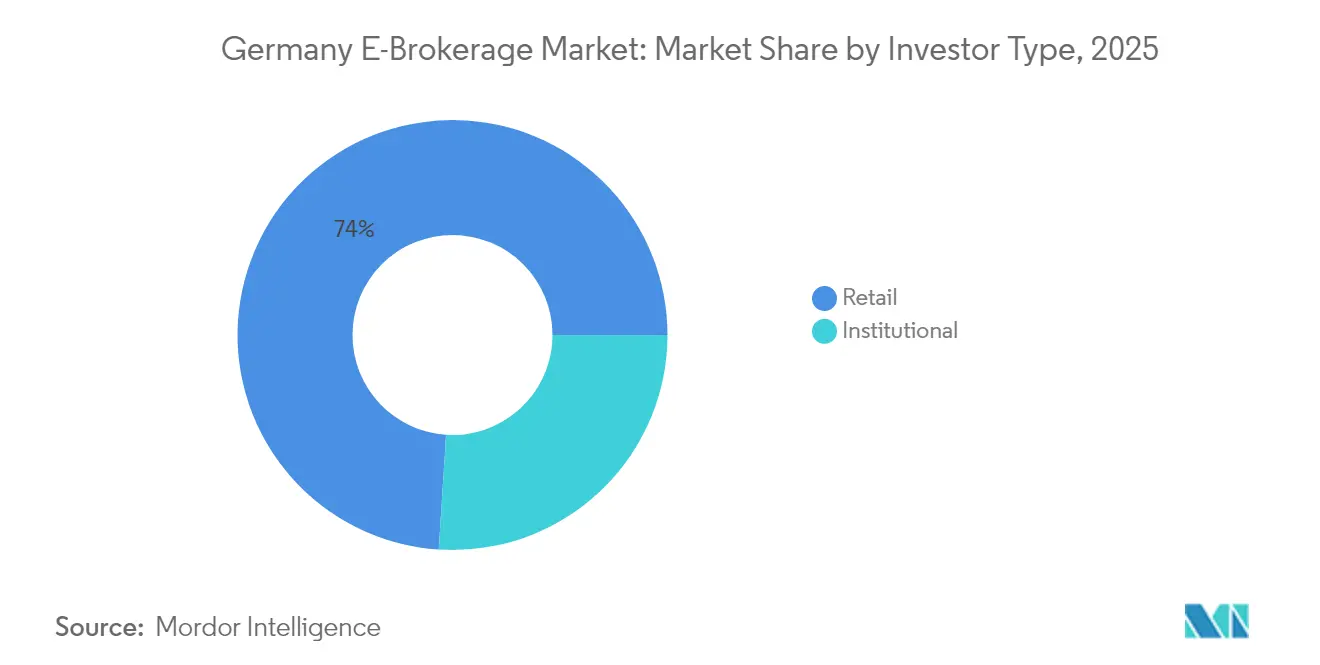

- By investor types, retail investors accounted for 73.98% of the German e-brokerage market share in 2025, while the German e-brokerage market size for retail investors under 35 years is projected to expand fastest at a CAGR of 16.05% between 2026 and 2031.

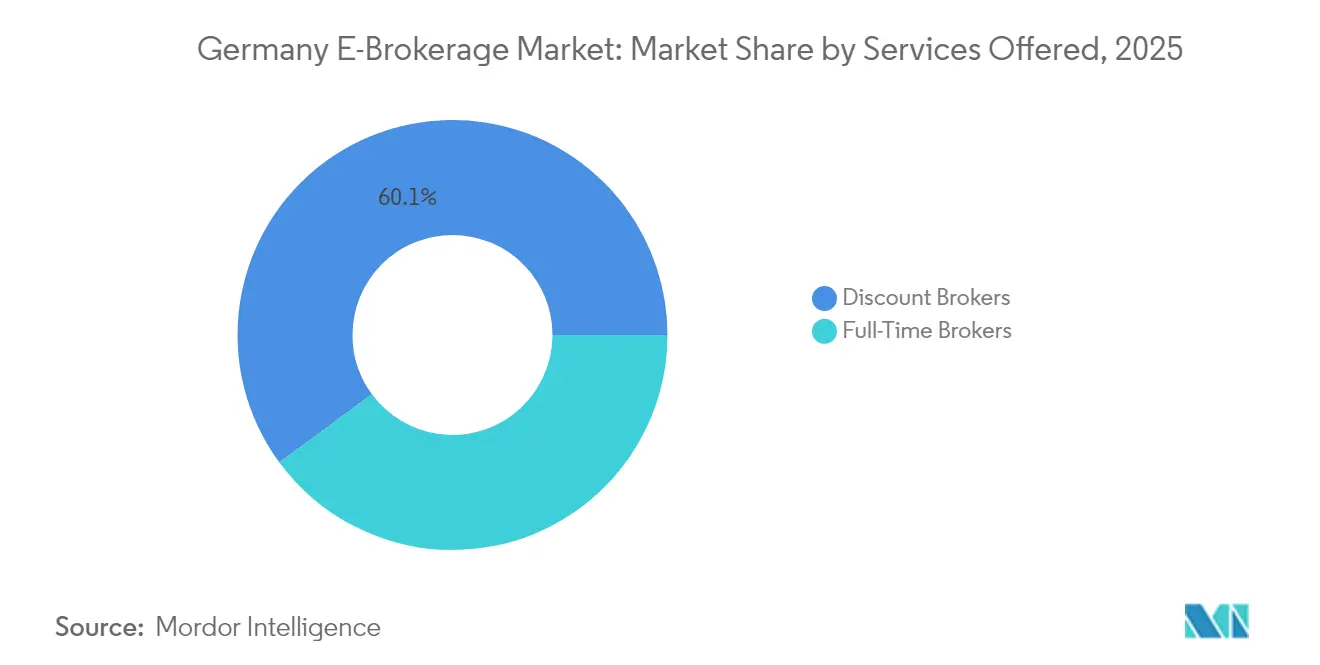

- By services offered, discount brokers captured 60.10% of the German e-brokerage market share in 2025, with the German e-brokerage market size for embedded-broker API (BaaS) offerings forecast to grow at the highest CAGR of 17.85% over 2026–2031.

- By operation, domestic players held 82.65% of the German e-brokerage market share in 2025, while the German e-brokerage market size for foreign-operated apps is anticipated to post a CAGR of 13.95% through 2031.

- By region, West Germany led with 28.05% of the German e-brokerage market share in 2025, with the German e-brokerage market size in East Germany expected to grow fastest at a CAGR of 6.20% during 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany E-Brokerage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in zero-commission models | +1.2% | National, urban hubs | Short term (≤ 2 years) |

| Generational shift to mobile-first apps | +0.9% | Berlin, Munich, Hamburg | Medium term (2-4 years) |

| BaFin proportionality initiative | +0.7% | Nationwide | Medium term (2-4 years) |

| Cash-interest offers above 2.25% | +0.8% | Competitive urban areas | Short term (≤ 2 years) |

| Fractional-share APIs enabling €1 trades | +0.6% | Tech-savvy demographics | Long term (≥ 4 years) |

| Pension reform equity pillar | +1.1% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Zero-Commission Models Attracting First-Time Investors

Zero-commission trading eliminated entry barriers and pulled millions of price-sensitive Germans into the capital markets. Brokers that relied on PFOF revenue must now replace lost income ahead of the 2026 ban, prompting moves such as Scalable Capital’s proprietary exchange launch that captures spreads directly. The transition introduces pricing uncertainty but also incentivizes innovation in subscription tiers and cash-management products. BaFin studies indicate that PFOF gave favourable execution for small orders, yet larger trades faced quality concerns. Platforms able to pivot quickly are positioned to capture share once commissions resurface, while late movers risk margin compression.

Generational Shift to Mobile-First Investing Apps

Younger users trade more frequently, diversify faster, and show a greater appetite for crypto and derivatives than older cohorts. BaFin has warned that behavioural nudges in app design can distort decision-making, pushing brokers to refine interfaces that prioritize investor protection[1]Bundesministerium der Finanzen, “Das Generationenkapital: für eine moderne Rente,” BMF.de . Traditional banks are facing ongoing challenges in addressing usability gaps, which continues to bolster the competitive advantage of digital-native players. In Germany, the aging population is expected to serve as a key driver of transformation within the e-brokerage market. Their shifting preferences are projected to influence platform design standards significantly, setting new industry benchmarks. This demographic trend is also likely to impact market strategies, compelling service providers to innovate and adapt to meet the evolving demands of this growing consumer segment.

BaFin's Proportionality Initiative Cutting Compliance Costs for Small Brokers

BaFin now tailors supervisory intensity to firm size, trimming reporting demands for roughly 950 small institutions, thereby lowering fixed compliance expenses. The relief lets startups channel resources into product innovation rather than regulatory overheads. The measure aligns with Basel Committee guidance on proportionality and encourages a vibrant field of specialized brokers[2]Basel Committee, “Proportionality in bank regulation and supervision,” bis.org . Leading market participants continue to comply with stringent prudential standards, creating a stratified framework that is likely to drive future consolidation trends. This strategic approach enhances competitive diversity within the market while fostering sustained growth and development in Germany's e-brokerage sector.

Pension Reform Introducing Equity-Fund Retirement Pillar

The Generationenkapital program earmarks EUR 200 billion for capital-market investments by the mid-2030s, supplementing Germany’s pay-as-you-go pension system[3]BaFin, “DORA: the countdown has begun,” bafin.de . Upvest, in collaboration with other stakeholders, promotes the adoption of a custody account model designed to allocate contributions directly into diversified investment portfolios. Brokerages that offer a wide range of ETFs, competitive fee structures, and comprehensive educational support are well-positioned to capitalize on this development. While the extended implementation timeline indicates that inflows will increase progressively, the reform establishes equity ownership as a foundational component of retirement planning. This initiative is expected to expand the addressable market for e-brokerages in Germany, creating new opportunities for growth and market penetration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU ban on payment-for-order-flow | -1.8% | EU-wide, Germany focus | Short term (≤ 2 years) |

| Cyber-incidents and platform outages | -0.6% | Nationwide | Medium term (2-4 years) |

| Rising retail risk-aversion | -0.4% | Nationwide | Short term (≤ 2 years) |

| Shortage of cloud and IT talent | -0.7% | Tech hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Ban on Payment-for-Order-Flow Shrinking Revenue Pools

From 2026, brokers in the German e-brokerage market will face the elimination of Payment for Order Flow (PFOF) as a revenue source, which has historically supported zero-commission trading models. This regulatory shift is prompting firms to explore alternative strategies to offset the financial impact. For instance, Scalable Capital has launched its own exchange, demonstrating a proactive approach to recapturing lost revenue streams. Such initiatives reflect a broader trend within the industry toward innovation and adaptation in response to regulatory changes. However, market makers have expressed concerns that integrated trading venues may replicate the conflicts of interest previously associated with PFOF, potentially attracting stricter regulatory oversight. This development highlights the growing urgency for brokers to diversify their revenue models to maintain competitiveness and ensure long-term financial stability in an increasingly regulated market environment.

Cyber-Incidents & Platform Outages Triggering Regulatory Scrutiny

Trade Republic’s April 2025 outage drew more than 7,000 complaints and spurred BaFin to stress platform-availability standards[4]The Munich Eye, “Trade Republic Experiences Service Disruptions Amid Market Decline,” themunicheye.com . From 2025 onward, the Digital Operational Resilience Act (DORA) is set to enforce stringent ICT control requirements, leading to a notable increase in compliance costs. This regulatory shift is likely to exert significant pressure on smaller brokerage firms, which may face difficulties in managing these additional financial and operational burdens. In 2023, BaFin reported that 7.12 million users were impacted by payment-service-related incidents, underscoring the sector's susceptibility to operational risks. The implementation of enhanced governance frameworks is expected to favor firms with robust technological infrastructure and strong capital reserves, positioning them to navigate the regulatory changes more effectively and maintain a competitive edge in the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Investor Type: Retail Dominance Drives Market Evolution

Retail investors held 73.98% of Germany's e-brokerage market size in 2025 as digital platforms removed cost and knowledge barriers. The segment is projected to rise at 16.05% CAGR through 2031, buoyed by fractional investing and intuitive mobile design that encourages first-time participation. Younger users conduct more trades and adopt a broader array of products, including crypto and derivatives, than institutional clients. Brokers meet their needs with gamified interfaces and real-time educational content, although regulators scrutinize possible behavioural manipulation. The institutional segment remains stable, leveraging e-brokerage for cost-efficient execution and accessing alternative asset classes outside traditional prime brokerage. MiFID II best-execution rules drive venue diversification, ensuring the continued relevance of electronic brokers.

The evolving dynamics of retail growth are driving a strategic shift in product development, with a heightened focus on integrating micro-investment functionalities and recurring ETF plans designed to accommodate smaller, consistent monthly contributions. Concurrently, institutional clients are demonstrating a growing demand for sophisticated capabilities, including advanced order-routing mechanisms, comprehensive analytics, and access to exclusive liquidity pools. These requirements are fostering the creation of premium service tiers tailored to meet the complex needs of institutional participants. Although institutional trading volumes are relatively lower, their flows contribute significantly to enhancing market depth and stabilizing bid-ask spreads, thereby improving overall market efficiency and quality. Additionally, regulatory frameworks aimed at safeguarding retail investors are exerting a considerable influence on platform design, particularly in areas such as disclosure practices and risk management protocols. These regulatory considerations are shaping architectural decisions that address the distinct requirements of both retail and institutional customer segments.

By Services Offered: Discount Models Reshape Industry Economics

Discount brokers captured 60.10% of the German e-brokerage market size in 2025 as investors gravitated toward low-fee, self-directed execution. Zero-commission pricing now faces sustainability pressures from the PFOF ban, prompting diversification through subscription bundles, interest income, and proprietary trading venues. Embedded broker APIs exhibit the fastest growth at 17.85% CAGR, enabling fintechs and non-financial brands to integrate turnkey trading modules without building infrastructure. Full-service brokers retain a niche among affluent clients who value advice and specialized strategies but must defend margins against digital challengers.

Lemon.markets represents a prominent example of the brokerage-as-a-service trend, providing BaFin-licensed trading infrastructure to partners that emphasize enhancing user experience and optimizing distribution channels. Discount brokerage platforms, such as Scalable Capital, address the challenge of margin compression by internalizing order flow through EIX, enabling them to retain spread income that was previously allocated to external trading venues. Meanwhile, full-service brokers are diversifying their offerings by incorporating value-added services such as tax optimization, estate planning, and alternative investment strategies to justify their fee structures and remain competitive. This increasing fragmentation of services within the German e-brokerage market is driving greater customer choice and fostering a higher degree of innovation across the industry.

By Operation: Domestic Focus Amid Cross-Border Growth

Domestic brokers controlled 82.65% of Germany's e-brokerage market share in 2025, reflecting investor trust in local supervision and tax handling. Foreign-operated apps, however, are expanding at 13.95% CAGR on the back of EU passporting and differentiated product offerings such as crypto and thematic portfolios. German clients appreciate native language support and clear tax statements, giving domestic incumbents an edge in ease of use. Yet platforms like Kraken extend reach via partnerships with BaFin-licensed custodians, narrowing the experiential gap.

Domestic brokerage firms capitalize on their established relationships with banks and their ability to integrate local payment systems, thereby optimizing the client onboarding process. On the other hand, foreign market entrants often differentiate themselves by excelling in specialized market segments or leveraging cost advantages derived from economies of scale across multiple markets. Regulatory requirements imposed by BaFin, including the necessity for a substantial local presence and adherence to stringent investor-protection standards, create significant compliance barriers. These regulations discourage opportunistic competitors while favoring operators with long-term commitments to the market. Consequently, the competitive landscape is transitioning toward a strategic equilibrium, characterized by robust domestic players maintaining market leadership and agile international challengers introducing competitive dynamics.

Geography Analysis

West Germany delivered 28.05% of 2025 revenues owing to the concentration of wealth around Frankfurt, Düsseldorf, and Munich. Established banks, fintech hubs, and deep talent pools underpin sophisticated demand for capital-market services. Nonetheless, platform saturation and intense rivalry cap growth rates, pushing brokers to seek incremental users elsewhere. East Germany’s 6.20% CAGR through 2031 underscores its potential as smartphone penetration and financial inclusion programs advance digital investing. Lower historical engagement with traditional banks means fewer switching frictions for app-based services.

North and South Germany present diverse opportunities shaped by maritime trade wealth and technology cluster affluence, respectively. Central Germany’s university centres generate tech-savvy cohorts that anchor steady adoption. BaFin’s uniform regulatory regime ensures consistent investor protections nationwide, enabling platforms to scale features efficiently across regions. As digital infrastructure gaps close, regional differences in adoption rates are expected to narrow, further integrating the Germany e-brokerage market.

Competitive Landscape

The top five brokers control a significant share of assets under custody, creating a concentrated yet dynamic field. Trade Republic commands more than 10 million users and USD 156.2 billion (EUR 150 billion) in assets, leveraging a full banking license to bundle payments, savings, and investments. FlatexDEGIRO follows with 2.96 million customers and USD 67.28 billion (EUR 64.6 billion) AuC through a dual-brand strategy targeting value-seekers and active traders. Scalable Capital leverages its proprietary exchange, EIX, as a strategic differentiator, positioning itself to adapt effectively to the evolving market landscape in the post-Payment for Order Flow (PFOF) era. This approach underscores the company's focus on innovation and its commitment to addressing regulatory and operational shifts within the financial services industry.

Emerging players such as lemon. Markets pursue brokerage-as-a-service opportunities, allowing non-financial brands to embed trading without direct licensing burdens. Traditional banks like Deutsche Bank’s MaxBlue and DKB revamp interfaces and lower fees to protect their share, but legacy systems hamper agility. The EU PFOF ban is the principal catalyst of strategic change, redistributing economics toward brokers able to internalize execution or monetize cash and subscription services. Operational resilience rose to the forefront after Trade Republic’s outage drew BaFin scrutiny, turning IT robustness into a crucial differentiator. Talent shortages and rising compliance costs further favour well-capitalized incumbents, yet proportionality rules preserve room for niche specialists that address underserved segments.

Germany E-Brokerage Industry Leaders

Trade Republic GmbH

flatexDEGIRO AG

Scalable Capital Broker GmbH

finanzen.net ZERO (Gratisbroker AG)

Smartbroker Plus (wallstreet:online)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Scalable Capital extended its high-yield cash strategy outside Germany by offering new Austrian customers 3% interest on broker cash balances, reinforcing deposit-based revenue diversification.

- June 2025: Scalable Capital raised USD 161.4 million (EUR 155 million) in its largest funding round to date, earmarking the proceeds for European platform expansion, kids’ accounts, and private-equity ELTIF access.

- May 2024: Kraken partnered with BaFin-licensed DLT Finance to roll out German cryptocurrency brokerage services, expanding localized compliance infrastructure.

- March 2024: Lemon. Markets obtained investment-firm licensing from BaFin and launched its brokerage-as-a-service platform in collaboration with BNP Paribas and Deutsche Bank.

Germany E-Brokerage Market Report Scope

E-brokerage allows users to buy and sell stocks electronically and obtain information with the help of a website. The report on the German E-Brokerage market provides a comprehensive evaluation of the market with market segmentation, product categories, existing market trends, market dynamics shifts, and growth opportunities. E-Brokerage Market in Germany is segmented by Investor Type (Retail and Institutional) and by Broker Ownership Type (Local and Foreign). The report offers the market sizes and forecasts in value (USD) for all the above segments.

By Investor Type

| Retail |

| Institutional |

By Services Offered

| Full-Time Brokers |

| Discount Brokers |

By Operation

| Domestic |

| Foreign |

By Region

| North Germany |

| South Germany |

| East Germany |

| West Germany |

| Central Germany |

| By Investor Type | Retail |

| Institutional | |

| By Services Offered | Full-Time Brokers |

| Discount Brokers | |

| By Operation | Domestic |

| Foreign | |

| By Region | North Germany |

| South Germany | |

| East Germany | |

| West Germany | |

| Central Germany |

Key Questions Answered in the Report

How large is the German e-brokerage market today?

The German e-brokerage market size stands at USD 1.06 billion in 2026 and is forecast to reach USD 1.41 billion by 2031.

What CAGR is expected for German e-brokerage platforms through 2031?

Overall sector revenues are projected to rise at a 5.95% CAGR between 2026 and 2031.

Which customer group drives the most transaction volume on German trading apps?

Retail investors account for 73.98% of market activity and are expanding fastest due to mobile-first platforms and fractional investing.

How will the EU PFOF ban affect German brokers?

From 2026, brokers must replace PFOF income, prompting moves toward subscription pricing, proprietary venues, and higher interest on cash balances.

Which region in Germany is growing the fastest for e-brokerage adoption?

East Germany shows the highest momentum with a 6.20% CAGR to 2031 as digital infrastructure and smartphone use rise.

Who are the leading players in German e-brokerage?

Trade Republic, flatexDEGIRO, and Scalable Capital dominate, collectively controlling a significant share of assets under custody.

Page last updated on: