China Pouch Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 6.20 Billion |

| Market Size (2026) | USD 6.53 Billion |

| Market Size (2031) | USD 8.44 Billion |

| Growth Rate (2026 - 2031) | 5.28% CAGR |

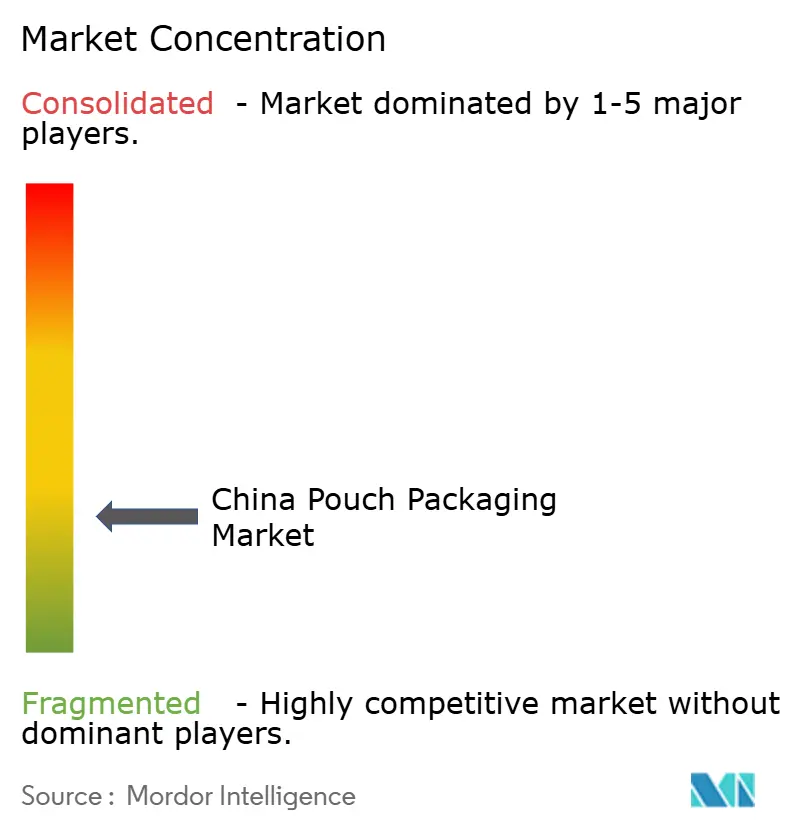

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Pouch Packaging Market Analysis by Mordor Intelligence

The China pouch packaging market size was valued at USD 6.20 billion in 2025 and estimated to grow from USD 6.53 billion in 2026 to reach USD 8.44 billion by 2031, at a CAGR of 5.28% during the forecast period (2026-2031). This steady ascent is propelled by China’s vibrant e-commerce ecosystem, tighter regulatory baselines for packaging safety, and rapid uptake of automation-ready flexible formats across food, beverage, and personal care verticals. Policymakers are driving material innovation through higher tariffs on polyvinyl chloride, fresh mandates on express-parcel packaging, and simplified cosmetic-ingredient approvals that expand premium pouch demand. Brand owners, meanwhile, are adopting mono-material polyethylene constructions to meet plastic-waste targets without sacrificing barrier performance. Tight profit margins in polyethylene and polypropylene value chains are spurring converters to upgrade equipment for efficiency gains and diversify into paper-based or bio-based substrates. Investments in post-consumer recycling infrastructure, alongside rising middle-class spending on premium foods, beverages, and cosmetics, reinforce the growth runway for the China pouch packaging market through 2030.

Key Report Takeaways

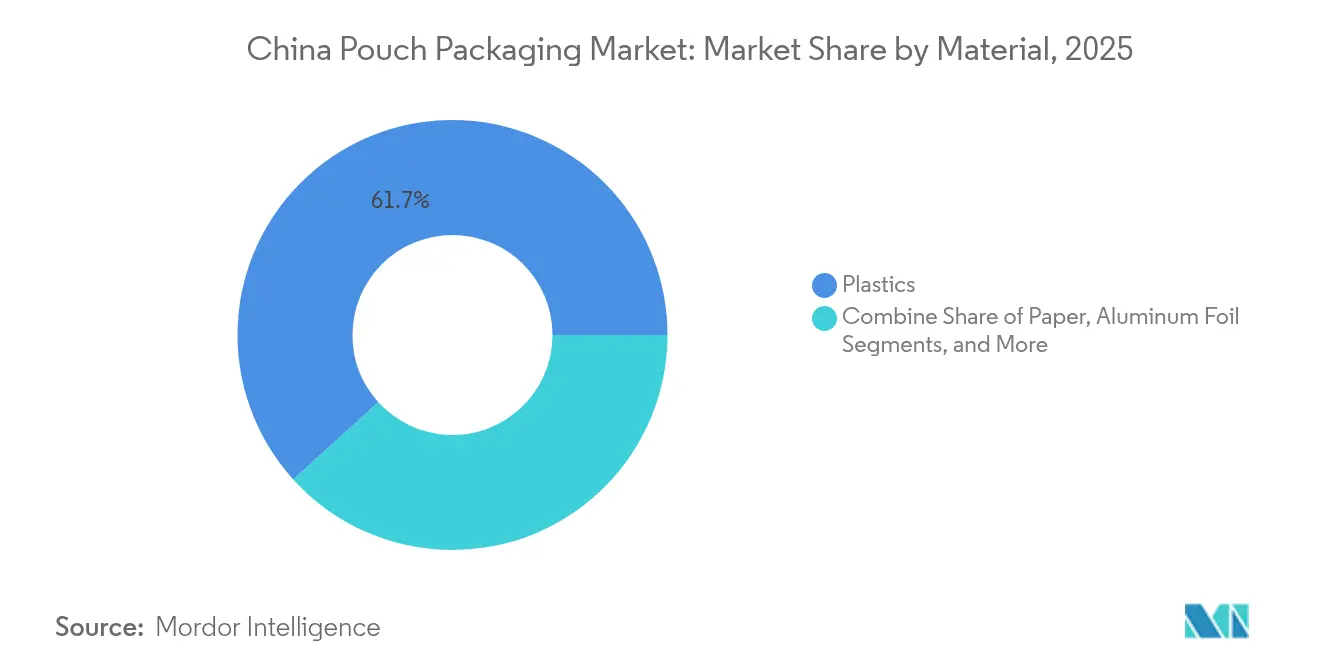

- By material, plastics led with 61.72% revenue share in 2025; paper-based formats are poised to expand at an 8.21% CAGR through 2031.

- By product type, flat pouches held 34.89% of the China pouch packaging market share in 2025, while stand-up versions record the fastest 7.12% CAGR to 2031.

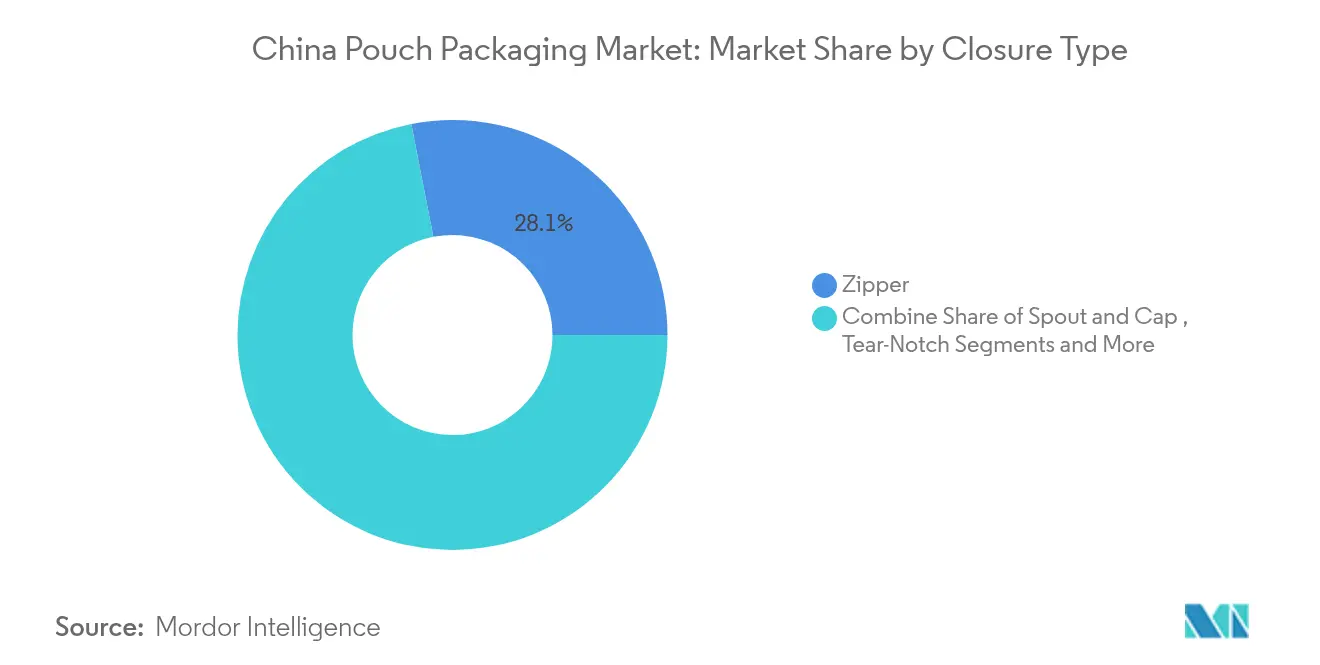

- By closure type, zipper systems accounted for 28.07% revenue in 2025; spout & cap solutions are advancing at a 9.01% CAGR.

- By end-user industry, food applications captured 39.74% revenue in 2025; personal care & cosmetics post the highest 8.07% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Companies active in China may frequently operate across several geographies, linking regional presence to global strategy. Mordor Intelligence captures the entire market landscape of the global pouch packaging industry and how these positions are distributed.

China Pouch Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth in Fresh-Food E-commerce Requiring High-Barrier Stand-Up Pouches | +1.2% | National, with concentration in Tier 1-2 cities | Medium term (2-4 years) |

| Government Plastic-Waste Mandates Accelerating Shift to Mono-Material Recyclable PE Pouches | +0.8% | National, with stricter enforcement in Eastern provinces | Long term (≥ 4 years) |

| Explosion of Domestic RTD Beverage Brands Adopting Spouted Pouches in Lower-Tier Cities | +0.9% | Lower-tier cities and rural markets | Short term (≤ 2 years) |

| Expansion of Pet-Food Manufacturing Capacity Driving High-O₂-Barrier Retort Pouch Demand | +0.6% | National, with manufacturing hubs in Shandong and Guangdong | Medium term (2-4 years) |

| OTC Pharma Shift to Child-Resistant Zipper Pouches under Revised NMPA Guidelines | +0.5% | National, with focus on urban pharmaceutical distribution | Medium term (2-4 years) |

| "Sachet Economy" in Rural Markets Boosting Sub-100 ml Stick Pouch Volumes | +0.5% | Rural markets and lower-tier cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Growth in Fresh-Food E-commerce Requiring High-Barrier Stand-Up Pouches

Online grocery adoption is escalating, and retailers expect pouches that survive automated sortation, thermal swings, and last-mile handling while preserving shelf appeal on mobile apps. Suppliers are therefore deploying nano-coating and plasma-treatment lines to drive oxygen-transmission rates below 0.3 cc/m²-day, a benchmark once limited to rigid formats. The shift is nudging the China pouch packaging market toward higher-margin, multilayer high-barrier structures and accelerating investment in digital-printing assets that support short runs demanded by e-commerce promotions.

Government Plastic-Waste Mandates Accelerating Shift to Mono-Material Recyclable PE Pouches

China’s Ministry of Ecology and Environment now requires phased reductions of single-use plastics, spurring brands to adopt easy-to-recycle polyethylene laminates. Amcor’s pledge to deliver 100% recyclable or reusable packaging by 2025 underscores the scale of reform sweeping the China pouch packaging market. Polyolefin-only laminates also sidestep rising nylon prices tied to tariff changes. Adoption is strongest in coastal economic belts, where local governments offer recycling subsidies and waste-sorting enforcement. Converted volumes of mono-PE pouches rose double digits in 2024 despite margin pressure, highlighting the structural pull of sustainability regulation.

Explosion of Domestic RTD Beverage Brands Adopting Spouted Pouches in Lower-Tier Cities

Energy-drink leader Eastroc logged 32.42% sales growth in 2024 on the back of its 4 million-outlet network. [1]FoodTalks, “Eastroc Beverage Growth Story,” foodtalks.cn Emerging beverage challengers mirror this momentum by standardizing on spouted pouches, whose lighter weight cuts logistics costs up to 55% against PET bottles. Unit pack sizes of 200–350 ml hit affordability thresholds in lower-tier cities while signaling premium cues through matte films and holographic inks. For the China pouch packaging market, this trend is catalyzing equipment upgrades for spout insertion and cap welding, with line speeds climbing beyond 200 ppm to meet promotional spikes.

Expansion of Pet-Food Manufacturing Capacity Driving High-O₂-Barrier Retort Pouch Demand

Domestic wet-pet-food value reached USD 3 billion in 2024 and is projected to rise at double-digit rates, buoying retort pouch consumption. [2]FoodTalks, “Eastroc Beverage Growth Story,” foodtalks.cn Processors require multilayer laminates able to withstand 121 °C sterilization while curbing oxygen ingress to under 0.1 cc/m²-day. Laminators are adopting alu-foil replacements that pair EVOH with vacuum-deposited SiOx to trim weight and align with recyclable-ready directives. These technical gains are setting new benchmarks within the China pouch packaging market for high-moisture, shelf-stable foods.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported Resin-Price Volatility (PE and EVOH) | -0.7% | National, with higher impact on coastal manufacturing hubs | Short term (≤ 2 years) |

| Inadequate Curb-Side Collection for Flexibles Limiting Recycling Targets | -0.4% | Urban centers with advanced waste management systems | Long term (≥ 4 years) |

| Rigid Metal Cans Retain Share in Premium Infant-Formula Segment | -0.3% | National, with concentration in premium retail channels | Medium term (2-4 years) |

| Uneven Food-Safety Certification Uptake in Western Provinces | -0.2% | Western provinces with developing regulatory infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Imported Resin-Price Volatility (PE and EVOH)

Ethylene and propylene oversupply has pushed cracker utilization below 80%, yet spot prices swing sharply on global outages and freight spikes. Pouch converters often lock in quarterly contracts only to face margin squeeze when PE or EVOH moves 12–15 % inside a month. Volatility discourages long-term innovation spend in the China pouch packaging market and forces smaller firms into tactical inventory hedging instead of strategic growth.

Inadequate Curb-Side Collection for Flexibles Limiting Recycling Targets

Flexible packaging recycling sits far below the 96.48% recovery rate achieved for PET beverage bottles, hamstrung by limited curb-side collection and sorting lines. E-commerce shippers adopting degradable pouches still struggle to ensure post-use capture. This gap slows the rollout of advanced recycling capacity and dampens the premium consumers will pay for “green” packs across the China pouch packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Plastic Leadership Faces Accelerating Paper Uptake

Plastic laminates generated 61.72% revenue in 2025, underscoring their unmatched barrier control, thermal resistance, and machinability within the China pouch packaging market. Polyethylene underpins most mono-material designs, while polypropylene grades dominate high-temperature and retort applications. EVOH and PVDC tie layers remain standard, though rising tariffs on PVC are prompting down-gauging and coextrusion tweaks to curb cost. Paper-based laminates, albeit at 8.21% CAGR, address omnichannel brands’ drive for a renewable image. Converters apply water-based coatings and dispersion barriers to lift grease and moisture resistance without compromising repulpability. The China pouch packaging market size for paper formats is set to surpass USD 1.12 billion by 2031, a figure that highlights regulators’ and retailers’ aligned push toward responsible sourcing.

Bio-based resins such as PLA and PBAT record sporadic demand tied to local bans on traditional plastics in food-delivery hubs. Projected PBAT capacity of 700,000 t encourages experimental blends combining starch, calcium carbonate, and compatibilizers to hit the mandated 180-day compostability window. Aluminum foil keeps a niche in pharmaceuticals and military rations where ≤ 0.01 cc/m²-day oxygen transmission is non-negotiable. Hybrid metalized or AlOx films broaden barrier options, though recovery streams for these packs remain nascent. Across all substrates, brand owners rely on lifecycle assessments to validate format shifts, embedding long-term momentum into material diversification in the China pouch packaging market.

By Product Type: Stand-Up Pouches Outpace Flat Formats

Flat pouches retained 34.89% share in 2025 thanks to low cost and compatibility with legacy VFFS lines. Yet stand-up designs now grow at 7.12% CAGR as hypermarkets, convenience stores, and livestream hosts showcase 360-degree graphics for impulse-driven snacks and cosmetics. Spouted variants combine controlled dispensing and child safety, carving share in beverage, sauce, and home-care categories. The China pouch packaging market size for spouted stand-ups is projected to climb toward USD 2.11 billion by 2031 on the back of beverage players moving down-pack to 250 ml servings.

Retort pouches, once confined to military meals, expand quickly in premium pet food and ready-meal kits where shelf stability reduces cold-chain spend. Aseptic pouches serve dairy smoothies and soy beverages targeting Gen-Z shoppers who prize portability and QR-code traceability. Stick packs remain vital to the “sachet economy,” enabling single-serve electrolytes, powdered collagen, and instant coffee to penetrate county-level drugstores beyond the reach of urban brands. Rollstock sales grow in parallel as co-packers favor on-line forming for high-volume SKUs, while nutraceutical challengers choose premade pouches to launch campaigns with minimal capex.

By Closure Type: Spouts Rise while Zippers Hold Ground

Zipper closures generated 28.07% of 2025 revenue, favored for cereals, nuts, and frozen foods demanding multiple openings. Premium sliders expand in pet treats and protein powder niches where one-handed resealing commands higher price points. Spout-and-cap solutions, however, accelerate at 9.01% CAGR, led by RTD beverages and ambient yogurt. Machinery vendors respond with servo-driven applicators that integrate ultrasonic welding to minimize leakers at 300 ppm. The China pouch packaging market share for spouted packs is forecast to top 18.45% by 2031 as beverage marketers cut back on HDPE closures.

Tear-notch pouches remain dominant for single-use condiments and health-supplement sachets. The National Medical Products Administration is pushing child-resistant zipper specs into OTC categories, spawning bicolor slider designs and multi-stage opening sequences. Tamper-evident foil seals combined with pressure-sensitive adhesive lines gain traction in snack sticks to counteract pilferage. Across closures, the China pouch packaging market sees brands balancing usability, sustainability, and regulatory compliance in final selection.

By End-User Industry: Personal Care Surges amid Food Dominance

Food retained 39.74% share in 2025, anchored by snack nuts, processed meats, and frozen dumplings. E-grocery adoption demands pouches with anti-fog windows, anti-condensation coatings, and high-definition reverse printing to catch shopper attention on apps. Beverage brands trigger spout growth as they tap price-sensitive audiences in counties under 500,000 residents. Personal care and cosmetics advance at 8.07% CAGR, underpinned by new ingredient allowances that cut launch times by up to 12 months. Sachet samplers support digital-first marketing, while full-size stand-ups house refill packs that align with zero-waste pledges.

Pet-food producers invest in retort and vacuum pouches to extend shelf life and reduce shipping weight. Pharmaceutical players adopt aluminum-free high-barrier laminates to lower carbon footprints without compromising API stability. Home-care SKUs such as laundry pods and refill concentrates turn to ultra-thin PE laminates that curb resin use 20%, signaling fresh savings for the China pouch packaging industry. Collectively, these shifts prepare the sector for diversified demand cycles through 2030.

Geography Analysis

China’s eastern seaboard provinces—Guangdong, Jiangsu, and Zhejiang—account for more than half of flexible-pack output thanks to deep ports, dense supplier ecosystems, and abundant technical labor. Guangdong alone hosts over 1,000 pouch-converting lines, many tied to global brand co-packing contracts. The Yangtze River Delta leads recycling pilots, where Amcor partners with Shanghai waste collectors to trial mono-PE take-back loops.

Lower-tier cities and rural counties log the fastest unit growth as snack and beverage marketers deploy sachet and spouted pouches suited to price-sensitive consumers. Retail chains such as Mingming Henmang, now spanning 14,394 outlets nationwide, depend on lightweight flexible formats to cut inbound freight and speed shelf replenishment. Logistics corridors linking inland hubs to coastal ports upgrade cold-chain capacity, opening fresh produce and dairy pouches to a wider catchment.

Northern clusters anchored in Shandong Province contribute 70% of China’s BPA capacity, offering pouch makers secure access to epoxy resins and specialized coatings. Western provinces lag in food-safety certifications, slowing penetration of high-value pouch applications and compelling converters to provide technical training for local processors. Across all regions, local governments balance economic revitalization with stricter packaging mandates, harmonizing growth prospects for the China pouch packaging market.

The pouch packaging market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as Europe, North America, and Asia, along with detailed country-level analysis for Japan, Vietnam, United Kingdom, Canada, Germany, and France.

Competitive Landscape

The China pouch packaging market shows low concentration, with multinational leaders retaining process know-how in high-barrier extrusion, solvent-free laminating, and in-line digital embellishment. Amcor’s 2025 merger with Berry Global forms a USD 20 billion revenue giant promising USD 650 million in synergies spread across material science, footprint optimization, and automated finishing. Domestic champions leverage cost and proximity to scale volumes for regional snack and condiment brands, often running lower-spec yet highly versatile converting cells.

Strategic moves pivot on vertical integration: UFlex began commercial polyester chip output in Panipat to anchor its BOPET film supply and reduce resin exposure for Chinese clients.Technology partnerships accelerate automation, with Sealed Air bringing 3D right-size packaging lines to Asia Pacific that churn out 1,100 packs per hour, an answer to labor shortages and e-commerce parcel surges. Mondi’s FlexStudios in Shanghai facilitates co-creation sprints where brand, regulator, and converter teams prototype mono-material pouches within days, re-shaping time-to-market norms.

Supply-risk mitigation is another theme: UFlex’s CPP plant launch in Russia and PET facility in Egypt diversifies feedstock sources, shielding Chinese buyers from occasional import bottlenecks. Domestic converters pursue M&A to add barrier-coating, rotogravure, and pouch-making capacity, cementing national champions capable of challenging foreign incumbents in premium niches of the China pouch packaging market.

China Pouch Packaging Industry Leaders

Amcor Plc

Mondi Plc

Sonoco Products Company

Cangzhou Hualiang Packaging Decoration Co., Ltd

TedPack Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Mondi opened FlexStudios, a Shanghai hub for collaborative development of recyclable flexible packs.

- February 2025: NMPA enacted provisions supporting cosmetic-ingredient innovation, shortening approval cycles and spurring demand for premium flexible formats.

- January 2025: China raised PVC import tariffs from 1% to 5.5%, pushing pouch makers toward alternative barriers.

- May 2024: Dow unveiled REVOLOOP™ PCR resins at Chinaplas, collaborating with Sealed Air on e-commerce packs with recycled content.

China Pouch Packaging Market Report Scope

Pouch packaging is a flexible product made from barrier films, paper, or foil, depending on the end-user’s requirement. The report analyzes the factors that impact geopolitical developments in the market based on the prevalent base scenarios, key themes, and end-user industry-related demand cycles. The analysis is based on the market insights captured through secondary research and the primaries. The market also covers the major factors impacting the growth of the pouch packaging market in terms of drivers and restraints. The estimates exclude the weight and the cost of the content inside the pouch packaging solution. The scope of the study is limited to B2B demand.

The China Pouch Packaging Market is Segmented by Material Type ( Paper, Plastic and Aluminum), by Resin Type - Plastic ( Polyethylene, Polypropylene, PET, PVC, EVOH, Other Resins), by Product ( Flat ( Pillow and Side Seal), Stand Up), by End-User Industry (Food (Candy & Confectionery, Frozen Foods, Fresh Produce, Dairy Products, Dry Foods, Meat, Poultry, And Seafood, Pet Food, Other Food Products (Seasonings & Spices, Spreadables, Sauces, Condiments, etc.)), Beverage, Medical and Pharmaceutical, Personal Care and Household Care, and Other End-User Industries).The market sizes and forecasts are provided in terms of value (USD) and volume (Units) for all the above segments.

| Plastics | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |

| Polyvinyl Chloride resin (PVC) | |

| Other Plastics | |

| Paper | |

| Aluminum Foil | |

| Other Materials |

| Flat (Pillow and Side-Seal) |

| Stand-Up |

| Spouted |

| Retort |

| Aseptic |

| Stick-Pack / Sachet |

| Rollstock / Premade Pouch |

| Zipper |

| Spout and Cap |

| Tear-Notch |

| Slider |

| Other Closure Type |

| Food | Candy and Confectionery |

| Frozen Foods | |

| Fresh Produce | |

| Dairy Products | |

| Dry Foods and Cereals | |

| Meat, Poultry and Seafood | |

| Pet Food | |

| Other Foods (Sauces, Condiments, Spreads) | |

| Beverage | Alcoholic |

| Non-Alcoholic | |

| Medical and Pharmaceutical | |

| Personal Care and Cosmetics | |

| Home Care and Household | |

| Other End-User Industry |

| By Material | Plastics | Polyethylene (PE) |

| Polypropylene (PP) | ||

| Polyethylene Terephthalate (PET) | ||

| Polyvinyl Chloride resin (PVC) | ||

| Other Plastics | ||

| Paper | ||

| Aluminum Foil | ||

| Other Materials | ||

| By Product Type | Flat (Pillow and Side-Seal) | |

| Stand-Up | ||

| Spouted | ||

| Retort | ||

| Aseptic | ||

| Stick-Pack / Sachet | ||

| Rollstock / Premade Pouch | ||

| By Closure Type | Zipper | |

| Spout and Cap | ||

| Tear-Notch | ||

| Slider | ||

| Other Closure Type | ||

| By End-User Industry | Food | Candy and Confectionery |

| Frozen Foods | ||

| Fresh Produce | ||

| Dairy Products | ||

| Dry Foods and Cereals | ||

| Meat, Poultry and Seafood | ||

| Pet Food | ||

| Other Foods (Sauces, Condiments, Spreads) | ||

| Beverage | Alcoholic | |

| Non-Alcoholic | ||

| Medical and Pharmaceutical | ||

| Personal Care and Cosmetics | ||

| Home Care and Household | ||

| Other End-User Industry | ||

Key Questions Answered in the Report

What is the current value of the China pouch packaging market?

The market is valued at USD 6.53 billion in 2026 and is projected to reach USD 8.44 billion by 2031, growing at 5.28% CAGR.

Which material dominates pouch production in China?

Plastic laminates lead with 61.72% revenue share, though paper-based alternatives are gaining traction at an 8.21% CAGR.

Why are stand-up pouches gaining popularity?

Brands favor stand-up formats for better shelf visibility and convenience, driving a 7.12% CAGR in this product category.

How are regulations shaping packaging choices?

Mandates on plastic reduction, express-parcel safety, and child-resistant pharma packs push brands toward mono-material PE and advanced closure systems.

Which end-user sector is the fastest growing?

Personal care and cosmetics post the highest CAGR at 8.07%, boosted by streamlined cosmetic-ingredient approvals.

What are the key challenges facing recycling of flexible pouches?

Limited curb-side collection and sorting infrastructure keep flexible-pack recycling rates far below rigid PET bottles, constraining circular-economy goals.

Page last updated on: