No Code AI Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

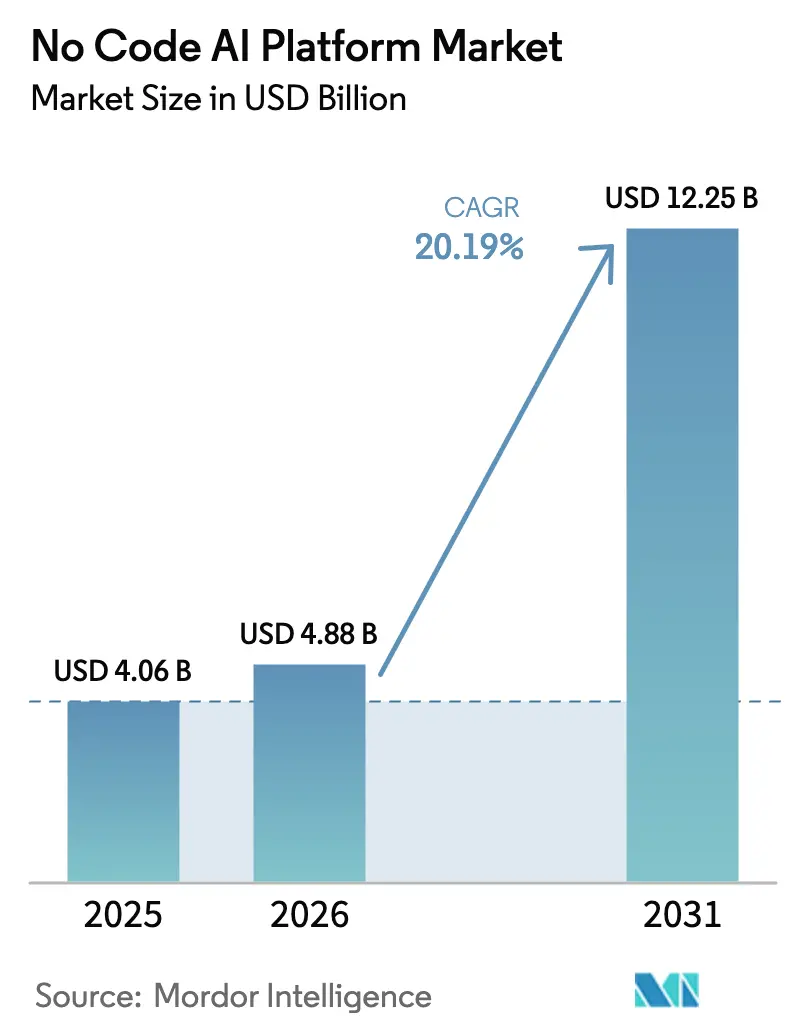

| Market Size (2026) | USD 4.88 Billion |

| Market Size (2031) | USD 12.25 Billion |

| Growth Rate (2026 - 2031) | 20.19% CAGR |

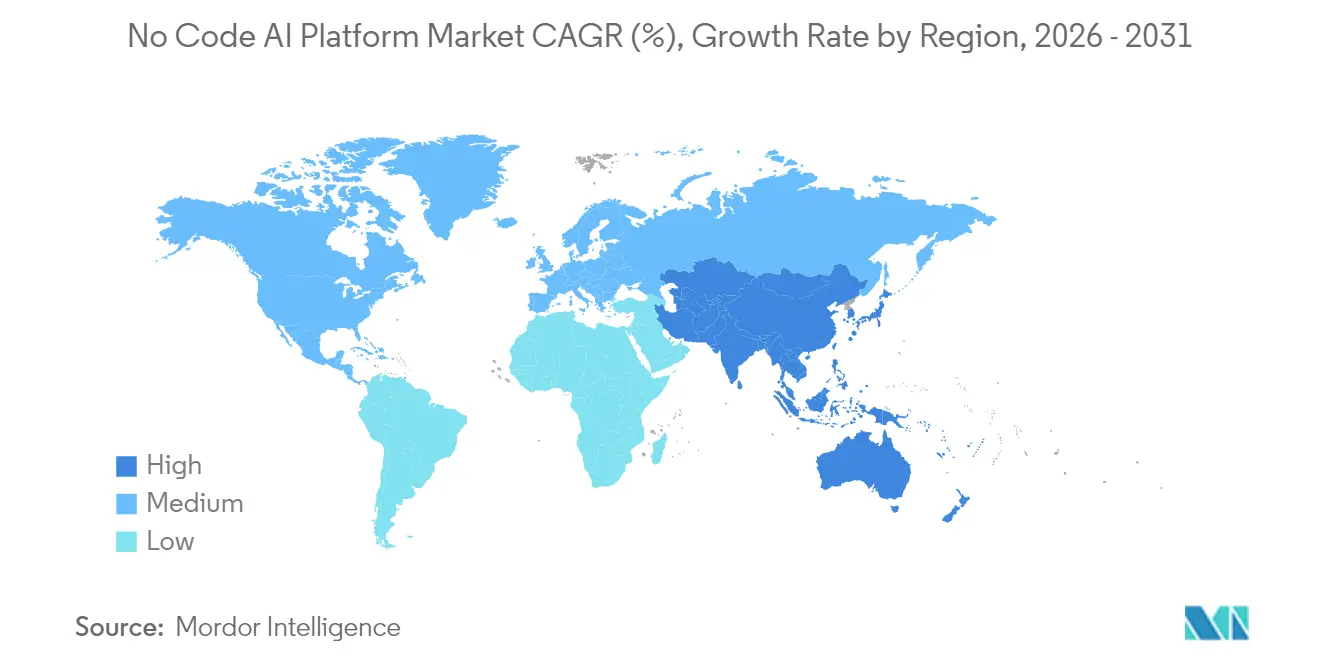

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

No Code AI Platform Market Analysis by Mordor Intelligence

The No-Code AI Platform market size in 2026 is estimated at USD 4.88 billion, growing from 2025 value of USD 4.06 billion with 2031 projections showing USD 12.25 billion, growing at 20.19% CAGR over 2026-2031. Strong enterprise demand for faster application delivery, growing citizen-developer programs, and steady advances in generative AI engines continued to lift adoption across industries. North America remained the largest regional hub, supported by deep venture capital pools and mature cloud infrastructure, while Asia-Pacific advanced as the fastest-growing arena on the back of government-backed digital transformation initiatives. Platform vendors deepened their marketplaces with pre-built models, helping firms with limited data-science talent jump-start AI projects. Heightened regulatory attention around model governance, however, reinforced a preference for private-cloud and on-premises deployments within healthcare and financial services.

Key Report Takeaways

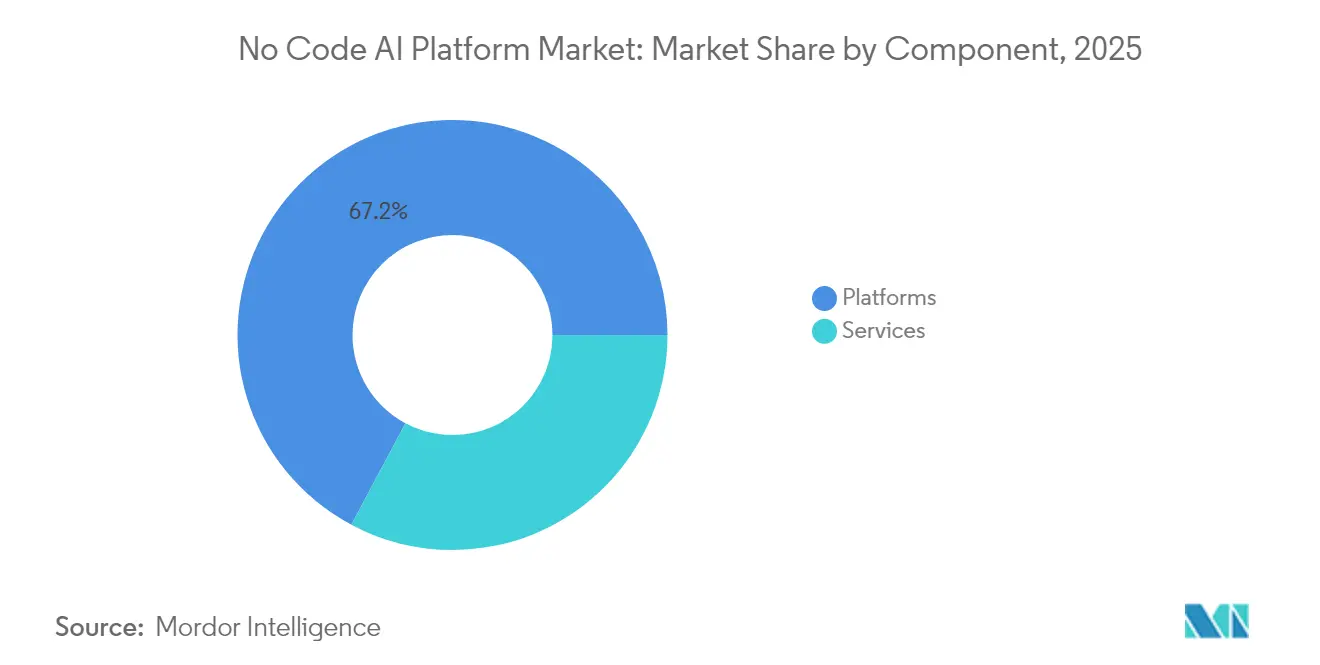

- By component, platforms and solutions led with 67.20% revenue in 2025, while services are projected to expand at a 29.74% CAGR through 2031.

- By technology, predictive and prescriptive analytics held 50.35% of the No-Code AI Platform market share in 2025; multimodal generative AI is expected to climb at a 44.26% CAGR to 2031.

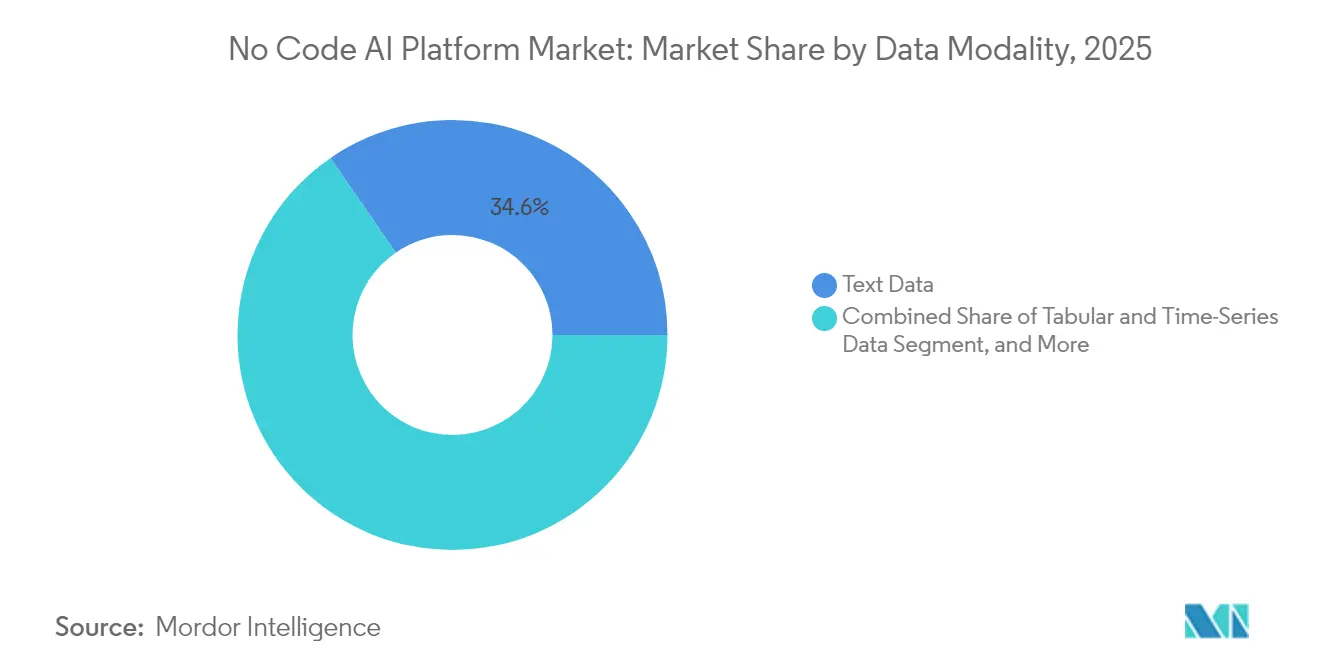

- By data modality, image and video processing applications are poised to grow at 36.48% CAGR from 2026-2031, outpacing text-centric use cases.

- By deployment mode, on-premises and private cloud options accounted for 56.25% of the No-Code AI Platform market size in 2025 as regulated sectors prioritized data sovereignty.

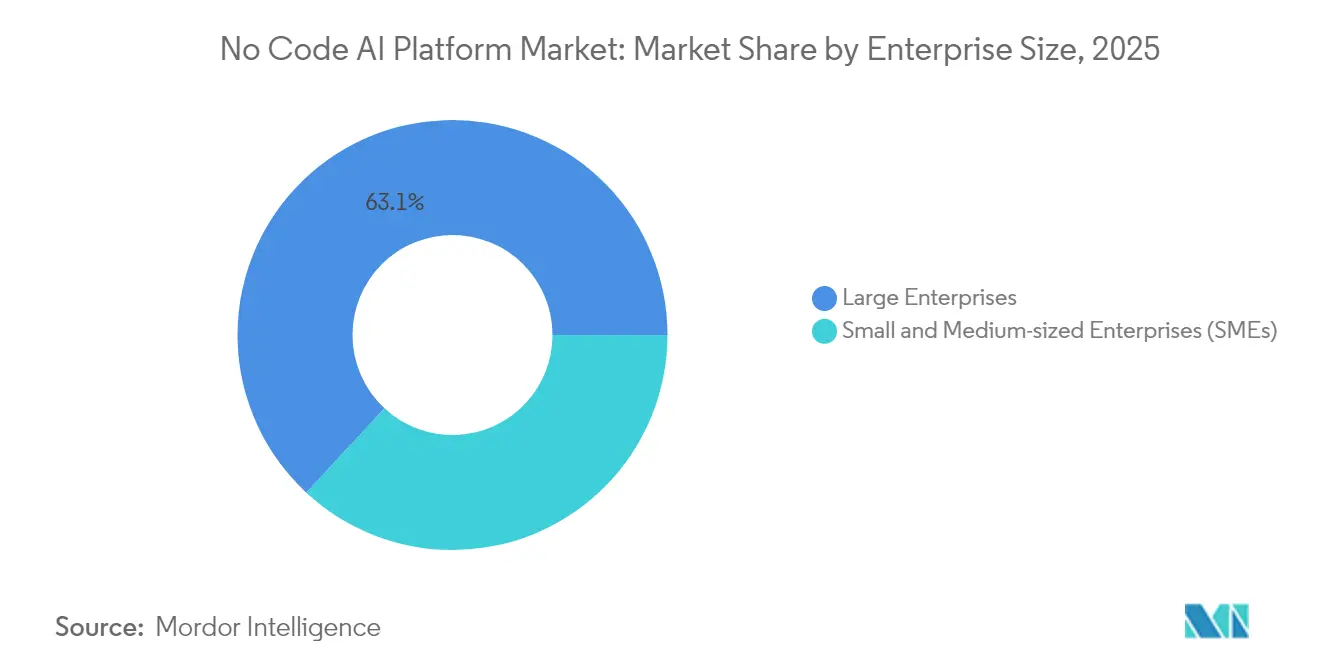

- By enterprise size, SMEs are forecast to grow at 38.62% CAGR through 2031, narrowing the usage gap with large enterprises that held 63.10% share in 2025.

- By vertical, BFSI maintained a 22.45% revenue lead in 2025, while healthcare is projected to post the fastest 35.12% CAGR through 2031.

- By geography, North America maintained a 37.40% revenue lead in 2025, while Asia-Pacific is projected to post the fastest 31.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global No Code AI Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of citizen-developer initiatives in BFSI | +3.5% | North America and Europe | Medium term (2-4 years) |

| Generative-AI add-ons boosting platform stickiness | +3.2% | Global | Short term (≤ 2 years) |

| Surging demand for verticalized no-code AI | +2.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Edge-optimised no-code ML for IoT fleets | +2.4% | Asia-Pacific, North America | Long term (≥ 4 years) |

| Expansion of AI marketplaces within platforms | +2.1% | Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Venture funding shift to hyper-specific use cases | +0.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Citizen-Developer Initiatives in BFSI

Major banks scaled internal programs that let business users build compliance and customer-experience workflows without coding, cutting manual review effort by up to 90%.[1]Lucinity, “7 Compliance and FinCrime Trends for 2025,” lucinity.com Budget ownership shifted from IT to line managers, accelerating project throughput and enlarging the addressable No-Code AI Platform market. Early movers reported faster loan-underwriting cycles and improved fraud-detection accuracy. Union Foncière de France demonstrated cost savings near 30% after rolling out a no-code sales-engagement engine. Such results encouraged regulators to view low-code tooling as a valid path toward operational resilience, further reinforcing adoption.

Generative-AI Add-ons Boosting Platform Stickiness

Vendors embedded multimodal large-language and vision models into drag-and-drop studios, enabling users to turn plain-language prompts into fully formed workflows. Microsoft Copilot Studio surpassed 230,000 organisational tenants during 2025, underscoring the retention uplift tied to generative extensions. Retailers leveraged these add-ons to generate marketing copy and imagery, while manufacturers applied them to swift design iterations. Each new capability kept customers within the same platform, curbing churn and enlarging subscription footprints across the No-Code AI Platform market.

Surging Demand for Verticalized No-Code AI

Hospitals, insurers, and industrial plants increasingly sought domain-specific templates that embed sector regulations and vocabulary. John Snow Labs released specialised medical language models tuned for clinical-note automation, illustrating the appeal of purpose-built solutions. Buyers valued shorter deployment times and certified compliance artifacts over generic toolkits, lifting ASPs and opening white-space for niche vendors within the No-Code AI Platform market.

Edge-Optimized No-Code ML for IoT Fleets

Latency-sensitive use cases in manufacturing and utilities drove interest in edge-ready workflows. Edge Impulse logged more than 118,000 projects on its tiny-ML service, showing an appetite for low-power inference pipelines that run without cloud links. Companies used no-code dashboards to compress and deploy models onto asset-monitoring sensors, enabling real-time anomaly alerts while satisfying data-sovereignty rules. This evolution expanded the reach of the No-Code AI Platform market into brownfield operational environments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited custom model governance frameworks | -2.4% | Global (focus on Europe) | Medium term (2-4 years) |

| Persistent “shadow-IT” security concerns in regulated sectors | -1.6% | North America, Europe | Short term (≤ 2 years) |

| Vendor lock-in tied to proprietary AutoML pipelines | -1.1% | Global | Long term (≥ 4 years) |

| Data-residency challenges for cross-border deployments | -0.7% | Europe, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Custom Model Governance Frameworks

Rapid citizen-developer growth outpaced internal review processes, creating blind spots in traceability and bias control. The FAICP framework urged firms to embed lifecycle checkpoints tailored to no-code assets, yet adoption remained uneven. In Europe, the impending AI Act mandated rigorous documentation for high-risk systems, raising compliance costs and slowing some purchase decisions inside the No-Code AI Platform market.

Persistent “Shadow-IT” Security Concerns in Regulated Sectors

Employees sometimes bypassed official procurement to trial external AI tools, broadening the threat surface. Academic work linked shadow-AI incidents to data-exposure risks, especially where sensitive financial or health records were involved. Financial institutions consequently tightened identity and access controls, delaying deployments until platforms delivered granular policy enforcement and audit logs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace Platform Growth

Services revenue accelerated on a projected 29.74% CAGR for 2026-2031, even though platforms held 67.20% share of the No-Code AI Platform market in 2025. Clients sought specialised support for model optimisation, cost governance, and organisational change. The introduction of FinOps-style engagements addressed the issue of runaway compute bills during experimentation phases. MIT Professional Education’s 12-week certificate, centred on practical low-code implementation, underlined the growing demand for workforce upskilling.

The consulting layer expanded beyond initial setup into managed-lifecycle services covering continuous validation and sector-specific compliance. This shift pushed many vendors to launch partner ecosystems, offering pre-certified consultancies to de-risk projects. The trend increased average contract values and fortified recurring revenue streams within the No-Code AI Platform market.

By Technology: Multi-modal GenAI Disrupts Analytics Dominance

Predictive and prescriptive analytics commanded a 50.35% share in 2025, yet multimodal generative AI is forecast to rise at a 44.26% CAGR. Google’s Gemini framework, capable of fusing text, image, and audio input, illustrated the widening toolkit available to non-technical builders. The No-Code AI Platform market size for generative functions is expected to expand sharply as firms embed AI-driven content production into marketing and design workflows.

Business users now compose applications with natural-language prompts, skipping SQL and Python entirely. Start-ups that integrate vector databases and retrieval-augmented generation gained traction, particularly for customer-service knowledge bots. This shift lowered time-to-value and anchored the No-Code AI Platform market around conversational experiences rather than dashboard-centric analytics.

By Data Modality: Image/Video Processing Accelerates Innovation

Text kept a 34.60% share in 2025, but computer-vision workloads are projected to grow at 36.48% CAGR to 2031. Retailers used visual AI to automate shelf monitoring, and hospitals trialled imaging triage tools. Super Annotate placed the multimodal AI segment value at USD 1.2 billion for 2023, with growth above 30% through 2032. No-code studios bundled pre-trained object-detection blocks, allowing domain experts to refine models using small, labelled datasets.

Tabular and time-series inputs remained crucial for IoT predictive maintenance. Vendors augmented these pipelines with low-latency embedding layers, letting builders mix sensor feeds and camera frames inside a single workflow. Such convergence lifted the practical ceiling on use-case complexity across the No-Code AI Platform market.

By Deployment Mode: Private Cloud Prioritises Security

Private-cloud and on-premise instances accounted for 56.25% of the No-Code AI Platform market size in 2025 amid heightened regulatory oversight. HPE introduced a turnkey private-cloud stack that promised same-day deployment of GPU clusters, appealing to banks and hospitals seeking data-sovereignty controls.

Public-cloud SaaS grew off a smaller base at 32.85% CAGR, helped by simplified subscription models. Red Hat OpenShift AI showcased hybrid orchestration that kept sensitive data local while bursting inference jobs to the public cloud during peaks. This flexibility widened deployment choices and removed a key barrier for cost-sensitive adopters inside the No-Code AI Platform market.

By Enterprise Size: SMEs Embrace AI Democratization

Large enterprises held 63.10% revenue in 2025, yet SMEs are set to expand at 38.62% CAGR through 2031, propelled by template libraries and consumption-based pricing. Appt.dev projected that no-code tooling would power 70% of new business apps by 2025, with small firms responsible for most deployments. Fast prototyping enabled a real estate agency to assemble a full property management suite in three weeks, highlighting the agility benefits.

For incumbents, no-code studios trimmed IT backlogs and unlocked shadow budgets inside functional departments. The cost parity between low-code and custom development tipped decisively in favour of simplified tooling, broadening the No-Code AI Platform market addressable base.

By Industry Vertical: Healthcare Leads Transformative Adoption

Healthcare is projected to post a 35.12% CAGR, overtaking early BFSI leaders. The US Department of Health and Human Services laid out a strategic blueprint that encouraged AI for clinical documentation and public-health forecasting. Hospitals adopted speech-to-text triage and imaging anomaly detection via drag-and-drop components, reducing administrative burden.

Retailers used recommendation engines and fraud-detection pipelines, while manufacturers embedded real-time quality control on production lines. Governments trialled citizen-service chatbots. Energy utilities leveraged forecasting templates to balance grids. This breadth illustrated the horizontal reach of the No-Code AI Platform market and its fit for regulated and unregulated sectors alike.

Geography Analysis

North America retained 37.40% revenue share in 2025, anchored by a rich vendor ecosystem and robust venture funding that reached USD 204 billion, half of which targeted AI start-ups. Financial-services leaders used citizen-developer programs to compress release cycles, while public-sector agencies piloted low-code portals for constituent engagement. Mature cloud and data-centre resources shortened onboarding times, reinforcing the region’s primacy within the No-Code AI Platform market.

Asia-Pacific delivered the fastest growth, projected at 31.46% CAGR through 2031. China ramped up AI hardware grants, while India’s IT-services majors packaged low-code accelerators for export and domestic clients. Kingdee International reported four consecutive years of low-code platform leadership in China and highlighted wide enterprise uptake of its AI assistants. Government incentives and smartphone ubiquity helped local SMEs leapfrog legacy software stages.

Europe emphasised privacy and ethical oversight. The forthcoming AI Act steers platform roadmaps toward explainable-AI dashboards and audit trails. Vendors responded with region-specific compliance packs and federated-learning options to sidestep cross-border data transfers. Nordic countries remained early adopters, while Southern Europe focused on public-sector digital-service upgrades, collectively growing the No-Code AI Platform market despite tighter rules.

Competitive Landscape

The vendor mix stayed moderately fragmented as enterprise software giants expanded suites and vertical start-ups carved niche footholds. Microsoft deepened Copilot Studio integrations with Dynamics workflows, locking in customers seeking unified user experiences. C3AI partnered with Google Cloud Marketplace to push no-code generative modules to a wider base.

Specialists emphasised industry-specific toolkits. John Snow Labs focused on healthcare NLP, while Edge Impulse targeted embedded sensors. Strategic alliances flourished: Citizens Financial Group opened a Hyderabad centre with Cognizant to co-develop banking AI powered by Neuro® platform components.[4]Citizens Financial Group, “Partnership with Cognizant,” news.cognizant.com

Ecosystem building grew critical. Vendors launched model registries and revenue-sharing marketplaces, enabling third-party developers to monetise templates. This flywheel attracted domain partners and expanded functional coverage, intensifying rivalry yet improving client choice inside the No-Code AI Platform market.

No Code AI Platform Industry Leaders

DataRobot, Inc.

Dataiku SAS

H2O.ai Inc.

RapidMiner Inc.

BigML Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Microsoft unveiled GitHub Copilot evolution and low-code Copilot customization features at Build 2025, noting 15 million developers on Copilot and 230,000 tenant adoptions of Copilot Studio.

- May 2025: John Snow Labs won the 2025 Oracle Excellence Award for its medical reasoning LLM and updated Generative AI Lab.

- May 2025: HPE launched Private Cloud AI for turnkey secure deployments.

- April 2025: Citizens Financial Group and Cognizant opened a Global Capability Center in Hyderabad to accelerate AI-driven banking solutions.

Global No Code AI Platform Market Report Scope

No-code AI tools enable automation via user-friendly plug-and-play or drag-and-drop interfaces. These intuitive ML platforms effectively harness the time, value, and knowledge trade-off, empowering users without AI coding expertise to enhance daily operations and address business challenges.

no code ai platform market is segmented by component (platform, and services), by enterprise size (large enterprises, and SMES), by deployment (on-premise, and cloud), by end users (IT & telecom, BFSI, retail & e-commerce, healthcare & lifesciences, government, and others) and by geography (North America, Europe, Asia Pacific, Latin America, Middle East And Africa). the market size and forecasts are provided in terms of value (USD) for all the above segments.

| Platforms (Solution Suites) |

| Services (Implementation, Training, Support) |

| Natural Language Processing |

| Computer Vision |

| Predictive and Prescriptive Analytics |

| Multi-modal / Generative AI |

| Text Data |

| Image/Video Data |

| Tabular and Time-Series Data |

| Cloud |

| On-premises / Private Cloud |

| Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) |

| BFSI |

| IT and Telecom |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Energy and Utilities |

| Government and Public Sector |

| Manufacturing and Industrial |

| Others (Education, Media, etc.) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Platforms (Solution Suites) | ||

| Services (Implementation, Training, Support) | |||

| By Technology | Natural Language Processing | ||

| Computer Vision | |||

| Predictive and Prescriptive Analytics | |||

| Multi-modal / Generative AI | |||

| By Data Modality | Text Data | ||

| Image/Video Data | |||

| Tabular and Time-Series Data | |||

| By Deployment Mode | Cloud | ||

| On-premises / Private Cloud | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium-sized Enterprises (SMEs) | |||

| By Industry Vertical | BFSI | ||

| IT and Telecom | |||

| Healthcare and Life Sciences | |||

| Retail and E-commerce | |||

| Energy and Utilities | |||

| Government and Public Sector | |||

| Manufacturing and Industrial | |||

| Others (Education, Media, etc.) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| Taiwan | |||

| India | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the No-Code AI Platform market?

The market was valued at USD 4.88 billion in 2026 and is projected to hit USD 12.25 billion by 2031.

Which region is expanding fastest for no-code AI platforms?

Asia-Pacific is expected to grow at a 31.46% CAGR from 2026-2031, driven by government digital-transformation programmes and expanding cloud access.

Why are private-cloud deployments dominant in regulated sectors?

Organisations in finance and healthcare prioritised data sovereignty and compliance, giving private-cloud and on-premise models a 56.25% share in 2025.

How quickly are SMEs adopting no-code AI platforms?

SMEs are forecast to grow platform spending at 38.62% CAGR through 2031 as template libraries reduce technical barriers.

Which technology segment is poised for the highest growth?

Multimodal generative AI capabilities are projected to grow at 44.26% CAGR, reshaping how users create cross-format applications.

What remains the biggest restraint to wider adoption?

Limited model-governance frameworks raise compliance risks, especially under the EU AI Act, slowing deployments until stronger controls mature.

Page last updated on: