Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

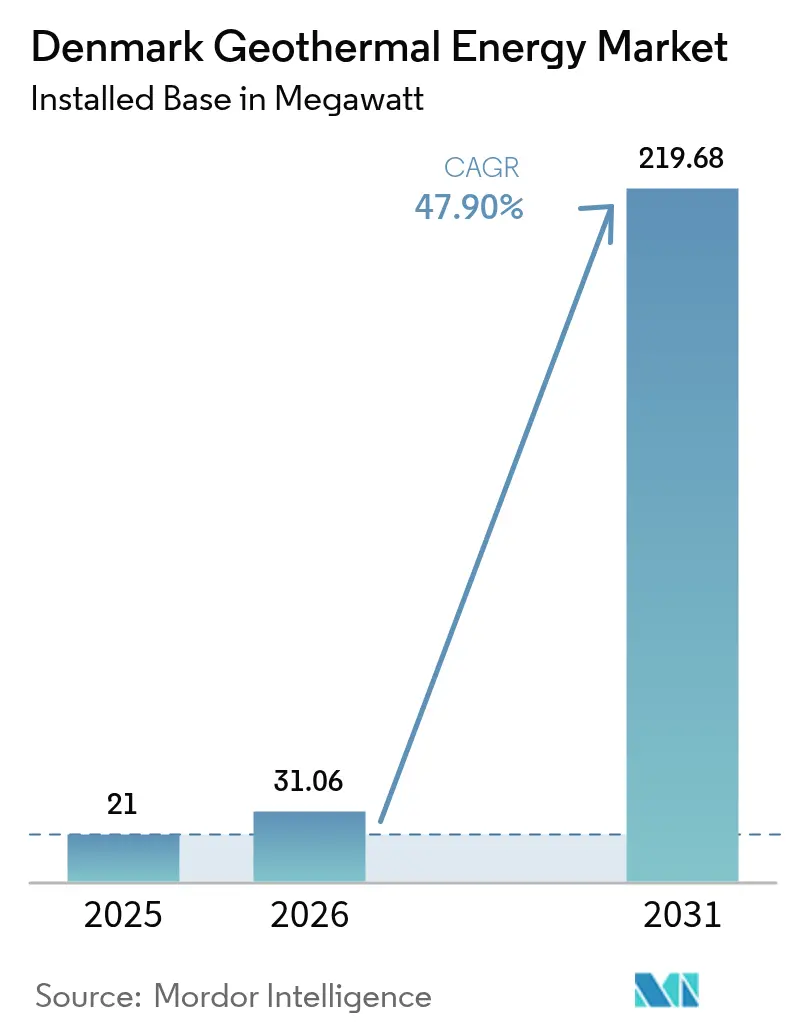

| Base Year Market Size (2025) | 21 megawatt |

| Market Volume (2026) | 31.06 megawatt |

| Market Volume (2031) | 219.68 megawatt |

| Growth Rate (2026 - 2031) | 47.90% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Denmark Geothermal Energy Market Analysis by Mordor Intelligence

Denmark Geothermal Energy Market size in 2026 is estimated at 31.06 megawatt, growing from 2025 value of 21 megawatt with 2031 projections showing 219.68 megawatt, growing at 47.90% CAGR over 2026-2031.

Recent policy mandates, including the phase-out of new natural-gas boilers from 2028 and a legally binding requirement for carbon-neutral district-heating utilities by 2030, give the Denmark geothermal energy market a predictable growth runway. Municipal heat-planning obligations under the Heat Supply Act convert latent demand into bankable offtake agreements, while EU Innovation Fund grants cushion early exploration risk for binary-cycle and enhanced-geothermal projects. Abundant 45-70 °C aquifers beneath Zealand align naturally with Denmark’s low-temperature district-heating grids, allowing binary-cycle developers to avoid costly advanced drilling or high-temperature technologies. As industrial heat-pump costs fall below EUR 500/kW, hybrid geothermal-heat-pump plants unlock additional value streams and reduce lifecycle heat costs for utilities facing tight decarbonization timelines.

Key Report Takeaways

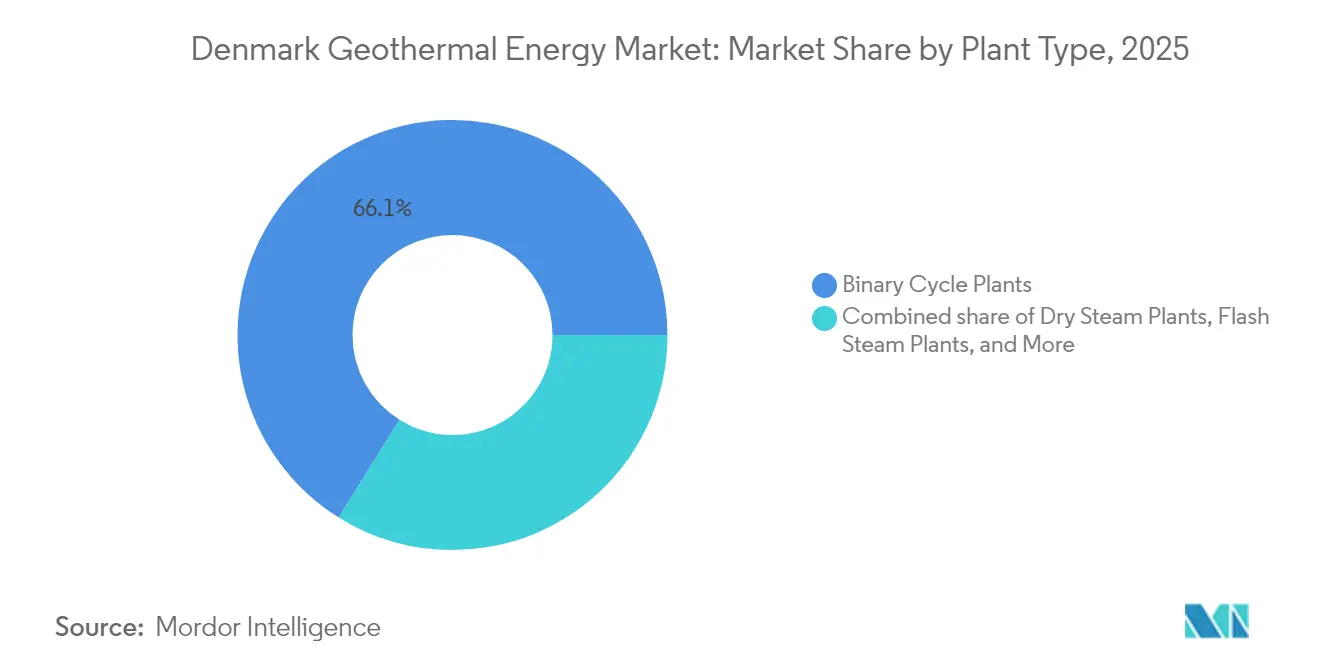

- By plant type, binary-cycle systems held 66.12% of the Denmark geothermal energy market share in 2025, while enhanced geothermal systems (EGS) recorded the fastest CAGR at 50.62% through 2031.

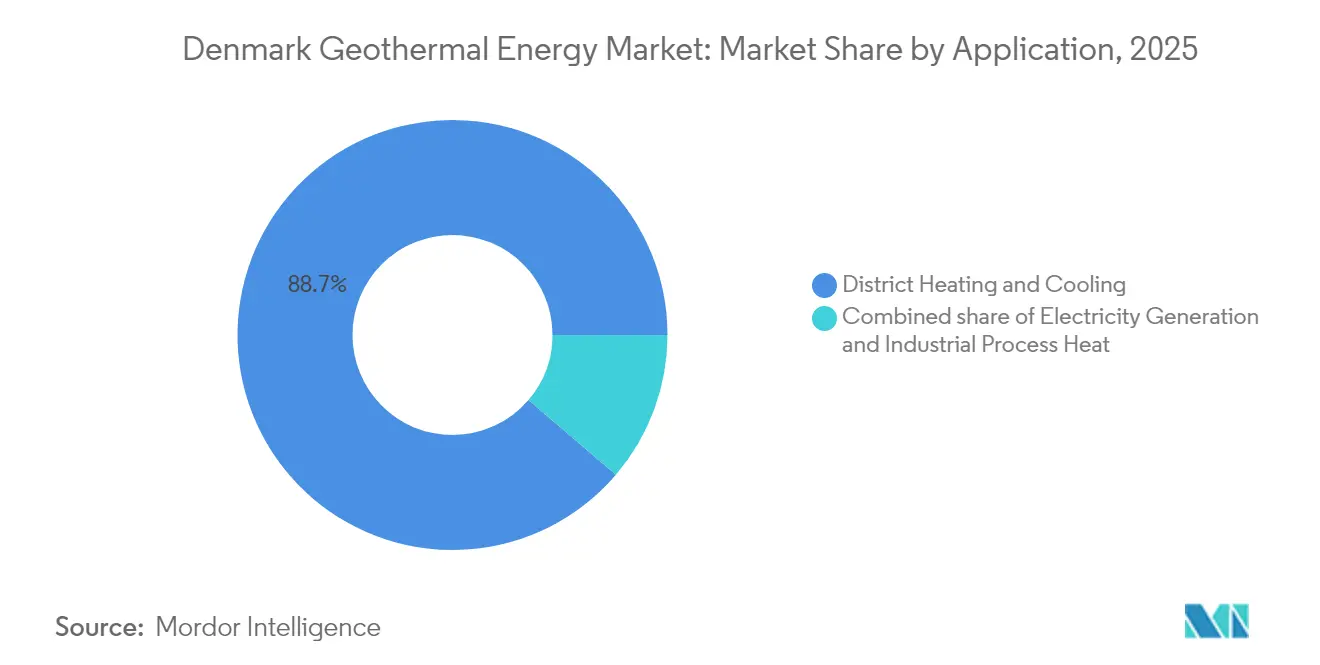

- By application, district-heating networks accounted for an 88.74% share of the Denmark geothermal energy market size in 2025 and are projected to grow at a 48.28% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Denmark Geothermal Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid decarbonization targets for district-heating utilities | 12.50% | Zealand & key Jutland municipalities | Medium term (2-4 years) |

| Phase-out of new natural-gas boilers from 2028 | 10.80% | National urban zones | Short term (≤ 2 years) |

| Abundant low-temperature sedimentary basins under Zealand | 8.20% | Zealand, Funen, southern Jutland | Long term (≥ 4 years) |

| Industrial-scale heat-pump cost declines (< EUR 500/kW) | 7.10% | Nationwide | Medium term (2-4 years) |

| EU Innovation Fund grants for geothermal clusters | 5.40% | National | Short term (≤ 2 years) |

| Data-center waste-heat offtake agreements | 4.90% | Copenhagen & Aarhus metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Decarbonization Targets for District-Heating Utilities

More than 400 municipal utilities must eliminate fossil-fuel backup systems by 2030, transforming geothermal from an optional resource to an operational necessity. Mandatory heat-planning filings reveal multi-year demand schedules, enabling developers to underwrite projects with 20-year heat-purchase contracts that cut offtake risk. Early movers such as HOFOR deploy advanced supervisory control systems to blend low-temperature geothermal heat with biomass and waste-to-energy feedstocks, lowering delivered heat costs under tightening CO₂ caps.[1]Geological Survey of Denmark and Greenland, “Sedimentary Basin Resource Assessment,” geus.dk The regulatory timetable, therefore, creates a flywheel: confirmed demand de-risks finance, financed projects prove technical success, and proven success accelerates further demand. Utilities adopting geothermal sooner lock in a secure heat supply and avoid later peak-demand surcharges on limited drilling rigs and service crews.

Phase-Out of New Natural-Gas Boilers from 2028

Denmark’s BR18 building code closed the door on fossil-fuel boilers in new construction inside district-heating zones, and the 2028 national ban eliminates gas as a fall-back option even in legacy buildings.[2]Danfoss, “Low-Temperature District-Heating Control Solutions,” danfoss.com State grants from Fjernvarmepuljen reimburse up to DKK 20,000 per converted boiler, channeling households toward network hookups and pushing utilities to secure renewable baseload capacity. Because binary-cycle plants require 3-5 years from seismic study to commissioning, the 2028 milestone perfectly matches developer timelines and is already visible in municipal tender schedules. Cutting gas out of the supply stack also raises the capacity factor requirements for heat pumps that depend on low-cost power, thus improving the load-factor economics of steady geothermal output. The boiler ban, therefore, removes lower-capex fossil competition and hardwires geothermal into future network expansion blueprints.

Abundant Low-Temperature Sedimentary Basins Under Zealand

Continuous sedimentary layers such as the Gassum Formation at 1,000-2,500 m depth deliver 45-70 °C fluids that fit directly into district-heating flow-temperatures of 70-90 °C.[3]Danish Ministry of Climate, “BR18 Building Regulations,” byggetilsynet.dk The predictable stratigraphy shortens exploration campaigns and raises drilling success rates, trimming one-third off typical dry-hole contingency budgets compared with crystalline basement targets. Recent 3-D seismic surveys extend positive thermal anomalies northwest toward Jutland, expanding the economically drillable footprint beyond Copenhagen. This resource match allows binary-cycle developers to bypass costly organic Rankine cycles designed for higher temperatures and instead deploy standardized plant modules, driving down installed cost per MW. With aquifer recharge managed via closed-loop injection, reservoir sustainability models indicate several hundred MW of recoverable heat by 2050, ensuring long-term supply security for the Denmark geothermal energy market.

Industrial-Scale Heat-Pump Cost Declines

OEM price quotes for 5-50 MW heat pump skids have fallen below EUR 500/kW, slashing capex for hybrid plants that pair geothermal fluid circuits with heat-pump evaporators. MAN Energy Solutions’ 70 MW CO₂-based seawater pump in Esbjerg supplies 25,000 households at a lower lifecycle cost than biomass once CO₂ pricing is included. When integrated with geothermal, heat pumps lift 50 °C brine to 80-90 °C supply temperature at coefficient-of-performance ratios above 3.5, trimming the electric input share of delivered heat. Danish manufacturers now bundle substation heat exchangers and smart-grid controllers, shifting geothermal flow rates in tandem with power-price signals. Falling hardware cost therefore broadens the viability envelope of geothermal projects, especially in municipalities with moderate resource temperatures that previously fell below economic thresholds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uncertain subsurface temperature gradients outside Zealand | -6.30% | Jutland & Funen | Long term (≥ 4 years) |

| Competition from surplus wind power-to-heat | -5.70% | Nationwide | Medium term (2-4 years) |

| Municipal balance-sheet caps delaying FID on > 150 MW projects | -4.20% | Mid-sized municipalities | Short term (≤ 2 years) |

| Public perception of induced seismicity after 2021 Viborg event | -2.90% | Viborg, spill-over to Zealand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Uncertain Subsurface Temperature Gradients Outside Zealand

Exploration wells in Jutland show variable gradients that swing from 20 °C/km to under 15 °C/km within short lateral distances, forcing developers to budget up to 50% more for seismic, coring, and step-out drilling before locking down full field development. Lenders price this geological uncertainty into higher interest-rate spreads, particularly for municipalities whose heat tariffs are capped by consumer-protection rules. Smaller utilities lacking diversified revenue bases are wary of dry-hole risk that could strand millions in sunk exploration cost, shrinking the pool of feasible offtakers. While EGS pilots promise to widen the resource base, their learning curve and distinct permitting paths mean commercial deployment remains several years away. Until exploration data density improves, the Denmark geothermal energy market will continue to cluster around Zealand’s proven aquifers.

Competition from Surplus Wind Power-to-Heat

Denmark generated record wind output in 2024, driving wholesale electricity prices near zero during storm peaks and turning immersion heaters into the cheapest short-run heat source for district networks.[4]Energinet, “Hourly Electricity Price Data 2024,” energinet.dkUtilities in west-coast regions exploit negative-price hours by bypassing boilers and heating water directly with resistive elements. This undercuts geothermal’s baseload value proposition during windy intervals, eroding cash flow in merchant-price-linked heat contracts. Yet during low-wind periods, the same networks flip to high marginal power prices, and utilities then pay premium tariffs unless they hold geothermal capacity. The resulting arbitrage squeezes financing for geothermal unless contracts incorporate capacity payments or ancillary-service revenues that compensate for wind-driven volatility. The wind-to-heat option, therefore, caps geothermal penetration rates in regions with high onshore wind build-out, at least until market structures reward round-the-clock renewable heat.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Plant Type: Binary Cycles Capture Low-Enthalpy Advantage

Binary-cycle facilities represented 66.12% of installed capacity in 2025, and their share of the Denmark geothermal energy market size is forecast to stay above 70% through 2031 as 110 MW of additional binary projects reach completion. The segment’s 47.35% CAGR reflects both subsurface temperature suitability and the ability to add ORC turbines without incurring seismic risks that accompany flash-steam designs. Innargi’s Skejby phase, commissioned in October 2025, showcases 55 °C brine lifted to 85 °C via ammonia heat pumps, achieving 75–80% system efficiency.

Enhanced geothermal systems remain in the pilot stage, led by Aalborg’s 2 MW Heat4Ever coaxial wellbores. Flash-steam and dry-steam technologies are absent, since Denmark lacks ≥150 °C reservoirs. Continued heat-pump cost reductions toward EUR 300–400 per kW by 2027 should further widen the cost gap in favor of binary construction, positioning the segment to approach 198.6 MW by 2031 if Copenhagen’s 26 MW Bunter Sandstone project hits performance milestones.

By Application: District Heating Dominates Demand Profile

District heating accounted for 88.74% of 2025 output and will retain the lion’s share as municipalities chase 2035 fossil-fuel bans. This application commands the highest Denmark geothermal energy market share and a forecast 48.28% CAGR, supported by 65% nationwide district-heating penetration and 98% household coverage in Copenhagen. Baseload capability with more than 8,000 full-load hours makes geothermal heat the natural successor to coal and gas in existing networks.

Electricity generation remains marginal because 50–65 °C fluids yield only single-digit turbine efficiencies. Industrial process heat is an emerging niche, demonstrated by a logistics hub in northern Denmark using groundwater with COP 4+ heat pumps. Wider industrial uptake depends on network extensions into manufacturing zones, a prospect encouraged by the 2024 Heat Planning Act.

Geography Analysis

Zealand concentrates about two-thirds of installed capacity and virtually all near-term drilling commitments, owing to well-mapped aquifers that overlay Copenhagen’s 1.3 million-resident district-heat demand hub. Innargi’s 26 MW Lyngby plant and Vestforbrænding’s planned cluster supply illustrate the economies of scale achievable when resource, population, and network converge within a 30 km radius. Capital recovery accelerates because high load factors flatten tariff curves, allowing user bills to fall even after factoring in exploration amortization.

Jutland is poised for the steepest growth curve as municipal utilities in Aarhus, Aalborg, and Viborg exhaust biomass co-firing credits and face escalating EU carbon prices. Green Therma’s Aalborg pilot leverages DKK 84 million EUDP support to de-risk step-out wells, and Aarhus city utility Kredsløb has contracted Innargi to drill seven sites that could cover 20% of city heating by 2030. Geological heterogeneity adds cost, yet subsidies under the Danish Energy Agency’s geothermal exploration window offset up to 39% of seismic expenses, narrowing the capex delta versus Zealand.

Island systems such as Bornholm and Lolland eye geothermal to cut reliance on tanker-delivered fuel oil and to stabilize grids exposed to wind lulls. The Climate Agreement earmarks extra funding for stand-alone energy islands, enabling pre-feasibility studies on 5-10 MW binary plants integrated with battery-backed microgrids. Though small in absolute megawatts, island projects unlock premium heat tariffs and showcase export-ready modular technology for other Nordic archipelagos. Collectively, these geographic dynamics position Zealand as the bedrock of early-stage scale while framing Jutland and the islands as diversification levers that will mature mid-decade.

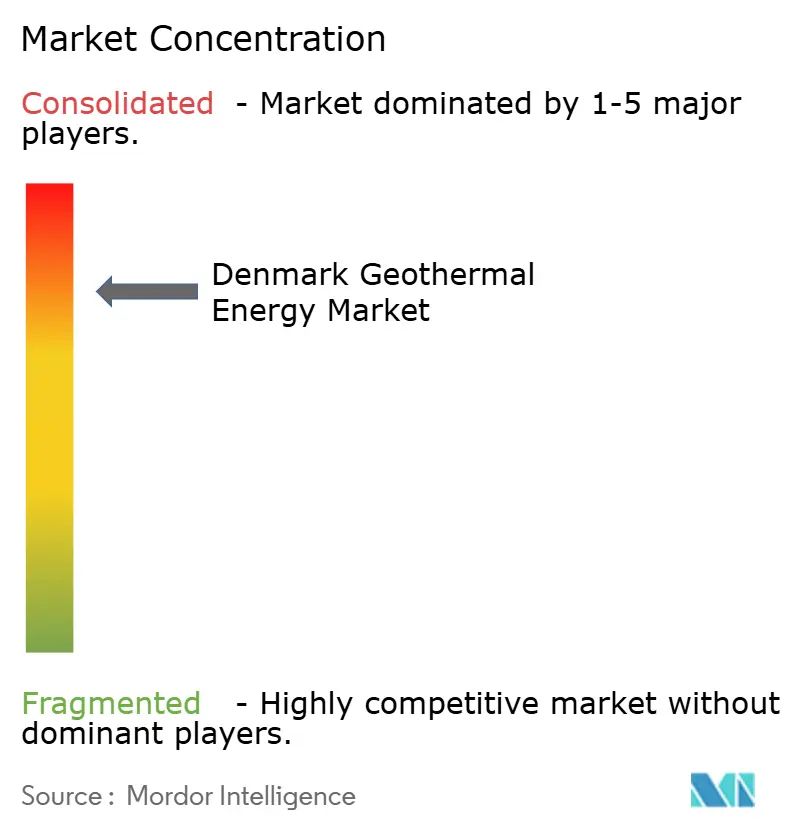

Competitive Landscape

Competitiveness in the Denmark geothermal energy market hinges on land position, municipal alliances, and financing agility rather than core technology, because binary-cycle systems are commercially standardized. Innargi A/S leads capacity pipelines with projects in Greater Copenhagen and Aarhus totaling 150 MW under construction or advanced planning, giving the firm a first-mover edge that could translate into 30-40% national capacity by 2030. Its funding model blends pension equity from ATP, EIB-backed green loans, and 20-year fixed-price offtake deals, lowering the weighted average cost of capital relative to municipally financed competitors.

Green Therma positions itself as a technology-agnostic integrator that bundles drilling, heat pumps, and data-center waste-heat loops. The firm capitalizes on municipal balance-sheet caps that limit on-book borrowing above DKK 1 billion, offering off-balance-sheet project vehicles that de-risk utility exposure. Equipment vendors such as Danfoss and MAN Energy Solutions capture value via turnkey EPC contracts and long-term service agreements, with Danfoss also monetizing control-software upgrades that optimize geothermal flow and electricity dispatch.

Competitive intensity remains moderate because only a handful of developers hold drilling licenses in prime Zealand acreage, yet barriers to entry are falling as the Danish Geological Survey releases new 3-D seismic data sets. Foreign entrants eye joint ventures, attracted by transparent permitting and predictable feed-in tariffs for heat. As capacity scales, supply-chain bottlenecks move from drilling rigs to high-capacity downhole pumps, prompting vertical-integration plays by equipment suppliers. Overall, collaboration between municipalities, pension funds, and technology vendors underpins a partnership-driven competitive landscape.

Denmark Geothermal Energy Industry Leaders

-

Innargi A/S

-

Danfoss A/S

-

Ramboll Group A/S

-

Welltec A/S

-

NIRAS A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Innargi A/S and H. Anger’s Söhne signed a three-year framework agreement for drilling services for around 20 deep geothermal wells in Denmark and Germany. The work will use Anger’s “City Rig 500,” a quiet, urban-focused rig developed with Herrenknecht Vertical.

- March 2025: Hillerød Forsyning and Innargi signed an agreement to explore geothermal district heating in Hillerød, aiming to phase out natural gas, reduce biomass use, and provide green, affordable heating as the network grows.

- November 2024: Vestforbrænding and Innargi agreed to develop geothermal energy for district heating, marking Denmark’s largest district heating project with 39,000 households switching from oil and gas. This initiative also introduces geothermal heating to the Greater Copenhagen area for the first time.

- October 2024: North Jutland-based renewable energy specialist Aalborg CSP has partnered with Innargi to deliver an integrated 18 MW heat pump station for a major geothermal project in Aarhus, Denmark. The station features a 10 MW electric heat pump that extracts energy from underground geothermal water and supplies it to Kredsløb’s district heating network in northern Aarhus.

Denmark Geothermal Energy Market Report Scope

In geothermal energy, heat is produced deep within the Earth's core. Geothermal energy is an unpolluted, renewable resource that can be used as a heat source and for electricity. The Geothermal Energy Market sizing and forecasts have been done based on installed capacity (MW). The Denmark geothermal energy market report includes:

By Plant Type

| Dry Steam Plants |

| Flash Steam Plants |

| Binary Cycle Plants |

| Combined Cycle/Hybrid Plants |

| Enhanced Geothermal Systems (EGS) |

By Application

| Electricity Generation |

| District Heating and Cooling |

| Industrial Process Heat |

| By Plant Type | Dry Steam Plants |

| Flash Steam Plants | |

| Binary Cycle Plants | |

| Combined Cycle/Hybrid Plants | |

| Enhanced Geothermal Systems (EGS) | |

| By Application | Electricity Generation |

| District Heating and Cooling | |

| Industrial Process Heat |

Key Questions Answered in the Report

How large is the Denmark geothermal energy market in 2026?

Installed capacity is 31.06 MW, and it is forecast to reach 219.68 MW by 2031.

Which plant type is growing fastest in Denmark?

Enhanced geothermal systems (EGS) are expanding at a forecast 50.62% CAGR through 2031.

What share of Danish geothermal output goes to district heating?

About 88.74% in 2025, with sustained growth as fossil fuels exit district networks.

Why is electricity generation a minor use of Danish geothermal resources?

Reservoir temperatures of 50–65 °C limit turbine efficiency, making direct heat more economical.

Who are the leading project developers?

Innargi A/S and Hovedstadens Geotermi P/S together control nearly three-quarters of the project pipeline.

How does wind surplus affect geothermal economics?

Low-price wind electricity favors immersion heaters during high-wind hours, trimming geothermal utilization to roughly 70–80%.

Page last updated on: