Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 388.74 Billion |

| Market Size (2031) | USD 490.67 Billion |

| Growth Rate (2026 - 2031) | 4.77% CAGR |

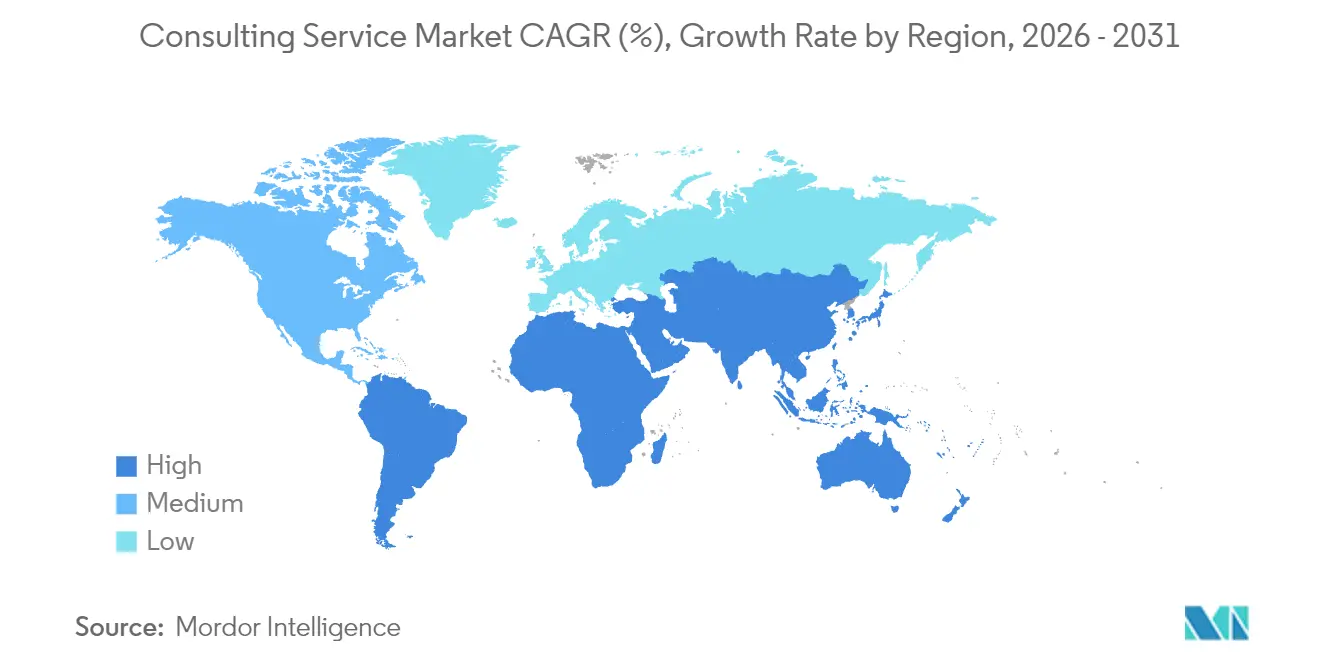

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

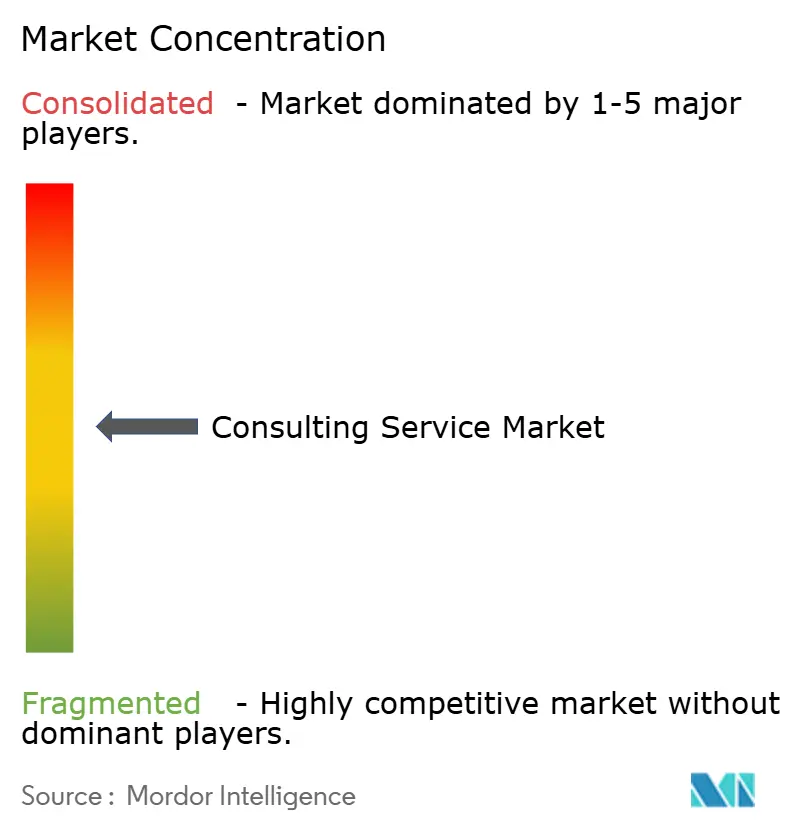

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Consulting Service Market Analysis by Mordor Intelligence

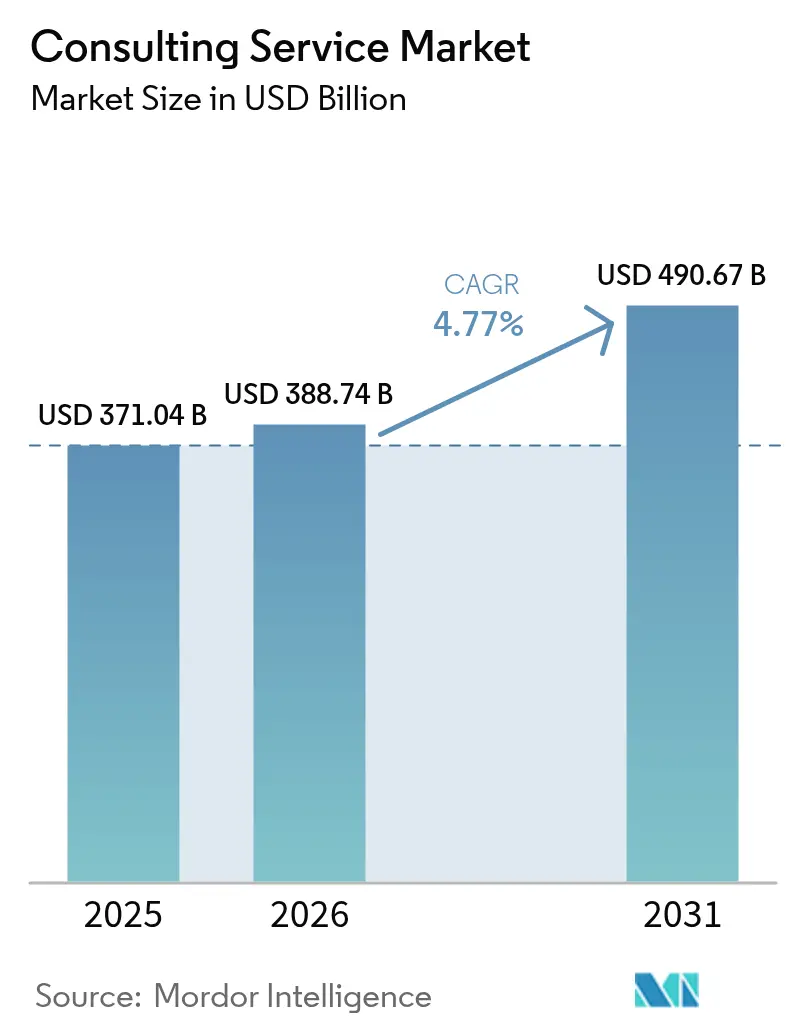

The Consulting Service market size is expected to grow from USD 371.04 billion in 2025 to USD 388.74 billion in 2026 and is forecast to reach USD 490.67 billion by 2031 at 4.77% CAGR over 2026-2031.

The market’s stable expansion reflects a decisive pivot from traditional advisory toward technology-enabled, outcome-oriented engagement models. Board-level urgency around digital transformation, heightened regulatory scrutiny on environmental, social, and governance (ESG) performance, and intensifying cyber risk are funneling enterprise spending toward high-value consulting offerings. Large firms are broadening capability sets through acquisitions that plug expertise gaps in artificial intelligence (AI), cloud migration, and energy transition, while boutique specialists win mandates by offering deep domain knowledge and agile delivery. Hybrid engagement models that combine on-site and virtual delivery are normalizing, allowing firms to access global talent, lower project costs, and reduce travel-related carbon footprints. Competitive differentiation hinges on proprietary platforms, data-driven methodologies, and demonstrable impact metrics that tie fees to measurable client outcomes.

Key Report Takeaways

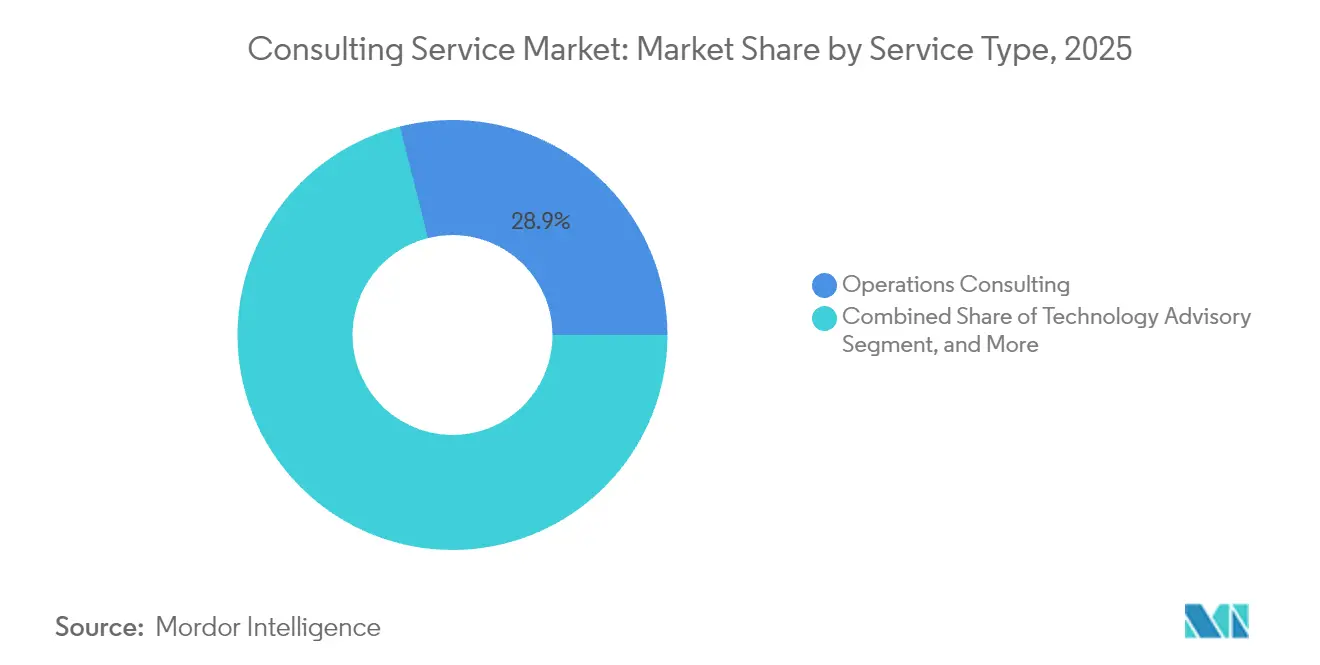

- By service type, Operations consulting held 28.94% of the consulting service market share in 2025, while Technology Advisory is forecast to grow at a 6.29% CAGR through 2031.

- By client industry, the Banking, Financial Services, and Insurance sector commanded 22.10% of the market size in 2025, whereas the Healthcare and Life Sciences sector is projected to expand at a 6.63% CAGR to 2031.

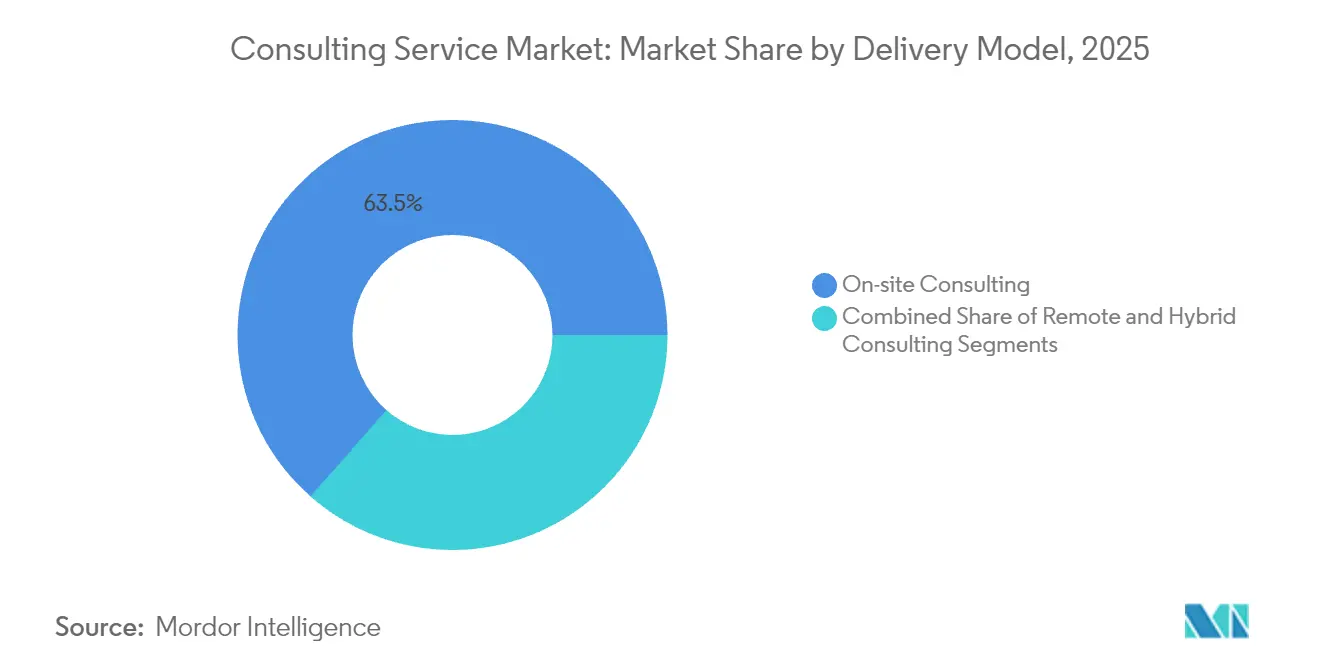

- By delivery model, On-site engagements represented 63.52% revenue share in 2025, but Remote-Virtual consulting is set to progress at a 5.92% CAGR over the forecast horizon.

- By organization size, large enterprises accounted for 70.55% of 2025 spend, yet small and medium-sized enterprises are advancing at the fastest 6.71% CAGR thanks to fractional consulting models.

- By geography, North America led with 40.62% revenue contribution in 2025, while Asia-Pacific is poised to record a 6.92% CAGR through 2031 on the back of infrastructure digitization and energy-transition mandates.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Consulting Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating digital-transformation mandates | +1.20% | Global, with concentration in North America and APAC | Medium term (2-4 years) |

| Heightened post-pandemic operational-efficiency focus | +0.90% | Global, strongest in Europe and North America | Short term (≤ 2 years) |

| Growing regulatory complexity in ESG and risk | +0.80% | Global, led by Europe with spillover to North America | Long term (≥ 4 years) |

| Rapid cloud and cybersecurity adoption | +1.10% | Global, with early gains in North America, APAC core | Medium term (2-4 years) |

| Demand for advisory on Gen-AI governance | +0.70% | North America and Europe, expanding to APAC | Short term (≤ 2 years) |

| Board-level pressure for Scope-3 value-chain decarbonisation | +0.60% | Europe and North America, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Digital-Transformation Mandates

Enterprises are compressing multi-year modernization programs into shorter cycles, driving premium demand for consultants who can orchestrate cloud migration, data modernization, and advanced analytics at scale. Industry-specific cloud solutions allow sector customization, prompting consultants to blend process redesign with technology implementation. Healthcare providers are deploying telehealth ecosystems, manufacturers are embedding sensors for predictive maintenance, and financial institutions are rolling out real-time payment rails. Consulting firms respond with dedicated industry-cloud practices that cover architecture design, data migration, and compliance alignment, repositioning themselves as execution partners rather than purely strategic advisors. The shift elevates long-term annuity revenue from managed services that follow the initial transformation phase.

Heightened Post-Pandemic Operational-Efficiency Focus

Cost containment remains a board priority as supply-side inflation and wage pressure erode margins. Organizations demand quantifiable return-on-investment from consulting engagements, spurring outcome-based fee models tied to throughput gains, automation intensity or working-capital release. Assignments increasingly revolve around process mining, intelligent automation and lean restructuring of hybrid workforces. Consultants embed performance dashboards that track key performance indicators in real time, ensuring transparency and accelerating decision-making. This results-oriented mindset cements consulting firms as value-creation partners rather than discretionary spend items, strengthening wallet share among cost-conscious clients.

Growing Regulatory Complexity in ESG and Risk

The U.S. Securities and Exchange Commission’s climate disclosure rule and the European Union’s Corporate Sustainability Reporting Directive force companies to present auditable carbon and social impact data. Consulting firms are developing integrated ESG offerings that span materiality assessment, data-architecture design, assurance readiness, and stakeholder communication. Scope-3 emission accounting demands cross-value-chain collaboration, supplying consultants with multi-year engagements that blend carbon-footprint modelling with supplier-enablement programs. As ESG evolves from a compliance requirement to a strategic differentiator, organizations seek advisors who can translate sustainability into a competitive advantage through portfolio realignment and product innovation.

Demand for Advisory on Gen-AI Governance

Proliferation of generative AI pilots has triggered governance concerns spanning model bias, intellectual-property leakage, and regulatory compliance. Clients turn to consultants for model-risk frameworks, responsible-AI policies, and talent-upskilling road maps that balance innovation with oversight. Structured governance accelerators, often developed in partnership with hyperscale’s, shorten adoption timelines while mitigating ethical and legal pitfalls. The nascent nature of regulations positions consulting firms as trusted intermediaries between technology vendors, regulators, and corporate boards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Client cost-cutting and in-house capability build | -1.10% | Global, strongest impact in North America and Europe | Short term (≤ 2 years) |

| Talent scarcity and wage inflation | -0.80% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Rising carbon-footprint scrutiny of travel-heavy projects | -0.30% | Europe and North America, emerging in APAC | Medium term (2-4 years) |

| Vendor-lock-in concerns around proprietary consulting assets | -0.40% | Global, particularly in technology consulting | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Client Cost-Cutting and In-House Capability Build

Economic caution is prompting enterprises to rebalance external spend toward strategic gaps only, while internal centers of excellence absorb routine advisory functions. Selective sourcing strategies emphasize value capture, pushing consultants to differentiate through proprietary tools, industry benchmarks and outcome guarantees. Simultaneously, firms offer co-sourcing models that embed consultants within client teams to transfer knowledge and speed capability maturation, preserving engagement opportunities despite budget restraint.

Talent Scarcity and Wage Inflation

Demand for practitioners versed in AI governance, advanced analytics, and ESG outstrips supply, inflating compensation and compressing project margins. Firms react by accelerating internal training academies, tapping alternate labour pools, and deploying offshore delivery centers. Flexible work arrangements, gig-based staffing, and alumni networks are leveraged to expand capacity while containing fixed costs. Sustained talent deficits may spur further consolidation as scale advantages in recruitment and learning development favour larger firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Technology Advisory Leads Growth

Operations consulting captured 28.94% of the consulting service market share in 2025, underscoring persistent demand for process optimization across manufacturing, retail, and energy sectors. Technology Advisory is expanding at a 6.29% CAGR as enterprises seek expertise in AI governance, cloud transformation, and cyber-resilience. The market benefits from the convergence of technology and traditional management advisory, prompting firms to invest in end-to-end capabilities spanning strategy, implementation, and managed services.Technology Advisory engagements increasingly bundle cloud-migration road maps with cybersecurity safeguards and data-modernization blueprints. Firms integrate proprietary accelerators to compress timelines and lower risk, creating annuity revenue through managed cloud operations. Operations consulting remains relevant by embedding digital twins, process-mining analytics, and robotic process automation into classic lean toolkits. Cross-selling between Operations and Technology practices deepens wallet share and exemplifies the consulting service market's shift toward integrated transformation solutions.

By Client Industry: Healthcare Drives Innovation

The Healthcare and Life Sciences segment is forecast to post a 6.63% CAGR, outpacing all other verticals as digital therapeutics, remote patient monitoring, and AI-assisted drug discovery reshape operating models. BFSI retained 22.10% of the consulting service market size in 2025, reflecting sustained cybersecurity, regulatory compliance, and core-bank modernization projects. Consulting opportunities in energy and utilities concentrate on decarbonization strategy, grid modernization, and hydrogen ecosystem planning, reinforcing the sector's reliance on multidisciplinary advisory.

Heightened data-privacy regulation, patient-centric care models, and reimbursement shifts underpin healthcare consulting momentum. Firms combine regulatory know-how with technology enablement, guiding providers through electronic-health-record upgrades and cloud-based clinical trial platforms. In financial services, demand centers on real-time payment rails, digital identity, and environmental risk stress-testing. Cross-vertical synergies emerge as ESG disclosure rules and data-governance standards converge, expanding the market's addressable scope.

By Delivery Model: Hybrid Transformation Accelerates

On-site delivery retained 63.52% revenue contribution in 2025, favoured for complex program mobilization and stakeholder alignment. Remote-Virtual engagements are advancing at a 5.92% CAGR as collaborative platforms, augmented-reality walkthroughs, and secure document-sharing remove geographic constraints. The consulting service market is converging toward hybrid models that flex travel intensity according to phase requirements, balancing relationship depth with cost and sustainability objectives.

Hybrid delivery allows firms to assemble global experts rapidly while embedding regional consultants for cultural alignment. Virtual whiteboard tools, digital twin simulations, and secure code repositories maintain productivity without physical co-location. Procurement functions adapt by enforcing service-level agreements that include uptime for collaboration technologies and measurable client-experience indicators. The emerging standard redefines consultant skill sets to include virtual facilitation, remote team leadership, and asynchronous workflow management.

By Organization Size: SME Growth Accelerates

Large enterprises generated 70.55% of 2025 consulting revenue, yet small and medium-sized enterprises are projected to record the fastest 6.71% CAGR through 2031. Democratization of expertise via cloud-delivered toolkits and subscription-based advisory lowers entry barriers, enlarging the consulting service market’s long-tail opportunity. Fractional chief information officer and part-time chief sustainability officer offerings allow SMEs to access senior talent without full-time cost commitments.

Standardized playbooks, modular deliverables, and AI-assisted diagnostics underpin SME service packages, enabling consultants to maintain margins while pricing competitively. Large enterprises remain essential clients for multi-year transformation programs, but growth in the SME segment enriches the demand mix and compels firms to adopt tiered pricing, streamlined contracting, and self-service knowledge portals.

Geography Analysis

North America generated 40.62% of 2025 revenue, buoyed by high technology adoption, federal cybersecurity funding, and stringent financial services regulation. U.S. enterprises engage consultants for AI governance frameworks, zero-trust architecture implementation, and ESG compliance road maps. Canada contributes niche growth in energy-transition consulting, leveraging its resource-rich economy to test carbon-capture and hydrogen pilot schemes. Intensifying climate-related disclosure mandates sustains long-term consulting demand across both countries.

Asia-Pacific is the fastest-growing region, set to expand at a 6.92% CAGR through 2031, propelled by large-scale digital-infrastructure projects, e-government initiatives, and renewables build-out. China anchors regional demand with AI-infused supply-chain optimization and consumer banking digitization. Japan’s emphasis on industrial robotics and Singapore’s status as a financial-services innovation hub create fertile terrain for specialized consulting shops. India blends healthcare digitalization, manufacturing automation, and smart-city programs, reinforcing the consulting service market’s momentum in the subcontinent.

Europe maintains steady growth, driven by energy-transition imperatives, data-privacy regulation and sustainability leadership. The Corporate Sustainability Reporting Directive compels companies to seek advisors who can meet stringent reporting timelines and assurance thresholds. Germany and France focus on Industry 4.0 productivity gains, while the Nordics pioneer circular-economy strategies that elevate demand for innovative operating-model rewiring. Middle East and Africa harness diversification policies and mega-infrastructure projects to attract global consulting expertise, whereas South America’s natural-resource producers require ESG and operational-efficiency road maps to remain globally competitive.

Competitive Landscape

Top Companies in Consulting Services Market

The consulting service market remains fragmented, although acquisition-led consolidation is rising as firms race to capture scarce capabilities in AI governance, energy transition, and industry-cloud deployment. The Big Four leverage integrated audit, tax, and advisory relationships to cross-sell transformation road maps, while strategy boutiques focus on high-impact C-suite issues. Technology giants such as IBM and Accenture are deepening sector reach through targeted buys of data-engineering specialists and sustainability boutiques, transforming themselves into one-stop transformation partners.

Boutique players differentiate through domain depth, agile delivery, and value-based pricing, winning mandates in niche fields such as quantum-safe cryptography or regenerative agriculture supply chains. Platform-based disruptors connect independent experts to clients via digital marketplaces, lowering switching costs and pressuring traditional pyramid staffing models. Outcome-based contracts that link fees to EBITDA uplift or emission-reduction milestones proliferate, reinforcing competitive emphasis on measurable impact.

Strategic positioning revolves around proprietary accelerators that shorten diagnosis cycles, AI-enabled knowledge management that reduces onboarding time and managed-services extensions that lock in multi-year revenue. Brand equity, talent density and global delivery reach remain core selection criteria, yet the market increasingly rewards firms that can demonstrate thought-leadership credibility and a track record of rapid value creation under constrained budgets.

Consulting Service Industry Leaders

Deloitte Touche Tohmatsu Limited

Accenture PLC

PricewaterhouseCoopers LLP

Ernst & Young Global Limited

Capgemini SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Accenture announced the acquisition of Maryville Consulting Group, bolstering technology-strategy depth and ServiceNow partnerships.

- July 2025: Marsh McLennan posted 12% revenue growth, with consulting segment sales at USD 2.4 billion driven by Oliver Wyman and Mercer performance.

- July 2025: Cognizant reported Q2 2025 revenue of USD 5.25 billion and record bookings totalling USD 27.8 billion across AI-led transformation megadeals.

- April 2025: EY revealed a collaboration with NVIDIA to launch AI-agent-powered service offerings.

Global Consulting Service Market Report Scope

The consulting service market encompasses a vast array of expertise and industries where professionals offer specialized knowledge and guidance to clients seeking solutions to complex problems or improving their operations.

The consulting service market is segmented by service type (operations consulting, strategy consulting, financial advisory, technology advisory, and other service types) and geography (North America [United States, Canada], Europe [United Kingdom, Germany, France, Benelux, Italy, Rest of Europe], Asia-Pacific, Latin America [Brazil and Rest of Latin America] and Middle East and Africa). The report offers the market size in value (USD) for all the abovementioned segments.

By Service Type (Value)

| Operations Consulting |

| Strategy Consulting |

| Financial Advisory |

| Technology Advisory |

| Human-Capital Consulting |

| Risk and Compliance Consulting |

| Other Service Types |

By Client Industry (Value)

| BFSI |

| Healthcare and Life Sciences |

| Energy and Utilities |

| Manufacturing and Automotive |

| ICT and Media |

| Public Sector |

| Consumer and Retail |

| Other Industries |

By Delivery Model (Value)

| On-site Consulting |

| Remote / Virtual Consulting |

| Hybrid Consulting |

By Organisation Size (Value)

| Large Enterprises |

| Small and Medium-sized Enterprises |

By Geography (Value)

| North America | United States | |

| Canada | ||

| South America | Brazil | |

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Asia-Pacific (APAC) | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Africa | South Africa | |

| By Service Type (Value) | Operations Consulting | ||

| Strategy Consulting | |||

| Financial Advisory | |||

| Technology Advisory | |||

| Human-Capital Consulting | |||

| Risk and Compliance Consulting | |||

| Other Service Types | |||

| By Client Industry (Value) | BFSI | ||

| Healthcare and Life Sciences | |||

| Energy and Utilities | |||

| Manufacturing and Automotive | |||

| ICT and Media | |||

| Public Sector | |||

| Consumer and Retail | |||

| Other Industries | |||

| By Delivery Model (Value) | On-site Consulting | ||

| Remote / Virtual Consulting | |||

| Hybrid Consulting | |||

| By Organisation Size (Value) | Large Enterprises | ||

| Small and Medium-sized Enterprises | |||

| By Geography (Value) | North America | United States | |

| Canada | |||

| South America | Brazil | ||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Asia-Pacific (APAC) | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Africa | South Africa | ||

Key Questions Answered in the Report

How big is the Consulting Service Market?

The Consulting Service Market size is expected to reach USD 388.74 billion in 2026 and grow at a CAGR of 4.77% to reach USD 490.67 billion by 2031.

What is the current Consulting Service Market size?

In 2026, the Consulting Service Market size is expected to reach USD 388.74 billion.

Who are the key players in Consulting Service Market?

Deloitte Touche Tohmatsu Limited, Accenture PLC, PricewaterhouseCoopers LLP, Ernst & Young Global Limited and Capgemini SE are the major companies operating in the Consulting Service Market.

Which is the fastest growing region in Consulting Service Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Consulting Service Market?

In 2026, the North America accounts for the largest market share in Consulting Service Market.

What years does this Consulting Service Market cover, and what was the market size in 2025?

In 2025, the Consulting Service Market size was estimated at USD 371.04 billion. The report covers the Consulting Service Market historical market size for years: 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Consulting Service Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: