Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

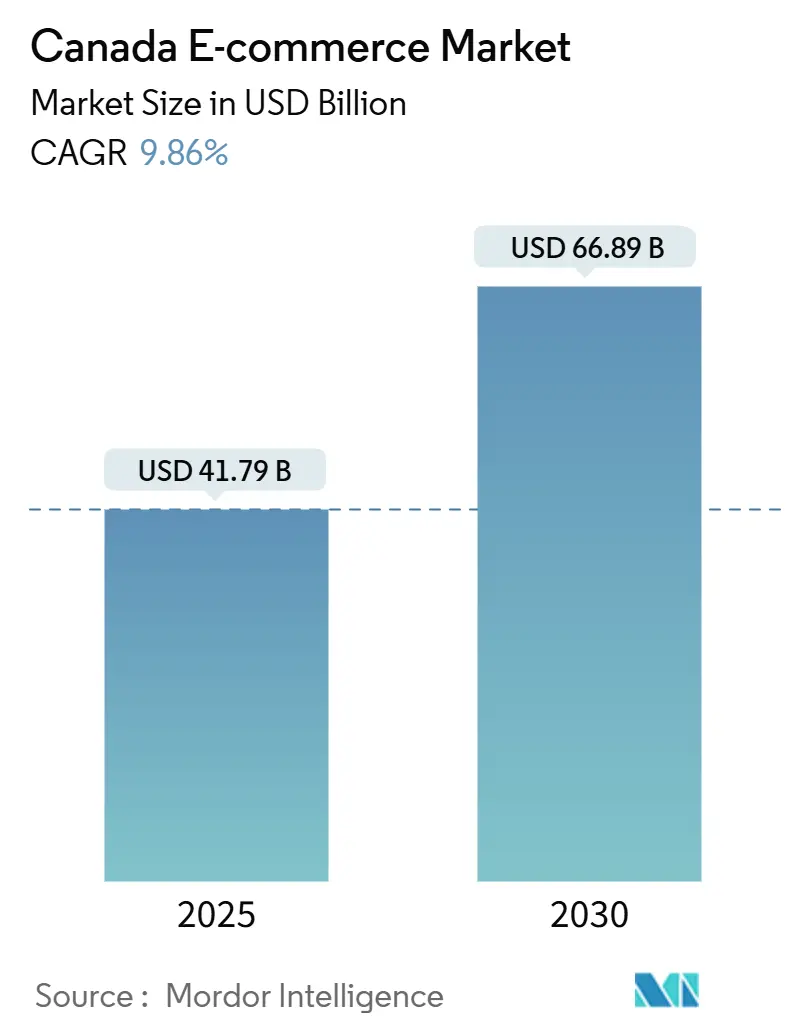

| Market Size (2025) | USD 41.79 Billion |

| Market Size (2030) | USD 66.89 Billion |

| Growth Rate (2025 - 2030) | 9.86% CAGR |

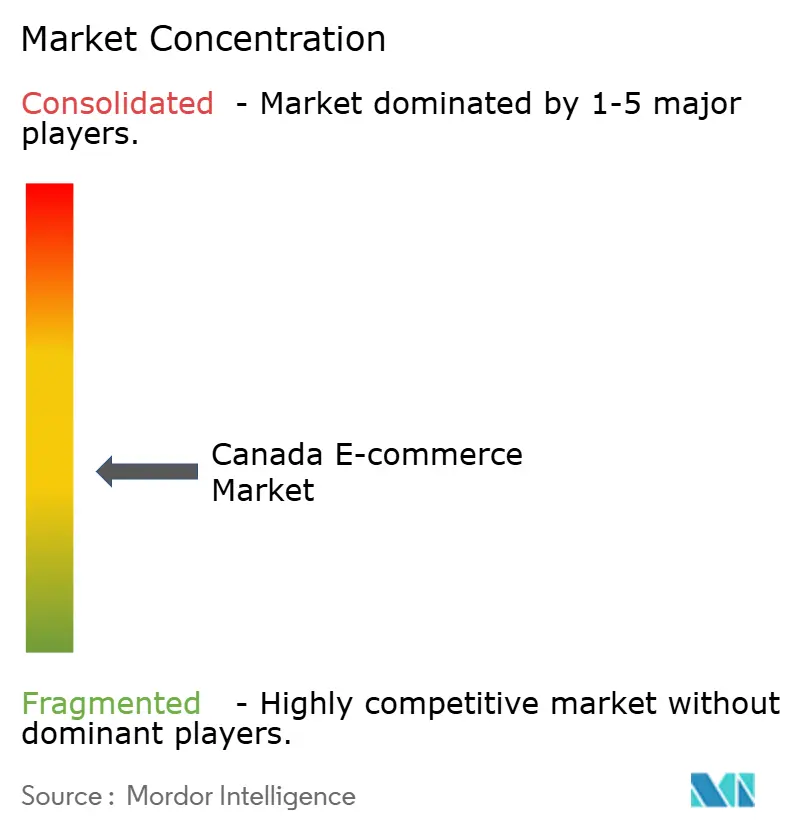

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canada E-commerce Market Analysis by Mordor Intelligence

The Canada e-commerce market is valued at USD 41.79 billion in 2025 and is forecast to reach USD 66.89 billion by 2030, translating into a 9.86% CAGR over the period. Steady smartphone adoption, faster fulfillment promises, and government incentives are reshaping shopper expectations while pulling more merchants online. Social commerce integrations, localized language capabilities, and payment diversification are further broadening reach and conversion. Intensified competition is motivating investments in micro-fulfillment networks and last-mile capabilities that shorten delivery windows. Meanwhile, regulatory shifts in privacy and cross-border duties are compelling firms to recalibrate data strategies and supply chains to sustain margin resilience. Together, these forces point to a Canada e-commerce market that is moving into a scale phase where omnichannel and logistics excellence determine share gains.

Key Report Takeaways

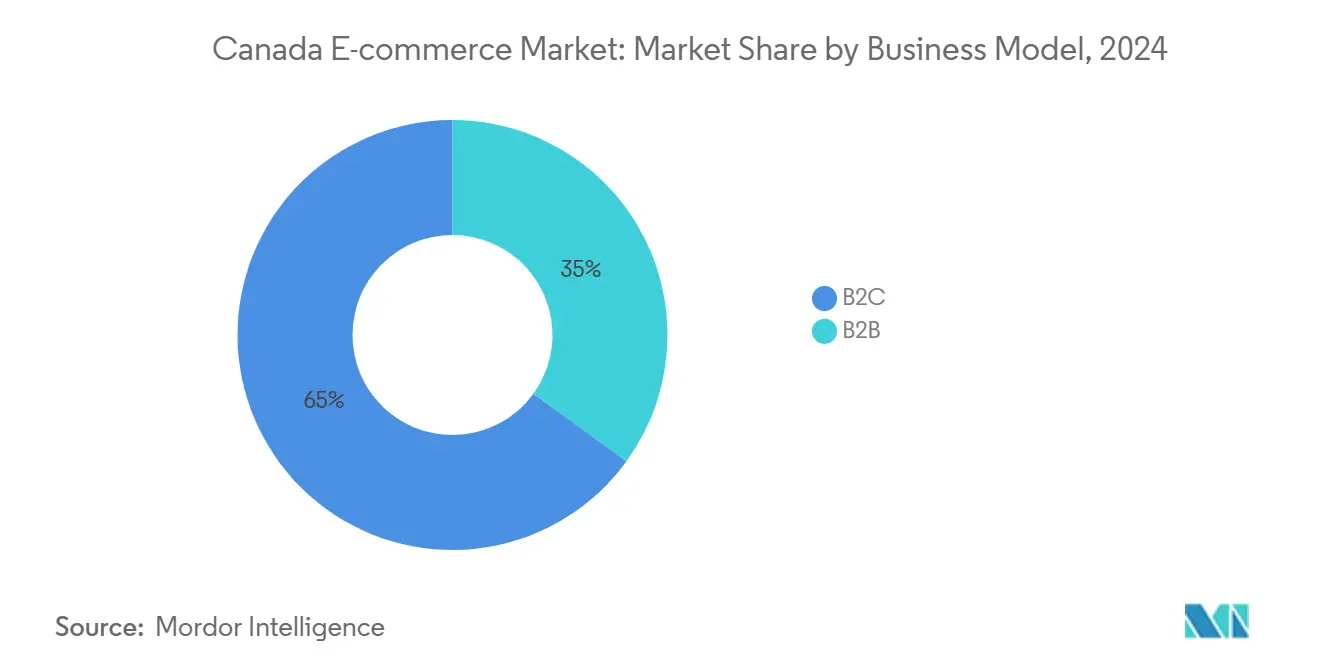

- By business model, the B2C segment led with 65% of Canada e-commerce market share in 2024, while B2B is projected to expand at a 12.5% CAGR through 2030.

- By device type, desktop/laptop held 55% of the Canada e-commerce market size in 2024; smartphones are advancing at an 18.1% CAGR between 2025 and 2030.

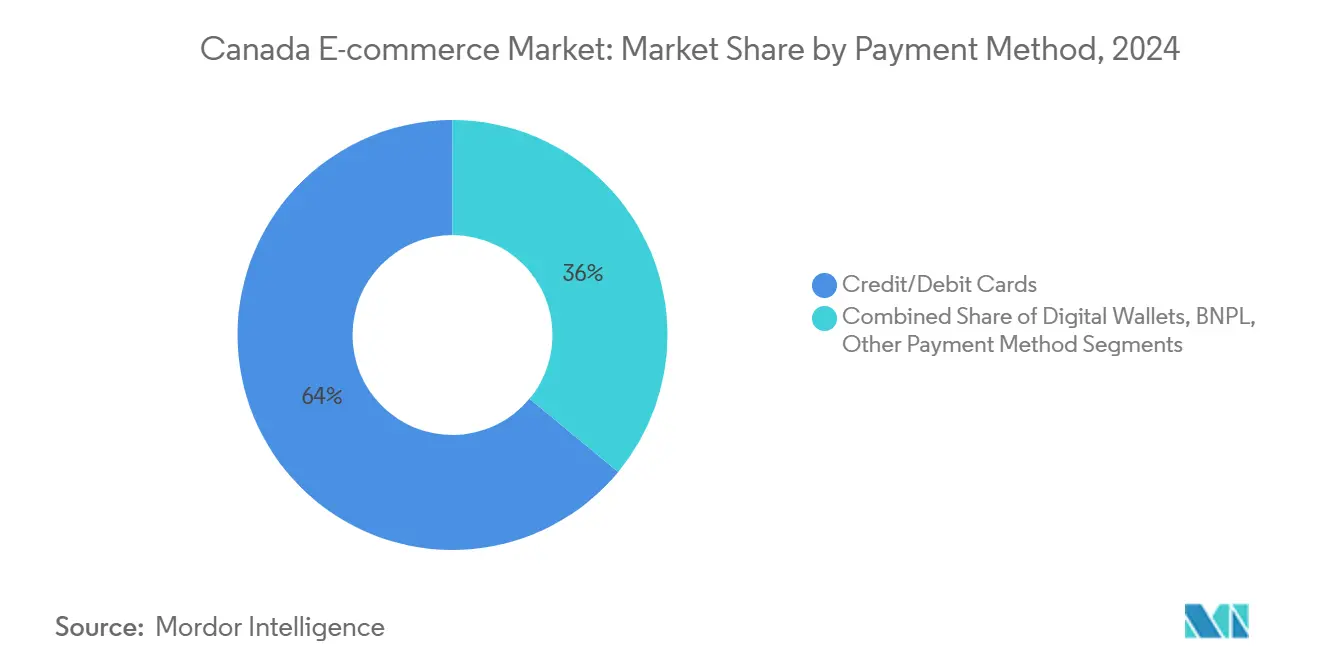

- By payment method, credit/debit cards commanded 64% share of the Canada e-commerce market size in 2024, with BNPL solutions growing at 19.2% CAGR to 2030.

- By product category, consumer electronics accounted for an 18% share of the Canada e-commerce market size in 2024, while beauty and personal care is rising at a 14.5% CAGR through 2030.

Canada E-commerce Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Same-Day Delivery Promos in Ontario's Urban Core | +2.5% | Ontario (Toronto, Ottawa, Hamilton), Quebec (Montreal) | Short term (≤ 2 years) |

| Accelerated Adoption of Interac Online & Contactless Debit among Gen-Z | +2.2% | National, with higher penetration in urban centers | Medium term (2-4 years) |

| U.S.–Canada Micro-Fulfilment Networks Lower Cross-Border Lead-Times | +1.8% | Border provinces (Ontario, Quebec, British Columbia) | Medium term (2-4 years) |

| Federal "Digital Adoption" Grants Boosting SMB Web-store Creation | +1.5% | National, with higher impact in smaller urban centers | Short term (≤ 2 years) |

| AI-powered Multilingual CX Tools Expanding Québec Conversion Rates | +1.2% | Quebec, with spillover to other bilingual regions | Medium term (2-4 years) |

Source: Mordor Intelligence

Intensifying Same-Day Delivery Promos

Same-day delivery has shifted from a premium extra to a baseline expectation in Toronto, Ottawa, and Montreal. Retailers adopting the service report 10% revenue lifts and 80% customer-satisfaction gains as density economics lower per-drop costs by 15-20% since 2024.[1]Supply Chain Brain, “Parcel Rate Hikes to Watch in 2024,” supplychainbrain.com Micro-fulfillment centers embedded within mixed-use properties now accelerate order cycles while reducing line-haul miles, freeing working capital tied up in regional warehouses. Property developers increasingly earmark logistics space to capture this demand. The strategic payoff extends to acquisition economics because shoppers view delivery speed as a proxy for reliability, boosting brand preference in crowded categories. As more merchants upgrade last-mile capabilities, the Canada e-commerce market will witness broad service-level parity that shifts competition toward assortment, loyalty, and price.

Accelerated Adoption of Interac Online & Contactless Debit

Gen-Z’s preference for debit-based payments is accelerating Interac Online and contactless debit volumes, up 27% in 2024.[2]Statistics Canada, “Retail Trade, December 2024,” statcan.gc.ca Card-linked options now contribute to lower cart abandonment, with merchants recording 22% fewer dropped baskets after integrating Interac checkout buttons. Debit dominance is also curbing churn in subscription models, as direct account funding reduces involuntary cancellations tied to expiring credit cards. The behavioral shift is prompting gateways to embed real-time balance checks and tokenized security, thereby enhancing trust. Over the medium term, payment providers able to bundle debit, BNPL, and open-banking rails within a single stack will secure a competitive edge as the Canada e-commerce market prioritizes seamless, low-fee settlement.

U.S.–Canada Micro-Fulfillment Networks

Cross-border lead times have collapsed from up to 10 days to under 3 days in priority corridors after retailers placed inventory in micro-nodes on both sides of the border.[3]Visigistics, “Major Changes to Section 321 De Minimis,” visigistics.com Section 321 duty-free suspensions for Canada-origin parcels entering the U.S. intensify the need for in-market stock, motivating Canadian sellers to lease U.S. warehouse space. Third-party logistics providers supply customs expertise and pooled transport, lowering landed costs while safeguarding delivery promises. Enhanced speed makes U.S. assortments more attractive to Canadian shoppers and vice versa, driving incremental sales on both ends. The development of cross-border micro-fulfillment is expected to keep the Canada e-commerce market competitive against U.S. rivals that already provide one- and two-day delivery nationwide.

Federal Digital-Adoption Grants

The Canada Digital Adoption Program disbursed grants of up to CAD 15,000 (USD 11,100) to 15,000+ SMBs, catalyzing web-store launches and integrated tech stacks. Beneficiaries report 32% sales increases within six months by adding real-time inventory, modern payment gateways, and CRM integrations. Smaller urban and suburban merchants are the main recipients, narrowing regional digital divides. The grant framework mandates advisory engagements that embed long-term digital roadmaps rather than single-feature fixes. Consequently, the program is expected to expand the total addressable base of sellers, adding fresh assortment to the Canada e-commerce market and intensifying category fragmentation.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistently High Rural Broadband Costs in Atlantic Canada | -1.6% | Atlantic Provinces (Nova Scotia, New Brunswick, PEI, Newfoundland) | Long term (≥ 4 years) |

| Returns-logistics Surcharges on Bulky Items Hinders the Market | -1.3% | National, with higher impact in remote areas | Medium term (2-4 years) |

| Rising Privacy-law Compliance Spend under CPPA & Quebec Bill-64 | -1.1% | National, with concentrated impact in Quebec | Medium term (2-4 years) |

| Intensified U.S. Marketplace Fee Structures Squeezing Margins | -0.9% | National | Short term (≤ 2 years) |

Source: Mordor Intelligence

Persistently High Rural Broadband Costs in Atlantic Canada

Atlantic Canada’s rural households pay 42% more for internet but still face slower speeds, holding online shopping participation 37% below the national average. Although Ottawa’s USD 3.225 billion Universal Broadband Fund targets 100% high-speed coverage by 2030, last-mile economics remain challenging. Retailers serving these regions contend with higher delivery surcharges and longer transit times that erode customer experience. The digital divide limits addressable demand for categories such as groceries and bulky goods that depend on reliable connectivity for scheduling and tracking. Until infrastructure investments reach completion, the Canada e-commerce market will exhibit two-speed growth that favors urban corridors over coastal rural communities.

Returns-Logistics Surcharges on Bulky Items

Parcel carriers raised base rates by 5.9% in 2024, and oversized-item surcharges jumped even higher, pushing total shipping costs up more than 20% within 25 months. Furniture, appliance, and DIY retailers face a strategic dilemma: absorb costs or risk conversion by passing them on. Consumer expectations for free returns intensify the margin squeeze. In response, merchants deploy augmented-reality configurators and detailed dimension filters that lower mismatch-driven returns by double-digit percentages. Despite these mitigations, elevated reverse-logistics expenses will constrain growth in bulky categories and temper the overall CAGR for the Canada e-commerce market through the medium term.

Segment Analysis

By Business Model: B2B Exhibits Accelerated Digital Migration

The B2C segment represented 65% of the Canada e-commerce market in 2024, underscoring its entrenched consumer adoption. However, the B2B channel is tracking a 12.5% CAGR from 2025 to 2030, well above the total market pace. Procurement departments are shifting to digital workflows that integrate catalog search, purchase-order automation, and budget controls. Vertical marketplaces for construction, healthcare, and industrial supplies simplify supplier discovery and compliance validation. Subscription replenishment and punch-out catalog features mirror consumer convenience, narrowing experiential gaps between business and personal shopping.

B2C growth persists as social-commerce funnels and DTC playbooks deepen engagement. Influencer-led drops and community memberships lock in repeat buyers. Meanwhile, B2B portals adopt AI-based demand-forecast modules that align purchasing with production schedules, reducing stockouts and over-ordering. The convergence of expectations is leading to unified platform architectures that serve both personas with role-based interfaces, thereby expanding total addressable volume in the Canada e-commerce market.

By Device Type: Smartphones Close the Conversion Gap

Desktops commanded 55% of transactions in 2024, yet smartphones are growing at 18.1% CAGR, reshaping merchandising priorities. Progressive web apps now deliver near-native performance, narrowing the historical 2.3x desktop-mobile conversion gap to 1.4x. Mobile wallets such as Apple Pay and Google Pay cut checkout friction and lift conversion by 28% when enabled. Voice commerce and connected-device shopping represent less than 5% of orders but signal a future multimodal landscape.

Retailers optimizing product imagery, one-hand navigation, and biometric login earn disproportionate share of wallet among younger cohorts. Inventory visibility tailored to geo-location supports last-minute pickup and delivery, boosting impulse purchasing. As smartphone penetration nears saturation, incremental growth will depend on latency reductions and richer real-time personalization that leverages device sensors, cementing the centrality of mobile in the Canada e-commerce market.

By Payment Method: BNPL Catalyzes Higher Basket Sizes

Credit/debit cards held 64% market share in 2024. BNPL, while nascent, is scaling at 19.2% CAGR and is forecast to reach USD 11.32 billion in transaction value by 2030. Merchants advertising BNPL at product pages see basket values climb 30-45% as consumers amortize higher-ticket purchases. Digital wallets rank second for popularity, especially on mobile, combining tokenized security with one-tap ease. Open-banking payments are in pilot but promise lower interchange fees and instant settlement.

Regulatory scrutiny from the Financial Consumer Agency of Canada is prompting providers to clarify fee structures and repayment schedules. Nonetheless, flexible terms resonate with budget-conscious shoppers, suggesting sustained double-digit expansion. Merchants adopting multi-rail orchestration can route transactions by cost and risk, optimizing net margin while meeting shopper preference across the Canada e-commerce market.

Note: Segment shares of all individual segments available upon report purchase

By B2C Product Category: Beauty Leads Growth Momentum

Consumer electronics remained the largest category with 18% share in 2024, aligned with high ASPs and frequent upgrade cycles. Beauty and personal care, however, is the fastest riser at a 14.5% CAGR to 2030, fueled by virtual try-on and replenishment subscriptions. User-generated content on social platforms drives discovery, with 54% of beauty transactions influenced by social feeds.

Fashion and apparel combat high return rates through AI sizing tools that cut misfits by 23%, while meal-kit providers maintain pandemic-era momentum via curated menu personalization. Furniture retailers leverage AR to visualize fit and color, reducing return freight costs. Each vertical’s optimized experience underlines the shift toward specialized value propositions within the Canada e-commerce market.

Geography Analysis

Ontario and Quebec control 65% of transaction value, supported by dense populations and robust fiber coverage. Urban centers such as Toronto, Montreal, and Ottawa show penetration levels comparable to leading U.S. metros. British Columbia and Alberta form the next tier, with lifestyle-driven category skews toward outdoor gear and wellness. Cross-border purchasing remains elevated in border provinces, where delivery times from U.S. micro-fulfillment hubs average two days. The recent duty-free suspension has spurred Canadian sellers to warehouse inventory stateside to protect competitive delivery times.

Quebec’s Bill 96 demands French-language parity across all digital touchpoints by June 2025, impacting 250,000 businesses. Compliance costs are encouraging adoption of AI translation and bilingual CX tooling that raises conversion by 35% among francophone shoppers. Atlantic Canada’s sparse connectivity suppresses adoption, though federal broadband initiatives promise incremental uplift post-2026. Prairie provinces exhibit strong agricultural-equipment e-procurement, illustrating regional specialization.

Growth pockets emerge in second-tier cities where cost-of-living advantages attract population inflows. Retailers tailoring assortments and fulfillment to these local nuances gain traction. Consequently, the Canada e-commerce market demonstrates a mosaic of micro-dynamics that require province-specific go-to-market blueprints.

Competitive Landscape

The top five players hold around 40% share, indicating moderate concentration. Amazon Canada leads with a Prime-driven value proposition that locks in loyalty through fast shipping and exclusive media. Walmart and Costco leverage store footprints as forward-inventory nodes, reducing last-mile costs and enabling same-day pickup. Canadian Tire’s agile curbside model converts its broad category mix into rapid fulfillment, supporting its omnichannel ambitions.

Shopify’s acquisition of Deliverr for USD 2.1 billion strengthens its fulfillment network, giving merchants two-day coverage nationwide and challenging Amazon’s logistics moat. Larger incumbents invest in robotics-enabled DCs to raise throughput and lower per-unit costs. Specialized vertical merchants capitalize on domain expertise and curated assortments to attract enthusiast consumers. Social-commerce natives use influencer coalitions and content commerce to bypass traditional advertising, gaining rapid brand awareness.

Privacy regulation and language mandates add new competitive variables. Firms with scalable compliance frameworks and bilingual platforms gain faster entry into Quebec and data-sensitive segments. As technology and last-mile capabilities converge, differentiation gravitates to loyalty ecosystems, curated private labels, and sustainability commitments, shaping the next phase of the Canada e-commerce market.

Canada E-commerce Industry Leaders

-

Amazon.com Canada Ltd.

-

Walmart Canada Corp.

-

Costco Wholesale Canada Ltd.

-

Home Depot of Canada Inc.

-

Apple Canada Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Shopify acquired Deliverr for USD 2.1 billion, securing nationwide two-day fulfillment that enhances merchant conversion and narrows delivery-speed gaps with Amazon.

- March 2025: Amazon Canada committed USD 1.2 billion to three robotics facilities in Ontario and British Columbia, aiming to scale inventory depth and shorten delivery windows for Prime members.

- February 2025: Walmart Canada introduced a Delivery-as-a-Service model, monetizing its logistics network by offering same-day last-mile solutions to third-party sellers targeting urban shoppers.

- January 2025: Canadian Tire earmarked USD 300 million for digital upgrades including AI search and enhanced mobile UX, accelerating omnichannel integration across its retail chain.

Canada E-commerce Market Report Scope

E-commerce is the buying and selling of goods and services over the Internet through online shopping. However, this term is often used to describe a seller's efforts in selling products directly to consumers. It begins when potential customers learn about a product, buy it, use it, and ideally maintain lasting customer loyalty. The report's scope includes market sizes and forecasts for B2B and B2C e-commerce.

The Canada e-commerce market is segmented by B2C e-commerce (beauty and personal care, consumer electronics, fashion and apparel, food and beverage, and furniture and home) and B2B e-commerce. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Business Model | B2C |

| B2B | |

| By Device Type | Smartphone / Mobile |

| Desktop and Laptop | |

| Other Device Types | |

| By Payment Method | Credit / Debit Cards |

| Digital Wallets | |

| BNPL | |

| Other Payment Method | |

| By B2C Product Category | Beauty and Personal Care |

| Consumer Electronics | |

| Fashion and Apparel | |

| Food and Beverages | |

| Furniture and Home | |

| Toys, DIY and Media | |

| Other Product Categories |

By Business Model

| B2C |

| B2B |

By Device Type

| Smartphone / Mobile |

| Desktop and Laptop |

| Other Device Types |

By Payment Method

| Credit / Debit Cards |

| Digital Wallets |

| BNPL |

| Other Payment Method |

By B2C Product Category

| Beauty and Personal Care |

| Consumer Electronics |

| Fashion and Apparel |

| Food and Beverages |

| Furniture and Home |

| Toys, DIY and Media |

| Other Product Categories |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Canada e-commerce market?

The market is valued at USD 41.79 billion in 2025 and is on track to reach USD 66.89 billion by 2030.

Which segment is expanding fastest within the Canada e-commerce market?

The B2B channel is growing at a 12.5% CAGR, outpacing the broader market’s 9.86% CAGR.

How quickly is mobile commerce growing?

Smartphone-based transactions are advancing at an 18.1% CAGR, eroding desktop’s historical dominance.

What payment method shows the highest growth momentum?

Buy Now Pay Later solutions are scaling at a 19.2% CAGR and are raising average order values by up to 45%.

How concentrated is the competitive landscape?

The top five companies hold around 40% market share, indicating moderate concentration and room for specialized entrants.

How are government grants influencing small business e-commerce adoption?

CDAP grants of up to CAD 15,000 have helped over 15,000 SMBs launch or upgrade online stores, driving 32% average sales lifts within six months.

Page last updated on: July 4, 2025