Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

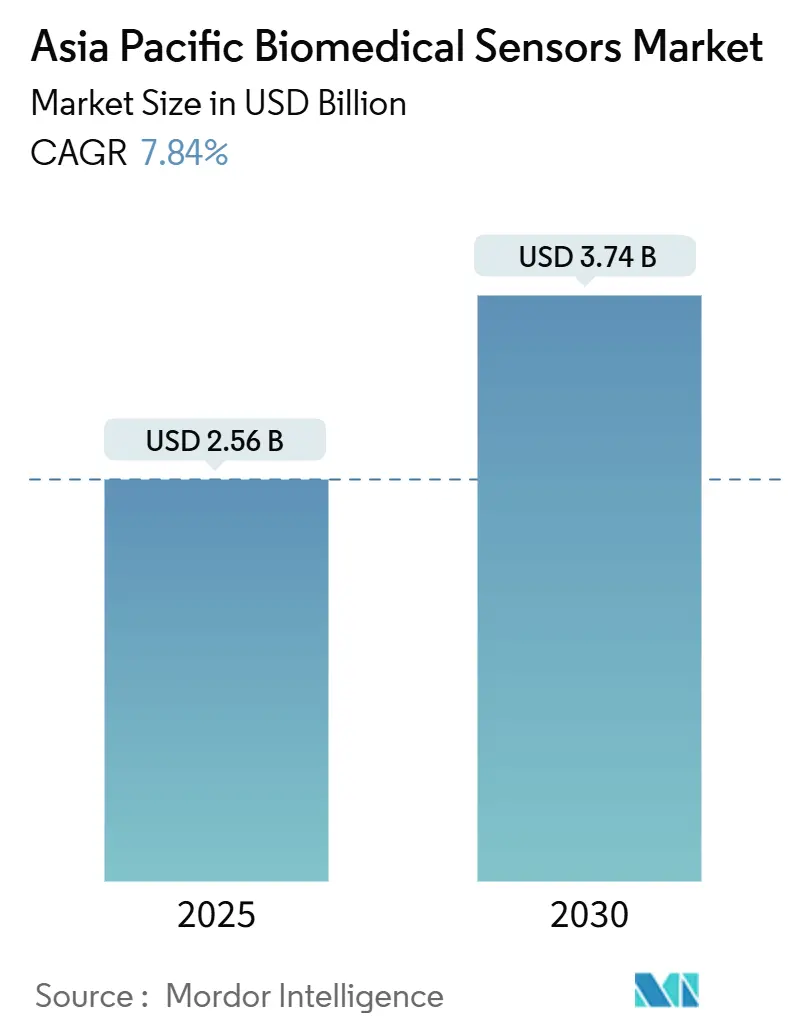

| Market Size (2025) | USD 2.56 Billion |

| Market Size (2030) | USD 3.74 Billion |

| Growth Rate (2025 - 2030) | 7.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Biomedical Sensors Market Analysis by Mordor Intelligence

The Asia Pacific biomedical sensors market size stands at USD 2.56 billion in 2025 and will reach USD 3.74 billion by 2030, expanding at a 7.84% CAGR. Distributed-care reimbursement in Japan, China’s MEMS localization subsidies, and value-based health-insurance pilots in South Korea accelerate adoption in hospitals, homes, and decentralized trials. Wireless devices already dominate, yet design attention is shifting to edge‐processing modules that avoid cloud latency. Biochemical sensors are the fastest climbers, riding the continuous glucose-monitor growth in China’s tier-2 cities where adult diabetes prevalence exceeds 12%. Implantables are growing quickly, as leadless pacemakers and insertable monitors reduce infection risks and simplify follow-up procedures. At the same time, new privacy penalties such as Singapore’s SGD 1 million fine against IHH Healthcare push security compliance to the foreground.

Key Report Takeaways

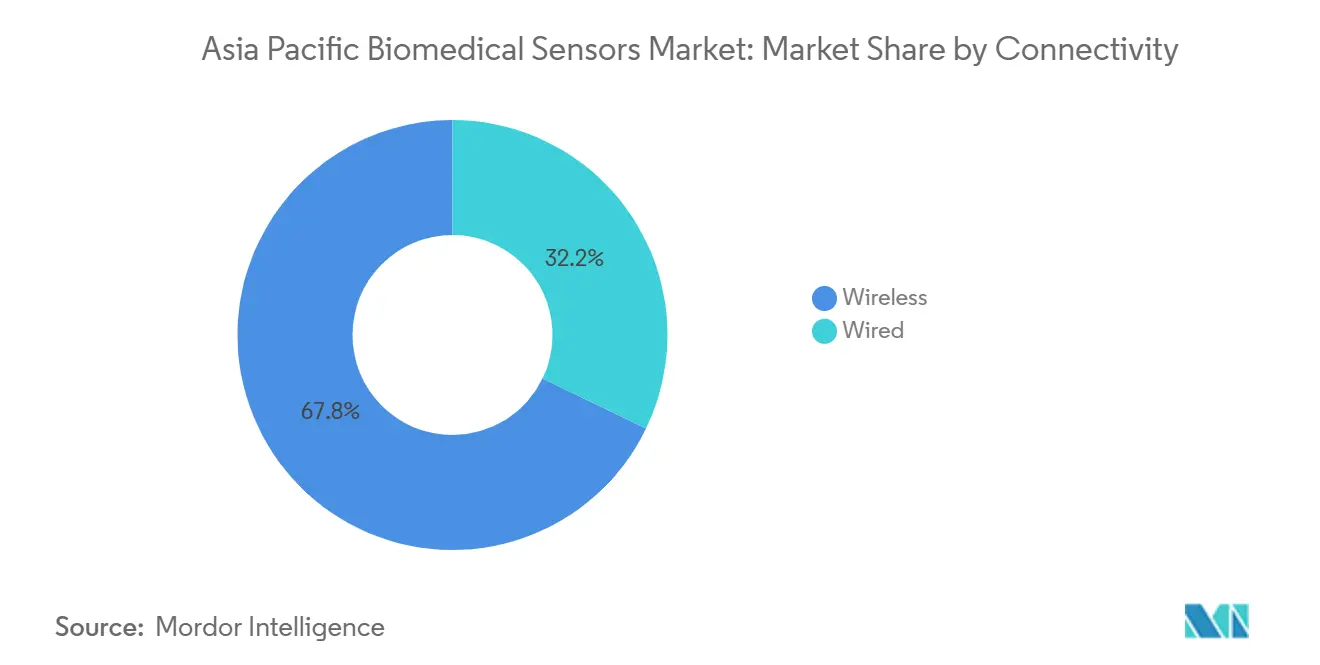

- By connectivity, wireless held 67.84% of the Asia Pacific biomedical sensors market share in 2024, while the same wireless advance at an 9.12% CAGR through 2030.

- By sensor type, temperature sensors commanded 25.74% share of the Asia Pacific biomedical sensors market size in 2024, while biochemical advance at an 8.11% CAGR through 2030.

- By form factor, wearable platforms led with 52.94% share in 2024 of the Asia Pacific biomedical sensors market, while implantables advance at an 8.99% CAGR through 2030.

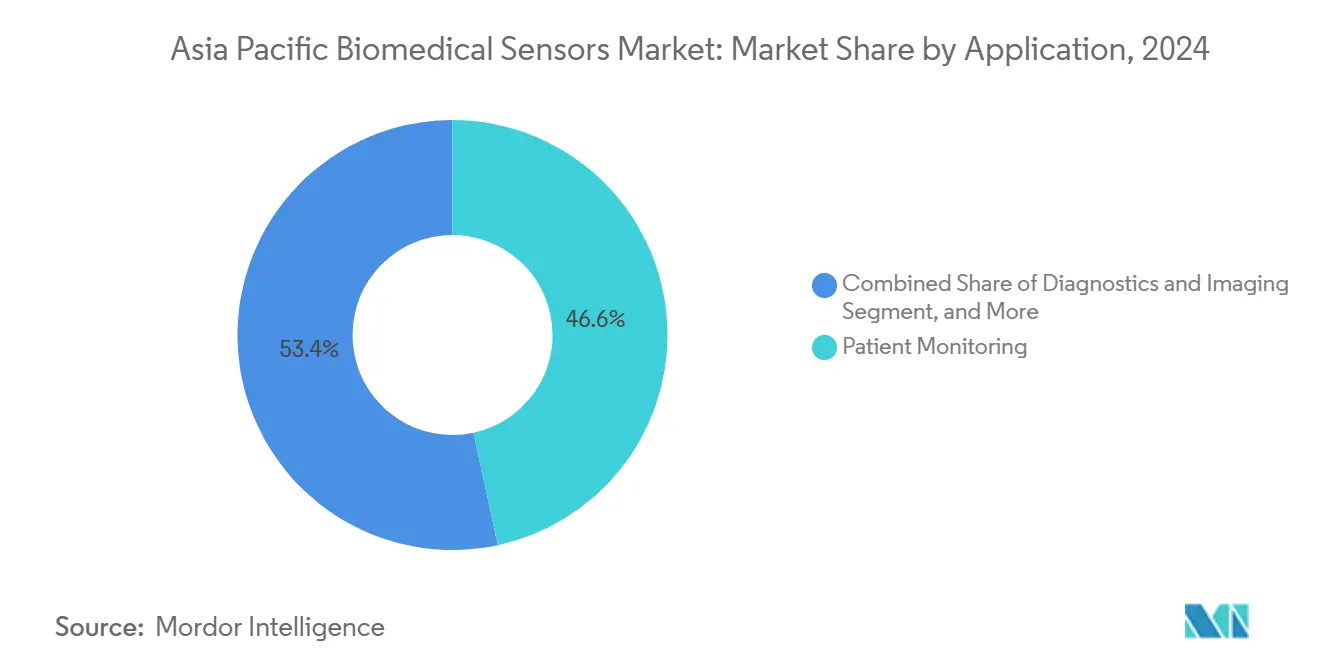

- By application, patient monitoring captured 46.62% of 2024 revenue of the Asia Pacific biomedical sensors market; therapeutics sensors grow fastest at an 8.67% CAGR through 2030.

- By end user, hospitals and clinics controlled 44.72% revenue in 2024 of the Asia Pacific biomedical sensors market; home-health and tele-care expand at an 8.55% CAGR through 2030.

Asia Pacific Biomedical Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wearable fitness and wellness adoption surge | +1.8% | China, India, South Korea; spillover to ASEAN urban centers | Short term (≤ 2 years) |

| Chronic-disease remote monitoring programs | +1.5% | Japan, Australia, Singapore; expanding to Malaysia, Thailand | Medium term (2-4 years) |

| IoT-enabled point-of-care diagnostics | +1.2% | Global Asia-Pacific, with early traction in Singapore, South Korea, urban China | Medium term (2-4 years) |

| Rapid ageing population in Asia-Pacific | +1.0% | Japan, South Korea, China; emerging in Thailand, Vietnam | Long term (≥ 4 years) |

| Japan's expanded RPM reimbursement codes | +0.9% | Japan national, with demonstration effects in South Korea, Taiwan | Short term (≤ 2 years) |

| China's MEMS sensor localisation subsidies | +0.7% | China national, with component exports to ASEAN assembly hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Wearable Fitness and Wellness Adoption Surge

China shipped 30% of global wearables in 2024, with sub-USD 50 units from Xiaomi and Huawei popularizing photoplethysmography for heart-rate variability tracking. Premium competitors differentiate by securing FDA-cleared arrhythmia alerts, as Apple’s ECG app did across Japan and Singapore in 2024.[1]Apple Inc., “ECG App Approved in Singapore,” apple.com India’s 2024 import-duty hike reduced smartwatch imports but spurred local assembly, including MediBuddy’s Chennai pulse oximeter line, which targets public tenders. South Korea has cleared 14 digital therapeutics that incorporate wearable sensor data, offering a regulatory template that is under review in Thailand and Malaysia. Broader adoption depends on interoperability, yet only 30% of Asia-Pacific hospitals utilize HL7 FHIR, which fragments data flows and limits economies of scale.

Chronic-Disease Remote Monitoring Programs

Japan’s April 2024 switch to “P” codes created predictable revenue for sensor-enabled teleconsultations and cut emergency visits for heart-failure patients by 35% MHLW. Australia followed by subsidizing the Dexcom G7, driving a 60% increase in uptake within one quarter. Singapore’s HealthierSG initiative, which enrolls 1.2 million residents, mandates uploads from home blood-pressure cuffs, resulting in an 18% increase in Omron’s regional sales. India’s 500 million digital health IDs still struggle with device-platform interoperability, which slows sensor penetration. In Indonesia, specialist shortages strengthen the economic logic for remote triage, creating urgency around sensor rollouts.

IoT-Enabled Point-of-Care Diagnostics

Singapore’s tele-ventilator pilot cut ICU transfers by 28% among COPD patients. China fast-tracked a 15-minute sepsis biomarker test for rural clinics, achieving 92% sensitivity UTS. Thailand’s 2024 pilot of point-of-care HbA1c testing shortened diagnostic delays from six weeks to same-day enrollment for 40,000 patients. Vietnam mandates multi-parameter analyzers in every district hospital by 2025, benefitting Roche and Abbott platforms. Supply-chain gaps remain as tropical humidity raises enzyme-strip spoilage, adding 15% to packaging cost.

Rapid Ageing Population in Asia-Pacific

Japan’s over-65 cohort exceeded 29% in 2024, triggering demand for ambient gait sensors embedded in flooring and smart toilets. South Korea earmarked KRW 300 billion for smart-home health hubs that link wearable ECG patches and medication reminders. China’s elder-care fees top CNY 500 monthly, unaffordable for many rural retirees, slowing uptake despite policy support. Australia now requires real-time location tracking for dementia patients in residential facilities, accelerating Bluetooth Low Energy beacon demand. Thailand collaborates with Sensirion to source low-cost temperature modules for community elder-care housing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of implantable sensor systems | -0.8% | India, Indonesia, Philippines, Vietnam; moderate impact in China tier-3 cities | Medium term (2-4 years) |

| Data-privacy and cybersecurity gaps | -0.6% | Singapore, Australia, Japan; emerging concerns in Malaysia, Thailand | Short term (≤ 2 years) |

| Fragmented biocompatibility rules in ASEAN | -0.5% | ASEAN-6 (Singapore, Malaysia, Indonesia, Thailand, Philippines, Vietnam) | Long term (≥ 4 years) |

| Miniaturised-battery supply limitations | -0.4% | Global Asia-Pacific, with acute shortages in implantable and ingestible segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Implantable Sensor Systems

Implantable cardiac monitors cost more than USD 10,000, far above reimbursement ceilings in India, Indonesia, and the Philippines. Patients often downgrade to conventional pacemakers to avoid paying the difference. Indonesian public hospitals still use decade-old devices because BPJS Kesehatan does not cover Bluetooth-enabled versions. Vietnam negotiated a 25% discount with Abbott in 2024 but implanted fewer than 500 units because only 12 electrophysiologists serve 100 million citizens. Singapore’s informal refurbishment market offers discounted devices but raises safety concerns for regulators.

Data-Privacy and Cybersecurity Gaps

Singapore fined IHH Healthcare SGD 1 million for a 2024 breach involving glucose-monitor data. The Cybersecurity Agency estimates 60% of IoMT devices run outdated firmware. Australia logged 18 healthcare data-breach notices in Q3 2024, most tied to unsecured Wi-Fi at aged-care homes. Japan’s 2024 audit found 40% of RPM platforms lack end-to-end encryption. Regional data-residency rules force multinational platforms to build separate servers in each ASEAN-6 country, adding USD 2 million-5 million to CAPEX.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Connectivity: Wireless Dominance Masks Edge-Processing Shift

Wireless architecture captured 67.84% of the Asia Pacific biomedical sensors market share in 2024 and is projected to grow at a 9.12% CAGR through 2030. The Asia Pacific biomedical sensors market now pivots toward on-device analytics, with Analog Devices’ MAX32664 hub running arrhythmia algorithms locally and sending only flagged events, cutting cellular data use 80%. Bluetooth Low Energy 5.3 extends the range to 200 m and reduces power draw by 30%, enabling 14-day continuous glucose monitor operation on a coin cell. Wired equipment remains relevant in ICUs, where EMI resilience is crucial. GE’s CARESCAPE line held 22% of the wired ICU monitor market share in 2024. Replacement cycles hinder wired-to-wireless migration because a central station can cost up to USD 1 million and typically lasts 10-15 years. EMC testing under IEC 60601-1-2 remains a hurdle for ASEAN manufacturers lacking accredited laboratories, which can extend certifications by six months.

Second-generation ultra-wideband chips from NXP add sub-meter geolocation, reducing caregiver search time by 40% and justifying a USD 300 price premium over Bluetooth-only modules. Edge-processing advances will keep the Asia Pacific biomedical sensors industry focused on wireless security and power efficiency tradeoffs, ensuring that wireless stays dominant but technologically dynamic.

By Sensor Type: Biochemical Gains Outpace Temperature’s Installed Base

Temperature devices still lead with a 25.74% market share after extensive pandemic deployments, but biochemical sensors are projected to clock an 8.11% CAGR through 2030. Sensirion shipped 10 million STS40 chips into Omron and Panasonic devices in 2024.[2]Sensirion, “STS40 Temperature Sensor,” sensirion.com Continuous glucose monitors are reaching gestational and pre-diabetes cohorts, 35% of Libre users in China are non-insulin-dependent. Infineon’s DPS310 barometric pressure sensor enabled Omron’s cuffless Evolv monitor, extending its use to patients who are uncomfortable with traditional cuffs.

ECG analog front-ends from STMicroelectronics widen single-lead patch availability, which Philips scaled to 2 million patients region-wide in 2024. Image sensors rise with the launch of Olympus’ EVIS X1 endoscopy, utilizing Sony 4K CMOS chips, which have been approved in China. Accelerometer-based fall detectors rely on Murata’s SCA3300 inclinometer inside ResMed’s AirSense 11 CPAP, cutting apnea events 18%. Each advance cements biochemical and motion modules as the high-velocity segments shaping the Asia Pacific biomedical sensors market.

By Form Factor: Implantables Surge as Surgical Techniques Mature

Implantables are expected to post an 8.99% CAGR and narrow the lead of wearables, which currently command 52.94% of the revenue. Medtronic’s Micra AV leadless pacemaker, approved in Japan in 2024, eliminates pocket infections that affect 2% of conventional units and cost USD 20,000 to revise. Strip-based disposables face fierce price erosion from sub-USD 0.10 Chinese glucose strips.

Ingestibles remain a niche but advanced option, and Otsuka’s Abilify MyCite antipsychotic embeds a Proteus sensor that logs ingestion events and aids adherence. Panasonic’s 30-day solid-state battery prototype hints at longer-term ingestible applications, although mass-market prices are not yet viable. ISO 10993 testing consumes 18 months and USD 200,000 per implantable variant, favoring multinationals that reuse legacy dossiers.

By Application: Therapeutics Overtakes Diagnostics in Growth Velocity

Closed-loop drug-delivery platforms are leading the way with an 8.67% CAGR, while patient monitoring maintains the largest share at 46.62%. MiniMed 780G adjusts insulin every five minutes based on Guardian 4 readings and cut glucose variability 12% in Australian rollouts MEDT780G. GE’s USD 5,000 Vscan Air ultrasound opened portable imaging to rural clinics, with 40,000 units sold in 2024.

Wearable smart socks from Sensoria detect gait asymmetry in marathoners and elite athletes across Singapore, illustrating the crossover of sensors into sports medicine. Propeller Health’s reimbursed inhaler sensor reduced asthma ED visits 30% in Japanese trials. Hyperspectral dermatology cameras detect melanoma with 89% sensitivity but remain pricey, limiting spread to tertiary hospitals

By End User: Home-Health Gains as Reimbursement Models Shift

Hospitals and clinics still generate 44.72% of revenue, yet home health grows rapidly on an 8.55% CAGR tailwind from outcome-based payment schemes. South Korea reimburses KRW 20,000 per sensor review, resulting in a 22% reduction in hypertension hospitalizations within six months. Pharmaceutical firms use sensors to streamline decentralized trials. Medable cut dropout rates to 18% by integrating CGM feeds from Dexcom in 15 Asia-Pacific diabetes studies.

Malaysia trains 10,000 community nurses for Bluetooth troubleshooting, spreading remote monitoring beyond urban areas. Novartis pilots ingestible sensors to boost adherence in Indonesia’s hypertension program, aiming to reduce the discontinuation rate to 60%. Academic institutes such as A*STAR published 12 biosensor papers, anchoring regional performance benchmarks.

Geography Analysis

China anchors the Asia Pacific biomedical sensors market, drawing on CNY 500 billion in digital health funding and 300 million remote monitoring users by 2024. Mindray boosted its MEMS capacity by 40% in Nanjing and feeds both domestic and ASEAN demand. Abbott’s Libre holds 35% of China’s CGM segment but faces competition from Sinocare’s CNY 300 sensor, which is now listed on 15 provincial insurance plans. Priority review at the NMPA cut innovative-sensor approvals to nine months, speeding launches by Dexcom and Medtronic.

Japan pivoted to clinician-prescribed sensors once “P” codes sliced CGM out-of-pocket costs 90% MHLW. Nihon Kohden retained a 25% ECG market share by embedding atrial fibrillation AI and increasing revenue by 15%. Fall-detection wearables gained momentum after Omron incorporated accelerometers into its blood-pressure monitor, capturing a 40% share of the elder-care market.

India’s wearable contraction from import duties triggered joint ventures like MediBuddy-ELECOM for local oximeter lines aimed at state tenders. South Korea’s K-Digital Health fund supports sensor–EHR integration and helped Samsung capture 30% of the domestic wearable ECG market. Australia’s PBS rebate for Dexcom slashed consumer costs to AUD 50 per month, lifting adoption by 60% in one quarter. New Zealand’s FHIR mandate delayed eight platforms but accelerated Philips’ compliant system deployment.

ASEAN-6 remains fragmented. Singapore fast-tracked 12 devices in 2024, but Malaysian regulators demand separate trials, adding USD 0.5 million per study. Indonesia reimburses only basic glucose meters for 220 million citizens, while private hospitals adopt sensor-rich systems. Thailand’s point-of-care HbA1c pilot now enrolls 40,000 diabetes patients. Philippines widened teleconsultation payments yet rural 4G gaps limit reach. Vietnam insists on analyzer procurement in every district hospital, aiding Roche and Abbott

Competitive Landscape

The Asia Pacific biomedical sensors market is characterized by a moderately concentrated field, with the top five companies holding approximately a 40% share, none of which exceeds 12%. Abbott, Medtronic, and Dexcom remain CGM leaders, whereas Roche and GE Healthcare leverage multi-parameter strengths. Analog Devices, STMicroelectronics, and Infineon dominate the analog front-end market, with none exceeding a 15% chip share, yet collectively supplying dozens of OEMs. Edge AI differentiation intensifies, Analog Devices’ MAX32664 reduced cloud-compute costs 80% and landed in 15 ECG wearables by end-2024.

Patent activity highlights priorities: Medtronic filed 42 patents related to leadless pacemaker miniaturization, and Dexcom filed 28 predictive glucose patents that rely on transformer models.[3]USPTO, “Patent Database,” uspto.gov Disruptive threats come from Chinese entrants like Sinocare, which prices CGM sensors 60% below those of multinationals, and from niche innovators targeting ingestible and intracranial pressure sensors, areas where current supply lags demand across ASEAN hospitals. Regulatory harmonization via the Asia Harmonization Working Party tightens performance benchmarks and squeezes under-capitalized startups

Asia Pacific Biomedical Sensors Industry Leaders

Abbott Laboratories

Analog Devices Inc.

Honeywell International Inc.

Infineon Technologies AG

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Japan’s Pharmaceuticals and Medical Devices Agency cleared Panasonic’s 30-day solid-state micro-battery for implantable and ingestible sensors, cutting replacement cycles by 60% in clinical devices slated for 2026 launch.

- June 2025: Shenzhen Mindray Bio-Medical Electronics commenced mass production of ingestible gastrointestinal pH sensors at its new Guangzhou MEMS line, targeting 3 million units annually for ASEAN export markets.

- March 2025: South Korea’s National Health Insurance Service started full reimbursement for sensor-enabled COPD telemonitoring, paying KRW 25,000 per monthly review and enrolling 80,000 patients in the first quarter.

- January 2025: Abbott introduced FreeStyle Libre 3 Ultra across India’s Ayushman Bharat network, offering 1-minute predictive hypoglycemia alerts and achieving national reimbursement within one month.

Asia Pacific Biomedical Sensors Market Report Scope

The Asia Pacific Biomedical Sensors Market Report is Segmented by Connectivity (Wired, Wireless), Sensor Type (Temperature, Pressure, Image, Biochemical, Inertial, Motion, Other Sensor Types), Form Factor (Wearable, Implantable, Ingestible, Strip/Disposable), Application (Patient Monitoring, Diagnostics and Imaging, Therapeutics and Drug-delivery, Sports and Fitness, Other Applications), End User (Hospitals and Clinics, Home-health and Tele-care, Pharmaceutical and Biotech Firms, Academic and Research Institutes), and Geography (China, Japan, India, South Korea, Australia and New Zealand, Rest of Asia Pacific). Market Forecasts are Provided in Terms of Value (USD).

By Connectivity

| Wired |

| Wireless |

By Sensor Type

| Temperature |

| Pressure |

| Image |

| Biochemical |

| Inertial |

| Motion |

| Other Sensor Types |

By Form Factor

| Wearable |

| Implantable |

| Ingestible |

| Strip/Disposable |

By Application

| Patient Monitoring |

| Diagnostics and Imaging |

| Therapeutics and Drug-delivery |

| Sports and Fitness |

| Other Applications |

By End User

| Hospitals and Clinics |

| Home-health and Tele-care |

| Pharmaceutical and Biotech Firms |

| Academic and Research Institutes |

Geographic Analysis

| China |

| Japan |

| India |

| South Korea |

| Australia and New Zealand |

| Rest of Asia-Pacific |

| By Connectivity | Wired |

| Wireless | |

| By Sensor Type | Temperature |

| Pressure | |

| Image | |

| Biochemical | |

| Inertial | |

| Motion | |

| Other Sensor Types | |

| By Form Factor | Wearable |

| Implantable | |

| Ingestible | |

| Strip/Disposable | |

| By Application | Patient Monitoring |

| Diagnostics and Imaging | |

| Therapeutics and Drug-delivery | |

| Sports and Fitness | |

| Other Applications | |

| By End User | Hospitals and Clinics |

| Home-health and Tele-care | |

| Pharmaceutical and Biotech Firms | |

| Academic and Research Institutes | |

| Geographic Analysis | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia Pacific biomedical sensors market in 2025?

The Asia Pacific biomedical sensors market size is USD 2.56 billion in 2025.

What CAGR will the Asia Pacific biomedical sensors market post through 2030?

The market is projected to expand at a 7.84% CAGR between 2025 and 2030.

Which connectivity segment leads sales?

Wireless connectivity holds 67.84% of 2024 revenue and continues to grow on edge-processing improvements.

Why are biochemical sensors growing fastest?

Demand for continuous glucose monitoring in Chinese tier-2 cities and gestational diabetes screening drives the 8.11% CAGR for biochemical sensors.

What shifts are happening in end-user segments?

Home-health and tele-care grow at an 8.55% CAGR as reimbursement models reward remote monitoring and outcome-based care.

Page last updated on: