Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

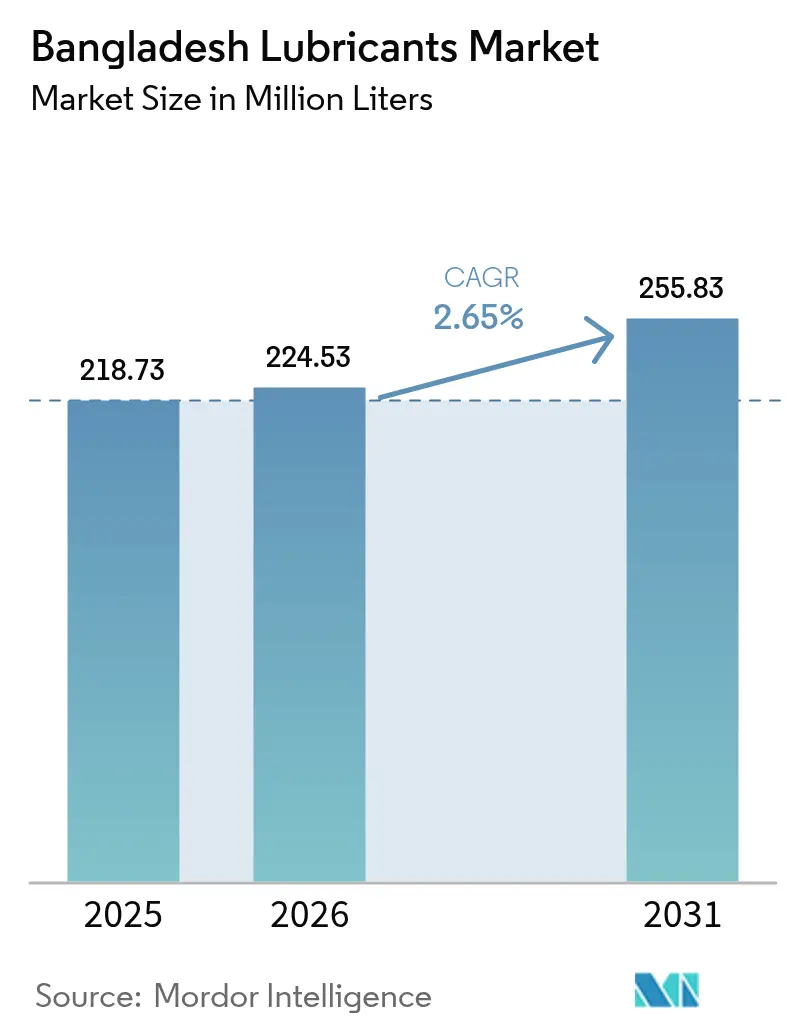

| Base Year Market Size (2025) | 218.73 Million liters |

| Market Volume (2026) | 224.53 Million liters |

| Market Volume (2031) | 255.83 Million liters |

| Growth Rate (2026 - 2031) | 2.65% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bangladesh Lubricants Market Analysis by Mordor Intelligence

The Bangladesh Lubricants Market size was valued at 218.73 million liters in 2025 and estimated to grow from 224.53 million liters in 2026 to reach 255.83 million liters by 2031, at a CAGR of 2.65% during the forecast period (2026-2031). Continued industrial diversification, an expanding vehicle parc, and rising consumer preference for higher-performance formulations underpin this trajectory. Synthetic and semi-synthetic grades are gaining momentum as original equipment manufacturers tighten engine-warranty requirements, while base-oil import rationalization encourages local blenders to recalibrate their additive packages. Post-pandemic construction, garment exports, and captive-power installations add incremental volume, yet widespread price sensitivity keeps mineral oils dominant in mass-market channels. Competitive fragmentation offers scope for niche positioning around fuel economy, extended drain intervals, and sustainable feedstocks, although quality-control enforcement will shape the pace of premiumization.

Key Report Takeaways

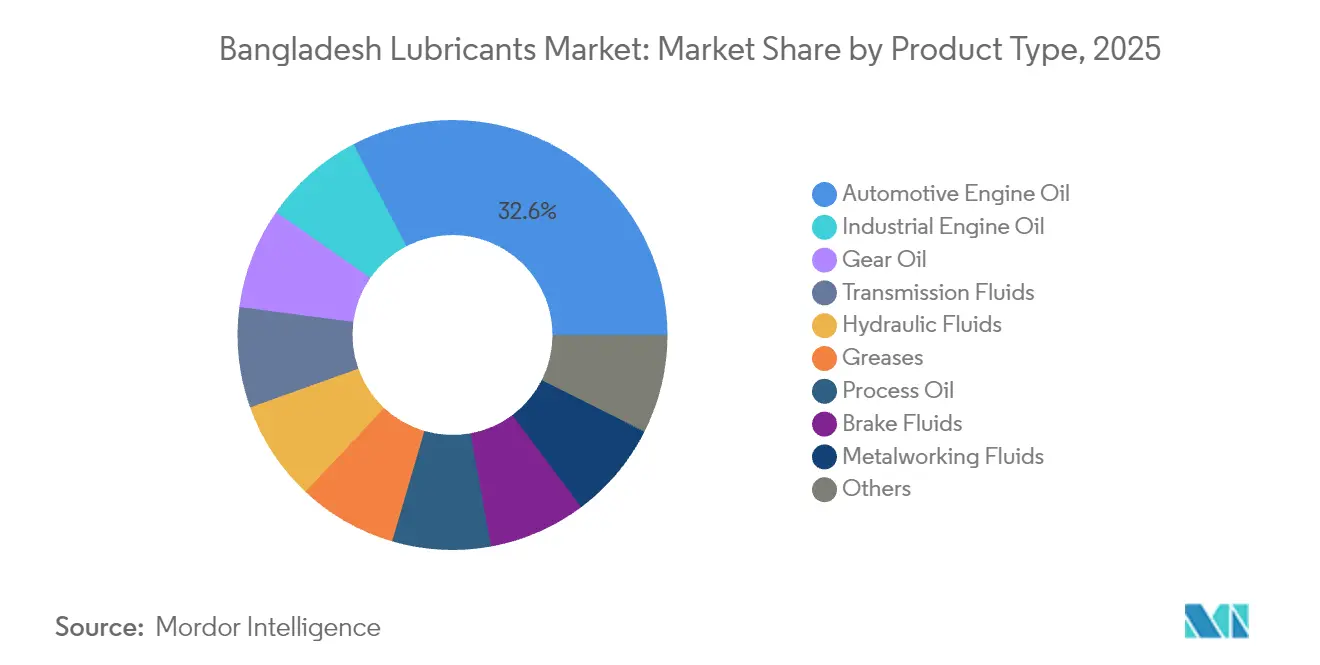

- By product type, automotive engine oil led with a 32.62% share in 2025; industrial engine oil is projected to grow at a 2.84% CAGR through 2031.

- By end-user industry, the automotive sector accounted for 47.35% of Bangladesh's lubricants market share in 2025, whereas industrial uses are projected to advance at a 2.72% CAGR through 2031.

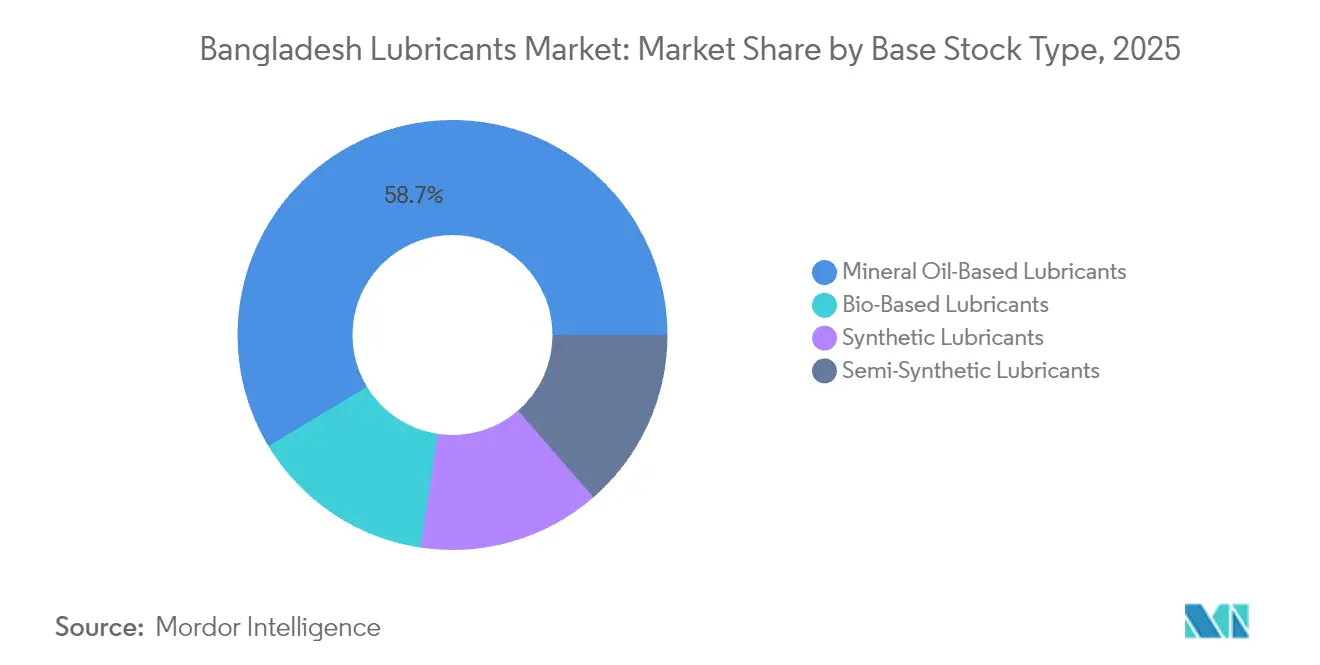

- By base-stock type, mineral oils captured 58.65% of Bangladesh's lubricants market size in 2025; bio-based grades are projected to expand at a 3.27% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bangladesh Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic rebound in transport, construction and industry | +0.8% | National, Dhaka-Chittagong corridor | Short term (≤ 2 years) |

| Rising two-wheeler ownership and ride-hailing penetration | +0.6% | Urban centers, expanding tier-2 cities | Medium term (2-4 years) |

| OEM shift toward synthetic/semi-synthetic lubes | +0.4% | Nationwide, assembly hubs | Long term (≥ 4 years) |

| Expansion of special economic zones with fiscal incentives | +0.3% | Designated SEZ belts | Long term (≥ 4 years) |

| Impending turbine-efficiency standards for captive power | +0.2% | Industrial clusters, textile regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-pandemic economic recovery drives lubricant consumption

Construction restarts, a rebound in textile orders, and resumed logistics operations lifted lubricant off-take across on-road fleets, hydraulic systems, and process equipment. Industrial buyers now factor energy savings and maintenance avoidance into procurement, accelerating the shift from monograde mineral oils to multigrade synthetics. Mega-projects, such as the Padma Bridge and Dhaka Metro, increase demand for heavy-duty engine oil, and garment factories adopt high-temperature spindle oils to reduce downtime. Distributor restocking cycles are becoming shorter as operators build safety stock against foreign-exchange volatility. Still, cash-flow stress among small transporters could delay the transition to extended-drain formulations.

Two-wheeler proliferation reshapes market dynamics

Motorcycle registrations have surged in urban and peri-urban areas, driven by ride-hailing apps and domestic assembly, resulting in increased demand for multigrade 10W-40 and 20W-50 oils. OEM-approved packs now claim shelf space in independent workshops, though price-sensitive riders often alternate between premium and economy brands. The trend compounds base-oil imports as blending plants raise Group II and III specifications to satisfy JASO MA2 requirements. Female ridership and youth demographics enhance the appeal of small-pack synthetics, which are often bundled with free filter-change services, a marketing strategy adopted by leading suppliers. Dealers, however, report margin compression as gray-market recyclers flood rural outlets.

Original equipment manufacturer specifications drive quality migration

Local assembly by Honda, Suzuki, and Bajaj requires warranty-compliant lubricants formulated with higher-quality base stocks and additive chemistries. Car assemblers mandate low-phosphorus, low-sulfated-ash engine oils compatible with after-treatment devices, prompting blenders to invest in automated dosing units and laboratory upgrades. Warranty claims linked to sludge formation have made consumers more receptive to synthetics despite the higher initial outlay. Multinationals capture the high-displacement motorcycle segment by co-branding factory-fill products, whereas domestic blenders co-develop semi-synthetic blends to stay within cost thresholds. Low VAT rebate on lubricant research and development still hampers rapid formula innovation.

Special economic zone expansion generates industrial lubricant demand

The government’s plan to operate 100 economic zones by 2030 is clustering power generation, apparel, and electronics plants, each requiring dedicated turbine oils, transformer fluids, and high-temperature chain oils. Developers offer duty-free import of raw materials, which encourages the use of on-site mini-blending units, thereby shortening delivery times and reducing logistics costs. Textile investors specify NSF-approved greases for knitting machines heading to export markets, and pharmaceuticals seek USP-grade white oils. SEZ authorities are piloting lubricant waste-collection schemes that may create a closed-loop feedstock for re-refining. The concentration effect boosts bulk orders, but it challenges suppliers to maintain multiple on-site technical service teams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on imported base oils and finished lubes | -0.5% | Port nodes Chittagong, Mongla | Medium term (2-4 years) |

| Grey-market recycled lubes eroding price premium | -0.3% | Nationwide, price-sensitive districts | Short term (≤ 2 years) |

| Low-grade imports expected after duty reduction | -0.2% | Border regions, informal channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Import dependency constrains market development

Bangladesh sources nearly all Group I-III base oils from Singapore and the Middle East, thereby exposing its supply chain to fluctuations in freight rates and foreign exchange. Domestic blenders face heightened cost pressures as the Finance Act 2024 raises the minimum customs value for base oil from USD 700 to USD 1,200 per metric ton[1]Abul Hassan Mahmood Ali, “National Budget Speech 2024-25: March Towards Smart Bangladesh,” Ministry of Finance, mof.portal.gov.bd . Small blenders must now carry larger working capital buffers or risk stockouts during peak farming and construction seasons. The lack of deep-draft jetties limits parcel size, thereby inflating landed costs compared to regional peers. Planned refinery upgrades could meet 10% of annual demand by 2028, but financing delays and unresolved environmental clearances remain.

Quality degradation threatens market premiumization

Re-refined and adulterated lubricants occupy informal retail shelves, sold in recycled bottles at discounts exceeding 40%. Poor additive treat rates lead to premature oxidation, bearing scuffing, and fuel-efficiency losses that negate OEM drain-interval gains. The absence of mandatory product-registration numbers hampers traceability, and enforcement teams face resource constraints. High disposal fees deter workshops from sending used oil to licensed collectors, feeding an illicit recycling loop. Reputable brands respond with tamper-proof seals, QR-code authentication, and workshop loyalty programs, yet the gray-market hold persists in suburban districts where price trumps performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Industrial engine oil outpaces automotive dominance

Automotive engine oil retained 32.62% of the Bangladesh lubricants market in 2025, while industrial engine oil posted the fastest 2.84% CAGR. Frequent oil-change intervals, particularly in tropical heat and stop-start traffic, help sustain automotive volumes, and branded garages reinforce adherence to periodic maintenance. Industrial gear and hydraulic oils, however, are closing the gap as ready-made garment factories automate looms and captive power plants align with stricter turbine efficiency targets. Transmission fluids and gear oils serve the growing fleet of medium trucks ferrying goods along the Dhaka-Chittagong corridor, whereas metalworking fluids cater to nascent auto-parts machining clusters.

Bangladesh's economic diversification, moving beyond its traditional automotive focus, is evident in the robust growth of its industrial engine oil segment. This surge is largely fueled by the installation of captive power plants and upgrades to manufacturing equipment.

Demand for high-temperature compressor oils spikes during summer load-shedding when textile mills rely on gensets. Marine lubricants find steady pull from inland cargo barges plying the Padma and Jamuna rivers, an overlooked yet sizable channel. White oils penetrate personal-care factories that supply regional markets, illustrating cross-vertical synergies for blenders able to certify food-grade compliance. Turbine-oil drain intervals now stretch beyond 6,000 hours in compliant plants, reducing total literage but increasing value per liter. The other product types bucket, including bio-hydraulic fluids, is expected to double its baseline by 2031, driven by SEZ environmental clauses.

By End-user Industry: Industrial ascent challenges automotive leadership

Automotive captured 47.35% of Bangladesh's lubricants market share in 2025, yet industrial applications are expanding at a 2.72% CAGR as the country’s manufacturing base widens. Two-wheelers alone generate more than half of the automotive lubricant market, with 10W-40 and 20W-50 grades dominating workshop shelves. Passenger cars typically use API SP 5W-30 synthetics to meet fuel-economy targets, whereas buses and trucks prefer CI-4+ 15W-40 oils with extended drain intervals. Marine and river transport require cylinder oils with a BN value greater than 70 to counteract the high sulfur content in residual fuels, representing a niche but margin-rich segment.

Industrial consumers span power utilities, steel rerolling mills, fertilizer plants, and agro-processing facilities. Textile mills increasingly monitor oil cleanliness to minimize loom downtime, driving sales of ISO VG-32 and VG-46 spindle oils with anti-wear additives. Pharmaceutical plants seek USP-grade lubricants for tablet presses, prompting blenders to register products with the Directorate General of Drug Administration. Construction-equipment AMCs bundle hydraulic-oil changes into leasing contracts, inserting predictable offtake flows. Aerospace remains a small market but gathers tailwinds from the national-carrier fleet renewal, stimulating demand for phosphate-ester hydraulic fluids subject to stringent approval lists.

By Base Stock Type: Bio-based grades gather green momentum

Mineral oils accounted for 58.65% of the Bangladesh lubricants market in 2025, while bio-based blends are projected to grow at a 3.27% CAGR through 2031. Group I remains the workhorse for cost-conscious fleets but faces supply tightening as regional refineries expedite closures. Group II adoption accelerates as additive packages evolve to meet Euro V targets, and Group III barrels arrive from the Middle East for premium passenger-car blends. Semi-synthetics appeal to motorcycle owners seeking mid-tier performance at a controlled cost, especially where warranty stipulations recommend the SAE 10W-30 viscosities. Fully synthetic PAO-based oils dominate the luxury-car and high-load industrial-compressor niches.

Bio-lubricants derived from castor and mustard seed oils exhibit promising kinematic viscosity stability and flash-point resilience, aligning with the green-washing audits of textile exporters. Life-cycle assessments report up to 40% lower greenhouse-gas footprints compared to mineral counterparts, a key selling point in buyer-driven apparel supply chains. Domestic farmers are eyeing cash-crop opportunities as oilseed demand grows, potentially localizing part of the feedstock loop. However, oxidative-stability enhancers and pour-point depressants increase formulation costs, meaning bio-grades will remain premium-priced until economies of scale are achieved.

Geography Analysis

Dhaka accounted for nearly half of organized lubricant sales in 2025, reflecting the region’s vehicle density, industrial clustering, and higher disposable income. Northern divisions such as Rangpur display mixed demand anchored in agricultural machinery, while Rajshahi’s silk and mango industries consume specialty greases and compressor oils. Khulna and Barishal in the south integrate river transport lubricants with emerging ship-building yards, diversifying end-use profiles.

Connectivity upgrades, notably the Padma Bridge, are poised to redistribute freight flows toward the southwest, potentially diluting Dhaka’s share but expanding overall consumption in the region. Special economic zones under development at Mirsarai and Araihazar promise concentric demand rings for process oils and high-grade transformer fluids as export-oriented factories ramp up production. Rural electrification has boosted transformer oil pull in off-grid micro-utility projects, while solar pumps in the delta region create a niche demand for biodegradable lubricants that minimize water-table contamination.

Port infrastructure shapes import logistics and pricing power. Chittagong’s draft limitations cap parcel size at 20,000 DWT, keeping freight costs elevated relative to Colombo or Singapore. The forthcoming Matarbari deep-sea port is expected to accommodate VLCC-sized base-oil shipments, thereby lowering CIF values and enabling competitive bulk pricing inland. Warehousing clusters around Narayanganj facilitate nationwide redistribution, but congested highways often extend delivery lead times beyond three days, compelling distributors to maintain buffer stocks. Digital commerce remains nascent, yet e-marketplace pilots suggest potential for direct-to-farmer packs in remote districts.

Regulatory Landscape

Bangladesh’s lubricants regulatory environment is shaped by product-quality standardization and border or tariff administration. The Bangladesh Standards and Testing Institution (BSTI), through its Chemical Divisional Committee (CSC-7: Lubricants and Related Products), aligns testing and specification practices to recognized international methods, including the BDS ISO 8068:2024 turbine-oil standard and referenced ASTM test methods used for lubricating-oil performance verification. This raises compliance expectations for formal-sector blenders and importers, while tightening standards for OEM-aligned quality claims.

At the operational level, the Chemicals (Management and Safety) Rules, 2023 extend safety obligations for the manufacture, import, and storage of hazardous chemicals, requiring safety reporting and audits for major hazard installations. This is relevant for additive handling and bulk storage. Environmental compliance for blending and related industrial units is anchored in the Bangladesh Environment Conservation Act, 1995 and associated EIA guidance, with Environmental Clearance Certificates managed by the Department of Environment (DoE). On the trade side, National Board of Revenue (NBR) instruments and the National Customs Tariff govern duties and regulatory duty (RD) treatment for lubricating oils and synthetic or semi-synthetic lubricants under relevant HS codes, while certain additive imports can access exemptions when brought in by VAT-compliant industrial blending units. Overall, these rules reinforce formalization and documentation discipline across the supply chain.

Value Chain Analysis

Bangladesh’s lubricants value chain starts with imported base oils (Group I-III) and additive packages arriving through port nodes such as Chattogram, followed by domestic lube oil blending plants (LOBPs) for formulation, filling, and packaging. Large organized players combine blending with laboratory testing and technical service, while an informal channel continues through unregistered blending and recycled or adulterated products that undercut price points in mass retail. Domestic production is supported by established facilities such as MJL Bangladesh’s LOBP in Chattogram (commissioned in 2003), which anchors higher-volume blending and bulk supply to automotive and industrial accounts.

Downstream, distribution includes bulk deliveries to industrial clusters (textiles, captive power, construction) and a fragmented retail network of workshops, dealers, and branded service points serving the vehicle parc. Logistics is shifting from reliance on coastal tanker movements toward pipeline-enabled petroleum transport, supported by infrastructure such as the Single Point Mooring (SPM) system (operational in February 2024) and the 250 km Chattogram-Dhaka oil pipeline (commissioning activity reported in February 2025). These changes improve supply reliability and reduce handling losses for petroleum movements, which benefits lubricant importers and blenders through more predictable inland distribution economics and inventory planning around major demand corridors.

Competitive Landscape

The Bangladesh Lubricant market is moderately consolidated. MJL Bangladesh leverages an exclusive mobile license, bulk storage terminals, and technical service teams to protect its lead across passenger-car and industrial specialties. Strategic pivots highlight technology localization and channel diversification. Meanwhile, e-commerce start-ups pilot subscription-based drain-interval reminders, linking end users directly to brand-authorized garages. Regulatory pressure on customs compliance is nudging market consolidation. Minimum customs values discourage under-invoicing, favoring large importers with robust working capital. Updated Bangladesh Standards and Testing Institution (BSTI) protocols enforce limits on phosphorus, sulfur, and zinc, thereby removing low-spec filler products from legitimate shelves. Yet, gray-market operators circumvent compliance by using recycled containers, underscoring enforcement gaps at district checkpoints. Multinationals lobby for lubricant-specific HS codes that distinguish between finished oils and process oils to curb misclassification practices.

Bangladesh Lubricants Industry Leaders

MJL Bangladesh Limited

BP p.l.c.

Shell plc

Chevron Corporation

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Premiumization and specification-driven demand create clear whitespace in Bangladesh for OEM- and standards-aligned formulations in both automotive and industrial segments, particularly where warranty compliance and equipment uptime shape procurement decisions. With automotive holding 47.35% of market volume in 2025 and mineral oils still accounting for 58.65% of base-stock share, suppliers have room to expand semi-synthetic and synthetic penetration through workshop programs, anti-counterfeit measures, and documented performance claims tied to API, SAE, and JASO needs highlighted by local assembly activity. BSTI’s evolving standards toolkit also supports differentiation by branded players, given that informal recycled or adulterated supply remains a recurring end-user concern.

Industrial specialization provides another set of targets, especially transformer oils, turbine oils, and textile or process applications that require tighter controls and technical service. A concrete indicator is Eastern Lubricants Blenders PLC entering a one-year agreement (July 2026) with Premier Petroleum Products & Lubricants Limited to market and distribute Ergon-brand transformer oil to government organizations, reflecting active channel build-out in power and utility-related lubricants. On the supply side, customs and valuation policy remains a swing factor for product mix and pricing; in June 2026, the National Board of Revenue proposed moving from fixed minimum customs values to a floating valuation formula for imported synthetic and semi-synthetic lubricants. This would increase the compliance premium for importers and reinforce the advantage of scale players and local blenders that can manage documentation, working capital, and product traceability.

Recent Industry Developments

- July 2026: Eastern Lubricants Blenders PLC entered into a one-year agreement with Premier Petroleum Products & Lubricants Limited to market, sell, and distribute Ergon-brand transformer oil to government organizations in Bangladesh. The move expands ELBL’s presence in specialized electrical and utility lubricant categories and strengthens access to institutional procurement channels.

- June 2026: Bangladesh’s National Board of Revenue proposed replacing fixed minimum customs values for imported synthetic and semi-synthetic lubricants with a floating valuation formula referenced to ICIS price assessments plus a minimum markup. The proposal heightened stakeholder concerns around pricing and compliance, and it increased the emphasis on formal documentation and customs-readiness for import-dependent premium lubricant portfolios.

- February 2025: Commissioning activity for the 250 km Chattogram-Dhaka oil pipeline progressed, improving inland supply reliability for lubricants and related petroleum products. The project increases throughput and reduces transit time between coastal imports and central blending hubs, supporting formalized distribution networks and inventory planning around key demand corridors.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Bangladesh lubricants market is the in-country consumption of finished lubricants used to reduce friction and protect equipment in vehicles and industrial machinery, measured across automotive and industrial applications, regardless of whether products are locally blended or imported.

Scope exclusions: This sizing excludes crude and unrefined base oils traded as feedstock, as well as lubricants sold outside Bangladesh even if they were blended in Bangladesh.

Segmentation Overview

- By Product Type

- Automotive Engine Oil

- Industrial Engine Oil

- Transmission Fluids

- Gear Oil

- Brake Fluids

- Hydraulic Fluids

- Greases

- Process Oil (Including Rubber Process Oil and White Oil)

- Metalworking Fluids

- Turbine Oil

- Transformer Oil

- Other Product Types

- By End-user Industry

- Automotive

- Passenger Vehicles

- Commercial Vehicles

- Two-Wheelers

- Marine

- Aerospace

- Heavy Equipment

- Construction

- Mining

- Agriculture

- Industrial

- Power Generation

- Metallurgy and Metalworking

- Textiles

- Oil and Gas

- Other End-Use Industries

- Automotive

- By Base Stock Type

- Mineral Oil-Based Lubricants

- Synthetic Lubricants

- Semi-Synthetic Lubricants

- Bio-Based Lubricants

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the demand picture and the operating context, then it is narrowed down to what can be counted as finished lubricants in Bangladesh. Public references were used to anchor the model, such as Bangladesh Bureau of Statistics for industrial activity indicators, Bangladesh Road Transport Authority for vehicle registration signals, Bangladesh Energy Regulatory Commission and power-sector publications for generator usage cues, and Bangladesh Petroleum Corporation materials for fuel and petroleum product context.

Trade and price direction checks were also added using sources such as Bangladesh Customs and UN Comtrade for import patterns, with HS-code notes to avoid mixing base oil with finished lubricants. We then cross-checked category definitions and technical conversion factors using lubrication and tribology literature and patent databases where formulation shifts needed clarification. Company annual reports, investor presentations, and credible local business press were reviewed to understand channel structures, blending capacity commentary, and pricing moves, and a paid subscription for shipment-level import-export data and company financials was used selectively to sanity check scale and timing. These sources are illustrative, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on filling the gaps that desk sources do not show clearly, especially pack-size mix, channel markups, and how pricing changes flow through after base-oil and additive cost swings. Interviews and surveys were completed with lubricant blenders and distributors, service workshop owners, fleet and industrial maintenance buyers, and a few domain specialists who track machinery upkeep practices across major end-use clusters. Since this is a country market, we also ensured responses reflect the main demand centers and import gateways, so assumptions on volumes and pricing are not driven by one city or one channel.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 14% | APAC: 46% |

| Mid tier: 52% | Functional/Unit leaders: 31% | EMEA: 36% |

| Smaller Players: 19% | Managers: 55% | Americas: 18% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand pool reconstructed from lubricant-consuming activity in Bangladesh, then stress-tested with selective bottom-up checks. On the top-down side, we translate the vehicle and equipment base into lubricant demand using inputs such as active vehicle parc by broad type, average annual drain intervals, typical sump-fill volumes, industrial operating hours for generators and key machinery, and the split between automotive and industrial use. Because the market is also sensitive to quality shifts, the model accounts for mix movement between mineral and higher grade products, which changes the implied average selling price even when volume grows slowly.

To keep totals realistic, sampled channel checks are run as a bottom-up approximation, where distributor throughput ranges, workshop off-take patterns, and a few sampled price points by pack size are multiplied and compared against the top-down outputs. Where direct data is thin, gaps are handled by using conservative ranges from interviews, then narrowing them based on import trends and the observed seasonality in vehicle servicing and industrial production cycles. Forecasting is done using scenario-based projections supported by exponential smoothing on core demand drivers, followed by analyst adjustments where experts expect step-changes from policy, construction cycles, or industrial expansion plans.

Data Validation & Update Cycle

Validation is done in layers so errors do not pass through unnoticed. Outputs are checked against independent signals such as lubricant import direction, proxy vehicle activity, and industrial output movements, then variances are investigated before numbers are finalized. When a segment grows faster than the demand indicators suggest, we re-check assumptions like drain interval shifts, product mix upgrades, or channel stocking changes, and we re-contact respondents if the gap looks structural.

A second analyst review is used to test calculations, unit conversions, and year-to-year continuity, followed by a final sign-off pass. The report is refreshed annually, and interim updates are triggered when major events occur, such as sharp currency moves, new tax and customs rules, or unusually large base-oil price changes. Before delivery, the latest public releases are re-scanned so clients receive the most current view that can be supported by the same repeatable steps.

Mordor Intelligence's Bangladesh Lubricants Market Sizing Compared With Other Published Estimates

Published market sizes for Bangladesh lubricants can look far apart because the counting rules are not always the same, and because volume and value can move in different directions when pricing shifts quickly. Differences also come from whether the estimate is tracking finished lubricants only, or whether nearby items like base oil and grease are mixed in without clearly stating it.

A refresh-led gap shows up when price assumptions are rolled forward using a single inflation factor or an outdated exchange rate, which can overstate value in USD even if liters are growing modestly. By refreshing pack-size weighted ASPs and the BDT to USD conversion timing during each update cycle, and then validating the implied price per liter against import and channel checks, Mordor Intelligence keeps the 2025 estimate tied to observable trading and consumption conditions rather than a one-time price snapshot.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 218.73 M (2025) | |

| Global Consultancy A | USD 186.00 M (2024) | Value-based sizing is presented without clear pack-size mix or exchange-rate timing, which can undercount premiumization effects and can also mismatch the year used for currency conversion. |

| Trade Journal B | USD 651.70 M (2026) | Article-style valuation is linked to a local currency estimate and broad market commentary, with no defined study period, no reconciliation to liters, and limited visibility on whether adjacent categories are included. |

The spread mainly comes from timing and definition choices, not from a hidden demand surge. When unit-of-measure, currency conversion date, and product boundaries are made explicit, the total becomes easier to reproduce and easier to compare across years, which is what most decision teams need for planning.

Key Questions Answered in the Report

What is the current size of the Bangladesh lubricants market?

The market stands at 224.53 million liters in 2026 and is projected to reach 255.83 million liters by 2031.

Which segment is growing the fastest within the Bangladesh lubricants market?

Industrial engine oil leads growth with a 2.84% CAGR through 2031 as captive-power and manufacturing demand climb.

What is driving the shift toward synthetic lubricants in Bangladesh?

OEM warranty requirements, consumer awareness of engine protection, and longer drain intervals are pulling demand toward synthetic and semi-synthetic formulations.

How dependent is Bangladesh on imported base oil?

Nearly all base-oil requirements are imported, making the sector vulnerable to fluctuations in freight costs, currency swings, and port logistics.

What regulatory trends are shaping the market?

Higher minimum customs values, stricter BSTI quality standards, and SEZ-based incentives are all influencing supplier strategies and product mix.

Page last updated on: