Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

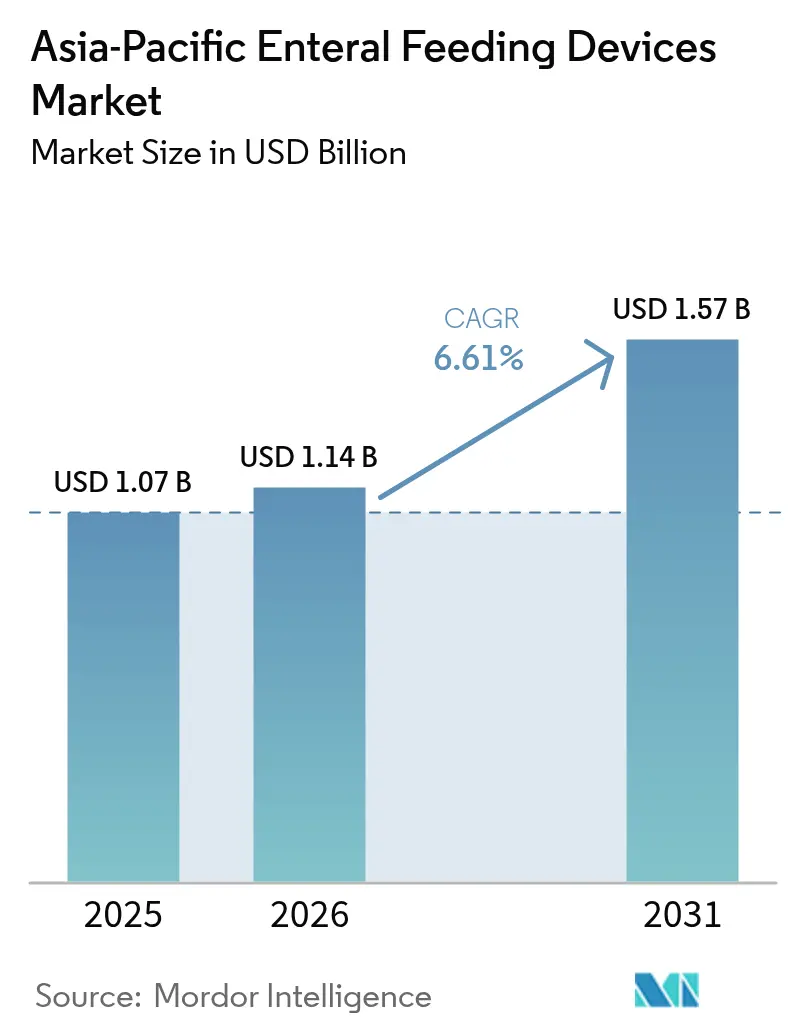

| Base Year Market Size (2025) | USD 1.07 Billion |

| Market Size (2026) | USD 1.14 Billion |

| Market Size (2031) | USD 1.57 Billion |

| Growth Rate (2026 - 2031) | 6.61% CAGR |

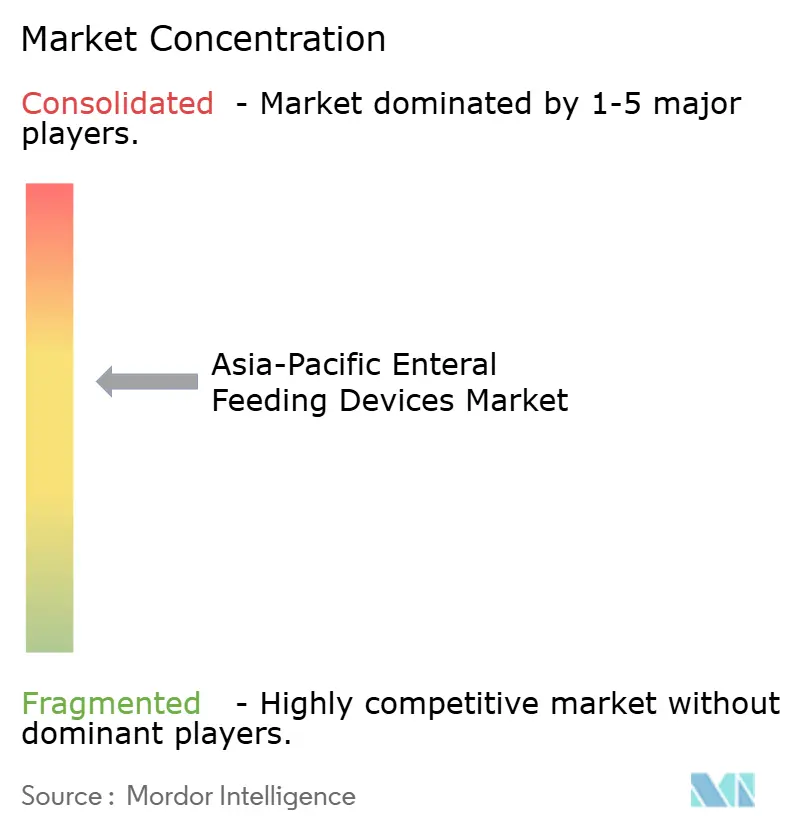

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Enteral Feeding Devices Market Analysis by Mordor Intelligence

Asia Pacific enteral feeding devices market size in 2026 is estimated at USD 1.14 billion, growing from 2025 value of USD 1.07 billion with 2031 projections showing USD 1.57 billion, growing at 6.61% CAGR over 2026-2031. Rising life expectancy, strong growth in chronic disease incidence, and accelerated hospital‐capacity expansion underpin this steady trajectory. An ageing demographic is especially influential; people aged 60 and older will account for 22.2% of ASEAN’s population by 2050, reinforcing demand for long-term nutritional support. Providers are pivoting toward connected feeding pumps that integrate with telehealth platforms, while governments encourage indigenous production to lower costs, particularly in India where locally manufactured devices may be priced 50% below imports. Investment in medical infrastructure also remains robust: ASEAN healthcare spending climbed 42% in the five years to 2021, creating additional headroom for equipment upgrades and replacement cycles. Competitive intensity is moderate, but product innovation—such as camera-guided tube placement and wireless pump monitoring—has emerged as the primary differentiator rather than price alone.

Key Report Takeaways

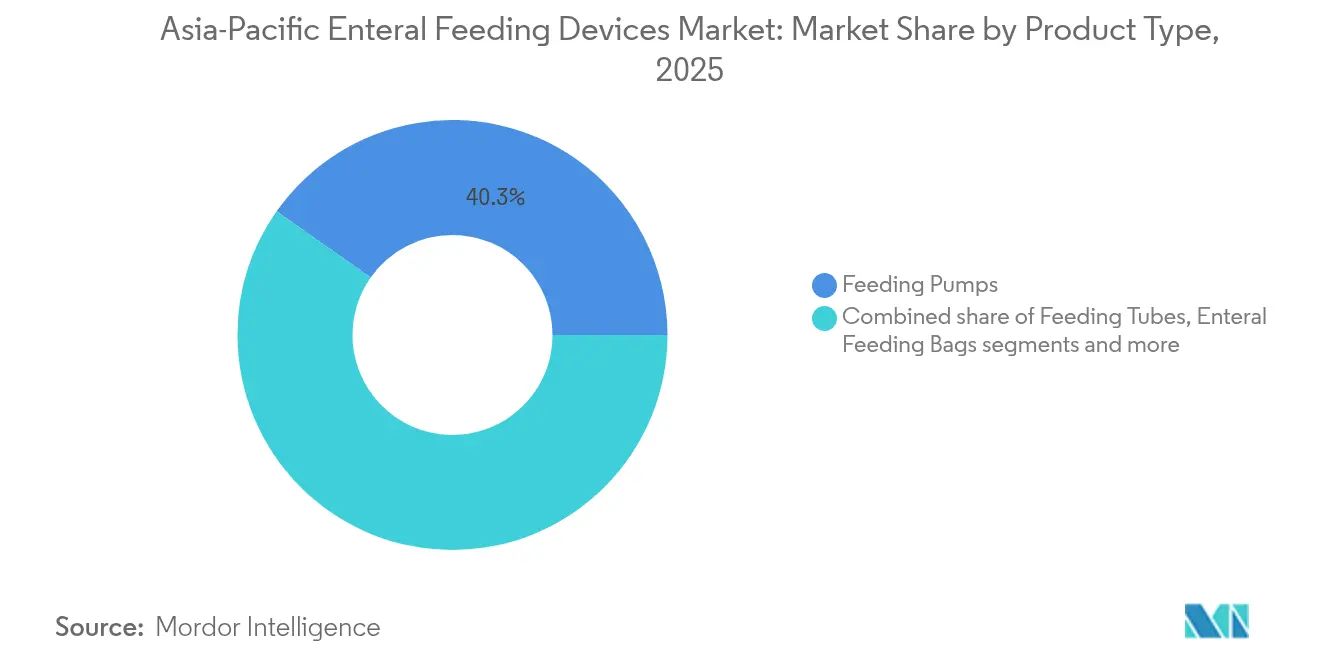

- By product type, feeding pumps led with 40.25% of the Asia Pacific enteral feeding devices market share in 2025, while feeding tubes are projected to expand at a 7.62% CAGR through 2031.

- By age group, adults accounted for 72.94% of the Asia Pacific enteral feeding devices market size in 2025; pediatric & neonatal care is the fastest‐growing cohort at 7.86% CAGR to 2031.

- By distribution channel, offline sales commanded 85.72% share in 2025; online channels are climbing at 8.05% CAGR thanks to digital procurement platforms.

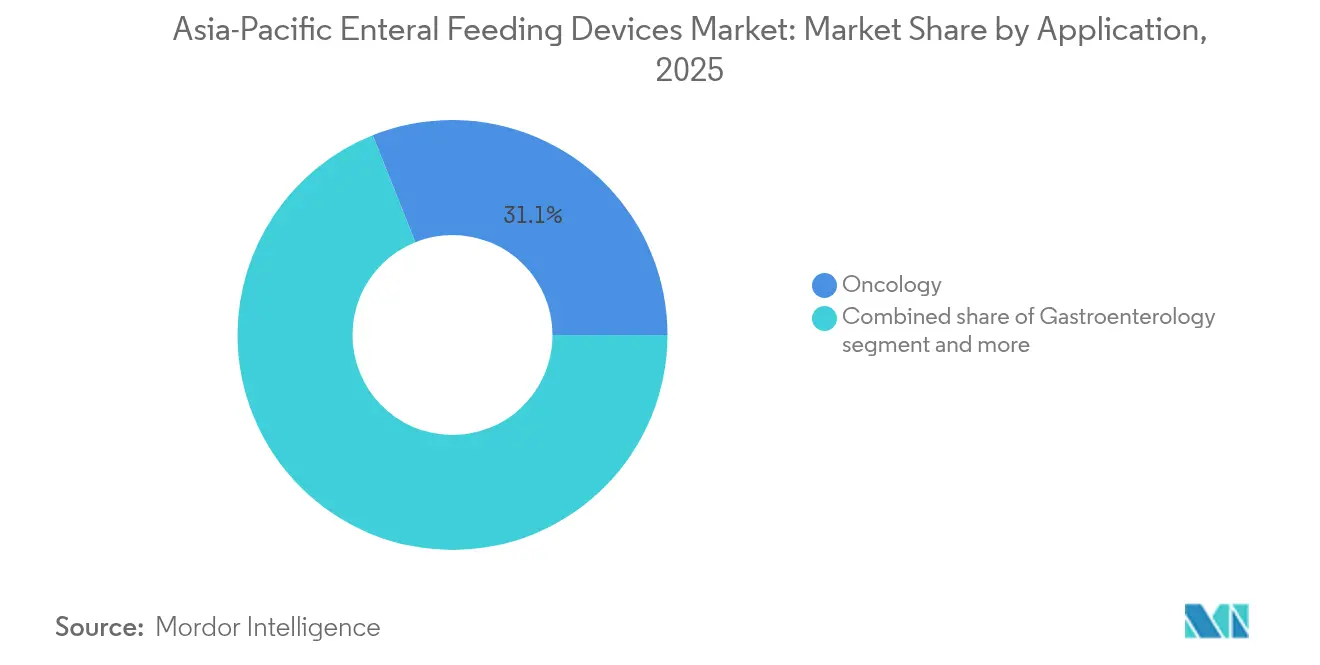

- By application, oncology held 31.05% of the Asia Pacific enteral feeding devices market size in 2025; critical care & trauma is set to grow at a 7.38% CAGR between 2026-2031.

- By end-user, hospitals represented 54.68% of 2025 revenue, while home care settings are growing 7.21% annually.

- By geography, China dominated with 40.88% share in 2025, whereas India is projected to log the highest 7.84% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Enteral Feeding Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Ageing Across East Asia Drives Post-Acute Nutrition Demand | +1.8% | China, Japan, South Korea | Long term (≥ 4 years) |

| Neonatal ICU Capacity Expansion Boosts Premature-Birth Feeding Volumes | +1.2% | India, China, Southeast Asia | Medium term (2-4 years) |

| Home-Based Long-Term Care Reimbursement Reforms in China & Japan | +1.0% | China, Japan | Medium term (2-4 years) |

| Telerehabilitation Protocols Mandate Pump Connectivity | +0.7% | Australia, Singapore, developed APAC | Short term (≤ 2 years) |

| Surge in Gastrointestinal Cancer Surgeries Elevating Post-Operative Tube-Feeding Adoption | +0.6% | China, Japan, India, Australia | Medium term (2-4 years) |

| Military Field-Hospital Procurement in Indo-Pacific | +0.5% | Australia, Japan, South Korea, India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Ageing Across East Asia Drives Post-Acute Nutrition Demand

East Asian health systems already treat malnutrition in 25% of older adults[1]Le Li., “Global patterns of change in the burden of malnutrition in older adults from 1990 to 2021 and the forecast for the next 25 years,” Frontiers in Nutrition, frontiersin.org, and absolute caseloads will rise alongside demographic ageing, reinforcing long-term reliance on enteral feeding solutions. Dysphagia after stroke is a common trigger for device placement, and clinical guidelines from the VA/DoD now recommend enteral nutrition as a standard stroke-recovery intervention. Community screening programs increasingly flag undernutrition, which correlates with 41% higher emergency-department visits[2]Lixia Ge, “Undernutrition and Increased Healthcare Demand: Evidence from a Community-Based Longitudinal Panel Study in Singapore,” Nutrients, mdpi.com and 52% greater inpatient admissions among seniors, intensifying payer focus on early nutritional therapy. As primary-care settings assume greater accountability for geriatric outcomes, demand shifts from hospital-only devices to portable pumps suitable for step-down and home environments. Manufacturers are responding with low-volume precision pumps that minimize aspiration risk while maintaining flow stability over extended use cycles.

Neonatal ICU Capacity Expansion Boosts Premature-Birth Feeding Volumes

Surging NICU bed counts in China, India, and much of Southeast Asia have improved survival for preterm infants, who require highly regulated enteral nutrition[3]Yao-Chi Hsieh., “Contemporary fluid management, humidity, and patent ductus arteriosus management strategy for premature infants among 336 hospitals in Asia,” Frontiers in Pediatrics, frontiersin.org to mitigate growth impairment. Hospitals deploying standardized feeding‐intolerance scoring systems can initiate enteral feeds within 7 days post-surgery, cutting complication rates in necrotizing enterocolitis cases by 17%. Clinical variability among 336 Asian hospitals—especially differences in ventilation and humidity protocols—creates headroom for advanced pumps offering adaptive flow control and real-time gastric-residual monitoring. Suppliers that bundle neonatal-specific tubes with micro-bore connectors stand to gain as care guidelines tighten around tube size, placement accuracy, and cleaning protocols. With governments funding NICU upgrades, procurement budgets increasingly include connected pumps that feed data back to centralized dashboards for audit and quality improvement.

Home-Based Long-Term Care Reimbursement Reforms in China & Japan

Only 40% of Asia Pacific countries reimbursed home enteral nutrition before 2024; that share is rising fast, led by China’s long-term care insurance pilots and Japan’s home-visit fee updates that cover nutritional support supplies. Correlation between national health-expenditure growth and commercial formula use is clear: middle-income markets shifting away from blenderized diets demand ready-to-hang solutions with extended shelf life. Vietnam’s 2024 reforms—streamlining drug registration and lifting insurance coverage[4]Gretchen Kunze, “Vietnam Advances Healthcare Reforms with Legislative and Strategic Initiatives,” US-ASEAN Business Council, usasean.org to 94.1%—signal a broader policy tailwind for home-care devices across ASEAN. Yet most nutrition-support teams remain concentrated in urban hospitals, so suppliers collaborate with visiting-nurse networks to train caregivers on pump programming, sanitation, and troubleshooting.

Telerehabilitation Protocols Mandate Pump Connectivity

Health systems that moved rehabilitation online during COVID-19 now require feeding devices that transmit dosage logs and alarm histories to clinical dashboards. Portable pumps featuring 19-hour battery life and WLAN connectivity integrate with electronic health records to trigger alerts when flow deviations exceed programmed tolerances. Studies across 18 telehealth programs show machine-learning algorithms can predict adverse events and recommend dosage adjustments, enhancing patient engagement while cutting nurse callouts by 14%. Cardinal Health’s Kangaroo Connect Portal exemplifies this model, giving clinicians secure browser access to feeding histories and facilitating remote diagnostics. As reimbursement parity for virtual care takes hold, IoT-ready devices are fast becoming table stakes in the Asia Pacific enteral feeding devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tube-Induced Mucosal Injuries & Infection Risks | -0.9% | Global, particularly developing markets | Long term (≥ 4 years) |

| Reimbursement Caps for Disposable Sets in Asean | -0.6% | ASEAN countries | Medium term (2-4 years) |

| Single-Use Plastic Regulations for Medical Tubing | -0.4% | Australia, Japan, developed APAC | Long term (≥ 4 years) |

| Local OEM Price Wars in India Lower Profitability | -0.3% | India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tube-Induced Mucosal Injuries & Infection Risks

Extended nasogastric placement can distort the epiglottis' shape and narrow the pharynx, particularly when paired with tracheostomy, leading to higher aspiration rates and prolonged hospitalization. HACCP-style monitoring programs reduce total microbial load in formula delivery, yet compliance remains uneven, and no cleaning technique fully eliminates bacterial colonization after 28 days. ISO 80369-3 connectors solve misconnections but not tube degradation or biofilm build-up. In resource-constrained wards, re-use of single-use components persists, elevating infection risk and dampening uptake of premium systems. Manufacturers must demonstrate measurable reductions in adverse events to overcome clinician hesitancy.

Reimbursement Caps for Disposable Sets in ASEAN

Government price ceilings on consumables in Indonesia, Vietnam, and Malaysia squeeze margins on administration sets and gravity bags, limiting hospitals’ ability to adopt newest-generation low-volume residual kits. Indonesia’s TKDN rules further tilt procurement toward domestically assembled sets, complicating the supply chain for multinationals and elongating tender cycles. Providers sometimes resort to re-sterilizing tubing, increasing infection liability while depressing replacement volumes. Harmonization under an eventual ASEAN Medical Device Directive could ease cross-border sales, but near-term revenue growth remains gated by fragmented reimbursement mechanisms that disfavor advanced single-use accessories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Precision Pumps Retain Lead While Tubes Accelerate

Feeding pumps generated 40.25% of the Asia Pacific enteral feeding devices market share in 2025, underscoring the central role of precision delivery technology in acute and chronic care. Volumetric models dominate because their peristaltic rollers maintain consistent flow irrespective of viscosity, a critical need in oncology and ICU settings. The Asia Pacific enteral feeding devices market size for feeding pumps is forecast to grow at a 5.18% CAGR that reflects pump-replacement cycles more than first-time installations. Wireless telemetry, dose-error-reduction software, and automated flush protocols differentiate premium units, while entry-level devices emphasize ruggedness for emerging-market hospitals.

Feeding tubes, in contrast, are expanding at 7.62% CAGR as basic access becomes universal across secondary hospitals. Innovations such as Cardinal Health’s IRIS camera-guided tube replace blind placement, cutting malposition rates by 87% and reducing radiographic confirmation cost. ENFit connectors gained regulatory mandates across Japan and Australia, compelling large-scale legacy stock conversions. Administration sets and syringes post mid-single-digit growth, primarily volume-driven, as each pump requires multiple disposables daily. Environmental scrutiny is rising, so suppliers explore bio-based PVC alternatives that maintain flexibility without leaching plasticizers, balancing cost and compliance with single-use plastic bans in Australia and some Japanese prefectures.

By Age Group: Adult Dominance Confronts Rapid Pediatric Uptake

Adults accounted for 72.94% of the Asia Pacific enteral feeding devices market size in 2025, a ratio reflecting high prevalence of stroke, cancer, and neurologic dysphagia in older cohorts. Adult products emphasize easy programmability for nursing staff and compatibility with thickened formulas used for dysphagia management. The Asia Pacific enteral feeding devices market share held by adults is expected to remain above 70% through 2031, albeit with incremental volume gains mainly in home-care settings.

Pediatric and neonatal segments, though smaller, are growing 7.86% annually. Very-low-birth-weight infants require micro-bore tubes and fortified breast-milk formulations; pump suppliers add ultralow-flow modes capable of 0.5 mL/h resolution to meet these needs. Portable warmers keep milk at physiologic temperature en route from milk bank to incubator, decreasing lipid adherence to syringe walls. Pediatric home-care programs in Australia trial connected pumps with gamified caregiver apps that flag occlusions and allow asynchronous dietitian consults, further accelerating uptake beyond hospital walls.

By Distribution Channel: Offline Rules but E-commerce Gains Momentum

Traditional hospital and distributor channels governed 85.72% of the Asia Pacific enteral feeding devices market share in 2025 as procurement teams valued bundled service contracts and 24/7 technical support. Large-volume tenders still favor multinationals able to finance consignment inventories and deliver on‐site training. However, online sales are rising 8.05% per year on a low base. Specialty e-pharmacies and device portals offer subscription replenishment for tubes and bags, syncing delivery intervals with pump usage logs.

Regulatory frameworks present a mixed picture: India allows licensed online pharmacies to fulfill class B device prescriptions nationally, while Indonesia requires local distributor registration, slowing cross-border platforms. Hospitals increasingly use e-tender portals to solicit quotes, compressing price-discovery timelines and improving transparency. Suppliers thus integrate e-commerce within customer-relationship portals that host training videos and preventive-maintenance schedules, aligning digital procurement with after-sales service expectations.

By Application: Oncology Care Leads as Critical Care Accelerates

Cancer-related malnutrition drives 31.05% of the Asia Pacific enteral feeding devices market size in 2025, as chemotherapy and radiotherapy compromise oral intake and increase metabolic requirements. Oncology protocols often switch from nasogastric to percutaneous endoscopic gastrostomy (PEG) within two weeks to reduce aspiration risk, lifting demand for low-profile buttons and ambulatory pumps. Formulation suppliers co-market immune-enhancing blends rich in arginine and omega-3 fatty acids to improve wound healing, bundling tube kits for protocol adherence.

Critical care & trauma is the fastest-growing application at 7.38% CAGR. Early enteral nutrition within 48 hours in ICU settings halves ventilator days and reduces sepsis incidence, pushing intensivists to adopt auto-priming pumps that begin feeding immediately after line placement. Combined trauma-oncology cases, such as maxillofacial cancer resections, necessitate feeding devices that transition from inpatient to outpatient use without changing connectors or bag formats, creating integrative product families across acuity levels.

By End-User: Hospital Core Endures, Home Care Outpaces

Hospitals absorbed 54.68% of the Asia Pacific enteral feeding devices market share in 2025, buoyed by operating-room tube placements and high‐throughput ICUs. They continue to purchase fleet-size pump systems with central docking chargers and enterprise data-capture licenses. Nevertheless, home care grows 7.21% annually, fueled by reimbursement expansion in China and Japan and more lenient insurance approvals for pump consumables. The Asia Pacific enteral feeding devices market size for home care is set to surpass USD 0.39 billion by 2031, reflecting a structural shift toward community-based chronic-disease management .

Ambulatory surgical centers incrementally add share as day-surgery volumes climb, but their purchasing remains tied to hospital group purchasing organizations. Long-term-care facilities in Australia adopt gravity sets for low-acuity residents, a cost-effective compromise where full pumps are unnecessary. Suppliers target this segment with bag-in-box formula formats that reduce plastic weight by 34% and minimize waste.

Geography Analysis

China generated 40.88% of 2025 revenue in the Asia Pacific enteral feeding devices market, a position anchored by aggressive hospital expansion and population ageing . NMPA reforms that streamline registration—coupled with provincial procurement initiatives—accelerate uptake of smart pumps featuring Mandarin language interfaces. Volume-based procurement, however, pressures pricing, prompting suppliers to localize assembly to meet cost thresholds. The government’s digital-health blueprint favors connected devices, enabling real-time nutritional data integration into hospital information systems.

India, the fastest-growing geography at 7.84% CAGR, benefits from a national production-linked incentive scheme that subsidizes domestic device manufacturing. With 70% of its devices still imported, joint ventures—such as Nestlé Health Science and Dr. Reddy’s—illustrate a pivot toward in-country value creation. State insurance programs push for cost-effective enteral solutions, so suppliers introduce modular pump platforms that accept both low-cost gravity-bag sets and premium auto-flush sets, optimizing for variable purchasing power across urban and rural hospitals.

Mature markets—Japan, Australia, and South Korea—demand high-spec connectivity and comply early with single-use-plastic restrictions, prompting R&D into recyclable elastomer tubing. Japan’s dual food-drug classification for formulas encourages collaboration between pharmaceutical distributors and foodservice logistics providers. Australia’s post-market surveillance audits raise the bar on adverse-event reporting, favoring manufacturers with robust quality systems.

The rest of Asia Pacific, encompassing Indonesia, Malaysia, Thailand, and the Philippines, collectively represents a fast-expanding opportunity. Indonesia spends IDR 218.5 trillion on healthcare annually and has achieved 98% universal coverage, although TKDN content rules dictate that at least 40% of device value be produced domestically. Thailand’s EEC medical-hub strategy allocates tax breaks for device makers that establish ASEAN distribution centers, strategically positioning the country as a logistics node for cross-border shipments.

Competitive Landscape

The Asia Pacific enteral feeding devices industry is characterized by moderate concentration. Abbott, Medtronic, Fresenius Kabi, Cardinal Health, B. Braun, Avanos Medical, and Nutricia collectively command the lion’s share of revenue, leveraging diversified portfolios and broad regional distribution. Abbott’s Nutrition segment grew 6.8% organically in Q1 2025 on the strength of Ensure and Glucerna, supported by USD 0.5 billion in incremental R&D and manufacturing investment targeted at emerging markets. Cardinal Health’s IRIS camera-equipped tube and Kangaroo Connect telemetry platform differentiate in placement safety and remote monitoring.

Local challengers in India and China manufacture cost-competitive tubes and gravity sets, often pricing 35-45% below multinationals. These players capitalize on public-sector tenders, emphasizing the lowest bid, yet may struggle to match premium feature sets such as ENFit transition kits or Bluetooth connectivity. Sustainability has become a new axis of competition; Nutricia reformulated its Nutrison range to reduce carbon footprint by 17% while increasing caloric density, meeting growing hospital sustainability KPIs. OEMs are also exploring silicone-free feed lines to comply with looming Japanese and Australian recycling mandates.

Strategic partnerships proliferate: Avanos and Samsung SDS pilot IoT middleware that synthesizes pump data with electronic medical records, whereas Fresenius Kabi collaborates with Alibaba Cloud for AI-enabled supply chain management in China. M&A activity remains measured but is expected to accelerate as digital-capability gaps widen between incumbents and niche innovators.

Asia-Pacific Enteral Feeding Devices Industry Leaders

Abbott Laboratories

Becton, Dickinson and Company

Boston Scientific Corp.

ConMed Corporation

Vygon S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Cardinal Health has unveiled plans to roll out its Kangaroo OMNI™ Enteral Feeding Pump, an innovative portable system designed to deliver thick, homogenized, and blended formulas. The pump is set to debut in Europe, Australia, and New Zealand in the first half of 2025, with an Asian launch slated for later that year.

- November 2024: Otsuka Pharmaceutical Factory introduced "Tumguide Fiber" with 0.5 mm and 0.75 mm outer diameters for use with Tumguide LED Light Source, a device that verifies the nasogastric tube tip's position. Designed for pediatric treatments, this optical fiber connects to the light source and is inserted into the stomach. The illuminated tip enables external visual confirmation of the tube's position using red light.

- April 2024: Hangzhou Primecare Medical Co., Ltd received FDA 510K approval for its CONOD enteral feeding sets.

- March 2024: Vygon launched Nutrisafe2, an enteral feeding system for neonates in India, to reduce tubing misconnections in NICUs. Nutrisafe2 is designed to prevent misconnections, which can have severe or fatal outcomes.

Asia-Pacific Enteral Feeding Devices Market Report Scope

Enteral feeding refers to the delivery of a nutritionally complete feed, containing protein, carbohydrate, fat, water, minerals, and vitamins, directly into the stomach, duodenum, or jejunum through devices, such as tubes and pumps. Enteral feeding tubes and pumps and other devices facilitate the process. It is used for people with functional GI tract, who are not able to ingest foods orally to meet their nutrient demand.

By Product Type

| Feeding Pumps | Volumetric Pumps |

| Ambulatory Pumps | |

| Syringe Pumps | |

| Feeding Tubes | Nasogastric Tubes |

| Gastrostomy Tubes | |

| Others | |

| Enteral Feeding Bags | |

| Administration Sets & Accessories | |

| Enteral Syringes |

By Age Group

| Adults |

| Pediatric & Neonatal |

By Distribution Channel

| Offline |

| Online |

By Application

| Oncology |

| Gastroenterology |

| Critical Care & Trauma |

| Other Applications |

By End-User

| Hospitals |

| Ambulatory Surgical Centers |

| Home Care Settings |

| Other End-Users |

By Geography

| China |

| Japan |

| India |

| Australia |

| South Korea |

| Rest of Asia-Pacific |

| By Product Type | Feeding Pumps | Volumetric Pumps |

| Ambulatory Pumps | ||

| Syringe Pumps | ||

| Feeding Tubes | Nasogastric Tubes | |

| Gastrostomy Tubes | ||

| Others | ||

| Enteral Feeding Bags | ||

| Administration Sets & Accessories | ||

| Enteral Syringes | ||

| By Age Group | Adults | |

| Pediatric & Neonatal | ||

| By Distribution Channel | Offline | |

| Online | ||

| By Application | Oncology | |

| Gastroenterology | ||

| Critical Care & Trauma | ||

| Other Applications | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Home Care Settings | ||

| Other End-Users | ||

| By Geography | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How is population ageing shaping demand for enteral feeding devices in Asia Pacific?

Longer life expectancy and higher stroke incidence are increasing the need for post-acute nutritional support, prompting hospitals and home-care providers to standardize tube-feeding protocols for older adults.

Why are connected feeding pumps gaining traction among healthcare providers?

Clinicians value devices that transmit dosage data to electronic records, which simplifies remote monitoring, reduces alarm fatigue, and supports reimbursement models tied to outcome tracking.

What role do neonatal intensive-care upgrades play in market adoption?

Expanded NICU capacity in China, India, and Southeast Asia is driving demand for micro-bore tubes and precision pumps that can safely deliver very low flow rates to premature infants.

How are sustainability requirements influencing product development?

Manufacturers are reformulating formulas to lower carbon footprints and experimenting with recyclable tubing materials to comply with single-use plastic regulations in Australia and Japan.

In what ways are local manufacturing incentives affecting competitive dynamics?

Government programs in India and Indonesia encourage domestic production, enabling local firms to offer lower-priced tubes and sets that intensify price competition for multinational brands

What procurement trends are emerging as hospitals digitize supply chains?

Health systems increasingly use e-tender portals and automated restock systems, rewarding suppliers that integrate training resources, maintenance scheduling, and ordering into a single digital platform.

Page last updated on: