Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

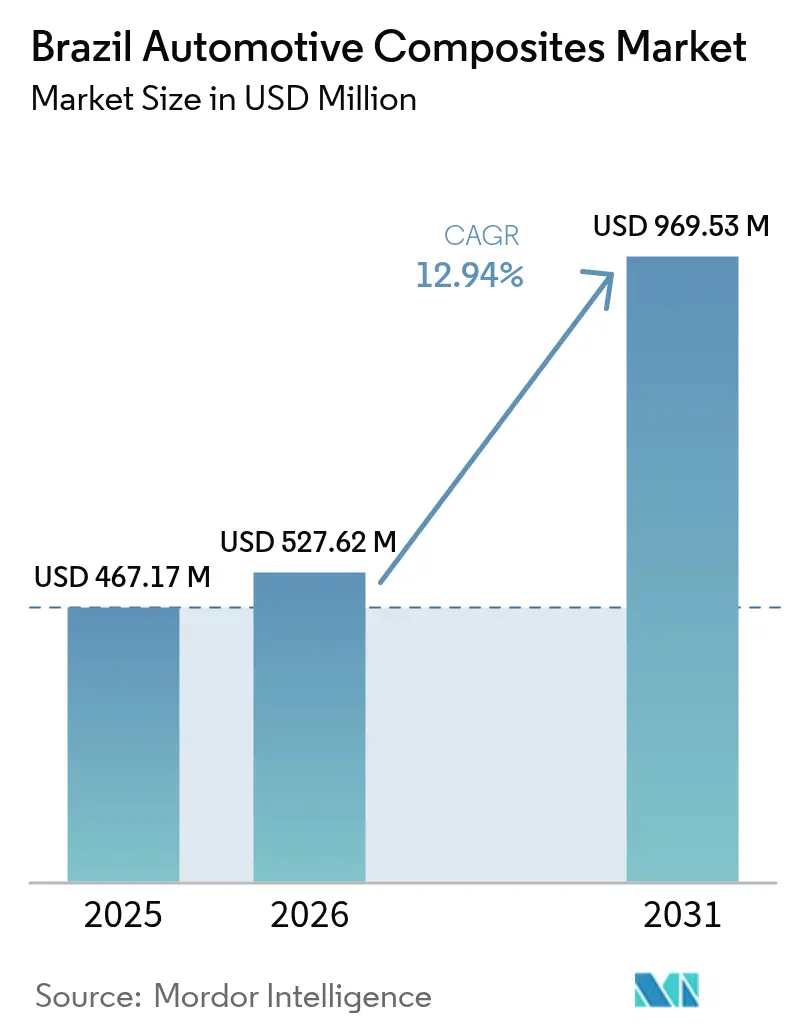

| Base Year Market Size (2025) | USD 467.17 Million |

| Market Size (2026) | USD 527.62 Million |

| Market Size (2031) | USD 969.53 Million |

| Growth Rate (2026 - 2031) | 12.94% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Automotive Composites Market Analysis by Mordor Intelligence

Brazil automotive composites market size in 2026 is estimated at USD 527.62 million, growing from 2025 value of USD 467.17 million with 2031 projections showing USD 969.53 million, growing at 12.94% CAGR over 2026-2031. The expansion is fueled by the National Green Mobility and Innovation Program (Mover)[1]Agência Brasil, “Government Tightens Emissions Targets,” agenciabrasil.ebc.com.br, rising OEM lightweighting demands, and the country’s renewed status as South America’s main vehicle‐manufacturing hub. Growing local content rules and tightening “well-to-wheel” carbon limits encourage automakers to substitute steel with composite solutions, particularly in structures and exterior body panels. Glass fiber composites currently dominate on cost and established supply, yet carbon fiber grades accelerate on premium vehicle lines and electric vehicle (EV) battery applications. Meanwhile, compression molding remains the volume workhorse, but continuous processing platforms gain favor as manufacturers seek faster cycles and higher material utilization.

Key Report Takeaways

- By material type, glass fiber accounted for 50.62% of Brazil's automotive composites market share in 2025, while carbon fiber is slated to grow at 15.42% CAGR through 2031.

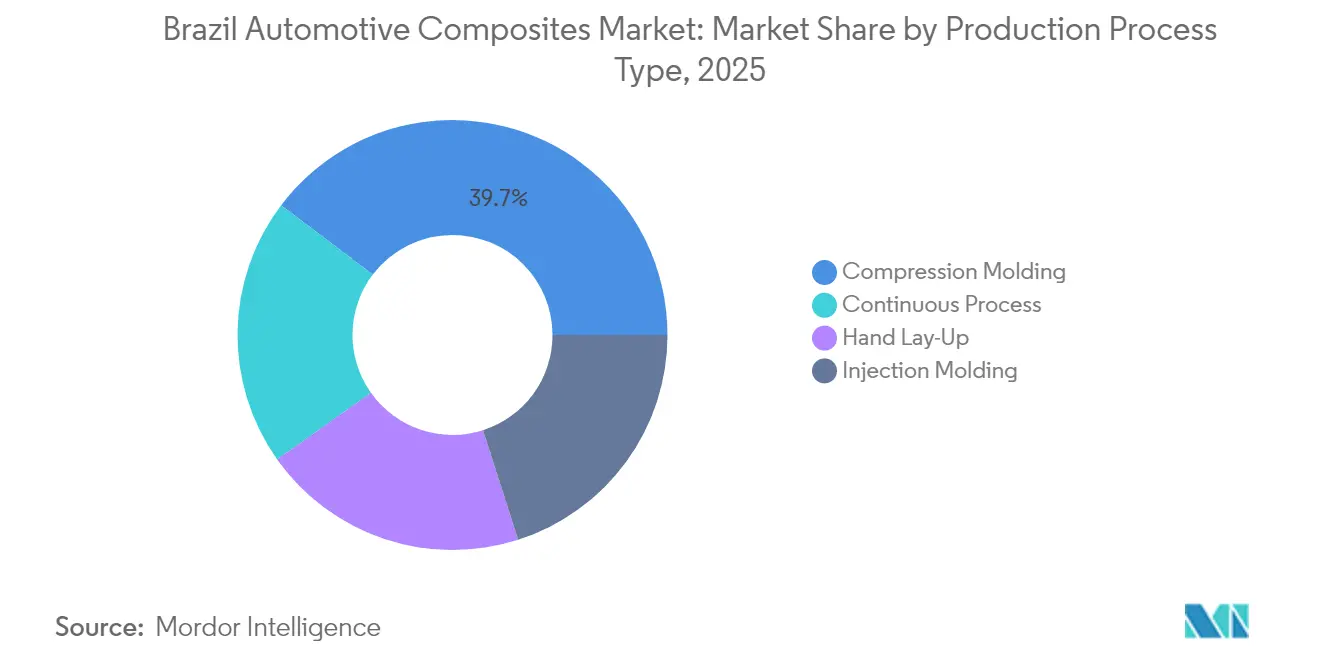

- By production process, compression molding led with 39.68% revenue share in 2025; continuous processing is expected to post the fastest 14.72% CAGR to 2031.

- By vehicle type, passenger cars commanded 49.10% of the Brazil automotive composites market size in 2025; the electric-vehicle segment is projected to expand at 15.98% CAGR through 2031.

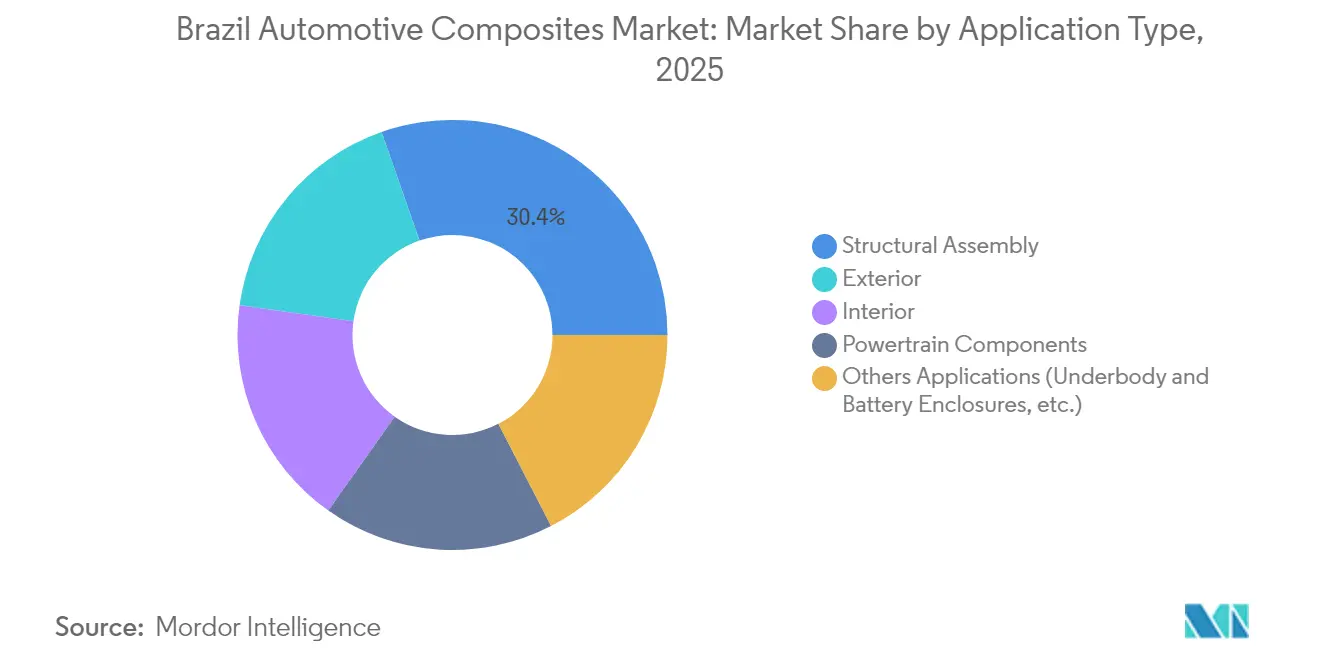

- By application, structural assembly captured 30.35% revenue in 2025, whereas exterior applications hold the highest 13.46% CAGR outlook.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Automotive Composites Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM lightweighting mandates | +2.1% | National, concentrated in the São Paulo automotive corridor | Medium term (2-4 years) |

| Rapid electrification of Brazil's bus and urban-delivery fleets | +1.8% | Major urban centers: São Paulo, Rio de Janeiro, Brasília | Short term (≤ 2 years) |

| Local supersport-utility assembly lines adopting carbon SMC body panels | +1.4% | São Paulo and Minas Gerais are production hubs | Medium term (2-4 years) |

| Growing demand for high-performance materials in automotives | +1.6% | National, with premium segment concentration in Southeast | Long term (≥ 4 years) |

| Expansion of domestic automotive production | +2.3% | National, with new investments in Paraná and Santa Catarina | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

OEM Lightweighting Mandates Drive Material Innovation

Brazilian OEMs confront stringent “well-to-wheel” carbon thresholds set to replace “tank-to-wheel” calculations, turning weight savings from a convenience into a regulatory necessity. Ford’s composite C-brace on the Bronco Raptor illustrates a 25-40% mass cut with superior torsional rigidity, a pattern now diffusing into local supply chains. Commercial‐vehicle makers also adopt composite cross-members to raise payload capacity, proving the mandate’s reach beyond passenger models. As lifecycle analytics become embedded in program approval gates, design engineers increasingly substitute welded steel with molded composite modules that integrate multiple functions. Domestic tier-1 suppliers respond by ramping thermoset sheet-molding-compound (SMC) output to secure OEM approval for 2026 model launches.

Rapid Electrification of Brazil’s Bus and Urban-Delivery Fleets

São Paulo alone targets 400 battery-electric buses by 2025, and nationwide charging‐station rollout aims for 150,000 units by 2035. Heavier traction batteries oblige OEMs to cut weight in bodies, roofs, and under-structures; composite floor pans and roof skins provide immediate 30-40% savings over metal. University fleet pilots show operating cost declines once renewable energy feeds chargers, reinforcing the economic proposition. Proterra’s 350-mile monocoque composite architecture underscores feasibility at scale. Urban last-mile vans mirror the trend, demanding composite battery enclosures with electromagnetic shielding and Impact resistance. These converging requirements spur toolmakers in Campinas to develop large-format closed-mold systems optimized for bus bodies.

Local Supersport-Utility Assembly Lines Adopting Carbon SMC Body Panels

Premium assemblers use carbon fiber SMC to cut tooling costs and bring exotic styling in-house, avoiding import tariffs on finished parts. The process delivers class-A surfaces after paint and allows integrated stiffening ribs, critical for supersport utility vehicles marketed on both aesthetics and torsional performance. Teijin’s Sereebo thermoplastic route trims cycle time by 10×, encouraging OEM engineers in Minas Gerais to select composite hoods and liftgates. The ability to bond directly to mixed-material structures aligns with Brazil’s evolving multi-material body architectures. High surface repeatability also reduces downstream sanding, offsetting carbon fiber’s unit cost.

Growing Demand for High-Performance Materials in Automotives

Complex electrified powertrains require composites that offer not only lightness but also thermal management and electromagnetic shielding. OEMs experiment with hybrid laminates, mixing glass and carbon to tailor stiffness zones while controlling the bill-of-material cost. Natural fiber curauá mats, grown in Pará, enter dashboards and door inserts, meeting sustainability requirements and generating rural income. Specialty resin systems with inherent flame retardancy enable under-floor battery trays that meet stringent thermal runaway criteria. As vehicles embed more electronics, automakers value composites’ damping attributes to reduce cabin noise in premium segments.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High import dependency for advanced fibres and resins | -1.9% | National, with an acute impact on advanced applications | Short term (≤ 2 years) |

| High material and processing cost | -1.5% | National, affecting cost-sensitive segments | Medium term (2-4 years) |

| Limited availability of recycling infrastructure | -0.8% | National, with urban concentration challenges | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Import Dependency for Advanced Fibres and Resins

September 2024 saw Brazil raise duties on 30 polymer categories from 12.6% to 20%, elevating raw-material costs for advanced laminates. Domestic plants cannot yet spin the aerospace-grade carbon tow required for structural battery cases, compelling converters to stockpile imports and tie up working capital. Supply-chain volatility forces molders to renegotiate delivery schedules with OEMs, who in turn risk production halts. Although petrochemical leaders evaluate scaling precursors locally, construction lead times push relief beyond the short term. Until then, tier-1 suppliers must diversify sourcing and hedge currency risks to protect margins.

High Material and Processing Cost

Carbon fiber typically runs 3-5× the price of equivalent-strength steel, a hurdle amplified in Brazil’s price-sensitive mass segments. Compression press investments reach USD 3-5 million each, requiring throughput certainty that niche volumes rarely justify. Labor-intensive hand lay-up, though flexible, clashes with OEM takt times. Solvay’s low-cost prepreg using robotic filament winding showcases one path for cost reduction, yet widespread adoption awaits full validation. Fleet operators evaluating composite bodies must weigh upfront premiums against fuel savings and corrosion avoidance, a calculation complicated by volatile diesel prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Process Type: Continuous Process Gains Manufacturing Momentum

Compression molding held 39.68% share of the Brazil automotive composites market in 2025 and remains the reference process for large, structurally demanding parts such as pickup beds, front-end modules, and floor panels. Decades of know-how allow local tier-1 suppliers to achieve repeatable tolerances, quick tool changes, and class-A surfaces that meet OEM paint shop standards. Yet every model revision forces engineers to trim grams, prompting line planners to scrutinize cycle times and scrap rates more aggressively than before.

At a forecast 14.72% CAGR, continuous lines are the fastest-growing technology, especially for battery-tray profiles where meter-long sections benefit from pultruded unidirectional stiffness. As OEMs push electrification deeper into mainstream models, ancillary accessories such as coolant manifolds and motor housings migrate to injection-grade reinforced polypropylene lattices demonstrably lighter than aluminum castings. These dynamics combine to position continuous manufacturing at the heart of capacity expansions, while legacy batch processes evolve toward niche, high-margin segments within the Brazil automotive composites market.

By Material Type: Carbon Fiber Adoption Accelerates Despite Cost Challenges

Glass fiber captured 50.62% market share in 2025 and remains the volume backbone for door modules, under-body shields, and spare-wheel wells because raw‐material costs align with entry-segment price points. Its entrenched supply chain stretches from petrochemical feedstocks in Rio Grande do Sul to rovings converted in São Paulo, facilitating localized stock buffers that shield OEMs from exchange-rate swings. Carbon fiber, however, charts the steepest growth curve at 15.42% CAGR through 2031 as premium assemblers and EV start-ups chase aggressive mass targets. High‐tension battery enclosures molded from quasi-isotropic carbon lay-ups cut 20–30 kg versus aluminum while embedding fire-resistant phenolic barriers.

Natural fibers such as curauá advance within door trim and headliners, where their specific stiffness rivals glass while offering 20–25% weight saving. Automakers highlight Brazilian biodiversity and low-carbon agriculture in marketing campaigns, reinforcing ESG positioning. Overall, the composite supply portfolio diversifies into a balanced matrix of cost-effective glass, performance-oriented carbon, and sustainable bio-fiber, each calibrated to specific platform needs in the evolving Brazil automotive composites market.

By Vehicle Type: Electric Vehicles Drive Composite Innovation

Passenger cars remained the dominant consumer at 49.10% of the Brazil automotive composites market in 2025, reflecting the segment’s entrenched production base, ranging from compact hatchbacks to midsize sedans. Traditional internal-combustion models continue to incorporate composite front-end carriers and trunk floors to offset heavier infotainment systems and safety devices. However, the EV category stands out with a 15.98% CAGR forecast, catalyzed by incentive schemes that grant tax relief and toll exemptions for zero-emission vehicles.

Commercial vehicles display steady uptake as fleet owners recognize total cost-of-ownership gains from composite bodies that resist corrosion on Brazil’s coastal delivery routes. Electric scooters aimed at last-mile gig couriers integrate glass-fiber decks and carbon tubing to balance affordability and robustness. Across all vehicle types, composites increasingly solve thermal-management challenges associated with power electronics; for instance, graphite-filled epoxy housings dissipate inverter heat more efficiently than die-cast aluminum. Thus, electrification broadens composite use cases beyond pure weight reduction, solidifying penetration across the Brazil automotive composites market.

By Application Type: Exterior Applications Lead Growth Through Design Innovation

Structural assemblies accounted for 30.35% revenue in 2025, with composite cross-members, floor pans, and rear header rails enabling automakers to meet stringent crash metrics. Crash-simulation validation conducted at local research labs demonstrates that composite energy absorption equals or surpasses steel when fiber orientation is optimized. Sandwich constructions with foam cores further boost bending stiffness at minimal mass penalty, a configuration increasingly specified on pickup tailgates in Minas Gerais. Yet exterior applications claim the fastest 13.46% CAGR to 2031, energized by supersport-utility designs featuring sculpted carbon SMC doors that could not be metal-stamped without complex hemming. The class-A finish attainable on molded parts reduces secondary sanding hours by 40%, unlocking assembly-line takt time savings.

Geography Analysis

São Paulo’s automotive corridor anchors over half of Brazil's automotive composites market demand, hosting OEM final-assembly plants, resin compounding centers, and Tier-1–3 suppliers within a 100 km radius. Dense logistics links, including port access at Santos, enable just-in-sequence deliveries of glass fabric rolls and pre-preg kits. Universities in Campinas and São Carlos feed talent into design offices, accelerating material qualification. Minas Gerais is the secondary locus, blending its metallurgical legacy with composite expertise to support premium supersport utility production and bus body builders. Its inland location reduces supply risk from coastal congestion, appealing to OEM business continuity plans.

Brazil’s North and Northeast currently register smaller composite consumption, yet long-term decarbonization. Co-location of renewable generation and chemical feedstocks could cut precursor energy cost by up to 40%, lowering the long-term price of domestic carbon tow. Such geographical diversification would de-risk supply chains and amplify composite penetration across nationwide vehicle programs.

Competitive Landscape

The Brazil automotive composites market remains moderately fragmented. Global heavyweights Hexcel Corporation, Solvay, BASF, and Toray Industries, Inc., pursue local partnerships or green-field plants to satisfy local-content rules and reduce import tariffs. Hexcel’s automotive sales rebound in 2025 despite aerospace softness, illustrating portfolio balancing[2]Hexcel Corporation, “Q1 2025 Earnings Call Transcript,” hexcel.com. Although the top five suppliers collectively capture sizable premium applications, plentiful regional molders manage commodity glass programs, keeping overall industry concentration moderate.

Brazil Automotive Composites Industry Leaders

Hexcel Corporation

Owens Corning

Solvay

Teijin Limited

TORAY INDUSTRIES, INC.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: SC Industrials announced a partnership between BeyondComposite and Protecta to supply ballistic-grade composite solutions for land, air, and sea defense platforms and personal protection gear.

- September 2023: Braskem and WEAV3D Inc. unveiled a demonstration part that combines Braskem’s polypropylene with WEAV3D’s thermoplastic composite lattice to boost structural performance in automotive applications.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts the value of fiber-reinforced polymer parts, semi-finished shapes, and compound pellets that enter on-road passenger and commercial vehicles built in Brazil. Coverage spans structural, exterior, power-train, and interior uses, irrespective of resin matrix, fiber type, or molding route.

Scope Exclusions: aftermarket repair kits, adhesives, and composites used only in motorcycles, farm machinery, or rail cars are excluded.

Segmentation Overview

- By Production Process Type

- Hand Lay-Up

- Compression Molding

- Injection Molding

- Continuous Process

- By Material Type

- Thermoset Polymer

- Thermoplastic Polymer

- Carbon Fiber

- Glass Fiber

- By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- Electric Vehicles

- Two-Wheelers

- By Application Type

- Structural Assembly

- Powertrain Components

- Interior

- Exterior

- Others Applications (Underbody and Battery Enclosures, etc.)

Detailed Research Methodology and Data Validation

Primary Research

Calls with tier-1 molders, resin formulators, OEM engineers, and trade officials across Sao Paulo, Minas Gerais, and Parana help us verify material penetration ratios, average selling prices, and cost pass-throughs, filling gaps spotted in desk work.

Desk Research

We begin by mapping Brazil's production and import flows using OICA assembly data, SENATRAN registrations, and customs codes published by the Foreign Trade Secretariat. Composite-content factors are sourced from peer-reviewed SciELO papers and patents filtered through Questel, while ABMACO's materials census and price curves from Polymer Update flesh out the demand skeleton. Macroeconomic guides from IBGE and emission rules issued by CONAMA frame scenario ranges, and capacity moves flagged in D&B Hoovers financials and Dow Jones Factiva news feeds sharpen our view. The sources named are illustrative; many other public and paid references support the desk stage.

Market-Sizing & Forecasting

A top-down and bottom-up hybrid converts vehicle volumes into potential composite kilograms, multiplies them by segment prices, and then cross-checks totals with selected supplier roll-ups. Key model levers include resin inflation, average part weight per vehicle, EV production share, fleet age, and carbon-credit incentives. A multivariate regression projects each driver to 2030, with ARIMA back-tests guarding statistical discipline. When bottom-up inputs are sparse, interview-based penetration ranges bridge gaps.

Data Validation & Update Cycle

Model outputs face variance scans against ABMACO consumption tallies, trade codes, and supplier disclosures before senior review. Reports refresh yearly, with interim updates triggered by material production or policy shocks, ensuring clients always receive our latest view.

Why Mordor's Brazil Automotive Composites Baseline Earns Trust

Mordor Intelligence values 2025 demand at USD 467.17 million.

External publications quote 2024 figures ranging from USD 175.83 million to USD 600.7 million, while one study suggests USD 3.6 billion for 2025.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 467.17 M (2025) | Mordor Intelligence | - |

| USD 600.7 M (2024) | Global Consultancy A | Includes storage tanks and aftermarket kits |

| USD 175.83 M (2024) | Regional Consultancy B | Uses OEM invoice prices only, omits import tariffs |

| USD 3.60 B (2025) | Industry Research House C | Applies global content assumptions without vehicle-mix correction |

Published estimates diverge mainly because of scope creep, differing price bases, and unadjusted vehicle-mix assumptions. By anchoring our baseline to verified production data, localized content factors, and an annual refresh cycle, we give decision-makers a balanced, transparent benchmark they can trace and replicate.

Key Questions Answered in the Report

What is the current size of the Brazil automotive composites market?

The market stands at USD 527.62 million in 2026 and is projected to reach USD 969.53 million by 2031 at a 12.94% CAGR (2026-2031).

Which material commands the largest share?

Glass fiber composites hold 50.62% market share due to their cost effectiveness and established local supply chains.

Why is carbon fiber gaining traction despite higher cost?

Premium vehicles and electric-vehicle battery enclosures require aggressive weight reduction and higher strength-to-weight ratios, propelling carbon fiber at a 15.42% CAGR through 2031.

Which production process is growing the fastest?

Continuous processing technologies such as pultrusion and automated fiber placement are expanding at 14.72% CAGR as OEMs demand shorter cycle times.

How will Brazil’s electrification goals influence composites demand?

Aggressive targets for electric buses and delivery fleets increase demand for lightweight composite structures to offset heavy battery packs and meet range requirements.

Page last updated on: