Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

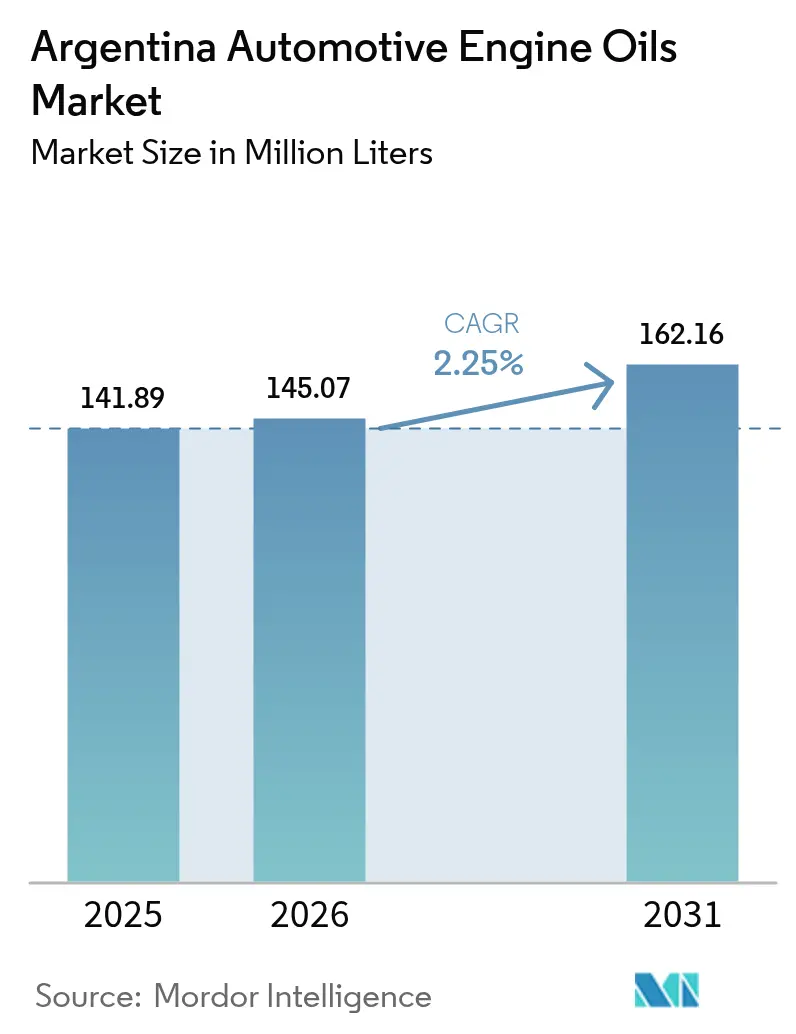

| Base Year Market Size (2025) | 141.89 Million Liters |

| Market Volume (2026) | 145.07 Million Liters |

| Market Volume (2031) | 162.16 Million Liters |

| Growth Rate (2026 - 2031) | 2.25% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Automotive Engine Oils Market Analysis by Mordor Intelligence

The Argentina Automotive Engine Oils Market size was valued at 141.89 Million Liters in 2025 and estimated to grow from 145.07 Million Liters in 2026 to reach 162.16 Million Liters by 2031, at a CAGR of 2.25% during the forecast period (2026-2031). This growth reflects the post-reform rebound in light-vehicle output, persistent aftermarket demand from an aging 15.55 million-unit vehicle parc, and incremental shifts toward low-SAPs synthetics that comply with tightening emissions rules[1]Instituto Nacional de Estadística y Censos, “Indicadores de Producción Industrial,” indec.gob.ar. Continued peso volatility, import-offset quotas, and the DJAI licensing system shape procurement strategies, boosting the competitive advantage of integrated domestic blenders that can ensure uninterrupted supply. At the same time, modest electric-vehicle penetration, currently at just 1,555 units, keeps lubricant demand firmly anchored in internal-combustion platforms. Fleet digitization, exemplified by connected-vehicle offerings from Scania and YPF’s Ruta system, is lengthening drain intervals yet raising viscosity and oxidation-stability requirements, creating opportunities for premium synthetic and semi-synthetic formulations.

Key Report Takeaways

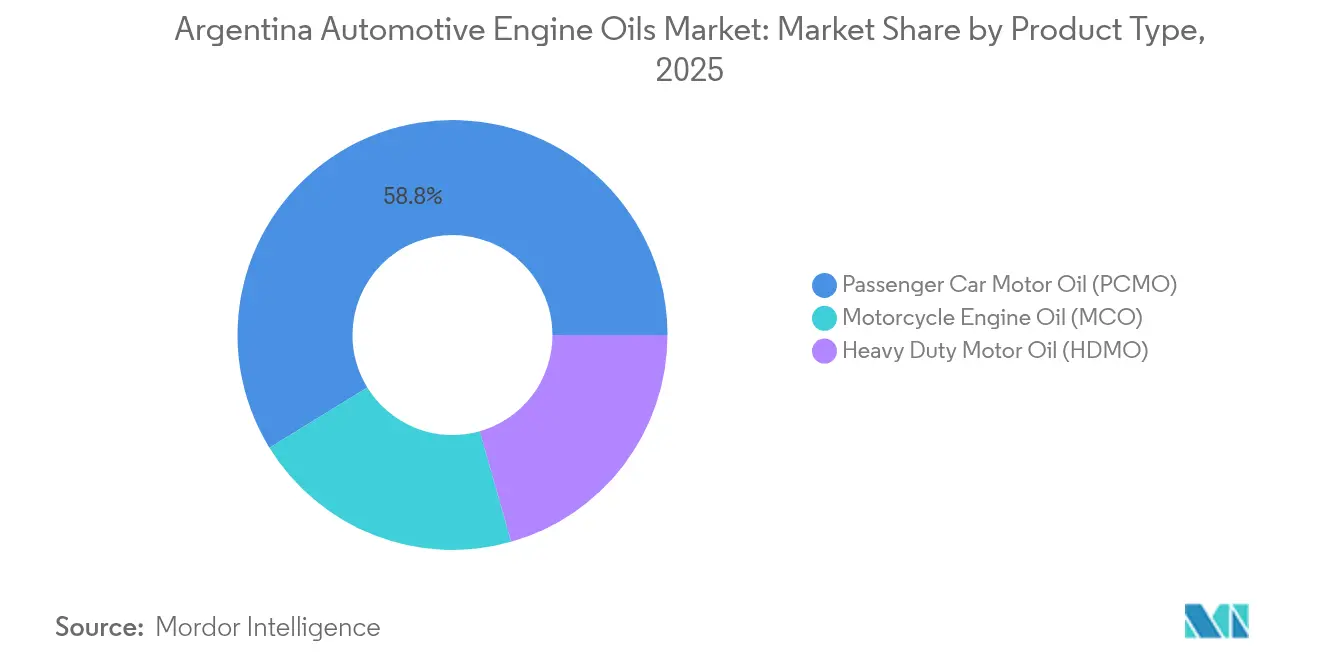

- By product type, Passenger Car Motor Oil held 58.78% of the Argentina Automotive Engine Oils market share in 2025, whereas Motorcycle Engine Oil is projected to grow the fastest at a 2.32% CAGR to 2031.

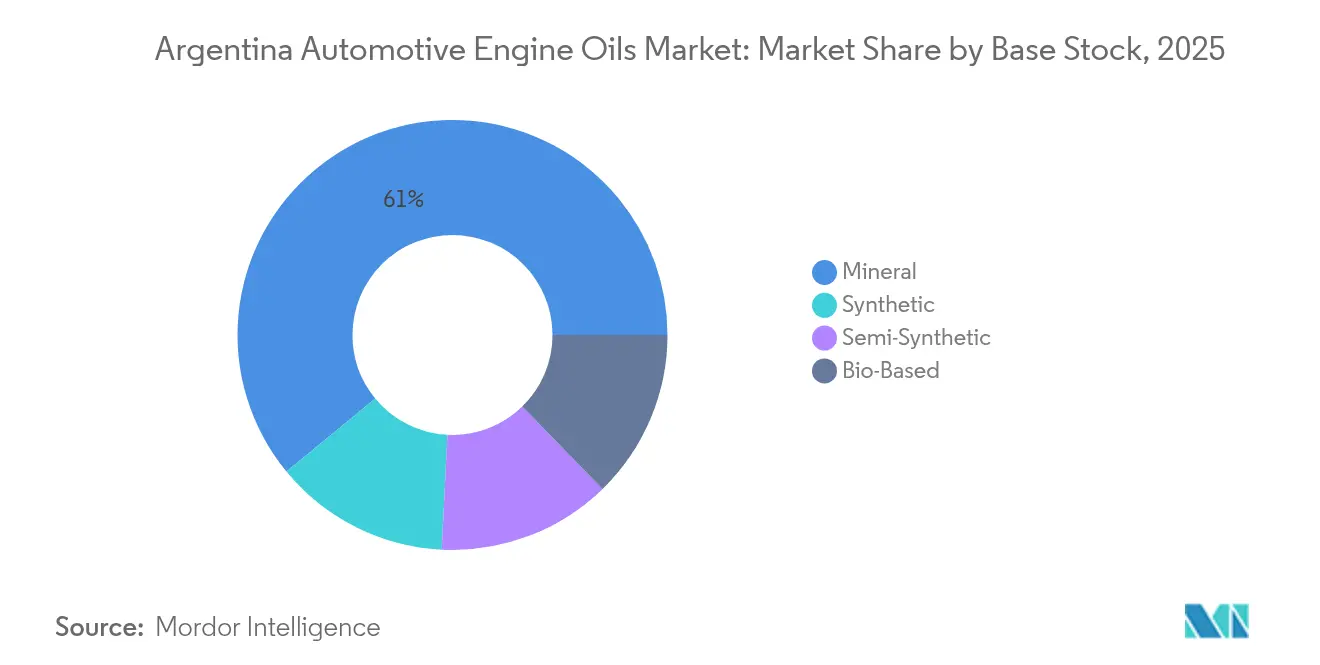

- By base stock, mineral oils commanded 60.95% of the Argentina Automotive Engine Oils market size in 2025, while synthetic oils are poised for the highest growth at a 2.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rebound of light-vehicle production post-2024 FX reform | +0.8% | National, with concentration in Buenos Aires, Córdoba automotive corridors | Short term (≤ 2 years) |

| Aging vehicle parc (>13 yrs) sustaining aftermarket demand | +0.6% | National, with higher impact in interior provinces | Long term (≥ 4 years) |

| Tightening fuel-sulphur & emissions rules favoring low-SAPs synthetics | +0.4% | National, with early adoption in Buenos Aires metropolitan area | Medium term (2-4 years) |

| OEM factory-fill contracts localizing to comply with import-offset quotas | +0.3% | National, concentrated in automotive manufacturing hubs | Medium term (2-4 years) |

| Fleet digitalization driving high-mileage long-drain oils | +0.2% | National, with early gains in Buenos Aires, Rosario, Córdoba commercial corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Rebound of Light-Vehicle Production Post-2024 FX Reform

Automotive output surged 23.2% y-o-y in January 2025 after Argentina unified its exchange rates, restoring manufacturer access to imported components and re-energizing OEM production targets. The resulting upswing in factory-fill demand injects new volumes into the Argentina Automotive Engine Oils market, especially for API-SP and ACEA A5/B5 formulations required by Toyota, Ford, and General Motors. Assemblers now forecast double-digit output gains for 2025; however, this incremental volume must coexist with the aftermarket’s 15:1 dominance, straining domestic blending capacity and favoring players such as YPF that own upstream base-oil assets. The episode highlights how macroeconomic policy shifts can abruptly realign lubricant demand patterns, challenging supply chains that are calibrated to steady aftermarket cycles.

Aging Vehicle Parc Sustaining Aftermarket Demand

With an average vehicle age of 14.3 years and 80% of units older than 10 years, Argentina’s fleet anchors stable lubricant off-take well beyond new-car sales cycles. Professional service centers perform 95% of oil changes, institutionalizing repeat demand through programs like YPF Boxes, which bundle products and services. Mandatory annual inspections for vehicles over three years old further institutionalize maintenance, ensuring the Argentina Automotive Engine Oils market remains resilient even in economic downturns. Cost-sensitive owners favor 15W-40 mineral grades, yet the gradual shift to semi-synthetics in urban regions signals a slow evolution of viscosity and performance preferences.

Tightening Fuel-Sulfur & Emissions Rules Favoring Low-SAPs Synthetics

Joint Resolution 01/2016 introduced Euro III heavy-duty limits and diesel fuel sulfur reductions to 30-50 ppm, compelling fleets to adopt low-SAP oils that protect DPFs and SCR systems[2]Secretaría de Energía, “Resolución Conjunta 01/2016,” argentina.gob.ar. Alignment with ACEA E8 and API CK-4 sequences is increasing oxidation stability and biodiesel compatibility requirements, particularly relevant under Argentina’s 5% biodiesel blend mandate. The regulation accelerates demand for Group II+ and Group III-based synthetics despite their 40-60% price premium, positioning premium suppliers for share gains in the Argentina Automotive Engine Oils market.

OEM Factory-Fill Contracts Localizing to Comply with Import-Offset Quotas

Import-offset rules oblige automakers to match every USD of imports with exports, incentivizing domestic sourcing of factory-fill lubricants. YPF has secured agreements with Suzuki, Volkswagen, Ford, and Chevrolet by leveraging its 244,000 m³/year Group I base-oil stream and multi-site blending capacity. Localization reduces DJAI-related delays, stabilizes production schedules, and embeds lubricant suppliers deeper into OEM value chains. The strategy, however, requires sustained investment in laboratory capabilities and additive technologies to meet global OEM specifications, thereby generating a technology-capability race among local blenders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Peso volatility inflating imported base-oil costs | -0.5% | National, with higher impact on import-dependent blenders | Short term (≤ 2 years) |

| EV & hybrid uptake in urban taxi fleets | -0.2% | Buenos Aires, Rosario, Córdoba metropolitan areas | Medium term (2-4 years) |

| DJAI-style import licensing uncertainty | -0.3% | National, affecting all import-dependent market participants | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Peso Volatility Inflating Imported Base-Oil Costs

Monthly 2.2% increases in refined-product prices during February 2025 reveal how currency swings feed straight into input costs for blenders reliant on imported Group II+ base stocks and additive packages. Independent players must either absorb margin hits or pass on costs, eroding their price competitiveness against YPF and Shell, which possess integrated or global supply chains. Elevated working-capital needs, with letters of credit often tying up funds for 180 days, limit investment capacity and slow premium-product launches, marginally dampening the Argentina Automotive Engine Oils market.

EV & Hybrid Uptake in Urban Taxi Fleets

Buenos Aires has earmarked 50,000 tariff-free EV and hybrid slots through 2026, specifically targeting taxi and ride-hailing fleets. Although EVs numbered only 1,555 units in 2024, high annual mileage in taxi operations magnifies lubricant displacement per vehicle, posing a focused threat to future demand. Limited charging infrastructure and power-grid constraints confine the phenomenon to metropolitan areas, mitigating its nationwide impact but creating pockets of volume loss in a market otherwise buffered by an aging combustion fleet.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PCMO Dominates Through Fleet Demographics

Passenger Car Motor Oil (PCMO) accounted for 58.78% of the Argentina Automotive Engine Oils market size in 2025, mirroring an 11.2 million-unit passenger-car parc that dwarfs commercial and two-wheeler counts. Increasing OEM demand for API SP and ACEA A5/B5 synthetics is nudging urban consumers toward semi-synthetic 5W-30 grades, though 15W-40 mineral oils remain prevalent in interior provinces due to price sensitivity.

The PCMO segment is also the primary arena for brand competition, with YPF, Shell, and TotalEnergies vying through loyalty programs and bundled services. Marketing pivots on drain interval guarantees and fuel economy claims validated by OEM co-branding. Digital booking apps for YPF Boxes and Shell Helix centers make oil change transactions traceable, enabling data-driven promotions that cement stickiness in the Argentina Automotive Engine Oils market.

Motorcycle Engine Oil (MCO) is growing the fastest, at a 2.32% CAGR, fueled by rising two-wheeler registrations in congestion-prone urban areas and surging last-mile delivery services. Air-cooled engines and wet-clutch systems require JASO-MA2-compliant oils, opening a value window for semi-synthetic 10W-40 grades. Domestic assemblers such as Bajaj and Honda stimulate factory-fill volumes and endorse branded oils at authorized workshops, reinforcing aftermarket pull-through.

By Base Stock: Mineral Oils Maintain Cost-Driven Dominance

Mineral formulations retained 60.95% of the Argentina Automotive Engine Oils market share in 2025, secured by YPF’s captive Group I output and cost-advantaged supply chain. The product continues to dominate rural and value-conscious consumer segments, where price outweighs considerations of drain interval or emissions. Merchandise bundling with fuel purchases at YPF and Shell stations further entrenches mineral grades in mainstream channels.

Synthetics, however, represent the growth frontier, posting a projected 2.55% CAGR as Euro III heavy-duty mandates, extended-drain targets, and OEM specifications converge. Import reliance for Group III base oils introduces currency-driven volatility; however, partnerships between TotalEnergies and Quimiguay on re-refined stocks could help temper cost hurdles over time. Semi-synthetics bridge the gap, blending domestic Group I with imported Group II+ cuts to balance performance with affordability, and are increasingly marketed as “transition” products for fleets upgrading to ACEA E8 or API CK-4 specifications.

Geography Analysis

The Buenos Aires metropolitan area commands a major portion of the Argentina Automotive Engine Oils market, nourished by dense vehicle ownership and proximity to OEM assembly plants such as Toyota’s Zárate and Ford’s Pacheco complexes. Elevated purchasing power and stricter emissions enforcement favor rapid uptake of low-SAPs synthetics, enabling premium pricing strategies.

Córdoba and Rosario corridors form the secondary demand belt, together lifting the combined urban share to nearly 69.70%. These provinces host production clusters for Renault, Volkswagen, and Fiat, driving steady OEM factory-fill volumes and facilitating lubricant supply through established logistics nodes. Service-center footprints are broad, allowing brands like Shell and TotalEnergies to pilot telematics-linked drain programs that upsell high-performance oils.

Interior provinces display divergent dynamics. Agricultural regions in Santa Fe and Entre Ríos align lubricant cycles with planting and harvest seasons, resulting in a spike in demand for 15W-40 heavy-duty mineral oils in tractors and harvesters. Patagonian climates, with temperature swings from -15°C to 40°C, stimulate niche demand for full synthetics capable of cold-start protection. Distribution to these remote areas rewards firms with robust reseller networks, reinforcing the strategic weight of channel management in the Argentina automotive engine oils market.

Competitive Landscape

The Argentina Automotive Engine Oils Market is concentrated.YPF leverages vertical integration, funneling Group I base oils from La Plata into over 380 YPF service sites, a model that secures both supply and point-of-sale dominance. Shell counters by leveraging global R&D and recently clinched a USD 12 million annual factory-fill contract with Toyota, underpinning its Helix Ultra positioning. Competitive fault lines, therefore, extend beyond price or brand equity to encompass technology depth, supply chain resilience, and ESG alignment—key axes shaping future share capture in the Argentine automotive engine oil market.

Argentina Automotive Engine Oils Industry Leaders

TotalEnergies

YPF

BP p.l.c.

Shell plc

Exxon Mobil Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: The FUCHS Group signed a deal to acquire the international LUBCON Group. This move aims to foster joint innovations in high-quality specialty lubrication solutions. Both companies serve as suppliers of engine oils in Argentina. With this acquisition, the FUCHS Group will strengthen its specialty lubrication product portfolio and enhance its competitiveness on the global stage.

- March 2023: Saudi Aramco finalized a USD 2.65 billion deal to acquire Valvoline Inc.'s global products business. This move, executed through a wholly owned subsidiary, propels Aramco closer to its ambition of becoming a leading player in the branded lubricants market, both in Argentina and globally.

Argentina Automotive Engine Oils Market Report Scope

By Product Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

Key Questions Answered in the Report

What is the current volume of the Argentina Automotive Engine Oils market?

The market totals 145.07 million liters in 2026 and is projected to reach 162.16 million liters by 2031.

How fast is demand expected to grow?

Volume is set to expand at a 2.25% CAGR during 2026-2031.

Which product type dominates consumption?

Passenger Car Motor Oil leads with a 58.78% share of 2025 volume.

Why are synthetics gaining traction?

Tightening Euro III emissions rules and longer drain-interval targets are pushing fleets and OEMs toward low-SAPs synthetic oils.

How do import-offset quotas influence lubricant sourcing?

They incentivize automakers to source factory-fill oils locally, favoring domestic blenders like YPF that meet technical and content requirements.

Page last updated on: