Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

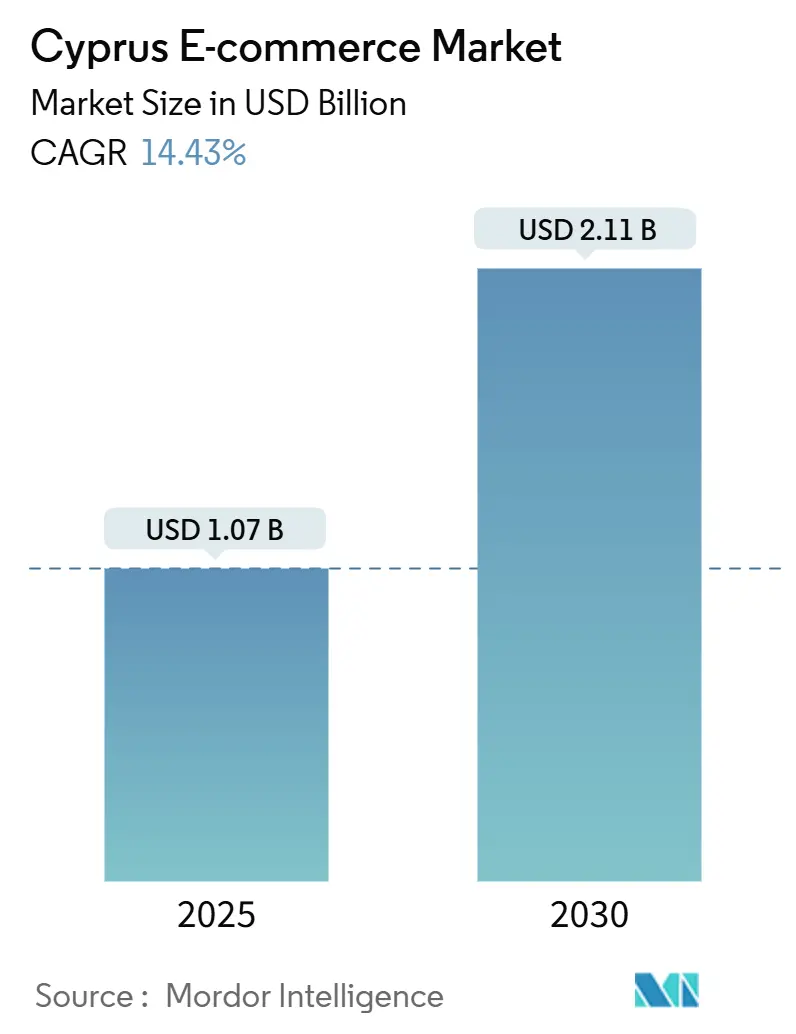

| Market Size (2025) | USD 1.07 Billion |

| Market Size (2030) | USD 2.11 Billion |

| Growth Rate (2025 - 2030) | 14.43% CAGR |

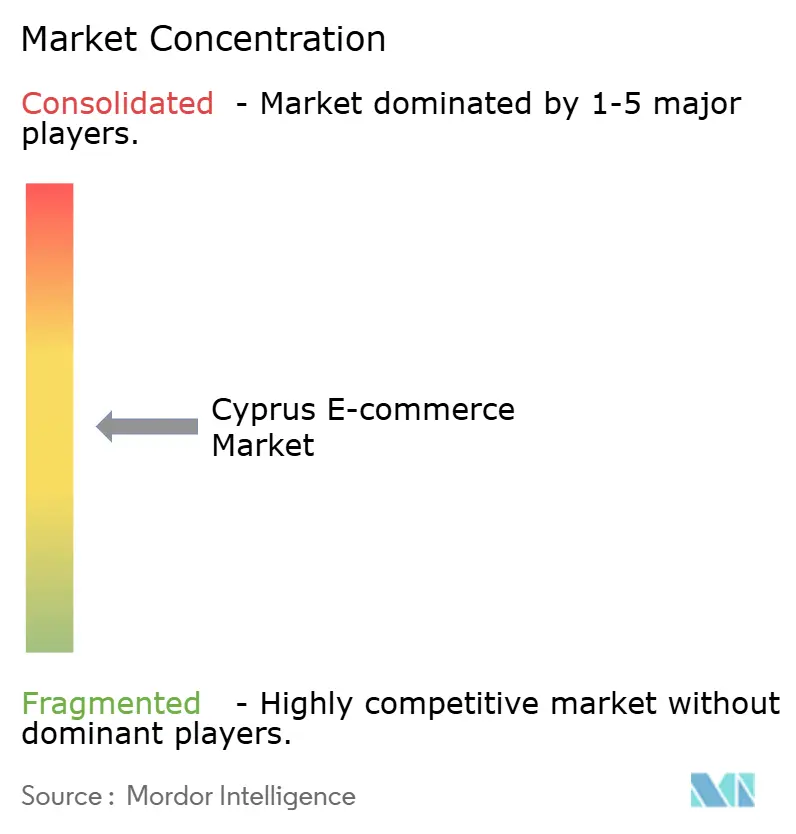

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cyprus E-commerce Market Analysis by Mordor Intelligence

The Cyprus e-commerce market reached USD 1.07 billion in 2025 and is forecast to post a 14.43% CAGR, doubling to USD 2.11 billion by 2030. This growth trajectory underlines how fast digital retail is scaling on the island. Robust 92% internet penetration, an 81% cross-border shopping culture, and smartphone-driven browsing that now makes up more than 65% of web traffic provide the structural backdrop. A payment ecosystem where digital methods cover 96% of cashless transactions, together with instant-payment rails launched in January 2025, removes critical friction at checkout. Intensifying competition is sharpening service quality; global marketplaces set delivery-time benchmarks that local merchants match through parcel-locker networks, last-mile partnerships and same-day urban dispatch. These operational gains, when combined with EU policy harmonisation and EUR 177.25 million (USD 195.0 million) in government digital-innovation funding, keep the Cyprus e-commerce market on a clear expansion path.

Key Report Takeaways

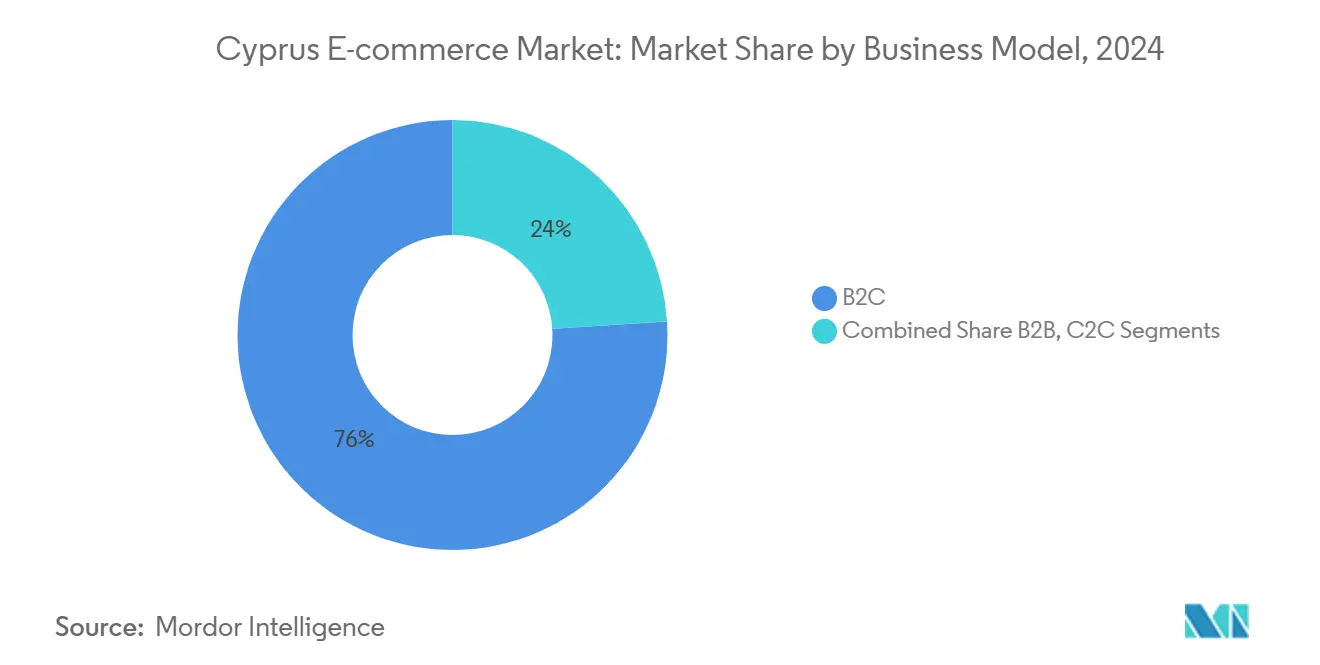

- By business model, B2C led with 76% Cyprus e-commerce market share in 2024; C2C is projected to expand at an 18.9% CAGR to 2030.

- By device, smartphones captured 69% of transactions in 2024, while mobile commerce is forecast to advance at a 17.5% CAGR through 2030.

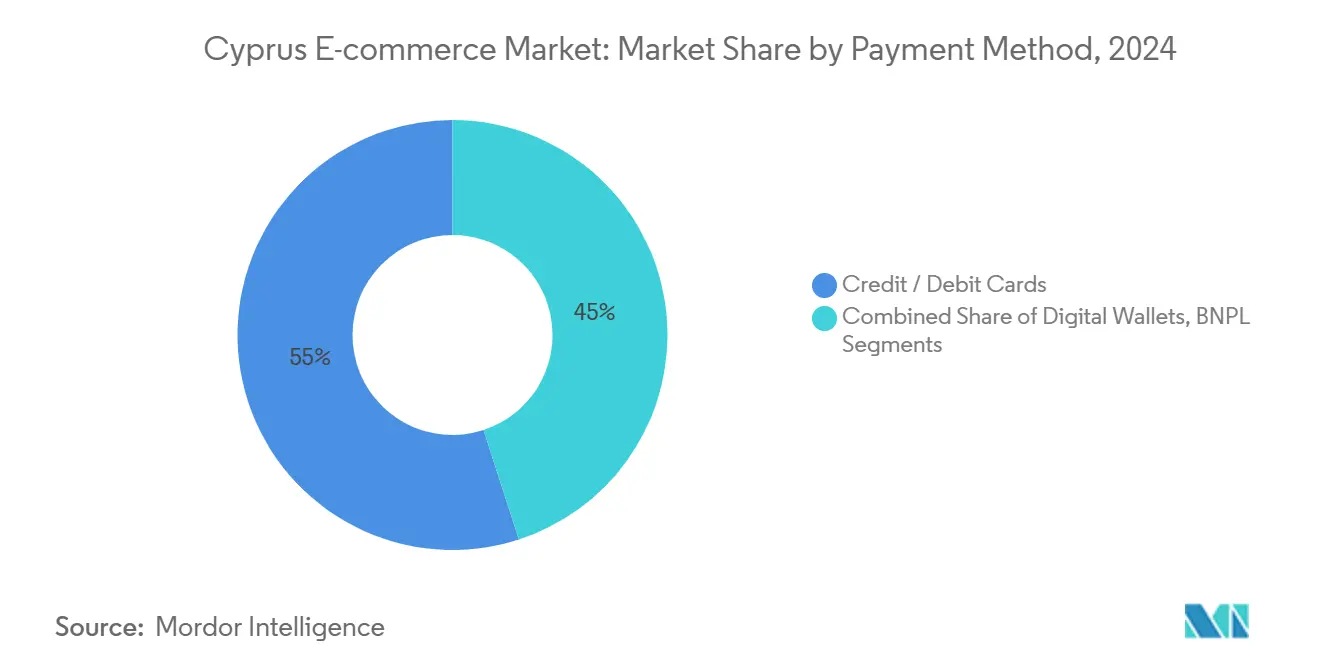

- By payment method, credit and debit cards accounted for 55% of transactions in 2024; digital wallets are projected to grow at an 18.1% CAGR to 2030.

- By product category, fashion and apparel held 32% revenue share in 2024; food and beverages is expanding at a 19.2% CAGR through 2030.

Cyprus E-commerce Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising mobile and internet penetration | +3.2% | National, with higher impact in urban centers | Short term (≤ 2 years) |

| Growing online demand for fashion and apparel | +2.8% | National, with concentration in Nicosia and Limassol | Medium term (2-4 years) |

| Improved last-mile logistics and parcel lockers | +2.1% | Urban centers, with gradual expansion to rural areas | Medium term (2-4 years) |

| EU e-Commerce VAT package harmonisation | +1.9% | National, with stronger impact on cross-border sales | Short term (≤ 2 years) |

| Govt digital-voucher schemes for rural consumers | +1.5% | Rural areas and smaller towns | Short term (≤ 2 years) |

| Diaspora-driven cross-border gifting flows | +1.3% | National, with concentration in areas with high emigration | Medium term (2-4 years) |

Source: Mordor Intelligence

Rising mobile and internet penetration

Mobile broadband coverage at 85% 5G reach and household internet uptake of 92% has lifted the Cyprus e-commerce market into a mobile-first era. Smartphone browsing drives micro-moment shopping, and 25% of card purchases already originate from phones. [1]Central Bank of Cyprus, “Speech by the Governor of the Central Bank of Cyprus at the 12th Banking Forum and Fintech Expo,” centralbank.cy Faster networks improve page-load speed and enable richer content such as AR try-ons, increasing conversion. Retailers that optimise UX for smaller screens and introduce one-tap checkouts capture incremental demand. This momentum positions mobile as the primary gateway to the Cyprus e-commerce market over the forecast horizon.

Growing online demand for fashion and apparel

Fashion’s USD 673.80 million revenue base in 2024 explains its 32% grip on the Cyprus e-commerce market. Social-media campaigns and limited-time discounts propel basket sizes, as highlighted by Zara’s Cyprus case study. Sustainable purchasing also plays a role; only 9% of the island’s 27,000 tons of textile waste is recycled, pushing eco-labels into the spotlight. Vintage marketplaces and circular-fashion pop-ups create fresh inventory streams, reinforcing apparel’s pull within the Cyprus e-commerce market.

Improved last-mile logistics and parcel lockers

Accuracy issues linked to fragmented addressing once stifled delivery reliability. A dense parcel-locker grid now gives shoppers flexible pick-up within urban centres, cutting mis-delivery rates and lowering courier costs. International Post Corporation data shows parcels taking more than 15 days dropped to 9% in 2024, versus 29% in 2020. The Port of Limassol hub anchors regional fulfilment strategies for merchants targeting Europe, MENA and North Africa, further enhancing the Cyprus e-commerce market’s logistical profile.

EU e-Commerce VAT package harmonisation

The Import One Stop Shop (IOSS) framework neutralises administrative overhead for SMEs shipping low-value parcels, letting Cypriot sellers concentrate on product quality instead of tax calculations. Harmonised rules join forces with the Digital Services Act to elevate consumer trust, stimulate basket growth, and foster a balanced Cyprus e-commerce market where local brands compete on even terms with multinationals.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Small domestic consumer base | -2.5% | National, with less impact in tourist areas | Long term (≥ 4 years) |

| High shipping and return costs for an island market | -2.1% | National, with greater impact in rural areas | Medium term (2-4 years) |

| Limited Greek-language UX across platforms | -1.2% | National, with higher impact among older demographics | Short term (≤ 2 years) |

| Fragmented address system hurting delivery accuracy | -0.9% | Rural areas and newer developments | Medium term (2-4 years) |

Source: Mordor Intelligence

Small domestic consumer base

A resident population of 1.23 million limits absolute transaction volume. Consequently, 81% of shoppers pivot to overseas merchants to widen assortment choice. [2]European Commission, “Digital Services Act starts applying to all online platforms in the EU,” cyprus.representation.ec.europa.eu Cypriot sellers often design cross-border propositions from day one to scale beyond island boundaries. EU rules that simplify customs and VAT, plus multilingual storefronts, partly offset size constraints. Nevertheless, demand density remains a structural headwind for the Cyprus e-commerce market.

High shipping and return costs for an island market

Sea-freight dependence inflates inbound logistics, and outbound return parcels can exceed product value for low-ticket items. Consumer expectations of free returns clash with merchant cost realities. Retailers mitigate by pooling inventory in local micro-fulfilment centres for fast-moving stock and employing drop-ship models for niche items. These tactics soften, but do not erase, logistics-related drag on the Cyprus e-commerce market.

Segment Analysis

By Business Model: C2C Platforms Disrupting Traditional Retail

The B2C segment accounted for 76% of the Cyprus e-commerce market size in 2024, underpinned by omnichannel chains and international marketplaces delivering consistent UX. Customer expectations around real-time inventory and AI-powered recommendations push merchants to invest in cloud commerce stacks. That investment pays off through higher repeat-purchase rates and larger average order values, reinforcing B2C dominance across the Cyprus e-commerce market.

C2C marketplaces, however, are shifting value capture. An 18.9% CAGR projection to 2030 signals how peer-to-peer trading redefines retail by converting consumers into micro-sellers. Platforms such as Bazaraki.com ease listing friction and build trust via escrow payments, unlocking second-hand and handmade product streams. SMEs comprise 93% of Cypriot firms, and as they digitise purchasing cycles, a latent B2B opportunity emerges. While B2B’s share of the Cyprus e-commerce industry is still modest, greater e-procurement usage portends strong upside after 2027.

Note: Segment shares of all individual segments available upon report purchase

By Device Type: Mobile-First Strategy Driving Conversion

Smartphones generated 69% of all transactions in 2024, underscoring the Cyprus e-commerce market’s clear mobile bias. Faster checkout flows, biometric authentication, and personalised push notifications raise mobile conversion efficiency. Combined with 5G’s 85% footprint, augmented-reality fitting rooms and video consultations become technically feasible, strengthening customer engagement.

Desktop retains relevance for high-consideration items and business users who require detailed configuration. Tablets and voice-commerce devices represent smaller but rising shares. Retailers re-platform front-end interfaces to deliver device-adaptive experiences, ensuring the Cyprus e-commerce market remains accessible across screen types while catering to the dominant mobile cohort.

By Payment Method: Digital Wallets Reshaping Transaction Landscape

Cards still underpin 55% of 2024 e-commerce value, but wallet adoption accelerates as consumers prioritise speed and security. The newest instant-payment rails make QR and mobile-number transfers viable for everyday shopping, nudging usage toward wallets. Cyprus Securities and Exchange Commission’s EUR 10.1 billion (USD 11.64 billion) AUM highlights the liquidity fintechs can tap to scale wallet propositions.

BNPL resonates with younger shoppers, capturing discretionary spend in fashion and electronics. Cryptocurrency acceptance remains niche but attracts high-tech circles. Whichever tender prevails, the Cyprus e-commerce market’s payment mix is diversifying, giving merchants multiple avenues to lift checkout success rates.

Note: Segment shares of all individual segments available upon report purchase

By B2C Product Category: Food and Beverages Outpacing Traditional Leaders

Fashion and apparel captured 32% of the Cyprus e-commerce market share in 2024, cementing its leadership with digitally savvy merchandising. Cross-border sourcing augments assortment, while local brands embrace circular fashion to address eco-concerns and claw back margin from global fast-fashion players.

Food and beverages grows at 19.2% CAGR—a clear outlier in velocity. Same-hour grocery fulfilment offered by Foody widens adoption beyond urban professionals to busy households. Consumer electronics, beauty, furniture and toys follow differentiated growth curves tied to category-specific online penetration barriers. Together, they broaden total Cyprus e-commerce market size over the forecast period.

Geography Analysis

Cyprus integrates tightly with the EU digital single market, and 81% of local online shoppers regularly transact with foreign sellers. Harmonised consumer-protection rules and IOSS reduce friction, underpinning sustained cross-border demand that lifts overall Cyprus e-commerce market activity. Urban strongholds Nicosia and Limassol enjoy dense fulfilment assets and drive category innovation, while government rural-voucher programmes push digital literacy into smaller towns.

Strategic geography matters: the Port of Limassol sits at the junction of Europe, MENA and North Africa, positioning Cyprus as a natural cross-docking node. Multinationals now co-locate micro-fulfilment centres near the port to shorten delivery routes into adjacent markets. Ninety-three foreign companies incorporated in Q1 2025, up 20% on 2024, many in software and digital commerce.

The National Long-Term Strategy for Sustainable Development sets a policy umbrella for innovation, allocating EUR 177.25 million (USD 195.0 million) to digital projects that underpin the Cyprus e-commerce market. ICT already contributes EUR 7 billion to GVA, exhibiting 200% growth since 2011. Enhanced broadband penetration and digital-skills programmes should narrow the urban-rural gap and bolster future Cyprus e-commerce market size.

Competitive Landscape

Global marketplaces—Amazon, eBay, AliExpress—serve Cyprus via cross-border shipping and wield economies of scale that translate into price competitiveness. Local specialists such as Bazaraki.com concentrate on C2C sales and category depth, achieving strong brand recall through localised language support. Traditional chains, including Public Cyprus and Stephanis, leverage store footprints for click-and-collect services, ensuring short lead times and convenient returns. This hybrid competitive mix keeps switching costs low for shoppers and intensifies the battle for loyalty within the Cyprus e-commerce market.

Merchants view technology as a strategic lever: 66% plan AI deployments for fraud screening and dynamic pricing. API-based commerce architectures let firms decouple front-end shopping experiences from back-end order management, accelerating feature releases and personalisation. [3]WDCSTechnology, “Navigating the Future of E-commerce: The Power of API-Based Digital Commerce,” wdcstechnology.ae Sustainability-focused fashion startups differentiate via closed-loop supply chains and digital product passports to win eco-conscious consumers, adding further complexity to competitive positioning.

Financing appetite is solid; Cyprus-based funds control 75% of the EUR 10.1 billion (USD 11.64 billion) AUM recorded in Q4 2024. These capital pools support acquisition roll-ups, marketplace consolidation and warehouse automation projects, accelerating scaling trajectories. As a result, bargaining power is slowly shifting toward platforms that can aggregate traffic and data at scale, shaping medium-term structure of the Cyprus e-commerce market.

Cyprus E-commerce Industry Leaders

-

Amazon.com, Inc.

-

eBay Inc.

-

AliExpress (Alibaba Group Holding Ltd.)

-

Bazaraki.com

-

Public Cyprus Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: The European Commission referred Cyprus to the Court of Justice of the EU over shortcomings at its Digital Services Coordinator.

- April 2025: 93 new foreign companies registered in Q1, a 20% year-on-year rise, led by technology and e-commerce.

- March 2025: A fact-check report confirmed accelerated adoption of e-commerce platforms and AI among Cypriot firms.

- February 2025: The European Commission unveiled actions to improve safety and sustainability of the 4.6 billion low-value parcels entering the EU in 2024.

Cyprus E-commerce Market Report Scope

The Cyprus e-commerce market is segmented by B2B E-commerce and B2C E-commerce. By B2C E-commerce, the market studied is further subdivided into beauty & personal care, consumer electronics, fashion & apparel, food & beverage, and furniture & home.

The study also tracks significant market metrics, underlying growth influencers, and significant industry vendors, providing support for market estimates and growth rates in Cyprus throughout the anticipated period. The study goes on to look at Covid-19's overall influence on the ecosystem.

| By Business Model | B2C |

| B2B | |

| C2C | |

| By Device Type | Smartphone / Mobile |

| Desktop and Laptop | |

| Other Device Types | |

| By Payment Method | Credit / Debit Cards |

| Digital Wallets | |

| BNPL | |

| Other Payment Method | |

| By B2C Product Category | Beauty and Personal Care |

| Consumer Electronics | |

| Fashion and Apparel | |

| Food and Beverages | |

| Furniture and Home | |

| Toys, DIY and Media | |

| Other Product Categories |

By Business Model

| B2C |

| B2B |

| C2C |

By Device Type

| Smartphone / Mobile |

| Desktop and Laptop |

| Other Device Types |

By Payment Method

| Credit / Debit Cards |

| Digital Wallets |

| BNPL |

| Other Payment Method |

By B2C Product Category

| Beauty and Personal Care |

| Consumer Electronics |

| Fashion and Apparel |

| Food and Beverages |

| Furniture and Home |

| Toys, DIY and Media |

| Other Product Categories |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current Cyprus e-commerce market size and growth outlook?

The market stands at USD 1.07 billion in 2025 and is projected to double to USD 2.11 billion by 2030 at a 14.43% CAGR.

Which segment leads the Cyprus e-commerce market by revenue?

Fashion and apparel leads with 32% revenue share in 2024, thanks to strong brand presence and omnichannel strategies.

How important is mobile commerce in Cyprus?

Mobile accounts for 69% of transactions and is expected to expand at a 17.5% CAGR, making smartphone optimisation critical.

What payment methods are gaining ground?

Digital wallets are growing at an 18.1% CAGR and are forecast to overtake cards before 2027, propelled by instant-payment infrastructure.

Why do Cypriot shoppers frequently buy cross-border?

Limited domestic assortment and EU harmonisation encourage 81% of local shoppers to purchase from other EU sellers, broadening choice and price competitiveness.

What structural challenges face the Cyprus e-commerce industry?

Island logistics drive up shipping and return costs, and the small domestic consumer base restricts scale, compelling local merchants to orient strategies toward cross-border expansion.

Page last updated on: June 22, 2025