Bahrain Fisheries And Aquaculture Market Analysis by Mordor Intelligence

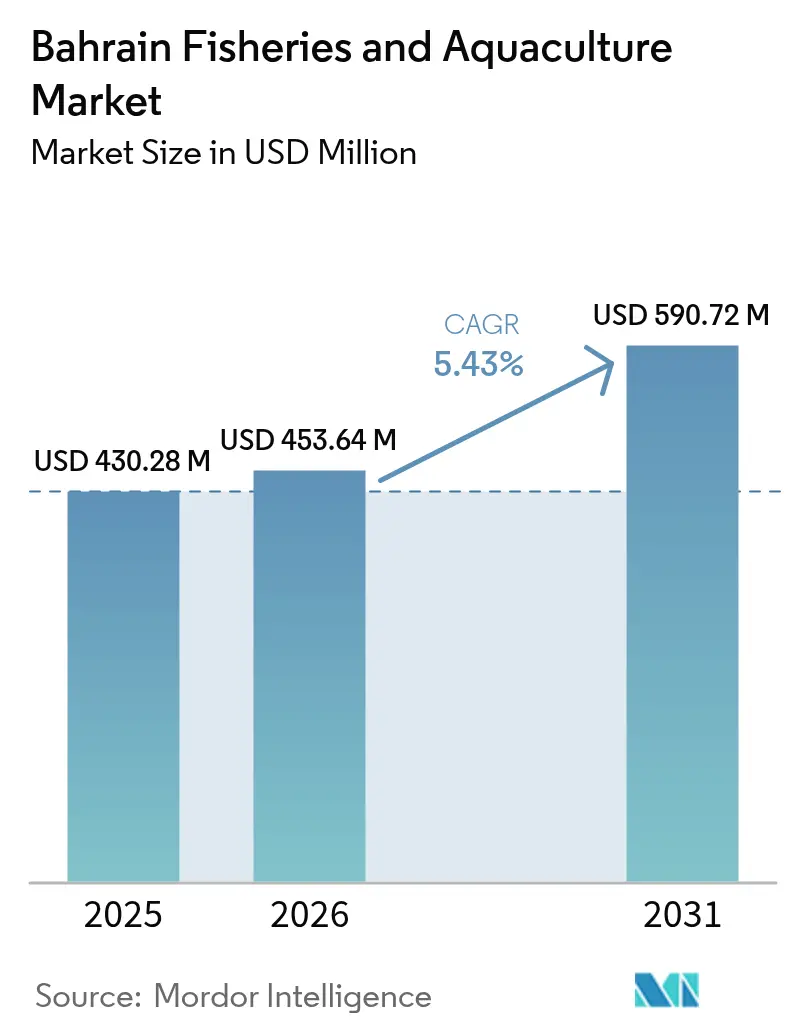

The Bahrain fisheries and aquaculture market size was valued at USD 430.28 million in 2025 and estimated to grow from USD 453.64 million in 2026 to reach USD 590.72 million by 2031, at a CAGR of 5.43% during the forecast period (2026-2031). This growth reflects the kingdom’s decisive pivot toward controlled farming systems after the March 2024 export ban on wild-caught seafood redirected premium tuna, mackerel, and shrimp to domestic shelves. Government subsidies covering up to 60% of recirculating-system capital costs, low-cost seawater supplied from industrial outfalls, and rising health-driven seafood consumption underpin steady demand and investment. Processors are deploying blockchain traceability and halal-certification technologies to defend their share in high-margin Gulf Cooperation Council (GCC) markets. Foreign-currency exposure on imported feed and fingerlings, together with summer disease outbreaks linked to Vibrio, remain key margin headwinds.

Key Report Takeaways

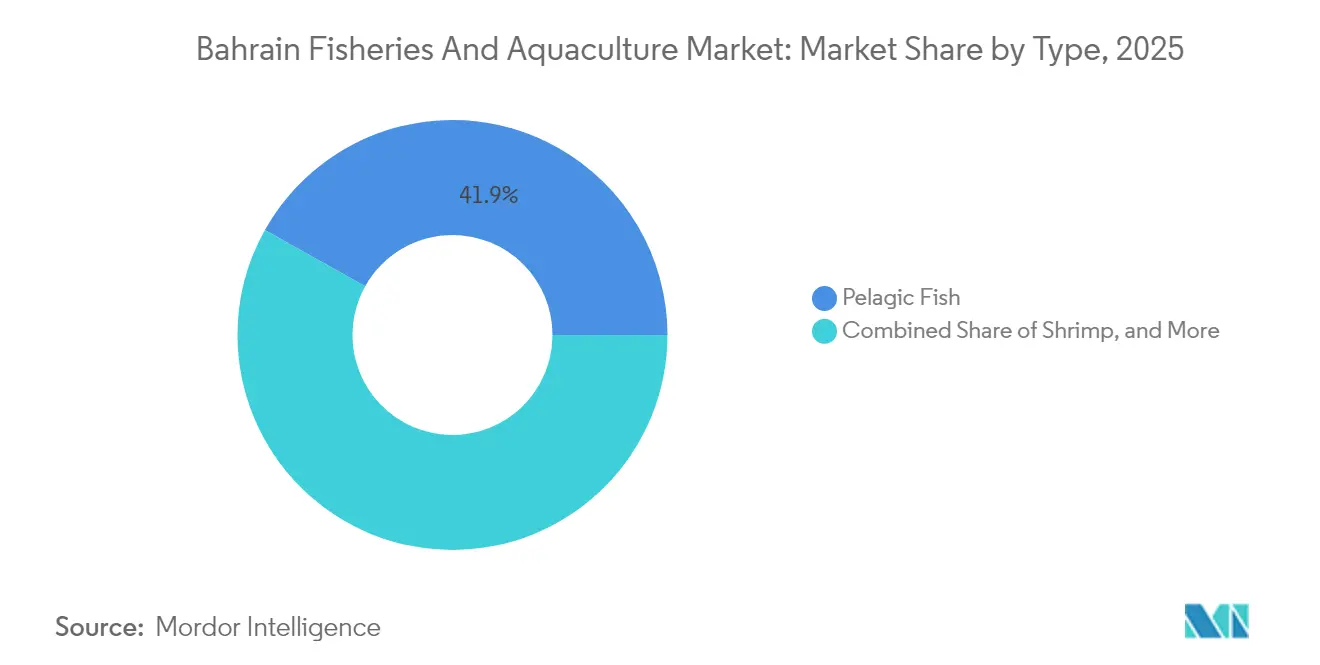

- By type, pelagic fish captured 41.88% of the Bahrain fisheries and aquaculture market share in 2025, while shrimp is forecast to expand at a 9.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bahrain Fisheries And Aquaculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government food-security subsidies for aquaculture expansion | +1.2% | National and Southern Governorate | Medium term (2-4 years) |

| Rising domestic seafood consumption driven by health awareness | +0.8% | Manama and Muharraq | Long term (≥ 4 years) |

| Advances in aquaculture technology | +1.0% | National pilot sites | Medium term (2-4 years) |

| Growing GCC demand for premium Bahraini shrimp and tuna exports | +0.9% | Saudi Arabia, UAE, Kuwait, and Qatar | Short term (≤ 2 years) |

| Repurposing industrial seawater infrastructure for low-cost grow-out | +0.7% | Sitra and Al Dur | Medium term (2-4 years) |

| Blockchain-based halal traceability platform rollout | +0.4% | GCC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Food-Security Subsidies for Aquaculture Expansion

The Supreme Council for Environment finalized a subsidy framework in February 2025 that reimburses up to 60% of capital expenditures for recirculating aquaculture systems, hatchery equipment, and biosecurity upgrades[1]Source: Bahrain News Agency, “Supreme Council for Environment Launches Aquaculture Subsidy Framework,” BNA.BH. The scheme aims to achieve an annual output of 9,250 metric tons and 50–62% seafood self-sufficiency, thereby directly offsetting Bahrain’s reliance on imports for its protein intake. Training delivered through the Ras Hayyan National Aquaculture Centre and Tamkeen equips 15–20 entrepreneurs each year with feed-conversion and pond-management skills. Four Food and Agriculture Organization technical cooperation agreements signed in 2024 include disease surveillance data, climate-resilient species screening, and genetic programs for rabbitfish and grouper. Mandatory ISO 22000 compliance incorporates traceability and hazard analysis controls into farm design from the outset.

Rising Domestic Seafood Consumption Driven by Health Awareness

Per-capita seafood intake continues to climb as the Ministry of Health’s 2024 dietary guidelines recommend three weekly servings of fish. Urban households in Manama and Muharraq now favor sashimi-grade tuna and ceviche-ready shrimp, while cold-chain investments by Banader Fish Processing enable same-day island-wide delivery. The export ban redirects premium pelagic landings into local channels, broadening access and moderating prices for middle-income buyers. Cold-store utilization in Manama’s wholesale district increased in 2024, underscoring a robust domestic demand. Social-media health content amplifies consumer awareness, strengthening demand for lean marine protein.

Advances in Aquaculture Technology

Recirculating systems equipped with biofloc reactors and sensor-based monitoring are now operational at Alba Fish Farm, achieving stocking densities of up to 60 kg/m³, triple the benchmark of open-pond systems, while reducing freshwater use. Bahrain Petroleum Company’s 2024 study integrates shrimp hatcheries with GE mobile desalination units, leveraging waste heat and brine streams. Oxygen-injection systems and IoT-enabled ammonia alerts have lowered grouper mortality. Tamkeen training modules on biofloc and diagnostics reduce dependence on expatriate technicians. Initial blockchain pilots attach QR codes that link farm GPS data and feed batches, meeting GCC halal rules and capturing shelf-price premiums in Saudi retailers[2]Source: Gulf Cooperation Council Standardization Organization, “Halal Certification Requirements for Seafood,” GSO.ORG.SA.

Growing GCC Demand for Premium Bahraini Shrimp and Tuna Exports

Aquaculture-origin shrimp and tuna remain export-eligible, and GCC neighbors represent a USD 2.3 billion seafood opportunity growing at double-digit rates. “Gulf White Shrimp” secures price premiums over Indian and Thai supply due to four-hour truck transit to Dammam and recognized halal credentials. Shell Fisheries Company commands Japan’s blue swimming crab imports and uses the same EU-certified plant for GCC shipments. The 2024 New Zealand-GCC free-trade pact will eventually bring duty-free salmon and mussels, heightening competitive pressure but validating the region’s appetite for traceable, sustainable seafood.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Overfishing pressure within Bahrain’s limited Exclusive Economic Zone | -0.9% | Northern fishing grounds | Short term (≤ 2 years) |

| Dependence on imported feed and fingerlings | -0.6% | All operators | Medium term (2-4 years) |

| Summer brackish-water disease outbreaks in pond farms | -0.5% | Southern pond clusters | Short term (≤ 2 years) |

| Seasonal government shrimp-catch ban disrupting processors | -0.4% | National processors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Overfishing Pressure Within Bahrain’s Limited Exclusive Economic Zone

Bahrain’s 8,000 km² EEZ has seen a drop in licensed fishers since 2020 and a fall in total catch, driven by grouper, emperor, and trevally depletion. Salinity exceeding 55 psu near Al Dur and summer water temperatures above 38 °C hinder reproduction, prompting fleets to venture into contested Qatari and Saudi waters. Enforcement remains thin, with only four patrol vessels for a 161 km coastline. The loss of mangroves has removed critical habitats for juvenile fish. The 2024 wild-catch export ban aims to rebuild stocks, but it also squeezes artisanal income.

Dependence on Imported Feed and Fingerlings

Over 90% of formulated feed and all shrimp post-larvae originate from Thailand, India, and Saudi Arabia, making operators vulnerable to freight disruptions and currency fluctuations[3]Source: International Maritime Organization, “Red Sea Shipping Disruptions and Freight-Rate Impacts,” IMO.ORG.. The 2024 Red Sea rerouting added 18 shipping days and increased landed feed costs by 20%. Ras Hayyan’s hatchery lacks the scale to supply shrimp juveniles, and alternative insect-meal proteins flagged by the World Bank remain nascent. Dollar peg stability softens the risk of the Bahraini dinar, but invoices in Thai baht and Indian rupees expose smaller farms to unhedged exchange rate movements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Pelagic Dominance Masks Shrimp’s Structural Shift

Pelagic fish contributed 41.88% to Bahrain fisheries and aquaculture market share in 2025, driven by sardine, mackerel, tuna, and barracuda landings that feed both retail and processing channels. Shrimp is scaling fastest at a 9.56% CAGR through 2031 as recirculating tanks tied to industrial outfalls slash energy and water costs. The Bahrain fisheries and aquaculture market size, driven by shrimp, is projected to expand sharply as hatcheries implement biosecurity upgrades and blockchain-verified exports secure GCC premiums. Pelagic supply growth will flatten once domestic demand absorbs redirected wild-catch volumes, while tuna continues to find niche opportunities in sashimi-grade domestic segments.

Demersal species, including grouper, trevally, emperor, and pomfret, face overfishing and habitat stress, limiting their future share. Niche categories, such as scallops, lobster, and caviar, each account for less than 3% of the value but offer diversification for operators investing in suspended-culture cages and controlled hatcheries. The “other” group, cuttlefish, jellyfish, and ribbon fish, leverages Shell Fisheries Company’s frozen export lines to Japan, demonstrating that value-added processing can circumvent local volume constraints. Blockchain traceability in these specialties strengthens halal claims, positioning Bahrain as a premium supplier in Saudi and Emirati supermarkets.

Geography Analysis

All commercial activity in the Bahrain fisheries and aquaculture market unfolds within a densely populated 765 km² island and along 161 km of coastline, concentrating competition for marine and industrial zone space. The Southern Governorate hosts approximately 70% of the national farming capacity, anchored by Ras Hayyan and Alba Fish Farm, which utilizes 300,000 m³/day of pre-filtered industrial seawater and achieves a stocking density of up to 60 kg/m³. These cost advantages underpin the governorate’s projected growth through 2030 and cement its lead in the Bahrain fisheries and aquaculture market size.

The Northern Governorate and Muharraq harbor the majority of artisanal fleets and cold stores that supply Manama’s wholesale hub. Cold-store utilization increased in 2024, as the export ban redirected pelagic volumes to the domestic market. Rising urban demand shortens inventory turnover and encourages processors to retrofit blast-freezers for higher-value chilled lines. Marine heatwaves in 2022 and 2023 forced fishers farther offshore, inflating fuel costs and reducing harvest windows.

The Capital Governorate drives consumption growth among health-conscious urban consumers who follow the Ministry of Health dietary guidelines. Retailers expanded their seafood aisles and introduced same-day delivery using upgraded cold vans. Adjacent wastewater-reclamation projects in Muharraq target inland aquaponics, pending approval for food-grade use. Coastal zoning rules now prioritize aquaculture over recreational developments, ensuring site availability for future recirculating facilities even as residential expansion pressures shoreline land values.

Competitive Landscape

Fifteen registered operators compete for a share of the Bahrain fisheries and aquaculture market, with no single firm exceeding 20% of the domestic revenue. Shell Fisheries Company operates a European Union-specification plant and holds the majority market share of Japan’s blue swimming crab imports, providing it with scale and export expertise. Banader Fish Processing focuses on chilled domestic distribution, while Alba Fish Farm leverages industrial outfalls to slash water-handling costs by 40%. The 2024 subsidy framework ties funding to ISO 22000 certification, accelerating consolidation as under-capitalized players exit or merge.

Technology adoption remains uneven. Fewer than 5% of farms deploy real-time water-quality sensors or blockchain traceability, leaving most reliant on manual logs. Early adopters gain a marketing edge and quicker customs clearance for GCC exports. Patent filings at the GCC Patent Office remain negligible, indicating reliance on imported know-how. Partnerships with FAO and Tamkeen aim to localize disease-surveillance capacity and genetic-improvement programs, but material productivity gains are unlikely before 2027.

The New Zealand-GCC free-trade pact, which phases in duty-free salmon and mussels, heightens pressure on domestic players to differentiate themselves through halal traceability, freshness, and shorter supply chains. Processors respond by upgrading blast-freezers, investing in modified-atmosphere packaging, and marketing provenance stories of Bahrain's fisheries and aquaculture market to GCC retailers. Industrial symbiosis models that integrate farming into refinery and smelter water circuits promise cost leadership and are attracting private-equity interest.

Recent Industry Developments

- March 2024: Bahrain's Marine Resources Directorate implemented a comprehensive export ban on all fish and shrimp caught in territorial waters, reversing decades of export-led growth to prioritize domestic food security.

- February 2022: The government placed a ban on the catching, trading, and selling of shrimp, which was in effect until July 31, 2022. This decision aimed to preserve marine wealth in a manner that contributes to the development of the shrimping industry and the protection of fish stocks in the Kingdom of Bahrain.

- January 2022: In partnership with the Professional Fishermen's Society, the Government of Bahrain has charted plans to develop the country's fishing sector. The aim was to launch initiatives that support Bahraini fishermen, in particular, and the fishing profession, in general.

Bahrain Fisheries And Aquaculture Market Report Scope

Fisheries can be defined as raising and harvesting wild marine and freshwater fish for food or industrial purposes. The commercial production of aquatic species, namely fish, and other edible aquatic species produced through the country's fisheries and aquaculture sector have been considered for the purpose of the market study. The Bahrain Fisheries and Aquaculture Sector is segmented by Type (Pelagic Fish, Demersal Fish, Freshwater Fish, Scallop, Shrimp, Lobsters, Caviar, and Other Types). The study includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Export Analysis (Value and Volume), Import Analysis (Value and Volume), and Price Trend Analysis. The Report Offers the Market Size and Forecasts in Terms of Value in (USD) and Volume in (Metric Tons) for all the Above Segments.

By Type ( (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis)

| Pelagic Fish | Sardines |

| Mackerel | |

| Tuna | |

| Barracuda | |

| Demersal Fish | Grouper |

| Trevally | |

| Emperor | |

| Pomfret | |

| Freshwater Fish | |

| Scallop | |

| Shrimp | |

| Lobster | |

| Caviar | |

| Other Types |

| By Type ( (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis) | Pelagic Fish | Sardines |

| Mackerel | ||

| Tuna | ||

| Barracuda | ||

| Demersal Fish | Grouper | |

| Trevally | ||

| Emperor | ||

| Pomfret | ||

| Freshwater Fish | ||

| Scallop | ||

| Shrimp | ||

| Lobster | ||

| Caviar | ||

| Other Types | ||

Key Questions Answered in the Report

How large is the Bahrain fisheries and aquaculture market in 2026?

It is valued at USD 453.64 million and is projected to reach USD 590.72 million by 2031 at a 5.43% CAGR. Which segment is growing fastest in Bahrain's seafood sector? Shrimp leads with a 9.56% CAGR through 2031, driven by recirculating systems tied to industrial seawater outfalls. What government policy most impacts domestic supply? The March 2024 export ban on wild-caught fish and shrimp redirected premium pelagic catch to local retailers, boosting domestic availability. How are Bahraini processors differentiating against imported salmon and mussels? Firms are adopting blockchain-verified halal traceability, shorter GCC supply chains, and value-added chilled formats. What limits further aquaculture expansion? Dependence on imported feed and post-larvae, disease risks in summer pond systems, and overfished natural stocks constrain growth. Where is most new farming capacity located? The Southern Governorate, especially sites adjacent to Aluminium Bahrain and Bahrain Petroleum Company industrial outfalls, hosts about 70% of new capacity.

Which segment is growing fastest in Bahrain's seed food sector?

Shrimp leads with a 9.56% CAGR through 2031, driven by recirculating systems tied to industrial seawater outfalls. What government policy most impacts domestic supply? The March 2024 export ban on wild-caught fish and shrimp redirected premium pelagic catch to local retailers, boosting domestic availability. How are Bahraini processors differentiating against imported salmon and mussels? Firms are adopting blockchain-verified halal traceability, shorter GCC supply chains, and value-added chilled formats. What limits further aquaculture expansion? Dependence on imported feed and post-larvae, disease risks in summer pond systems, and overfished natural stocks constrain growth. Where is most new farming capacity located? The Southern Governorate, especially sites adjacent to Aluminium Bahrain and Bahrain Petroleum Company industrial outfalls, hosts about 70% of new capacity.

What government policy most impacts domestic supply?

The March 2024 export ban on wild-caught fish and shrimp redirected premium pelagic catch to local retailers, boosting domestic availability.

Why are Bahraini processors differentiating against imported salmon and mussels?

Firms are adopting blockchain-verified halal traceability, shorter GCC supply chains, and value-added chilled formats. What limits further aquaculture expansion? Dependence on imported feed and post-larvae, disease risks in summer pond systems, and overfished natural stocks constrain growth. Where is most new farming capacity located? The Southern Governorate, especially sites adjacent to Aluminium Bahrain and Bahrain Petroleum Company industrial outfalls, hosts about 70% of new capacity.

What limits further aquaculture expansion?

Dependence on imported feed and post-larvae, disease risks in summer pond systems, and overfished natural stocks constrain growth.

Where is most new farming capacity located?

The Southern Governorate, especially sites adjacent to Aluminium Bahrain and Bahrain Petroleum Company industrial outfalls, hosts about 70% of new capacity.

Page last updated on: