Bromobenzene Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.24 Billion |

| Market Size (2031) | USD 1.55 Billion |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

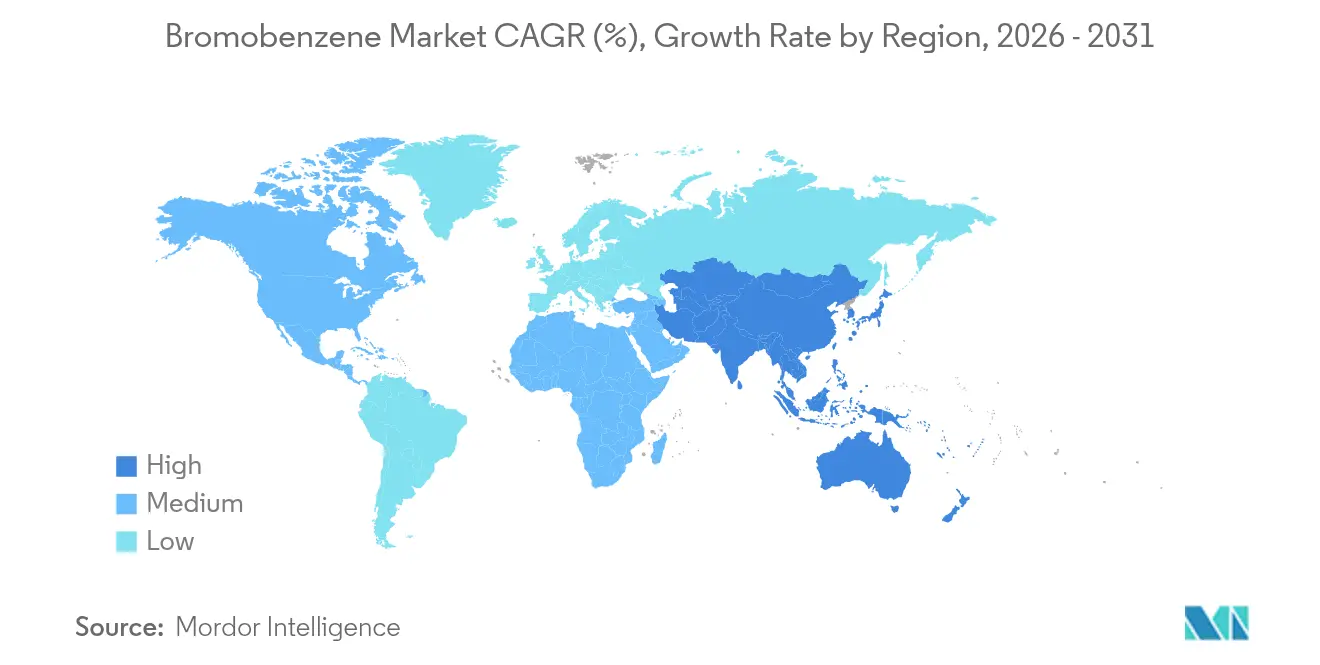

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

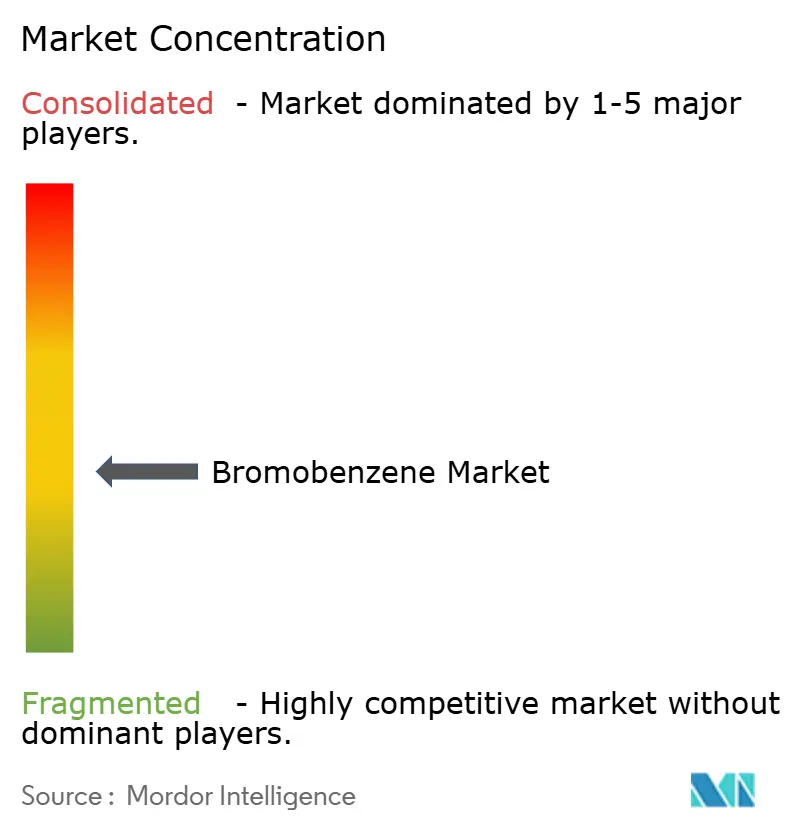

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bromobenzene Market Analysis by Mordor Intelligence

Bromobenzene market size in 2026 is estimated at USD 1.24 billion, growing from 2025 value of USD 1.19 billion with 2031 projections showing USD 1.55 billion, growing at 4.55% CAGR over 2026-2031. This expansion is rooted in bromobenzene’s indispensable role as a Grignard reagent precursor that underpins high-value pharmaceutical intermediates and specialty chemicals. Continuous outsourcing of complex synthesis to contract manufacturing organizations, especially in Asia Pacific, keeps utilisation rates high while sustained semiconductor capital expenditure widens demand for electronics-grade solvent grades. Firms that integrate upstream bromine extraction with downstream bromobenzene processing maintain cost advantages that preserve margins in spite of raw-material price swings. Regulatory tightening in Europe and North America raises compliance costs, yet the compound’s synthetic selectivity and lower volatility compared with many chlorinated analogues support a stable demand floor. The bromobenzene market also benefits from process innovations such as continuous-flow Grignard production that lift yields, curb waste, and open new application windows in advanced materials.

Key Report Takeaways

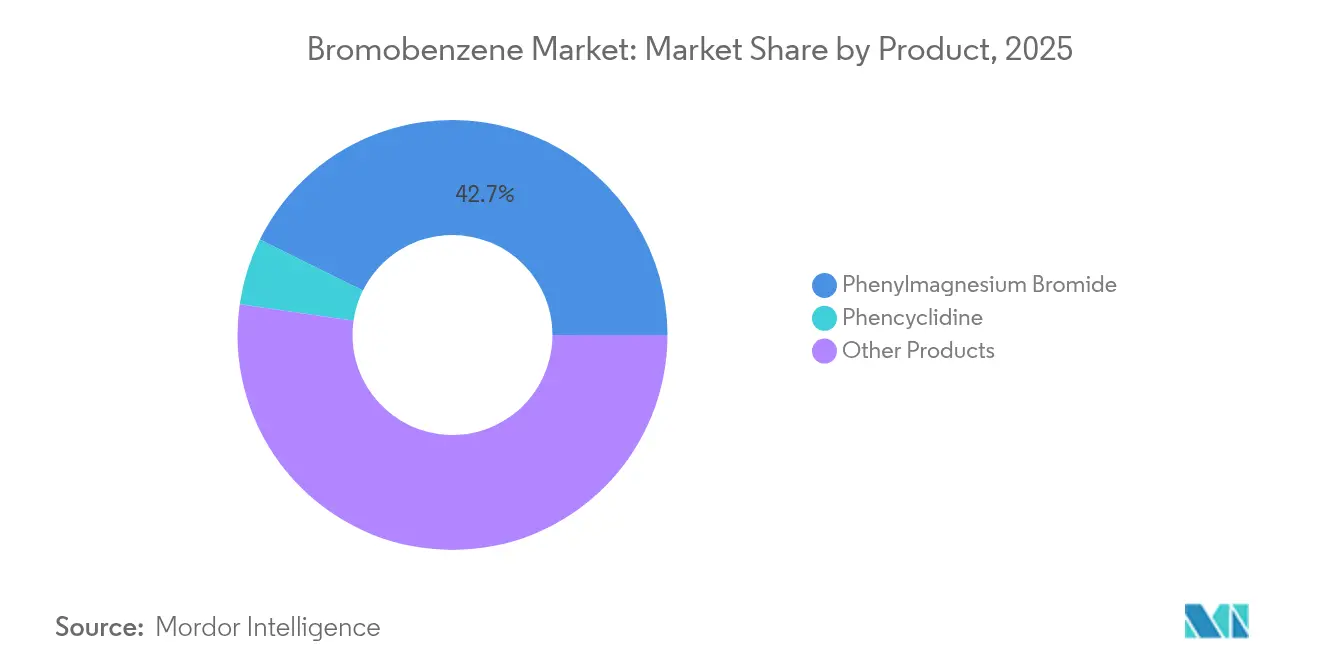

- By product category, phenylmagnesium bromide led with 42.68% of the bromobenzene market share in 2025, while phencyclidine captured a small but specialized 5.03% slice in the same year.

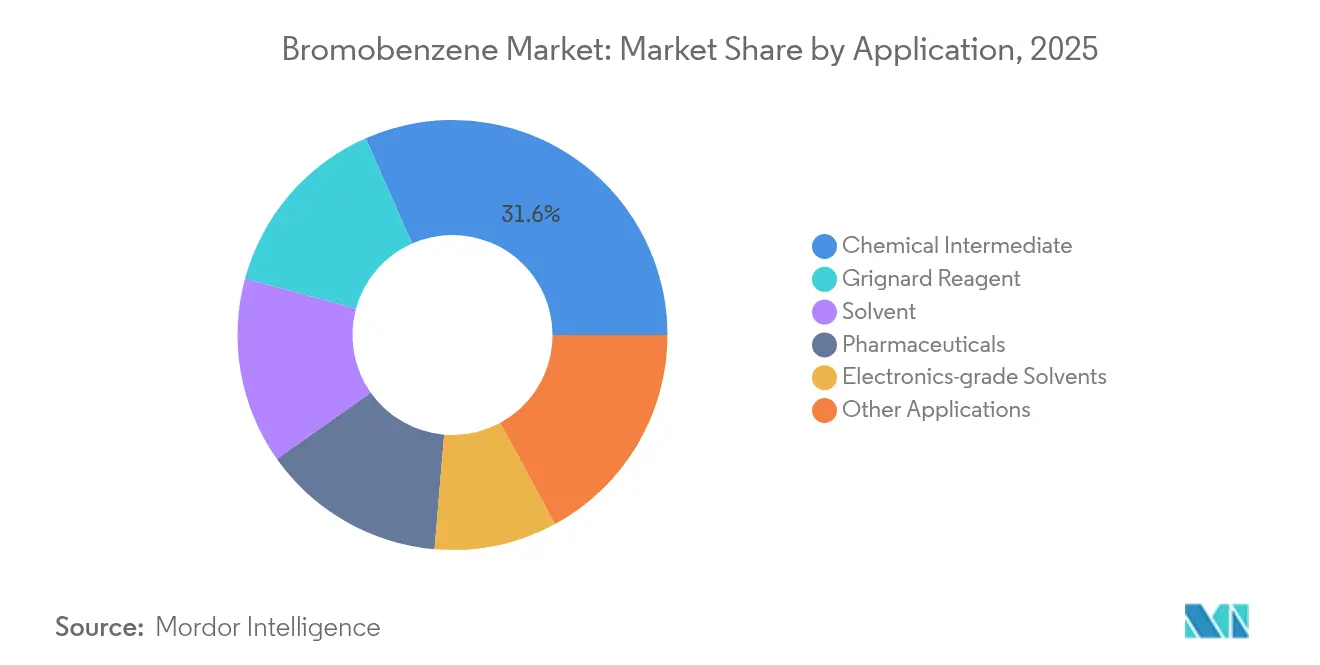

- By application, the chemical intermediates segment accounted for 31.62% share of the bromobenzene market size in 2025, whereas electronics-grade solvents recorded the highest forecast CAGR at 5.43% through 2031.

- By geography, Asia Pacific held 41.72% revenue share in 2025 and is projected to post the steepest regional CAGR at 5.62% to 2031, supported by China’s integrated bromine ecosystem and India’s capacity expansion plans.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bromobenzene Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pharmaceutical outsourcing in Asia Pacific | +1.20% | Asia Pacific core, spill-over to North America | Medium term (2-4 years) |

| Expansion of Grignard‐based manufacturing for high-value intermediates | +0.90% | Global, with concentration in Asia Pacific & Europe | Long term (≥ 4 years) |

| Growing demand for high-purity solvents in electronics | +0.80% | Asia Pacific & North America | Medium term (2-4 years) |

| Surge in contract production of psychoactive APIs | +0.60% | Global, regulatory-dependent regions | Short term (≤ 2 years) |

| Transition to low-VOC solvents in coatings | +0.40% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Pharmaceutical Outsourcing in Asia Pacific

Surging life-science outsourcing is reshaping bromobenzene demand profiles across India, China and Southeast Asia. Regional contract development and manufacturing organizations have scaled bromination and organometallic synthesis lines to secure Western supply contracts for psychoactive and oncology APIs. Regulatory harmonisation under ICH guidelines simplifies technology transfer while China’s abundant bromine feedstock cuts logistics costs, reinforcing price competitiveness for downstream phenylmagnesium bromide production.

Expansion of Grignard-Based Manufacturing for High-Value Intermediates

Pharmaceutical, agrochemical, and materials firms are widening their use of Grignard cross-coupling to access complex scaffolds at higher throughput. Continuous-flow reactors raise space-time productivity and suppress side reactions, making bromobenzene-derived phenylmagnesium bromide a cost-efficient nucleophile for difficult carbon–carbon bond formations[1]G. Cahiez and F. Alami, “Recent Advances in Grignard Reagent Chemistry,” Journal of Organometallic Chemistry, sciencedirect.com . Emerging rhodium-catalyzed homo-couplings extend bromobenzene’s reach to integrin inhibitor syntheses and other frontier therapeutics[2]N. Gensch et al., “Rhodium-Catalysed Homo-Coupling of Arylmagnesium Bromides,” Beilstein Journal of Organic Chemistry, beilstein-journals.org .

Growing Demand for High-Purity Solvents in Electronics

Ever-smaller semiconductor nodes heighten contamination sensitivity, lifting specifications for solvent purity. Electronics-grade bromobenzene supports wafer-cleaning, lithography, and OLED precursor synthesis owing to its narrow boiling profile and strong solvation of π-conjugated molecules. Taiwanese and Korean fab expansions scheduled through 2028 earmark additional offtake contracts for ultra-pure grades.

Surge in Contract Production of Psychoactive APIs

Mental-health-focused drug pipelines increasingly rely on controlled synthetic routes that deploy phenylmagnesium bromide for key carbon frameworks. Specialist CDMOs with validated bromobenzene handling systems win long-term supply agreements as innovators seek regulatory surety and reduced cap-ex exposure. Market expansion hinges on multi-jurisdictional compliance with narcotic regulations, yet revenue visibility remains strong for established players.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price competition from chlorinated aromatics | -0.70% | Global, particularly Asia Pacific | Short term (≤ 2 years) |

| Stricter REACH/TSCA restrictions on organobromines | -0.90% | Europe & North America | Medium term (2-4 years) |

| Volatility in bromine supply from Dead Sea producers | -0.50% | Global supply chain impact | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price Competition from Chlorinated Aromatics

Chlorobenzene’s 15-20% price discount challenges bromobenzene adoption in cost-sensitive formulations. The differential widened in 2024 after bromine feedstock prices spiked on supply disruptions, prompting some formulators to redesign synthesis routes around chlorinated aromatics. Producers counter by highlighting bromobenzene’s superior selectivity and lower reaction temperatures, yet aggressive price matching erodes margins.

Stricter REACH/TSCA Restrictions on Organobromines

The 2025 REACH update imposes higher dossier costs and potential use-specific authorisations for many brominated intermediates, amplifying compliance spending for European suppliers. Parallel TSCA risk-evaluation programmes extend scrutiny in the United States. Customers face uncertainty over future registration status, leading a few to pre-emptively test non-brominated alternatives despite performance sacrifices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Phenylmagnesium Bromide Dominates Synthesis Applications

Phenylmagnesium bromide represented 42.68% of the bromobenzene market in 2025, underscoring its ubiquity as a Grignard reagent for carbon-bond construction across pharmaceutical and specialty-chemical workflows. Flow-chemistry retrofits improved space utilisation and cut solvent volumes, lifting reactor uptime for this marquee product. Pharmaceutical integrators continue to prioritise phenylmagnesium bromide procurement because substitutions often compromise yield or stereochemistry. This demand stability shields the bromobenzene market from wider organobromine volatility. Continuous process intensification and a patent-protected electrochemical bromination route capable of 90% Faradaic efficiency are poised to enhance competitiveness, yet entrenched batch methods remain dominant in many Asian plants.

Other products, including ortho- and para-brominated derivatives plus specialised research chemicals, together form a diversified tail that services agrochemical, material-science and fragrance intermediates. Although these niches are smaller in volume, they command higher per-kilogram margins that temper revenue cyclicality. Phencyclidine, holding 5.03% share, illustrates the pattern: tight regulatory controls constrain scale, yet recurring demand from validated therapeutic protocols keeps price realisations elevated. Over the long run, incremental gains in continuous-flow selectivity may allow small-volume products to chip away at phenylmagnesium bromide’s share, but the broader bromobenzene market will likely remain product-concentrated through 2031.

By Application: Chemical Intermediates Lead Market Utilisation

Chemical-intermediate manufacture accounted for 31.62% of the bromobenzene market size in 2025 as the compound’s aryl bromide functionality enables efficient nucleophilic substitutions central to fine-chemical synthesis. Hybrid outsourcing models, whereby innovators retain route-design control yet delegate scale-up to Asian CDMOs, anchor sustained throughput in this segment. Grignard reagent manufacture ranks second, absorbing large volumes of phenylmagnesium bromide for onward reaction, followed by solvent use. Electronics-grade solvent demand is small in absolute terms, yet its 5.43% CAGR easily outpaces other application lines because each new wafer-fab demands class-zero contamination thresholds that bromobenzene can meet. Adoption will accelerate as fab projects in Korea and Taiwan come on-stream from 2026 onwards, driving contract stipulations for multi-year offtake.

Pharmaceutical end-use is intertwined with chemical intermediates, yet merits separate tracking because stringent validation requirements limit supplier substitution. Rising prevalence of psychoactive API pipelines adds a dedicated demand layer that buffers against downturns in commodity chemical consumption. Coatings and other industrial uses together form a long tail of emerging opportunities where bromobenzene’s low volatility and specific solvency outperform lighter aromatics. However, total penetration remains low due to price sensitivity and ongoing regulatory visibility. Diverse application exposure therefore insulates the bromobenzene market from narrow end-market shocks while preserving upside in technology-intensive niches.

Geography Analysis

Asia Pacific, with a 41.72% share in 2025, is the operational and demand epicentre of the bromobenzene market. China is a significant producer of elemental bromine, which supports nearby bromobenzene and downstream phenylmagnesium bromide plants. These facilities cater to both local formulators and fulfill export contracts. India’s Aarti Industries and other domestic groups are spending INR 1,500-1,800 crore on debottlenecking and backward integration to secure bromine availability and meet stricter impurity limits demanded by European buyers. Japanese and Korean electronics clusters generate incremental volumes for ultra-pure solvent grades. Southeast Asian countries add low-cost tolling capacity that supports the region’s overall CAGR through 2031.

North America remains a critical technology hub for the bromobenzene market, even though its consumption is lower than Asia Pacific. The United States hosts advanced pharmaceutical research pipelines that specify bromobenzene-derived intermediates for next-generation oncology and CNS actives. Albemarle Corporation’s brine operations in Arkansas strengthen local supply resilience and moderate price volatility. Canadian and Mexican buyers secure regional feedstock through spot imports, though their domestic production remains limited. Regulatory momentum under TSCA encourages investment in greener synthesis but also raises registration thresholds that smaller users find burdensome.

Europe operates under the strictest regulatory regime yet sustains specialty demand streams in high-value applications. German fine-chemical producers deploy closed-loop bromine recovery to curtail emissions, ensuring continuity of supply despite REACH dossier costs. Pharmaceutical multinationals headquartered in Switzerland, France, and the United Kingdom drive demand for GMP-grade bromobenzene intermediates used in small-batch, high-potency drug substances. Eastern European chemical parks attract contract formulations that benefit from lower labour costs and EU single-market access. Despite limited consumption in the Middle East and Africa, Jordan's significant bromine production capacity positions it as a pivotal regional raw-material hub, potentially spurring future bromobenzene projects. South America remains a small but rising consumer as Brazilian and Argentine agrochemical producers explore aromatic bromides for new active ingredients.

Value Chain Analysis

Upstream bromobenzene supply relies on benzene and elemental bromine, with availability and input-price volatility tied to access to bromine from brine-based assets and regional bromine ecosystems. Integrated producers that source bromine upstream and run downstream bromination and purification can better protect delivered costs when bromine tightens, while non-integrated suppliers depend more on spot procurement and tolling arrangements that can amplify swings.

Midstream activity includes bromination (commonly iron-catalyzed) and purification, such as vacuum distillation, to meet high-purity specifications (including 99%+ grades for pharmaceutical and laboratory buyers). Downstream distribution splits between bulk supply for chemical intermediates and Grignard reagent value chains, where phenylmagnesium bromide supports pull-through demand, plus smaller-lot channels for pharma, electronics-grade solvent qualification, and laboratory or research catalogs. In practice, SDS, impurity profiles, and traceability requirements gate access to higher-margin end uses. Asia-Pacific clusters, especially in China and India, concentrate both production and consumption, helping CDMOs and fine-chemical customers manage lead times, while exporters still handle additional qualification steps for regulated markets.

Competitive Landscape

The bromobenzene market is moderately fragmented. Albemarle Corporation integrates bromine extraction at brine fields with chlor-alkali feedstock optimisation, allowing it to deliver stable volumes at lower delivered cost. Shandong Henglian Chemical and other Chinese producers cluster facilities in Shandong and Hebei provinces to leverage proximity to upstream elemental bromine. They employ energy-efficient stirred tank reactors and recycle hydrobromic acid to curb waste. Indian players such as Aarti Industries focus on high-purity grades aligned with European pharmacopoeia specifications and have installed automated vacuum distillation lines to meet tighter metal and chloride limits.

Technology adoption differentiates competitors. Continuous-flow Grignard production improves reaction control, enabling higher throughput without scale-related safety risks. Electrochemical bromination breakthroughs reported at lab scale promise 15-20% raw-material savings and near-zero halogen fugitive emissions. Albemarle and Lanxess have piloted cell-stack retrofits that could move commercial within three years. Meanwhile, smaller Asian producers rely on legacy batch bromination yet maintain competitiveness through low-cost labour and export incentives. European specialists offset higher costs via customer-intimate service models and bespoke impurity profiling.

Strategic moves throughout 2024 and 2025 highlight the race for capacity and compliance. Aarti Industries raised capital expenditure guidance to scale a new multi-purpose bromination block. Lanxess doubled benzyl alcohol capacity in Washington state, indirectly boosting domestic bromobenzene pull-through. Chinese regulators accelerated licence approvals for integrated chem-parks that recapture hydrogen bromide streams, lowering environmental-permit hurdles for expansion. Industry participants continue to study bio-based aromatic routes, yet commercialization remains distant due to sluggish yields and limited natural feedstock availability.

Bromobenzene Industry Leaders

Aarti Industries Limited

Albemarle Corporation

Lanxess AG

Merck KGaA

Shandong Henglian Chemical Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term opportunity concentrates in higher-specification and service-intensive grades where buyers pay for consistent impurity control, documentation, and validated handling. Electronics-grade solvent demand, though smaller than chemical-intermediate volumes, creates room for producers that can demonstrate tighter metals and ionic contamination control and then maintain multi-year qualification cycles linked to semiconductor and display supply chains. On the pharma and fine-chemicals side, continued outsourcing of complex synthesis to Asia-Pacific CDMOs broadens the addressable pool for suppliers that can deliver stable lots for Grignard chemistry and coupling-reaction intermediates, supported by purification investments (for example, vacuum distillation) and process-safety systems.

A second opportunity is supply-chain resilience through backward integration and diversified bromine sourcing, which is reinforced by recent reminders that local disruptions can spill over into organobromine availability. Albemarle has highlighted that the Jordan Bromine Company joint venture returned to full operating rates after a flooding-related impact on volumes in early 2026, which aligns with buyer focus on redundancy and inventory strategy for bromine-linked intermediates. Regulatory compliance also functions as a differentiator, not just a cost, as REACH registration and restriction frameworks, along with TSCA and other inventory requirements referenced in supplier documentation, raise the value of vendors that can maintain consistent dossiers and product stewardship across regions.

Recent Industry Developments

- May 2026: Aarti Industries Limited reported its FY2026 consolidated results and reiterated ongoing progress on growth and integration initiatives, including actions aimed at optimizing capacity utilization. For bromobenzene-linked portfolios, these execution and utilization initiatives influence reliable supply into downstream intermediate and specialty-chemistry programs.

- February 2026: Albemarle Corporation noted that the Jordan Bromine Company (JBC) joint venture in Jordan was temporarily impacted by a flooding event and later returned to full operating rates. The incident underscored how operational continuity at large bromine assets can affect availability and pricing across bromine-derived intermediates, including bromobenzene value chains.

- May 2024: Aarti Industries continued to advance its multi-year capital program focused on debottlenecking and backward integration, aligning with tighter impurity expectations from regulated export markets. This type of investment supports higher-purity aromatic bromides and helps domestic producers compete on quality and supply assurance beyond commodity grades.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as the value generated from the sale of bromobenzene as a chemical product across regions, counted at the point where it is traded for use in further synthesis or as a solvent.

Scope exclusions: Finished pharmaceuticals, formulated agrochemical products, and downstream derivatives where bromobenzene is no longer sold as a distinct input are excluded.

Segmentation Overview

- By Product

- Phenylmagnesium Bromide

- Phencyclidine

- Other Products

- By Application

- Grignard Reagent

- Solvent

- Chemical Intermediate

- Pharmaceuticals

- Electronics-grade Solvents

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base and to avoid building the model on assumptions that cannot be defended. We referenced public sources such as customs and tariff statistics for aromatic chemicals, chemical safety and classification records (for example SDS and regulatory listings), and macro indicators tied to industrial output and chemical production.

To ground demand-side signals, we also used sources such as United Nations trade statistics, US and EU regulatory and chemical agency publications, peer-reviewed chemistry journals that discuss synthesis routes and uses, and trade association updates on chemical manufacturing. On top of that, we reviewed annual reports, investor presentations, and credible press coverage for capacity additions, maintenance shutdowns, and demand comments. Company financials and intelligence, a patent database, and a shipment-level import and export database were used selectively to confirm key assumptions where public data was thin. These desk sources are illustrative and not exhaustive, and many other references were used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work was done to pressure-test what we saw in published data, especially around use splits between chemical intermediate, solvent, and Grignard reagent related demand. We spoke with stakeholders across the value chain such as producers, distributors, and procurement and production roles at downstream users, and we covered APAC, EMEA, and the Americas so regional pricing and availability effects could be reconciled.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 20% | APAC: 44% |

| Mid tier: 44% | Functional/Unit leaders: 33% | EMEA: 37% |

| Smaller Players: 20% | Managers: 47% | Americas: 19% |

Market-Sizing & Forecasting

The model starts with a top-down build where production and trade indicators for brominated aromatics are translated into an addressable bromobenzene demand pool, which is then allocated by region based on manufacturing intensity and end-use exposure. Once that structure is set, we corroborate the totals using selective bottom-up approximations such as sampled price ranges by region and an ASP x volume check for key application buckets, followed by adjustments where the two views do not line up.

Key inputs used in the model include import and export volumes for relevant chemical codes, regional operating rates and capacity change signals, typical purity and grade mix movements, application-level demand pull from pharmaceuticals and chemical intermediates, and observed price spreads by region and contract type. When gaps showed up in the bottom-up checks, they were handled through conservative proxying using adjacent period averages and interview-confirmed ranges, and then re-tested against the top-down control totals.

For forecasting, scenario analysis was used so we could reflect different outcomes for downstream pharma and specialty chemical activity, along with supply tightness from plant turnarounds and incremental capacity. The scenarios were anchored to expert views gathered in interviews, and the final forecast was selected only after the near-term path looked consistent with trade flows and price behavior.

Data Validation & Update Cycle

Outputs were validated by triangulating the model against independent signals such as trade balances, regional price direction, and capacity news, and then checking that implied consumption did not break realistic use patterns. Any large variance between regions or sudden jumps in implied demand were flagged, reviewed in multiple steps by analysts, and clarified through follow-up outreach when needed.

The report is refreshed annually, and interim updates are triggered when material events occur, such as major capacity expansions, prolonged shutdowns, or sharp changes in trade restrictions. Before delivery, an analyst runs a fresh pass on key inputs and assumptions so clients receive an updated view aligned to the latest available data.

Mordor Intelligence's Bromobenzene Market Size Measured Against Other Published Estimates

Published market sizes for bromobenzene can look different even when the topic name is the same, because the underlying scope and counting point are not always aligned. Differences commonly come from whether the number represents the standalone chemical product, which years are treated as the base, and how pricing is converted across regions.

Finished pharmaceutical products and formulated agrochemical outputs sit outside Mordor Intelligence's scope for this market, which is one reason our 2026 value does not move in the same direction as estimates that blend bromobenzene into higher-level downstream revenue. Gaps also show up when one estimate uses a short historical window with a single price snapshot, while another smooths prices across contracts and regions, and then applies a different currency timing for conversion.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.24 B (2026) | |

| Global Consultancy A | USD 1.28 B (2024) | Uses a 2023 base with a 2024 market value update, and the sizing window appears tied to a shorter forecast horizon, which can amplify spot price effects and shift the year-on-year level versus a 2026 base. |

| Industry Publisher B | USD 1.40 B (2024) | Uses 2024 as the base year and presents several overlapping segment share cuts (grade, purity, application, and end use), which can lead to broader counting of the same demand pool and a higher total if not normalized to mutually exclusive buckets. |

The table shows that most of the spread is explained by different base years and how tightly the definition stays on bromobenzene as a traded chemical versus being blended into downstream value. By keeping the inputs tied to trade flows, capacity signals, and interview-checked price ranges, the sizing steps remain clear enough to re-run and to update without needing hard-to-access data.

Key Questions Answered in the Report

What is the current size of the bromobenzene market?

The bromobenzene market size reached USD 1.24 billion in 2026 and is forecast to attain USD 1.55 billion by 2031 at a 4.55% CAGR.

Why does phenylmagnesium bromide dominate product demand?

Phenylmagnesium bromide captured 42.68% of 2025 volume because it is the preferred Grignard reagent for carbon–carbon bond formation in pharmaceutical and specialty-chemical synthesis.

Which region consumes the most bromobenzene?

Asia Pacific held 41.72% of global demand in 2025 due to integrated bromine supply chains in China and rising pharmaceutical outsourcing in India.

How are regulations influencing the bromobenzene market?

Stricter REACH and TSCA frameworks raise compliance costs and create registration uncertainty, trimming projected CAGR by an estimated 0.9%.

What are the fastest growing applications?

Electronics-grade solvents show the highest forecast CAGR at 5.43% as semiconductor manufacturers tighten solvent purity specifications.

Who are the key players in the bromobenzene industry?

Albemarle Corporation, Aarti Industries, Shandong Henglian Chemical, Merck KGaA, and Lanxess lead the field in 2024.

Page last updated on: