Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

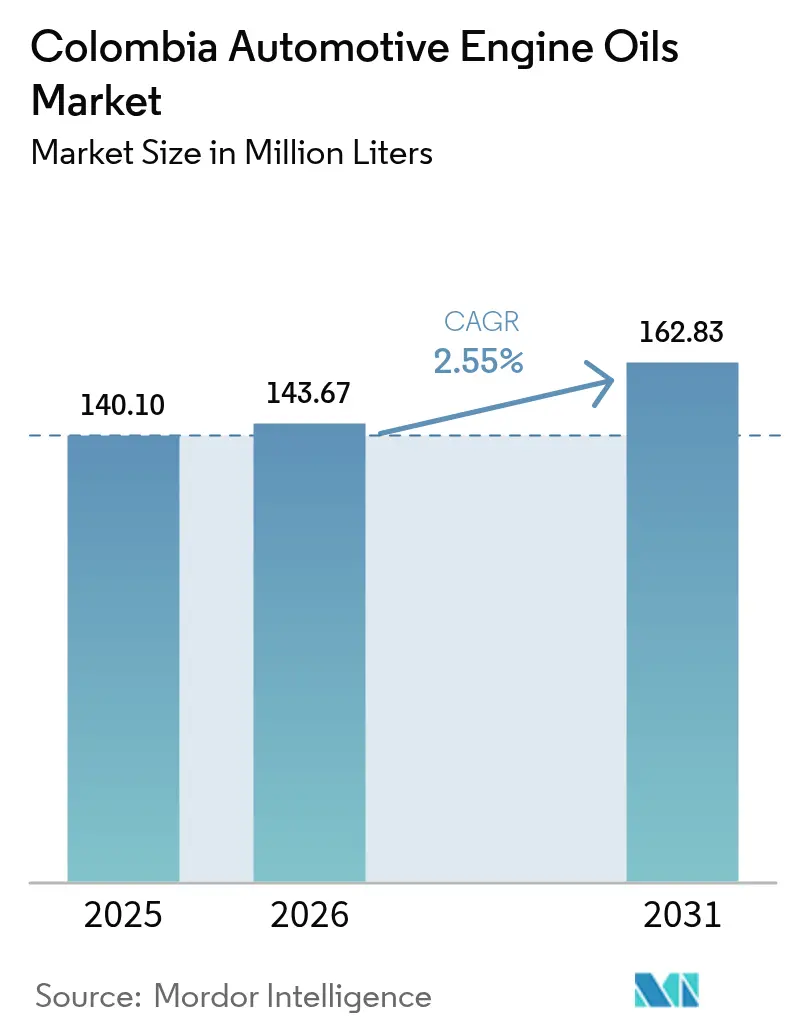

| Base Year Market Size (2025) | 140.10 Million Liters |

| Market Volume (2026) | 143.67 Million Liters |

| Market Volume (2031) | 162.83 Million Liters |

| Growth Rate (2026 - 2031) | 2.55% CAGR |

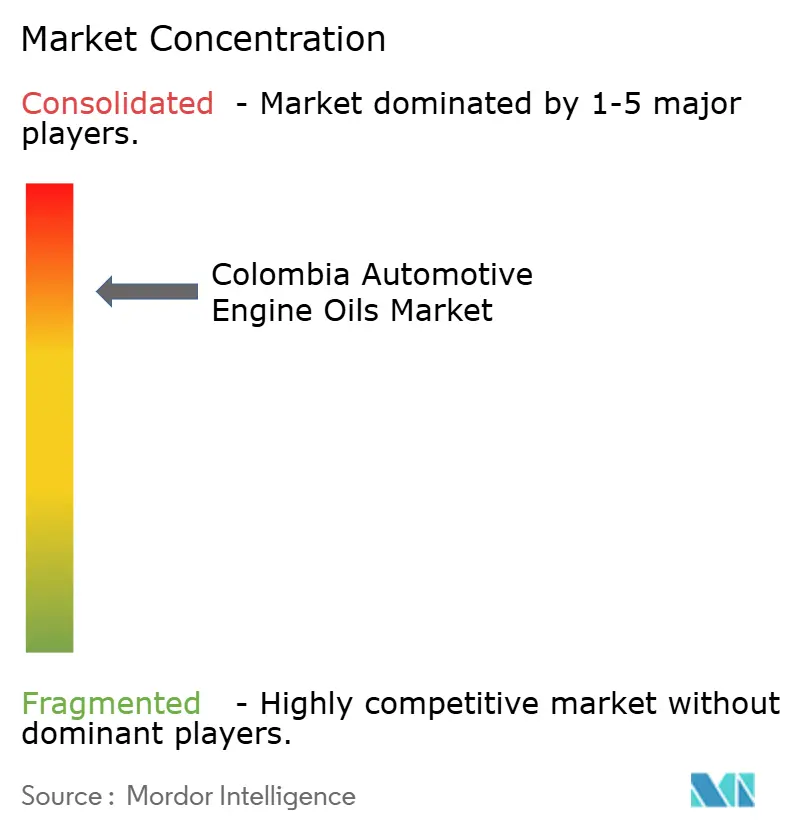

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Colombia Automotive Engine Oils Market Analysis by Mordor Intelligence

The Colombia Automotive Engine Oils Market size was valued at 140.10 million liters in 2025 and estimated to grow from 143.67 million liters in 2026 to reach 162.83 million liters by 2031, at a CAGR of 2.55% during the forecast period (2026-2031). This growth trajectory is shaped by the motorcycle-centric mobility boom, gradual electrification of commercial fleets, and peso depreciation that extends vehicle replacement cycles and sustains lubricant consumption[1]Ministerio de Transporte, “Colombia firma la Declaración de Vehículos de Cero Emisiones (ZEV),” mintransporte.gov.co . Demand patterns diverge across passenger car motor oil, heavy-duty motor oil, and motorcycle engine oil, with motorcycle registrations up 35.32% year over year in October 2024. Base-stock preferences remain skewed toward mineral formulations even as OEMs specify low-viscosity synthetics for fuel-efficiency gains. Consolidation activity, exemplified by Saudi Aramco’s USD 3.5 billion acquisition of Primax’s Colombian network, intensifies competitive pressures and underscores the importance of distribution reach.

Key Report Takeaways

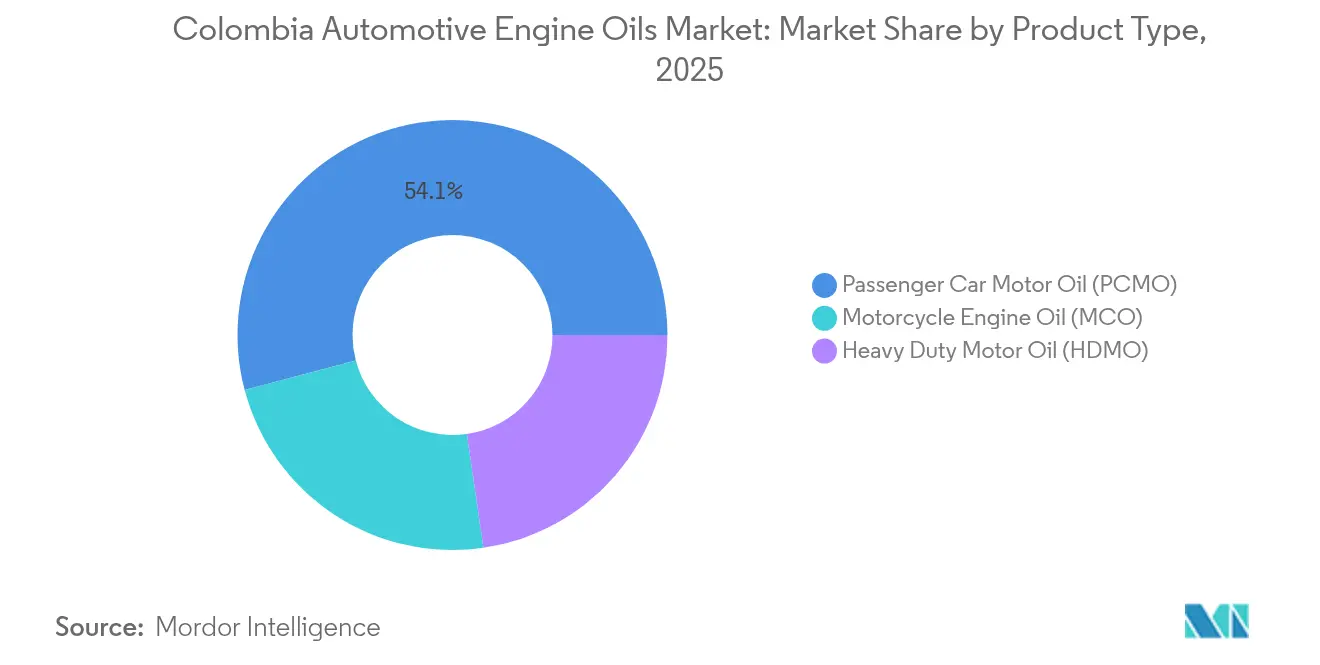

- By product type, passenger car motor oil accounted for 54.12% of the Colombia automotive engine oils market share in 2025, while motorcycle engine oil is forecast to expand at a 2.74% CAGR through 2031.

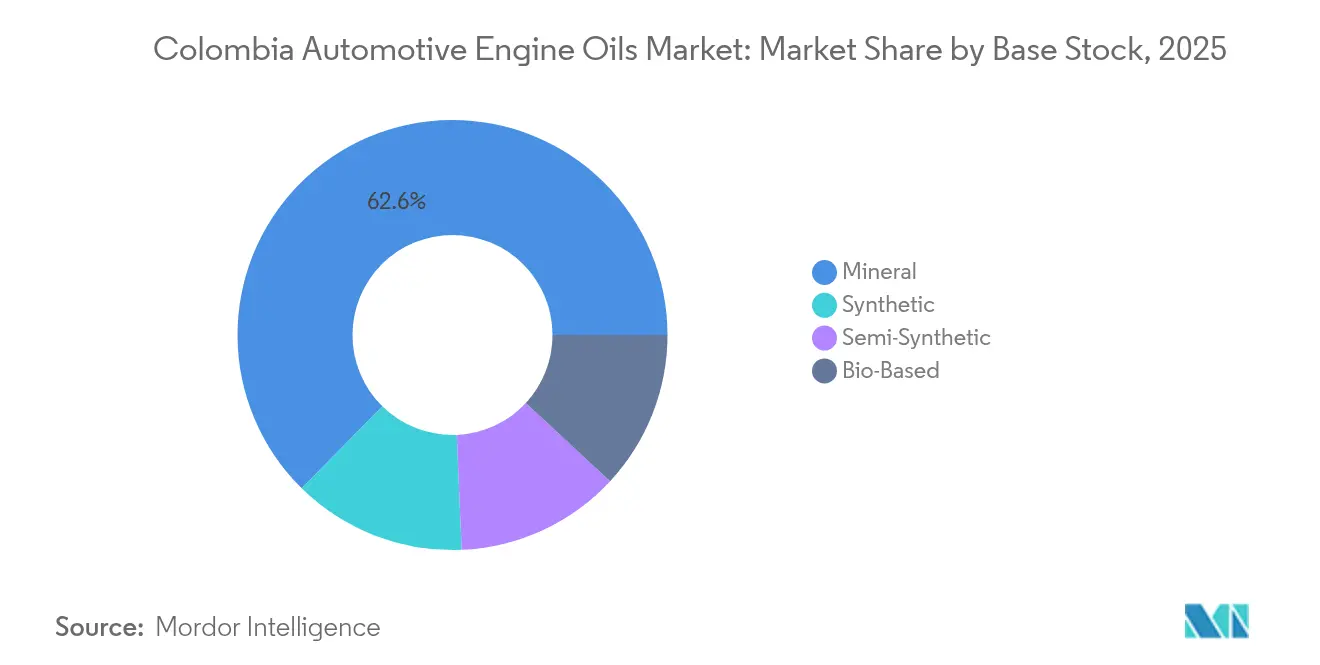

- By base stock, mineral formulations held 62.63% of the Colombia automotive engine oils market size in 2025; synthetic variants are projected to grow at a 2.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Colombia Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Motorcycle-centric mobility boom | +0.80% | Bogotá, Medellín, Cali corridors | Medium term (2-4 years) |

| Aging passenger-car and light-truck parc | +0.60% | Nationwide; stronger in secondary cities | Long term (≥4 years) |

| Expansion of quick-lube and retail chains | +0.40% | Major urban centers | Medium term (2-4 years) |

| OEM pivot to low-viscosity synthetics | +0.30% | Nationwide | Long term (≥4 years) |

| SUV & pickup local assembly increasing sump volumes | +0.20% | Manufacturing hubs: Bogotá, Medellín regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Motorcycle-centic Mobility Boom

Motorcycle registrations climbed 16.71% year over year to 658,637 units through October 2024, underscoring a structural shift toward two-wheel mobility in congested cities. The installed base expansion amplifies demand for motorcycle engine oils because service intervals range from 3,000–4,000 km for mineral grades to up to 10,000 km for synthetics under Colombian conditions. Quick-lube operators target this high-frequency maintenance segment, prompting lubricant marketers to tailor pack sizes and additive packages for wet-clutch performance. Extended idling in heavy traffic accelerates thermal degradation, further elevating change frequency. As a result, the Colombia automotive engine oils market experiences volume uplift that offsets slower passenger-car growth.

Aging Passenger-Car and Light-Truck Parc

Peso depreciation and limited inventory inflate new-vehicle prices, pushing consumers to keep older cars longer and escalating oil-change frequency relative to factory recommendations. Vehicles exceeding 10 years dominate secondary cities, where cost sensitivity promotes mineral or semi-synthetic oils. High-viscosity PCMO grades remain prevalent because older engines have broader clearances and higher consumption rates. Service providers leverage the aging parc by bundling oil and filter promotions to capture repeat business. This behavior preserves base volume even as synthetic penetration increases in premium urban fleets, reinforcing resilience in the Colombia automotive engine oils market.

Expansion of Quick-Lube and Retail Chains

Retailers such as Terpel plan 60 new sites, while Coéxito rolls out Energiteca bays that integrate fuel sales with quick-lube services. The standardized model trims service times and elevates product credibility through brand visibility. Urban consumers value convenience, encouraging recurring visits that lift throughput and lubricant pull-through. Franchise formats like Grease Monkey exploit established traffic flows, enabling scale efficiencies in inventory management. Distribution partnerships become decisive as chains mandate assured stock and OEM-approved products, deepening competitive moats for suppliers with robust logistics. These factors buoy annual volumes across the Colombia automotive engine oils market.

OEM Pivot to Low-Viscosity Synthetics

Global emission and fuel-efficiency mandates push automakers to recommend 0W-20 or even 0W-16 grades for import models. Transitioning from 15W-40 to 10W-30 delivers fuel savings near 1% and supports extended drain intervals of 7,000–10,000 km, partially offsetting higher product cost. High retail premiums restrict adoption to warranty-sensitive buyers and fleet operators with total cost-of-ownership metrics, yet gradual penetration improves profitability mix. Blenders respond with semi-synthetic hybrids to bridge cost gaps. As OEMs align Colombian specifications with global platforms, synthetics’ share edges upward, enriching the value pool of the Colombia automotive engine oils market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Taxi and bus electrification programs | -0.30% | Bogotá, Medellín | Medium term (2-4 years) |

| Base-oil price volatility | -0.20% | National | Short term (≤2 years) |

| Informal re-use / extended-drain culture | -0.10% | Rural and secondary urban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Taxi and Bus Electrification Programs

Pilot e-taxi projects in Bogotá and Medellín reveal annual maintenance costs of USD 97 for battery-electric powertrains versus USD 588–619 for internal-combustion equivalents, accelerating adoption in high-utilization fleets. Public-sector procurement guidelines favor zero-emission buses, eroding heavy-duty motor oil volumes in the Colombia automotive engine oils market. Nonetheless, infrastructure gaps and acquisition costs temper the shift, ensuring a prolonged ICE–EV mix. Lubricant marketers explore EV-thermal-management fluids to offset volume attrition. Training programs for mixed fleets create cross-selling moments during the transition period.

Base-Oil Price Volatility

Imported base oils expose local blenders to crude-price swings and currency risk, with Brent projected near USD 73 per barrel through 2026[2]World Bank, “Commodity Markets Outlook,” worldbank.org . Small-scale players face margin squeezes when peso depreciation bumps input costs faster than retail prices. Distributors adjust inventory cycles to hedge exposure, but abrupt pricing shifts can prompt consumers to defer maintenance, briefly denting volume in the Colombia automotive engine oils market. Diverse sourcing from the U.S. Gulf Coast and Caribbean refineries softens single-point disruptions. Larger firms capitalize on volatility through forward-buying strategies, reinforcing competitive hierarchy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Demand Resilience in PCMO Amid Rapid MCO Uptick

Passenger Car Motor Oil anchored 54.12% of the Colombia automotive engine oils market share in 2025, mirroring the entrenched 6.9 million-unit light-vehicle parc. Routine city driving on congested routes accelerates oil oxidation, prompting 6-month change intervals despite OEM guidance on extended drains. Mineral 10W-30 and 15W-40 grades dominate for vehicles older than 8 years, while 5W-30 synthetics rise in late-model imports. Motorcycle Engine Oil advances at a 2.74% CAGR to 2031, underpinned by sustained two-wheel adoption that multiplies oil events. Motorcycles average 8,000 km annually and demand formulations compatible with wet clutches and air-cooled engines. HDMO remains steady as freight activity grows around logistical hubs, yet faces gradual displacement from urban bus electrification. Altogether, these forces preserve diversified demand within the Colombia automotive engine oils market and create channel-specific opportunities for bundled service offerings.

Widening viscosity spectrum within PCMO illustrates OEM divergence: turbocharged gasoline direct-injection engines favor 0W-20 synthetics for piston deposit control, whereas legacy engines persist with 20W-50 monogrades in budget-sensitive regions. The Colombia automotive engine oils market size for PCMO is forecast to rise modestly, buoyed by aftermarket promotions in quick-lube chains. MCO gains share through sachet packs tailored to daily commuters. Advanced additive chemistries that manage sludge during repetitive cold-start cycles receive growing attention. The interplay of price sensitivity and performance expectations guides product tiering, ensuring overlapping mineral, semi-synthetic, and synthetic sub-segments that cater to distinct consumer cohorts in urban and peri-urban areas.

By Base Stock: Mineral Majority Holds as Synthetics Strengthen Value Mix

Mineral oils retained a 62.63% share of the Colombia automotive engine oils market size in 2025, a testament to affordability in a price-conscious landscape. Semi-synthetic blends bridge cost and performance, capturing incremental upgrades from consumers influenced by OEM endorsements but constrained by budgets. Full synthetics, expanding at 2.86% CAGR, cater to warranty-protected vehicles and fleets seeking longer drain intervals that cut downtime. Resolución 2238 de 2023 mandates used-oil collection targets that favor durable formulations, indirectly accelerating synthetic adoption through lifecycle cost benefits. Bio-based stocks remain experimental but gain interest from sustainability-minded corporate fleets.

Cost premiums, often reaching threefold the mineral benchmark, keep synthetic penetration below 30% in rural and secondary markets. However, bundled service packages at chain garages reduce perceived price gaps by amortizing oil cost across wider maintenance menus. The Colombia automotive engine oils market integrates group II+ and group III imports to formulate low-volatility multi-grades, improving oxidation stability in high-ambient coastal provinces. Strategic alliances with additive suppliers expedite API SQ updates, positioning blenders for incoming specification cycles. Over the forecast horizon, mineral dominance erodes gradually yet continues to provide foundational volume, ensuring balanced growth across the value spectrum.

Geography Analysis

Colombia’s three principal metros—Bogotá, Medellín, and Cali—represent more than half of national consumption because high vehicle density, short trip frequency, and elevation induce accelerated oil aging. Premium synthetics achieve double-digit penetration in these markets thanks to franchised service chains that educate consumers on extended drains. Traffic congestion leads to average driving speeds below 25 km per hour, magnifying idling and thermal stress that shorten oil life and heighten purchase frequency.

Secondary cities such as Barranquilla, Bucaramanga, and Pereira exhibit different dynamics where the Colombia automotive engine oils market maintains mineral predominance. Here, prolonged vehicle ownership periods and informal workshop networks cultivate demand for budget-focused formulations sold in bulk drums or five-liter canisters. Distribution relies on regional wholesalers capable of navigating mountainous roadways that inflate transport costs. Suppliers with localized depots outperform import-dependent rivals during peak harvest seasons when road congestion intensifies lubricants’ last-mile challenges.

The Caribbean coastal belt experiences average ambient temperatures exceeding 30 °C, making volatility control and oxidation stability critical formulation parameters. Meanwhile, Andean highlands impose altitude-related stress that necessitates optimized detergency to counter incomplete combustion. National regulations on used-oil recovery, carbon pricing under the PNCTE, and EV adoption targets converge across regions, prompting blenders to promote circular-economy solutions that reinforce brand equity. Collectively, these geographic variances ensure nuanced demand profiles that preserve balance within the Colombia automotive engine oils market.

Competitive Landscape

The Colombia automotive engine oil is consolidated, with Terpel leveraging its fueling network to dominate packaged-oil distribution and command shelf visibility across 2,400 service stations. Saudi Aramco’s acquisition of Primax’s 914 stations extends vertical integration and injects a new global entrant armed with proprietary base oils, intensifying bargaining dynamics along the supply chain. International majors—Shell, ExxonMobil, and Chevron—retain brand equity through OEM approvals and technical training while partnering with local bottlers to mitigate logistics risk.

Domestic companies such as Coéxito, Biomax, and Petromil differentiate through agile regional distribution and culturally attuned marketing. Fuchs’s joint venture expansion into neighboring Peru signals ambitions for Andean synergy, foreshadowing cross-border competition in Colombia. Product innovation accelerates around low-SAPs additive packages and EV thermal-fluid lines, areas where early mover status confers OEM recommendation advantages. Marketing spends pivot toward digital channels that resonate with younger motorcycle owners.

Distribution alliances with quick-lube chains become pivotal because standardized service protocols favor single-brand supply contracts. Suppliers offering comprehensive technical support, used-oil collection programs, and lubricant-related training gain preferential access. While price sensitivity persists, rising synthetic uptake lifts average revenue per liter, enriching margins. These vectors collectively shape a dynamic yet orderly Colombia automotive engine oils market that rewards scale, technical acumen, and network depth.

Colombia Automotive Engine Oils Industry Leaders

BP p.l.c.

Chevron Corporation

Shell plc

Terpel

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Effective May 31, 2025, the American Petroleum Institute's API SQ standard came into force. LIQUI MOLY has updated several products from its Special Tec AA and Molygen New Generation series. These engine oils, primarily designed for American and Asian vehicles, now comply with the latest API SQ requirements.

- April 2024: Shell Lubricants has unveiled three new products under its flagship Shell Helix Ultra brand, catering to enhanced industry standards and original equipment manufacturer (OEM) specifications, empowering customers to harness greater engine performance.

Colombia Automotive Engine Oils Market Report Scope

By Product Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

Key Questions Answered in the Report

How large is the Colombia automotive engine oils market in 2026?

It reached 143.67 million liters in 2026 and is projected to grow at a 2.55% CAGR to 2031.

Which product segment leads lubricant demand in Colombia?

Passenger Car Motor Oil retained leadership with 54.12% share in 2025, driven by the sizable light-vehicle fleet.

What is the fastest-growing segment in the country?

Motorcycle Engine Oil is forecast to expand at 2.74% CAGR through 2031, reflecting sustained two-wheel adoption.

How are mineral and synthetic oils positioned?

Mineral oils still dominate at 62.63%, but synthetics are growing 2.86% annually due to OEM fuel-efficiency requirements.

Which regions consume the most engine oil?

Bogotá, Medellín, and Cali account for the bulk of demand because of dense traffic and frequent maintenance cycles.

How is electrification affecting lubricant sales?

Taxi and bus electrification trims heavy-duty volumes, but overall impact remains modest as EV parc penetration is still low.

Page last updated on: