Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

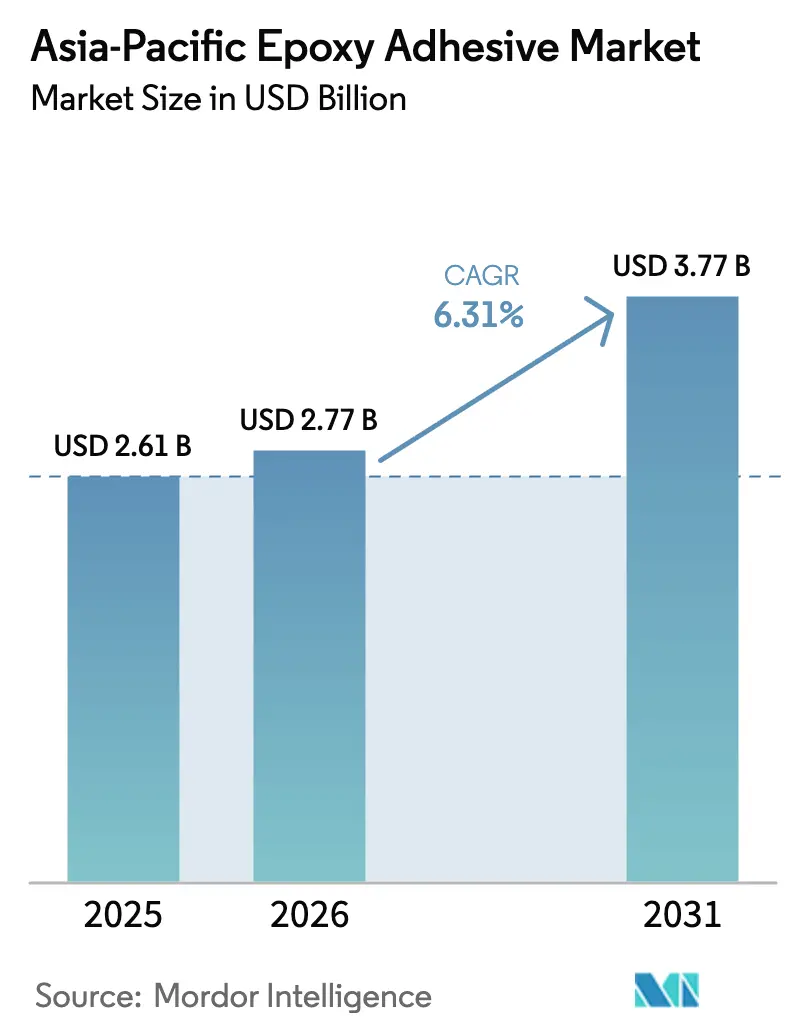

| Base Year Market Size (2025) | USD 2.61 Billion |

| Market Size (2026) | USD 2.77 Billion |

| Market Size (2031) | USD 3.77 Billion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

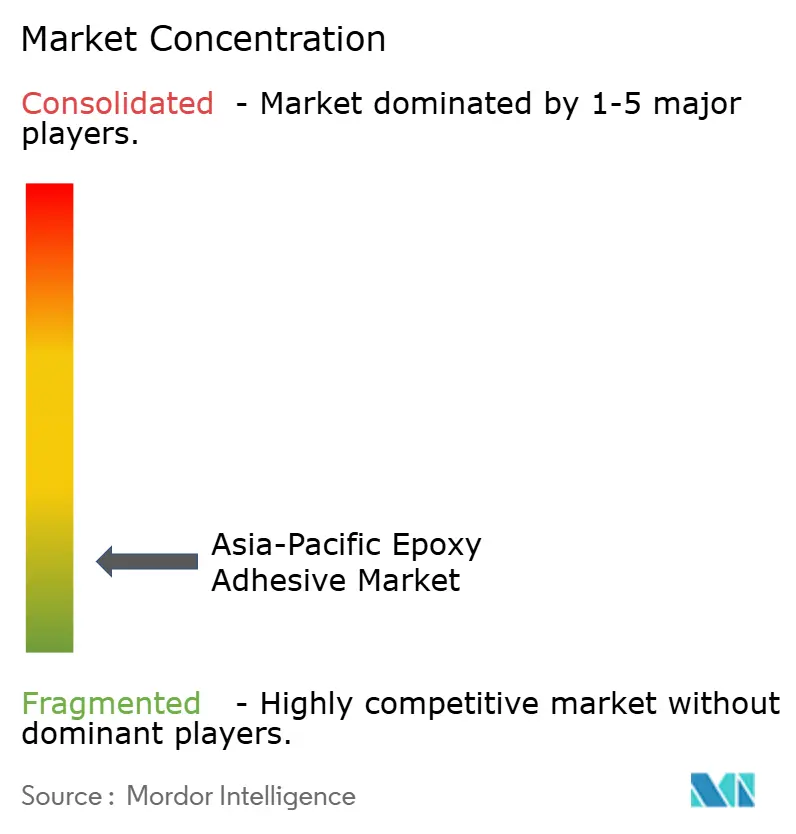

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Epoxy Adhesive Market Analysis by Mordor Intelligence

The Asia-Pacific epoxy adhesives market size is expected to grow from USD 2.61 billion in 2025 to USD 2.77 billion in 2026 and is forecast to reach USD 3.77 billion by 2031 at 6.31% CAGR over 2026-2031. Steady electrification of transport, an upturn in semiconductor packaging investments, and record urban infrastructure spending are converging to lift structural bonding demand across the region, allowing the Asia-Pacific epoxy adhesives market to outpace global averages. Two-component reactive systems continue to command pricing power as vehicle makers replace welding with lightweight composite bonding, while stringent indoor-air-quality rules are steering construction projects toward low-VOC hardeners that cure at near-ambient temperatures. Major chemical suppliers are scaling regional laboratories to shorten formulation cycles for electric-vehicle batteries, photonics chiplets, and high-rise façade panels, a shift that tilts competitive advantage toward firms with local application-engineering depth.

Key Report Takeaways

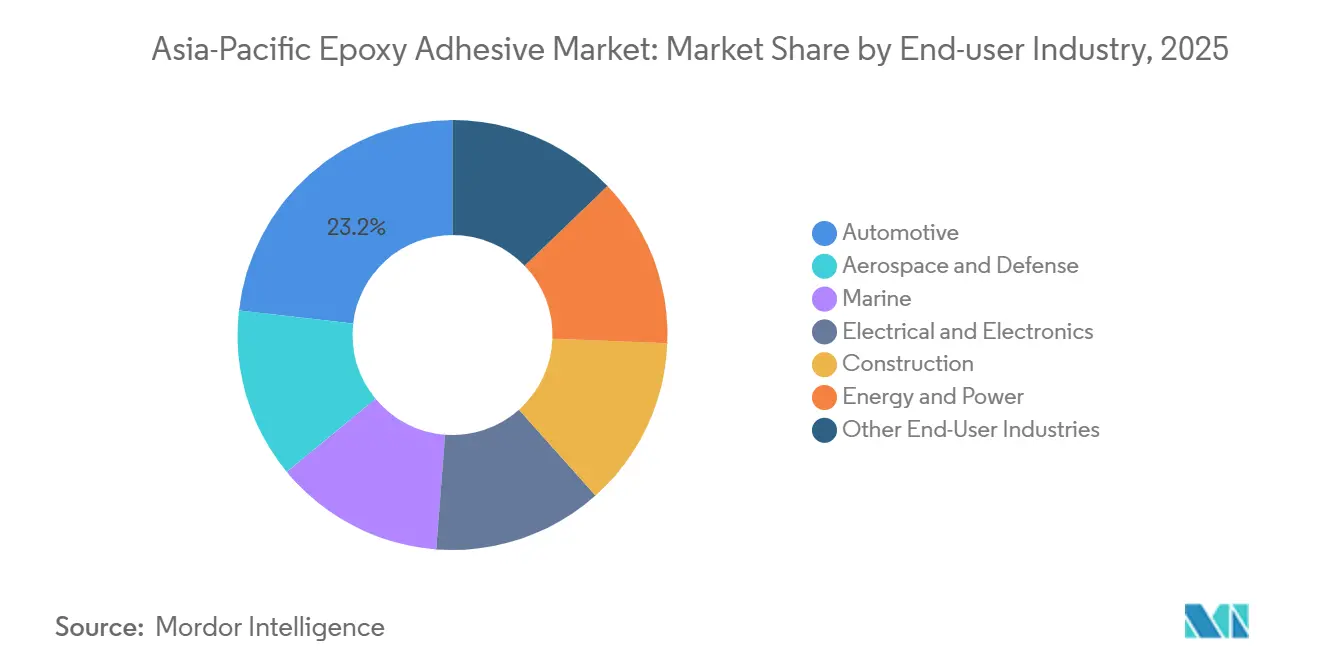

- By end-user, automotive captured 23.18% of Asia-Pacific epoxy adhesives market share in 2025, whereas electrical and electronics is advancing at a 6.58% CAGR during the forecast period (2026-2031).

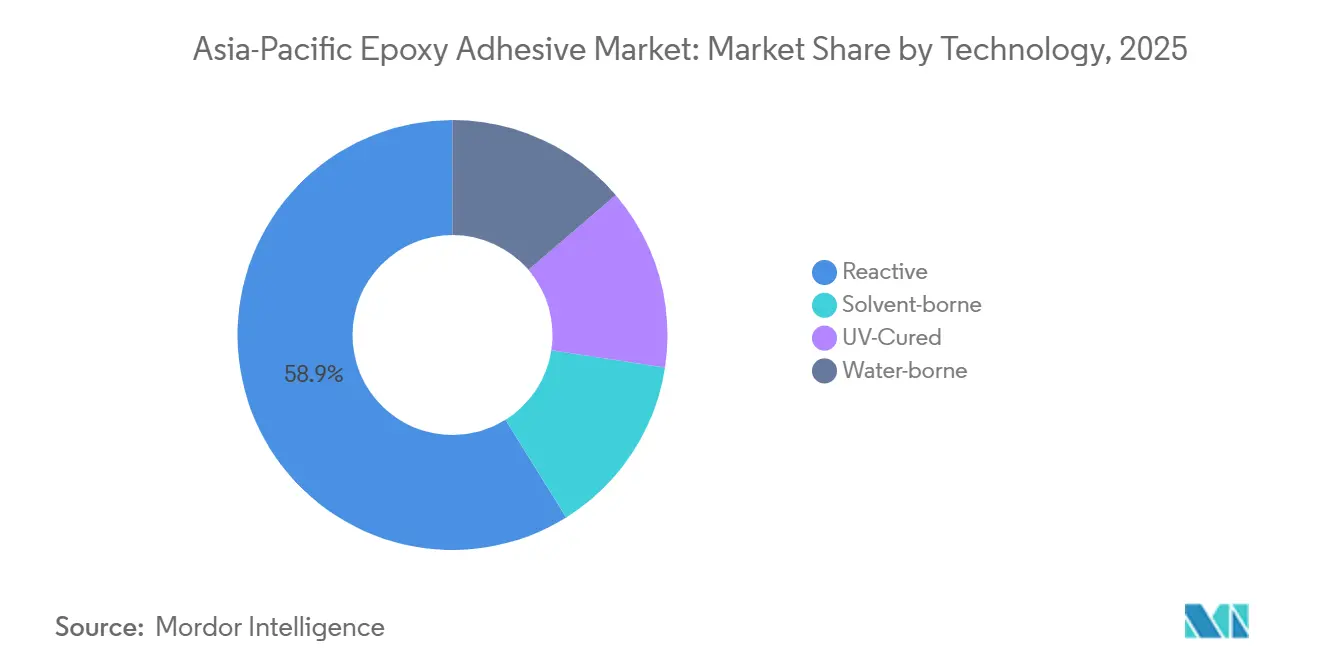

- By technology, reactive formulations held 58.87% of the Asia-Pacific epoxy adhesives market size in 2025; water-borne grades posted the quickest 6.2% CAGR during the forecast period (2026-2031).

- By country, China led with 44.12% of Asia-Pacific epoxy adhesives market share in 2025, while India is expanding at a 7.14% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Epoxy Adhesive Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in EV and lightweight automotive manufacturing | +1.8% | China, Japan, South Korea, India, Thailand, Indonesia | Medium term (2-4 years) |

| Rapid infrastructure and high-rise construction spending | +1.5% | China, India, Indonesia, Vietnam, Malaysia | Long term (≥ 4 years) |

| Expansion of electronics and semiconductor assembly | +1.6% | Taiwan, South Korea, China, Malaysia, Singapore | Short term (≤ 2 years) |

| Domestic aircraft programs adopt localized qualifications | +0.9% | China, Japan, India, South Korea | Long term (≥ 4 years) |

| Anti-dumping tariffs spurring backward integration | +0.7% | China, India, ASEAN core | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging EV And Lightweight Automotive Output

In the Asia-Pacific region, electric vehicle plants are increasingly turning to adhesive solutions for various components, including battery modules, cell-to-pack systems, and aluminum-composite body panels. This trend is bolstering the region's epoxy adhesives market, especially as original-equipment manufacturers aim to reduce curb weight by 15-20%. Major investments from industry giants like BYD, Hyundai, and LG Energy Solution are driving a multi-gigawatt-hour battery capacity. These batteries rely on gap-filling epoxies known for their high thermal conductivity and rapid green strength. Additionally, a newly commercialized silver-paste epoxy, which can be stored at room temperature for up to six months, is revolutionizing the production of silicon-carbide power modules. By eliminating the traditional sintering steps, this innovation not only streamlines inverter production but also reduces energy consumption by as much as 40%.

Rapid Infrastructure And High-Rise Construction

In 2025, governments across the Asia-Pacific region invested over USD 5 trillion in construction. This surge in urbanization heightened the demand for products like façade glazing, anchor grouts, and repair mortars, all of which depend on high-toughness epoxies. Additionally, a newly introduced low-temperature hardener, capable of curing between 5 °C and 10 °C, is revolutionizing winter concreting. This innovation is particularly beneficial for northern China's construction and India's high-altitude rail projects, eliminating the need for expensive heating blankets.

Expansion Of Electronics And Semiconductor Assembly

At a rapid pace, Asia-Pacific is establishing advanced-packaging cleanrooms. This surge is steering the region's epoxy adhesives market towards die-attach films, capillary underfills, and ultraviolet-curing grades that achieve full strength in just ten seconds. In Singapore and Penang, regional labs are enabling formulators to evaluate halogen-free, low-ionic additives. These additives meet the JEDEC reliability standards for both 2.5D and 3D chip stacks.

Anti-Dumping Tariffs Spurring Backward Integration

In India and Vietnam, the introduction of new mixing and packaging facilities has been driven by 20-40% duties on imported formulated epoxies. These facilities have managed to reduce lead times from twelve weeks to under four. Additionally, they benefit from the "Make-in-India" initiative, which offers reimbursements of up to 4% of the ex-factory value for locally sourced chemistries.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile BPA and ECH feedstock prices | -0.8% | Global, acute in China, Japan, India | Short term (≤ 2 years) |

| Stringent VOC and IAQ regulations on solvent systems | -0.6% | China, Singapore, Australia, Japan | Medium term (2-4 years) |

| Performance gap and cost premium of water-borne epoxies | -0.5% | China, India, ASEAN manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility In Bisphenol A And Epichlorohydrin Feedstocks

Mid-tier mixers, lacking long-term resin contracts, face margin compression due to quarterly price swings exceeding 20%. As a restraint, several processors in Southeast Asia are turning to bio-based epoxies. These epoxies, sourced from rosin and cardanol, boast glass-transition temperatures surpassing 230 °C, albeit at a 30% price premium.

Stringent VOC And Indoor-Air-Quality Regulations

China's GB 33372-2020 regulation limits solvent content in epoxy adhesives to 100 to 200 g/kg. This move is pushing manufacturers to pivot towards reactive or water-borne products[1]Standardization Administration of China, “GB 33372-2020: Limits of Harmful Substances in Adhesives,” sac.gov.cn. In Singapore, the Green Building Masterplan, alongside Australia's Green Star tools, is bolstering the demand for formulations. These formulations must ensure their total VOC emissions are below the 50 µg/m³ benchmark. Notably, the new low-temperature Baxxodur® hardener not only meets this stringent threshold but also reduces cure times by an impressive two-thirds[2]BASF, “Baxxodur® EC 151 Technical Bulletin,” basf.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Electronics Outpaces Automotive

Electronics and semiconductor applications are expanding at a rate of 6.58% CAGR. This segment is surpassing the automotive sector as fabs for power devices and photonic modules emerge across regions, including Hsinchu and Kulim. The automotive sector, however, remains the largest contributor, holding a 23.18% share. The Asia-Pacific epoxy adhesives market within this segment continues to grow, driven by applications in vehicle structures, battery packs, and powertrains.

The high-frequency gallium-nitride and silicon-carbide devices segment is fueling demand for silver-filled epoxies with bulk thermal conductivity exceeding 150 W/m-K. This trend is strengthening R&D collaborations between chemical suppliers and substrate manufacturers. Additionally, the construction, energy, and marine segments collectively maintain steady demand. Government investments in infrastructure are focusing on projects such as bridges, wind blades, and hull refurbishments, all of which require high-modulus bonding.

By Technology: Reactive Dominates Despite Water-Borne Push

In 2025, reactive two-part systems commanded a dominant 58.87% share of the Asia-Pacific epoxy adhesives market. Their success can be attributed to their ambient storage stability and rapid mechanical build-up, which align perfectly with the speed targets of the auto and rail industries. While water-borne chemistries are making the fastest strides in the market, they face challenges. Issues like pot-life and moisture tolerance restrict their use in assets exposed to varying climates, resulting in a modest market size for these grades in the Asia-Pacific region.

Ultraviolet-cured epoxies, are making inroads into applications like camera modules and fingerprint sensors. Their ten-second curing time is ideal for high-volume pick-and-place operations. Meanwhile, dual-cure variants, which merge UV initiation with latent thermal agents, are finding applications in sensor housings and fiber-optic connectors. These areas, often containing shadowed zones, highlight the industry's shift towards hybrid cure mechanisms.

Geography Analysis

China dominates the Asia-Pacific epoxy adhesives market with a 44.12% share in 2025, bolstered by its strong foothold in automotive, Printed Circuit Board (PCB), and major public-works projects. However, varying compliance standards across provinces compel suppliers to produce multiple VOC-compliant variants for a single jobsite. Meanwhile, India's 'Make-in-India' initiative is rapidly advancing cell-to-pack lines and smartphone assembly hubs. This surge is leading to six-year adhesive supply contracts, favoring formulators who invest in local resin storage.

Japan and South Korea focus on premium segments, particularly in power semiconductors and hydrogen-fuel platforms. This focus has led to the introduction of silver-paste die-attach materials, which cure below 200 °C and are designed to endure 25 years of thermal cycling. In the ASEAN region, the localization of electronics, solar-module, and rolling-stock plants has created a diverse demand pool. This diversification mitigates risks associated with reliance on a single country, ensuring a steady upward trend for the Asia-Pacific epoxy adhesives market.

Australia's ongoing projects in offshore wind, lithium mining, and modular housing sustain a steady import flow. Concurrently, Taiwan's advanced packaging sectors drive demand for ultra-low-ionic epoxies, which meet the stringent JEDEC Level 3 standard at 260 °C. These dynamics solidify the Asia-Pacific's position as the global leader in specialty adhesive chemistries.

Competitive Landscape

The Asia-Pacific epoxy adhesives market is fragmented in nature. In 2026, Henkel opened Southeast Asia’s largest application lab in Singapore, allowing a swift 48-hour prototype turnaround on PFAS-free electronics grades. In 2025, Sika and BASF rolled out a joint innovation: a low-temperature, low-VOC hardener that cuts floor-coating cycle times by two-thirds, proving invaluable for winter concreting in northern regions.

Regional players are also on the rise. Pidilite, in collaboration with CollTech, is establishing an electronics-adhesive hub in Bangalore, eyeing a slice of the USD 1 billion EV and semiconductor pie by 2030. Meanwhile, Taiwan's Nan Pao has teamed up with Advanced Echem to co-create underfills tailored for high-density interposers. The M&A landscape is buzzing: Arkema took over Dow’s flexible-packaging lamination unit in 2024, and H.B. Fuller acquired HS Butyl, enhancing their waterproofing tape offerings and expanding distribution channels.

Current innovation trends spotlight bio-derived resins, ultra-high-thermal-conductivity fillers, and halogen-free fire-retardant solutions. Suppliers integrating local production with on-ground service teams are poised for success, as clients increasingly prefer timely deliveries that sidestep shipping delays and tariff challenges.

Asia-Pacific Epoxy Adhesive Industry Leaders

3M

H.B. Fuller Company

Henkel AG & Co. KGaA

Sika AG

Huntsman International LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Henkel opened a Singapore hub featuring Southeast Asia’s largest electronic-adhesives application lab, with pilot lines designed for photonics chiplets and PFAS-free formulations.

- March 2025: BASF and Sika released Baxxodur EC 151, a low-VOC hardener curing at 5-10 °C for winter construction.

Asia-Pacific Epoxy Adhesive Market Report Scope

Epoxy adhesives are a high-strength, two-part adhesive consisting of a resin and a hardener that, when mixed, cures into a rigid, durable, and waterproof polymer. It excels at bonding, sealing, and filling gaps between diverse materials like metal, wood, and glass. Epoxy is renowned for its superior resistance to chemicals, moisture, and extreme temperatures.

The Asia-Pacific Epoxy Adhesives market report is segmented by technology, end-user industry, and geography. By end-user industry, the market is segmented into aerospace and defense, automotive, marine, electrical and electronics, construction, energy and power, and other end-user industries. By technology, the market is segmented into reactive, solvent-borne, uv-cured, and water-borne. The report also covers the market size and forecasts for epoxy adhesives in 9 countries across the Asia-Pacific region. For each segemnt market sizing and forecasts are provided in terms of value (USD).

By End-User Industry

| Aerospace and Defense |

| Automotive |

| Marine |

| Electrical and Electronics |

| Construction |

| Energy and Power |

| Other End-User Industries |

By Technology

| Reactive |

| Solvent-borne |

| UV-Cured |

| Water-borne |

By Country

| Australia |

| China |

| India |

| Indonesia |

| Japan |

| Malaysia |

| Singapore |

| South Korea |

| Thailand |

| Rest of Asia-Pacific |

| By End-User Industry | Aerospace and Defense |

| Automotive | |

| Marine | |

| Electrical and Electronics | |

| Construction | |

| Energy and Power | |

| Other End-User Industries | |

| By Technology | Reactive |

| Solvent-borne | |

| UV-Cured | |

| Water-borne | |

| By Country | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Malaysia | |

| Singapore | |

| South Korea | |

| Thailand | |

| Rest of Asia-Pacific |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the epoxy adhesives market.

- Product - All epoxy adhesive products are considered in the market studied

- Resin - Under the scope of the study, one component and two component based epoxies are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms