Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

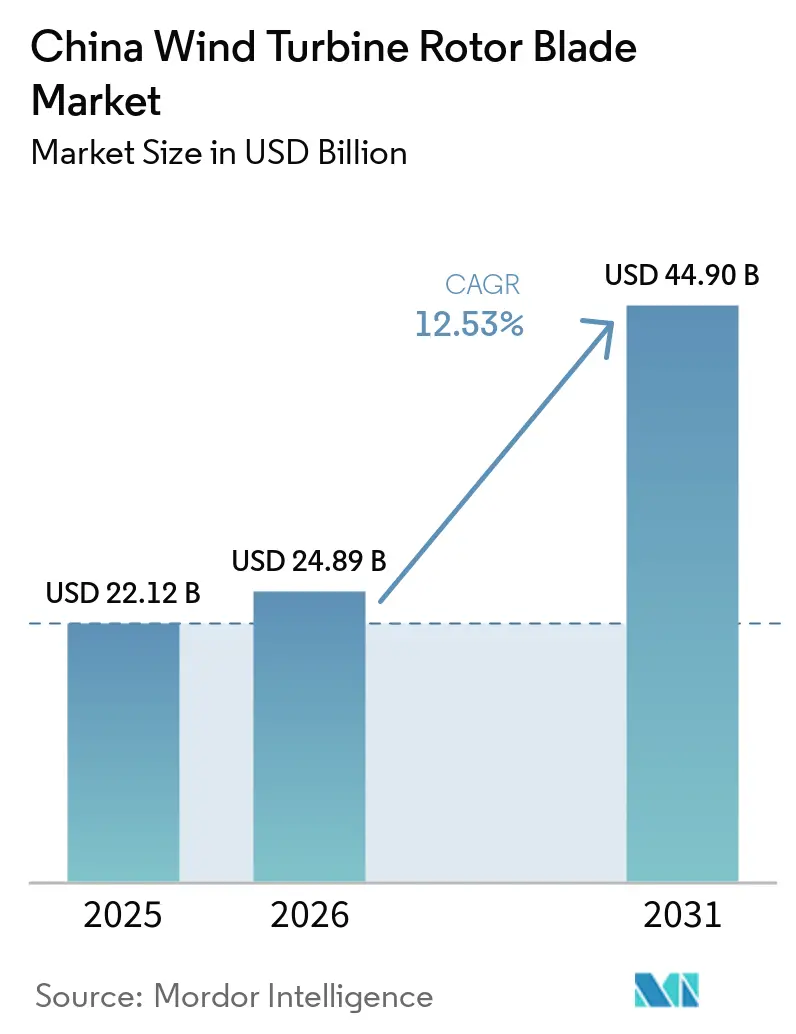

| Base Year Market Size (2025) | USD 22.12 Billion |

| Market Size (2026) | USD 24.89 Billion |

| Market Size (2031) | USD 44.90 Billion |

| Growth Rate (2026 - 2031) | 12.53% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Wind Turbine Rotor Blade Market Analysis by Mordor Intelligence

The China Wind Turbine Rotor Blade Market size was valued at USD 22.12 billion in 2025 and estimated to grow from USD 24.89 billion in 2026 to reach USD 44.9 billion by 2031, at a CAGR of 12.53% during the forecast period (2026-2031).

A nationwide push toward carbon neutrality by 2060, a forecast of 140 GW of new wind additions in 2025, and fast-rising average rotor diameters are the primary growth catalysts. The aggressive repowering of 2010-era turbines, rapid coastal and offshore build-outs, and continuous cost declines in longer hybrid blades collectively reinforce demand. Tight local competition encourages automation, while digital-twin strategies are extending asset life and lowering levelized costs. Supply-chain volatility around epoxy resins and PET foam, alongside ongoing curtailment risks in the Three-North region, tempers near-term margins but also accelerates material innovation and grid-integration solutions.

Key Report Takeaways

- By location of deployment, onshore installations held 92.12% of the China wind turbine rotor blade market share in 2025 and are expected to grow at a 13.05% CAGR through 2031.

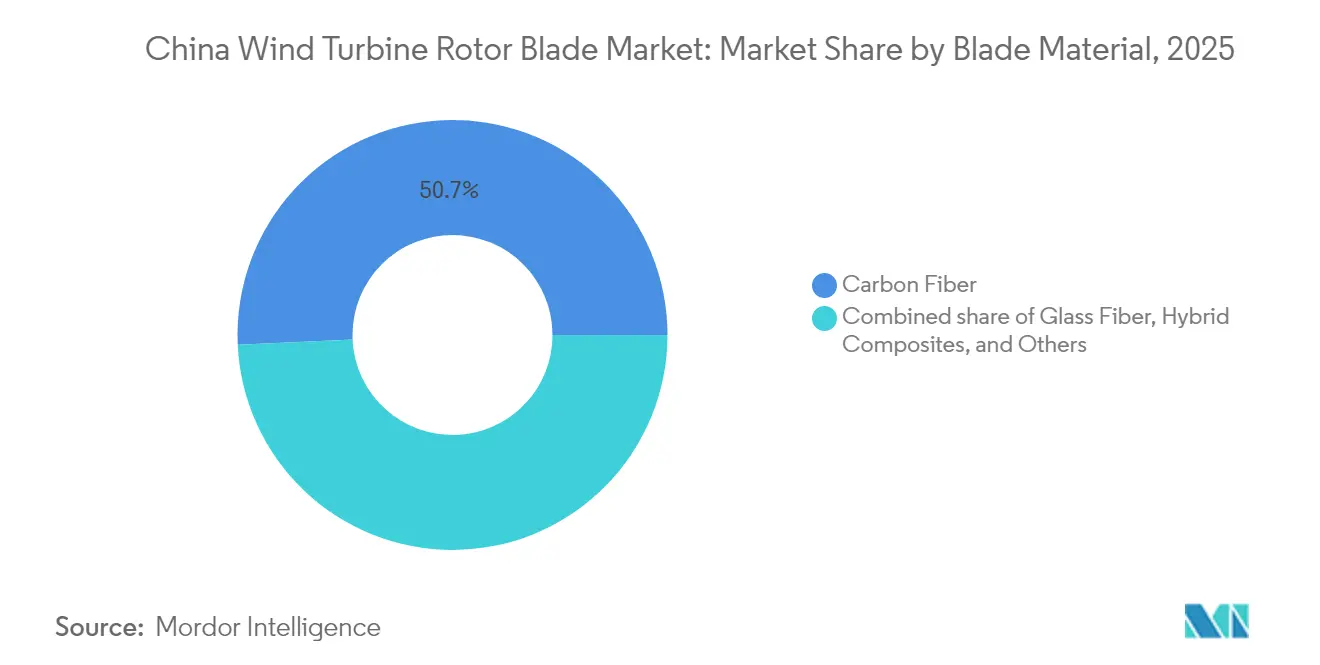

- By blade material, carbon fiber captured a 50.72% revenue share in 2025, whereas hybrid composites are poised for the fastest growth, with a 13.28% CAGR through 2031.

- By blade length, the 61–75 m segment commanded 46.98% of the China wind turbine rotor blade market size in 2025; however, blades above 75 m are expected to surge at a 14.18% CAGR through 2031.

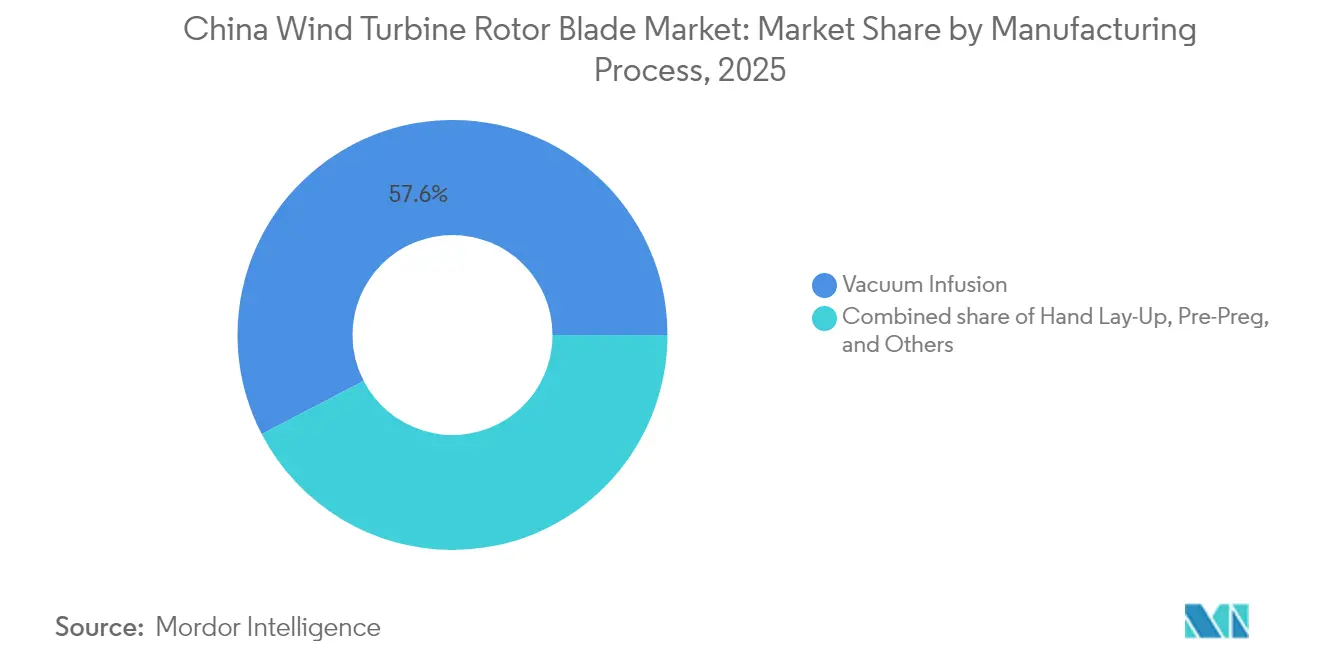

- By manufacturing process, vacuum infusion led with a 57.62% share in 2025, while pre-preg techniques are projected to post a 12.87% CAGR to 2031.

- Goldwind, Envision, and Mingyang jointly exceeded 50% domestic installations in 2024, underscoring a highly concentrated competitive arena

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Wind Turbine Rotor Blade Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ambitious 2030 wind-power capacity targets | 2.80% | Nationwide; strongest in Three-North region | Long term (≥ 4 years) |

| Cost decline in > 80 m carbon-glass hybrid blades | 2.10% | Jiangsu, Guangdong export hubs | Medium term (2-4 years) |

| Rapid offshore build-out along coastal provinces | 1.90% | Jiangsu, Guangdong, Zhejiang | Medium term (2-4 years) |

| Accelerating replacement of 2010-era onshore turbines | 1.70% | Inner Mongolia, Xinjiang clusters | Short term (≤ 2 years) |

| Commercialisation of pultrusion-based blade lines | 1.40% | Eastern China manufacturing belts | Medium term (2-4 years) |

| Digital-twin enabled life-extension models | 1.20% | Large national wind farms | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ambitious 2030 Wind-Power Capacity Targets

China plans to hit 400 GW of cumulative wind by 2030, with 140 GW slated for 2025 alone. This policy certainty drives the long-term procurement of ever-larger rotors, 58.6% of which now exceed 180 m in diameter.[1]Global Wind Energy Council, “Global Wind Report 2025,” gwec.net Grid-parity objectives force OEMs to optimize blade aerodynamics for diverse inland and coastal conditions. Consistent government backing sustains capital inflows into new blade factories, sparking technology upgrades that keep the Chinese wind turbine rotor blade market on a steep growth curve.

Cost Decline in > 80 m Carbon-Glass Hybrid Blades

Hybrid composites reduce blade weight by 38% and costs by 14% compared to glass-only designs, while maintaining stiffness.[2]Advanced Materials Research, “Hybrid Composite Blades for Offshore Wind,” advancedmaterials.org Automated fiber placement and thermoplastic processing now enable serial manufacture, anchoring China’s leadership in blades exceeding 80 m in length for offshore use. Local suppliers of polyurethane resin systems are strengthening hybrid adoption, pushing the China wind turbine rotor blade market toward lightweight, high-performance solutions suited for 16 MW-class turbines.

Rapid Offshore Wind Build-Out Along Coastal Provinces

Jiangsu already hosts 55% of national offshore capacity, and the 800 MW Dafeng deep-sea array became China’s farthest offshore project in 2025. Coastal incentives and reduced transmission losses encourage the use of larger rotors to harness stable marine winds, thereby increasing blade demand. Government estimates indicate that offshore resources could yield over 1,000 TWh annually, accounting for a third of coastal electricity needs. These factors collectively propel the China wind turbine rotor blade market deeper into high-margin offshore segments.

Accelerating Replacement of 2010-Era Onshore Turbines

Early-generation ≤ 2 MW machines with ≤ 45 m blades are financially outclassed by today’s > 5 MW, 150 m-rotor units. Operators leverage existing grid links to repower, multiplying site output without new land acquisitions. Warranty expirations and high O&M costs heighten urgency, channeling orders into modern blades and boosting near-term revenue in the China wind turbine rotor blade market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile epoxy & PET foam prices squeezing margins | -1.80% | Eastern China composites clusters | Short term (≤ 2 years) |

| Grid curtailment risk in Northern bases | -1.50% | Gansu, Xinjiang, Inner Mongolia | Medium term (2-4 years) |

| Stricter land-use & ecological approvals | -1.20% | Environmentally sensitive zones nationwide | Long term (≥ 4 years) |

| Shortage of skilled composites technicians | -0.90% | Jiangsu, Guangdong, Shandong | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Epoxy & PET Foam Prices Squeezing Margins

Shift from scarce balsa to PET foam magnifies exposure to petrochemical swings; resin spikes already compress OEM margins by up to 3 percentage points.[3]United States International Trade Commission, “PET Foam Supply Chain Trends,” usitc.gov Currency shifts and import tariffs complicate budgeting, compelling supply-chain diversification and trials of bioplastics, also known as bio-resins. Price pass-through is limited amid cut-throat turbine bidding, keeping profitability pressure high across the Chinese wind turbine rotor blade market.

Grid Curtailment Risk in Northern China Wind Bases

Curtailment once topped 47% in Gansu, eroding ROI for new blades despite recent UHV line progress.[4]Energy Policy Journal, “Curtailment and Market Reforms in Northwest China,” energypolicy-journal.org Spot-market reforms improved utilization by 26.8% in Northwest China; however, seasonal oversupply still poses a threat to cash flows. Storage projects and cross-provincial trading are crucial for locking in demand and safeguarding growth in the Chinese wind turbine rotor blade market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location of Deployment: Onshore Repowering Steers Near-Term Volume

Onshore blades contribute 92.12% of 2025 installations and are projected to log a 13.05% CAGR to 2031, driven by large-scale repowering that rapidly expands the China wind turbine rotor blade market size for this segment. Fleet owners in Inner Mongolia and Xinjiang swap out sub-2 MW units for modern 5 MW designs that increase site yields by more than 70%

Latest province-level auctions include strict LCOE caps, prompting OEMs to opt for longer rotors to maximize megawatt-hours within fixed tariffs. Enhanced aerodynamics and hybrid materials keep nacelle mass in check, ensuring logistics feasibility across rugged inland transport routes. The result is a virtuous cycle of capacity factor gains and declining costs that entrenches onshore leadership in the Chinese wind turbine rotor blade market.

Offshore arrays, though smaller today, represent the fastest-growing slice, adding more than 10 GW annually after 2025. Jiangsu’s deep-sea sites pioneered 240-m rotor trials in 2025, signalling future procurement of extra-long, splash-zone-resistant blades. Floating foundations under test in Fujian could unlock Southern deep-water zones, expanding geographical diversity and boosting the overall China wind turbine rotor blade market.

By Blade Material: Hybrids Challenge Carbon Fiber Dominance

Carbon fiber’s 50.72% share stems from its stiffness-to-weight edge, especially for > 10 MW offshore machines. Yet, hybrids will see a 13.28% CAGR to 2031 and could overtake carbon by volume before 2032, reshaping the China wind turbine rotor blade market share landscape.

Producers blend carbon unis with glass fabrics, lowering cost while retaining critical bending stiffness. Thermoplastic resins make large-part recycling feasible, aligning with China’s 2030 circular-economy standards. Hybrids thus bridge the cost and sustainability gap, widening the addressable demand and anchoring market expansion.

By Blade Length: Above 75 m Category Sets the Pace

The 61–75 m class holds 46.98% share, but blades above 75 m are advancing at 14.18% CAGR, the strongest of any segment. This length class anchors 16 MW offshore turbines and next-generation 8 MW onshore units, which drive down LCOE by capturing steadier, high-altitude winds.

Logistics constraints on road transport are driving the development of modular blade concepts, which ease last-mile delivery to remote mountain sites while sustaining the China wind turbine rotor blade market for ultra-long products. Specialized rail and river-barge corridors further enhance growth prospects for the category, exceeding 75 m.

By Manufacturing Process: Pre-Preg Gains Traction Amid Automation

Vacuum infusion’s 57.62% share reflects mature workflows and moderate capex. Pre-preg, growing at 12.87% annually, couples automated layup with low void content, which is crucial for fatigue life in duty cycles exceeding 20 years offshore.

Pultrusion of spar caps and shear webs cuts resin wastage and supports serial production, enhancing throughput in plants targeting 6,000 blade sets per year. Integrated digital twins detect defects in situ, reducing rework and supporting cost competitiveness throughout the Chinese wind turbine rotor blade industry.

Geography Analysis

The Three-North region still accounts for over 60% of cumulative installations and remains central to the China wind turbine rotor blade market; however, curtailment and harsher climates mean growth rates trail the national average. Ultra-high-altitude sites in Tibet went online at 4,650 m in 2024 and require custom low-temperature resin systems that widen technological niches.

Coastal provinces, particularly Jiangsu, dominate offshore capacity and are home to dense manufacturing clusters. Proximity between plants and ports reduces transport risk for blades exceeding 100 m. Guangdong and Zhejiang augment demand with generous feed-in premiums and streamlined approvals, underpinning double-digit regional CAGR.

Central and Eastern provinces, such as Shandong, strike a balance between inland and coastal advantages. Mature rail links feed export shipments, making Shandong a pivotal hub for international blade orders that broaden the addressable China wind turbine rotor blade market beyond domestic needs. Improved inter-provincial power trading further incentivizes developers to site new projects where grid stability and load proximity coincide.

Competitive Landscape

China Wind Turbine Rotor Blade Market is moderatly consolidated. Direct control of blade factories ensures alignment with rapid product-upgrade cycles, reinforces IP protection, and compresses procurement timelines in the Chinese wind turbine rotor blade market.

Independent blade suppliers respond by specializing in hybrid materials, thermoplastic designs, and circular-economy recycling. The adoption of pultrusion and automated sanding lines cuts labor per blade by up to 30%, preserving margins amid fierce price competition.

Global expansion remains strategic. Chinese OEMs installed 94% of their turbines domestically in 2024 but began shipping complete rotor sets to South America and the MENA region in 2025, diversifying revenue and reducing policy risk. Partnerships with European composites firms accelerate accreditation for international safety standards, cementing China’s role as a global supply center for advanced blades.

China Wind Turbine Rotor Blade Industry Leaders

Lianyungang Zhongfu Lianzhong Composites Group Co. Ltd

Sinoma wind power blade Co. Ltd

Zhuzhou Times New Material Technology Co., Ltd

Tianshun Wind Energy (Suzhou) Co., Ltd.

LM Wind Power (GE Renewable Energy)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: NEA released the 2024 Wind & Solar Resource Report showing > 300 W/m² mean wind density across Heilongjiang, Jilin, and Inner Mongolia.

- July 2024: NEA forecasts 140 GW of 2025 wind additions, a 77.1% annual jump.

- June 2024: Gurit signed a CHF 25 million PET core supply deal with a Chinese blade maker, underlining PET’s ascendancy.

- May 2024: Chinese OEMs led global turbine orders with Goldwind at 17.7%, Envision at 17.4% and Mingyang at 16.1%.

China Wind Turbine Rotor Blade Market Report Scope

Wind turbine rotor blades are the key components of wind turbines, as they are in direct contact with high-speed winds. Rotor blades convert the wind's kinetic energy into rotational energy, which is later converted into electrical energy.

China's wind turbine rotor blade market is segmented by location of deployment and blade material. By location of deployment, the market is segmented into onshore and offshore; by blade material, the market is segmented by carbon fiber, glass fiber, and other blade materials. For each segment, the market sizing and forecasts have been done based on revenue (USD Billion).

By Location of Deployment

| Onshore |

| Offshore |

By Blade Material

| Glass Fiber |

| Carbon Fiber |

| Hybrid Composites |

| Others |

By Blade Length

| Below 45 m |

| 46 to 60 m |

| 61 to 75 m |

| Above 75 m |

By Manufacturing Process

| Hand Lay-Up |

| Vacuum Infusion |

| Pre-Preg |

| Others |

| By Location of Deployment | Onshore |

| Offshore | |

| By Blade Material | Glass Fiber |

| Carbon Fiber | |

| Hybrid Composites | |

| Others | |

| By Blade Length | Below 45 m |

| 46 to 60 m | |

| 61 to 75 m | |

| Above 75 m | |

| By Manufacturing Process | Hand Lay-Up |

| Vacuum Infusion | |

| Pre-Preg | |

| Others |

Key Questions Answered in the Report

What is the current size of the China Wind Turbine Rotor Blade Market?

The China Wind Turbine Rotor Blade Market is valued at USD 24.89 billion in 2026 and is projected to reach USD 44.9 billion by 2031, registering a compound annual growth rate (CAGR) of 12.53% during the forecast period (2026-2031).

How does China's position in the global wind market influence the rotor blade market?

China dominates the global wind market, with Chinese OEMs achieving unprecedented market leadership in 2024, installing over 127 GW of new capacity worldwide. Chinese manufacturers now represent six of the top ten global turbine manufacturers, with 94% of installations occurring in the domestic market, creating substantial demand for rotor blades.

Which deployment segment dominates the market?

The onshore segment commands 92.12% market share in 2025 while simultaneously representing the fastest-growing deployment category at 13.05% CAGR through 2031. This reflects both massive installed base expansion and accelerating turbine replacement cycles.

How is automation impacting blade manufacturing?

Automation is revolutionizing blade production through advanced techniques like automated fiber placement, thermoplastic tape winding, and integrated digital quality control systems. This addresses labor shortages while improving quality consistency and reducing production costs.

How will recycling and sustainability impact the market?

China's proposed recycling standards targeting 35 million tonnes of waste by 2030 will create new market segments for blade recycling and repurposing technologies. This represents both a challenge for waste management and an opportunity for companies developing circular economy solutions.

Page last updated on: